ni-co

-

Posts

978 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by ni-co

-

Great blog post that sums up the current situation nicely: http://thefelderreport.com/2015/03/04/why-the-smart-money-is-beginning-to-worry-about-the-downside/

-

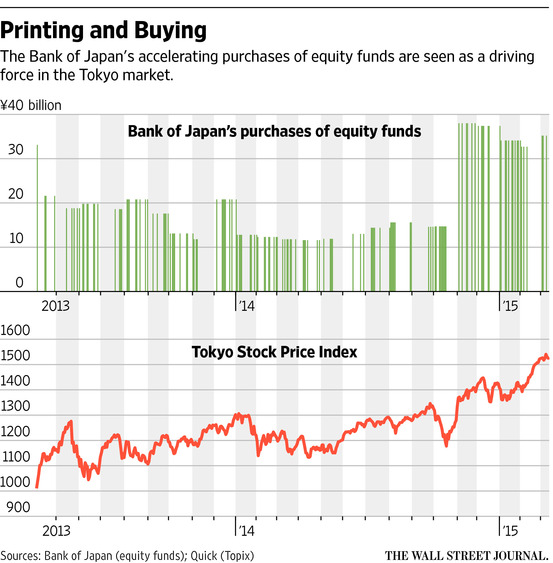

How crazy is this? http://www.wsj.com/articles/forex-market-erupts-on-central-bank-moves-1426773181 [via Google] I didn't know that the BOJ has been buying Japanese stock ETFs – and they want to expand it!

-

The Billion Prices Project shows inflation coming back: http://www.pricestats.com/us-series

-

60 Minutes lead story on Michael Lewis - Flash Boys

ni-co replied to TorontoRaptorsFan's topic in General Discussion

Timely update by Michael Lewis: http://www.vanityfair.com/news/2015/03/michael-lewis-flash-boys-one-year-later -

I completely agree. People could ignore macro, currencies in particular, for the last few years because it didn't really make that much of a difference. There was very low volatility. This has changed in a significant way. As a European investor investing in the US I couldn't ignore EUR/USD but I felt very comfortable with it until last year because the euro didn't seem undervalued no matter how you looked at it. Now I'm forced to make macro decisions – ignoring macro is also a decision, that is to completely give up control. Not only grew macro more important, I think it will be the main driver of nearly every market going forward for the next few years: unwinding carry trades and diverging policies by central banks are so large in size that they significantly overweigh what the "real" world economy is doing (which is close to nothing, momentarily). If we're lucky we will be facing a highly volatile deleveraging phase that will lead to significantly slower growth for a decade or more, if we're not so lucky we will watch the world's central banks screwing up our fiat monetary system. What I simply can't imagine is the next 5 years looking like the last 5.

-

Betting on the Market 1997 Frontline Stock Market Documentary

ni-co replied to berkshire101's topic in General Discussion

At its core, regular index investing (depositing the same amount in a fixed asset allocation of index funds every month) requires you to buy completely blindly of valuation. Historically, when people have bought completely without minding valuation, bad things have happened. But maybe this time will be different? Looking back at the past, asset allocation and rebalancing of market-cap weighted indexes has been the optimal strategy for people living their lives, or at least the people who have been able to stick with it. Completely agree with the first part of your statement – but I doubt that it will be different this time. My 2 cents on it: Think about the most undoubted statement out there: You can never (yes, people really say "never") loose in the long run by buying and holding the index; or – the slightly more conservative variant – by holding 60/40 stocks and bonds. Now think about where stocks are, think about where bonds are and think about how comfortable you'd feel holding 100% cash for a prolonged period (let's say 10 years – when the demographics in the developed countries and China will become really ugly). It doesn't take a lot (e.g. 1-2 decades of deleveraging) to crush this giant bull market. I just can't understand why people don't think about this. In retrospect, there might be a point in time where we will say that the most dangerous thing happening to us was the post 2008 recovery. People stared into the abyss… – and nothing happened. People who bought "the dip" are considered geniuses right now. I bought equities from 2009 on and felt like a genius because I made 30+% returns almost every year; that is until late in 2014 when I finally asked the question: What if we only stopped the clock for a few years by inserting an insane amount of liquidity into the system? I don't think that you can repeat that. There is such complacency out there. I'm afraid that before the end of this decade we're going to see "the death of equities" (with it the "death of indexing") and the "death of derivatives". My best guess is that the coming bear market has to last for so long that people completely loose faith in stocks – like they did in the 1930s; only that this time government bonds (around the world!) look very dangerous, too. -

