ni-co

-

Posts

978 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by ni-co

-

Nice, thanks for the link. Note that he is 177% Long and 77% Short, resulting in Net of 100% and Gross of 254%. Will be interesting to watch in choppy market. ;) I don't think this would change anything because of the index-like diversification of these funds (> 400 stocks long and > 400 short). I guess the worst case would be a period like 98/99 with value stocks severely underperforming.

-

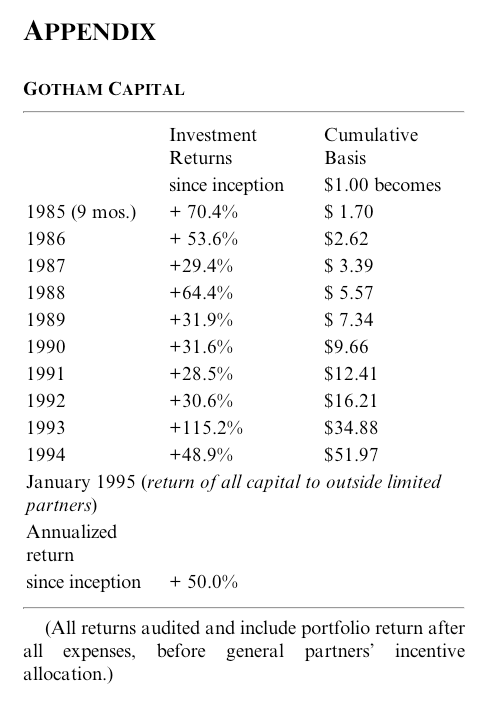

Well that's not quite what he said. He said he would be happy using it, but he things it has one too many factors - i.e. the ROIC calc detracts from performance. You can test it on portfolio123.com (with Compustat data) back to 1999 – it's not that far back but as far as it goes I don't see that he's got a valid point there. At least in my test (1-year rolling periods), the Magic Formula out-performed pure EV/EBITDA or EV/EBIT by about 6% per year. His is hardly the only analysis I've seen, and the data Greenblatt himself talks about is supportive of the statement. I've played around with something like this (as well as other quality factors) and arrived at a similar conclusion. 6% a year BTW is a massive number to outperform EV/EBIT by. Massive. That' would be like almost 10% annualized over the market return. Yes, it's massive. So are the results in Greenblatt's book. Heck, it's only a year but he's very much on track beating the S&P 500 by 10% with his long/short fund: https://www.gothamfunds.com/Funds.aspx?FundID=1

-

Well that's not quite what he said. He said he would be happy using it, but he things it has one too many factors - i.e. the ROIC calc detracts from performance. You can test it on portfolio123.com (with Compustat data) back to 1999 – it's not that far back but as far as it goes I don't see that he's got a valid point there. At least in my test (1-year rolling periods), the Magic Formula out-performed pure EV/EBITDA or EV/EBIT by about 6% per year.

-

Hey, and I thought, I was the only one ;) I think this is a good indicator to keep an eye on over the very long term: http://www.economist.com/content/big-mac-index

-

Great point. Pro-cyclicality is exactly what I meant by "volatile earnings". Yeah! Great point... Except you have not understood I am not suggesting what to do! I don’t care. All I am saying is: know the true value of what you own… because sometimes numbers on the Balance Sheet might not make much sense… That’s all! Gio Ok. Then I really misunderstood you, sorry. Another point: Maybe... But, if I decide to sell my apartment, I will find someone tomorrow morning willing to give 10 times the cost of the underlying land... Because I would not be selling square meters of land, but square meters of an apartment... An apartment in a building that, if depreciated over a 40 years time horizon, would be worth less than zero today! I would guess that this is rarely the case. I don't know Italian law, but at least in Germany by owning an apartment you simultaneously are part of the owners group that commonly owns the underlying land. I guess, over time, this is where the actual value of your apartment comes from.

-

Great point. Pro-cyclicality is exactly what I meant by "volatile earnings".