Betting on the Market 1997 Frontline Stock Market Documentary

ni-co replied to berkshire101's topic in General Discussion

Very much enjoyed it, thanks! And that that bull market kept on going for almost 3 years – crazy. -

Do you think Bitcoin is a safe store of value?

ni-co replied to mikazo's topic in General Discussion

I think this is exactly the right way to think about it. I heard an interview with Raoul Pal where he explained it as an option without expiry date: downside is your invested capital, the upside are millions of today's $ per BTC. This is a very nice risk/reward ratio to speculate just a little bit. There is also a "nice" catalyst in the making: alternatives to the current fiat monetary system (be it gold, Bitcoin or another one) will become a much broader discussed topic in the upcoming months or years. The more QE is done worldwide and the more baby-boomers are retiring, the more this topic will grow in importance. Momentarily, there are still far too much conspiracy theorists leading that discussion (same with gold) – but that's only because Joe Average is either shortsighted or doesn't want to hear about it. Add to this that Bitcoin also has the potential to become a public ledger for owning practically every asset – this is a huge deal which hasn't been discussed much in this thread. -

http://www.valuewalk.com/2015/02/daniel-loeb-oil-investments/

-

For all of these years that I have followed Buffett, Buffett chooses his words VERY, VERY CARFULLY. He would never take shots like he did unless the facts are there to back him up. Read btw the lines of what Buffett said. Do you think Buffett didn't do his homework on David Winters' performance before he spoke up? So what? You could make those statements about the lion's share of active managers - doesn't mean anything about the validity of Winters's complaints about KO. Buffett didn't say this to defend KO's management compensation but to criticize shareholder activists – and especially Winters. Of course this was also a kind of revenge for Winter's making his critique personal and for keep on going after having lost his fight.

-

Classless move. What Winters charges in fees is known up front and voluntarily entered into. Come on. You know that this is just a marketing game. I'd bet you that 90% of his shareholders have neither an idea what he's charging nor that he's underperforming.

-

I don't find it classy though Buffett has a point here. Winters is really the one who made the whole thing personal by bringing up conflict of interest etc. – and then drawing +$20m from his fund's clients/shareholders for long-term underperformance while criticizing KO management for their excess compensation is really throwing bricks in a glass house.

-

Thanks! I believe him when he's saying that he's not speculating with the currency. But I think the weak euro has very much to do with WEB going into offense mode. This is the buying opportunity of a lifetime. If the euro broke apart, he'd have to pay up significantly for assets in Germany.

-

The leading indicator (http://bpp.mit.edu/usa/) seems to be indicating a -1% MoM and YoY. This will be interesting. Take a look at this, it's more current: http://www.pricestats.com/us-series

-

Capital account vs income account and business structure

ni-co replied to cloud's topic in General Discussion

btfd! ::) I think we all should print out and frame this post – it's a perfect sign of our times. -

Yeah, I think this is exactly the question: Are we facing a recession? Or a secular global deleveraging process? I'd agree with you if we were facing a recession but I think it's the latter and we have been facing it since 2008. In 2009, China was able to delay its impact but they thought the rest of the world would have recovered by now. Well, it didn't. I think this is a huge worldwide problem – and now China has to face it, too. The fears people had back in 2009? They weren't irrational. If you think this process through logically you'll come to a point where you have to ask yourself what the markets are going to do when they discover that central banks can only solve liquidity problems but they can't create demand out of thin air (once credit expansion isn't an option anymore). Then what? I think that people like Druckenmiller, Dalio, Bass are absolutely spot on here – Soros has been worrying about it since the 1980s. Do you know any great global macro manager not worrying about this today? I can't think of a single one.

-

I am negative on China mid-term. They have taken on too much debt and they have to delever. I don't think that even the Chinese government would argue with that. Long term I understand your bullish arguments though I'd think there's quite a difference between arguing with work ethics and with potential productivity gains. But what you're talking about is the very long term (20+ years). I'd be very cautious to conclude from Dalio's arguments that China is going to be great for the next 10 years. You never know but I think the probability isn't high. Every debt bubble is slightly different. Brazil has great potential, too and been having it for 50 years but that didn't keep them from having a lost decade. Debt expansion and contraction are very powerful and far more important than productivity gains when you're planning for the shorter to midterm. I don't think that Dalio would argue otherwise.

-

Capital account vs income account and business structure

ni-co replied to cloud's topic in General Discussion

This is called a bull market ;D -

Yadayada, that's almost exactly 1:1 what the mainstream was saying about Japan in the 1980s. Japanese are still known for their work ethics and look what Japan's economy has been doing! EDIT: Sorry, Liberty, I didn't see your post, at first – take this as an agreement with your Japan argument ;D Completely agree with you in seeing the Halo effect at work and also with regard to Germany. I'm old enough to remember that Germany was called "The Sick Man of Europe" and now we're the "hard working Germans" (with a 39-40h workweek and 30 leave days paid in a lot of industries…). Yadayada, it's not that Pettis is saying structural reforms, work ethics etc. are not important! As Pete pointed out, Pettis is saying that the importance of trade and how your economy is structured is completely underestimated and that people are much too focused on issues like work ethics – they are overrated in their relative importance. It's a bit ironical that you accuse him of not taking this into account because the overemphasis of work ethics is exactly one of his major points – and he makes this clear in his books and quite a few articles (s. this for example). +1. Yes, this is a very important point, too, and one that's quite hard to argue with. The same was true for Japan during the 1980s and for Brazil during the 1960s – examples Pettis provides in his China book – both "economic miracles" ending with "lost decades".

-

Shilling didn't say that $10 will be the equilibrium price but that that's how far prices could go temporarily. I think this is possible but I don't know how probable it is. I didn't mean to say that Russia literally stores it for them. But Russia and China have huge oil and gas deals with fixed volume and pricing. Does it really matter in the end, whether the oil and gas is first transported to China and then stored there or whether it stays in the ground in Russia and is only transported when China actually consumes it? Russia is the marginal producer of oil and China the largest marginal consumer. When those countries agree on a lower price – like they did twice last year – this will be the new world price for oil – everything else will be temporarily. US supply has been completely dependent on demand from China meaning that China's genera demand for oil drove the price so far up that shale oil became viable in the first place. Now, China's demand softens and it's completely logical that the oil price drops. But if you think about that mechanism it's also logical that the price will remain low for quite some time if this is indeed the case.

-

1) There'd be great benefits for Italy. They could devalue their currency, inflate away their debt and export more goods to Germany. They'd probably have a domestic investment boom and could thereby get rid of their high unemployment. 2) Seems reasonable to me that they'd want to to peg it to the Yuan. Sooner or later China will want to "merge" HK into China – though that might be some years down the road – and pegging the currencies might be one step towards this goal. On another note, China doesn't seem to intervene directly in the currency markets at the moment because the Yuan is relatively weak. – Though the decision to cut rates is essentially another form of intervention to keep their trade surplus where it is. I don't think that HK will break the peg to the USD. It's really engrained in the HK economy and they are prepared to defend it. I know there's a lot of financial data on this somewhere but I'm a bit busy right now to look it up for you guys. Also to Ni-co's point, the HKD is already kinda pegged to the yuan if you think about it. The yuan is loosely pegged to the USD and HKD is pegged to the USD. Thus transitively the HKD is loosely pegged to the yuan. In regards to Italy exiting the euro. I'm sorry, I don't think they will, and the benefits aren't that big for them. Firstly, they don't need to devalue their currency. Italy is running a trade surplus of 2.3% of GDP, so unit labor costs are competitive. As for debt, yes Italy has high gov debt, but they always had high gov debt. And their public finances are not in that bad a shape. They have a deficit of 2.3% of GDP, but also a primary surplus of 2.2% which is very good. And the deficit should decrease as they roll over debt on lower rates. Furthermore Italy is not very levered. Yes gov debt is high, but has little private debt so as a country they're actually doing pretty good. Where Italy would gain by going off the Euro, is getting their own currency, central bank and monetary policy. That way they could stop bank runs and do some of their own monetary stimulus to bring the economy towards full employment as it looks like the unemployment is due to sluggish domestic demand. But I don't think that Italy would like to endure the bank runs and all that nasty stuff that comes with a Euro exit just to shave 3% off the unemployment rate. The countries that would really benefit from Euro exit are Greece, Portugal, and Spain. In those cases I'm pretty sure that the Euro survives Greece and Portugal, Spain--- I don't know. rb I'm sorry but I completely disagree. In my opinion you are heavily overestimating the power of politics vs. market forces. I think it's quite naive to assume that the USD/HKD or USD/RMB peg is a purely political decision. If there's no other form of rebalancing going on they will be overrun by the markets – as it has always been with such pegs. Don't you think that Italy's banks are perceived to be safer under an implicit ECB guarantee than on a standalone basis? I don't get that argument. Neither do I understand your argument with Italy's surplus. This has been the case since 2013 only. It took ZIRP and massive unemployment in Italy to get to that point. The obvious elephant in the room is that Italy can't devalue in relation to Germany – which is the only really important aspect of breaking the euro apart. Yes, Italy would gain by getting its own monetary policy which was exactly my point. With regard to Italy's private household debt: I think what matters in the end is total debt to GDP ratios – including accounting for retirement claims which no country within the EU does momentarily. From this perspective every country in the EU looks just outright awful. I don't share your optimistic view with regard to the euro staying either. Yes, Spain is a problem but so are Italy and France with their huge debt loads – the absolute numbers matter far more here because what matters in the end is whether markets assume that other countries are even able to somehow counterbalance/shoulder them (and are politically willing to!). In the long term the only way I can see the euro surviving is a United States of Europe scenario – but this doesn't seem to be the most probable case to me.

-

1) There'd be great benefits for Italy. They could devalue their currency, inflate away their debt and export more goods to Germany. They'd probably have a domestic investment boom and could thereby get rid of their high unemployment. 2) Seems reasonable to me that they'd want to to peg it to the Yuan. Sooner or later China will want to "merge" HK into China – though that might be some years down the road – and pegging the currencies might be one step towards this goal. On another note, China doesn't seem to intervene directly in the currency markets at the moment because the Yuan is relatively weak. – Though the decision to cut rates is essentially another form of intervention to keep their trade surplus where it is.

-

Here is an interesting discussion between Wilbur Ross and Gary Shilling about the further development of the oil price and how producers are going to react: http://www.bloomberg.com/news/videos/2015-02-18/opec-playing-game-of-chicken-with-oil-shilling-says Interesting what Ross is pointing out towards the end: at the big oil companies cashflow doesn't cover capex plus dividends.

-

What I tried to say is that China has been stock piling hard commodities (like copper or iron ore) for years and that this was not sustainable. They used it to fuel their synthetic domestic investment boom. It doesn't matter that they don't have storage capacity for oil because they have long term oil and gas agreements with Russia – so Russia is basically storing for them. Now, the Chinese investment spree is over because they aren't able to keep it up and, at the same time, the rest of the world's demand for China's products and/or for commodities hasn't picked up either but rather been slowly declining. Can you imagine what it means when the country that consumes 45% of most important industrial commodities (like copper), which used them for years partly to fuel an unsustainable investment boom and partly to stockpile them, now begins to end this game? It took the world years to ramp up all this commodity production capacity and because of the economics of mining/drilling it will take the world years to reduce them back to where real demand is. Also think about that producing and transporting those hard commodities is very energy intensive. It is highly likely in my opinion that what we are witnessing is only the beginning of a massive, secular decline in commodity consumption (except for food) and therefore prices (because of the lag involved in reducing production capacities). I think this decline will go on for years and most people seem to completely underestimate it. Add to this the energy production boom in the US and you can imagine why Prince Al-Waleed says we will "never" see $100 oil again (though this might be a bit too pessimistic).

-

I think people are a bit too fixated at the supply side because that's what's immediately relevant to the U.S. right now. But look at the way demand for most hard commodities is developing – China has been stock piling them basically since 2009 and the market is telling you that they couldn't keep it up any longer. This is at least as much a demand as a supply story. In my opinion the demand side is even far more important. Oil is hit especially hard because all the increases in supply came at just the wrong time. But that's really more of a distraction.