-

I have never said it is practical… But when the Balance Sheet doesn’t tell you the true value of what you own, you should take notice. Gio, you asked for the reason for not carrying RE at market values on the balance sheet. And that's the simple reason: practicability – there is no other reason. A balance sheet, or any accounting number for that matter, is always a trade-off between "true" value and practicability. Of course you could try to value every single pencil in a company every quarter and reflect that on the balance sheet. But it's highly impractical and error-prone – which, in turn, would cause a lot of volatility in the company's accounted earnings. Accounting for RE simplifies it in two ways. First, you set the purchase price as the initial value of the asset; maybe your purchase was a bargain and its market value is significantly higher – doesn't matter, because you simplify by taking the only number that you can be absolutely sure of: your purchase price. Then, in a second step, you take the length of the average replacement cycle of this asset – here a building – and spread the purchase price out over this time – that's your depreciation. Now you might say: "but my apartment lasts longer than x years" – that's beside the point. On average a building lasts x years and that's the amount of years they will be depreciated. This has nothing to do with maintenance capex. I have never said that buildings are enduring assets. But you're implying it with your statement that you don't see the need to depreciate buildings. Depreciation is not the 1:1 equivalent to capex. This is only a rule of thumb. For buildings it can be severely off base, especially when you replace perfectly functional buildings long before they become unusable – that's what I tried to point out with my skyscrapers example. Because on average buildings are replaced long before they "wear out".

-

Think of the consequences of marking RE to market every year (or every quarter!) – it's simply impractical. Even if it was easy to get a halfway decent estimate of the value, you'd get wildly fluctuating earnings at the companies using this RE to do their business, e.g. retailers. The underlying assumption would be that they could always sell all of their RE anytime, and this doesn't make sense. Look no further than to SHLD if you need an example. Stocks and bonds are as liquid as cash, RE isn't, especially when it's being used by the company to do its business. I don't agree with the notion that buildings are enduring assets. Look around you: Most people don't live in 500 year old buildings. Why not? There wouldn't be any skyscrapers in NYC on the ground of your assumption. It's not about how long things last theoretically but after what amount of time they will actually be replaced on average. It can be perfectly reasonable to tear down a twenty year old skyscraper and build a new one on the same spot, even though, theoretically, the old building could have been used for another 100 years or so.

-

The data is freely available to play with: http://www.econ.yale.edu/~shiller/data.htm Barry Ritholtz has a nice weekend reading list on the whole CAPE ratio discussion: http://www.bloombergview.com/articles/2014-08-22/your-weekend-reading-on-the-cape Especially enjoyed Cliff Asness's take on it: https://www.aqr.com/Portals/1/ResearchPapers/ShillerPECommentary_AQRCliffAsness.pdf

-

I agree. 90% of money managers did not foresee the housing bubble, but many survived by not exposing themselves to the worst of the housing dependent stocks. In other words, you wear a seatbelt not because you forecast an accident, but because you really don't know what will happen. Agreed. Having never read one of Nygren's letters before, I found it to be quite thoughtful and candid, though. Needless to say that I'm in complete agreement with their current thesis on banks.

-

I don't think this is correct. Joel Greenblatt's public track record for the 10 years he had his hedge fund, which did exactly the type of investing he describes in You Can Be a Stock Market Genius, was 50.0% per year gross/40% net of incentive fees. I don't think that Buffett beats this in any 10 year period. Buffett's track record is very long and he is one of the richest people in the world. I don't see Greenblatt putting up a similar performance when he hits Buffett's age. Guys, what is your point? Nobody disputes that Buffett is a great investor. I don't dispute that he may be a better investor than Greenblatt and I know that Greenblatt talks about being Buffettized. And achieving high returns on billions instead of millions is simply another league – it's incomparable. What you can't say, though, is that Buffett has the better track record, when there is no ten year period in which Buffett had better returns than Greenblatt managing similar amounts of money. Saying "spin-offs are bad investments because Buffett is the better investor" just doesn't make any sense. This is especially the case, because Greenblatt's 10 year track record is simply insane and – I know you don't want to hear it – he achieved it by investing in special situations and especially spin-offs. We're talking about the attractiveness of investing in spin-offs after all, aren't we?

-

This reminds me of Isaiah Berlin's essay "The Hedgehog and the Fox" ("The fox knows many things, but the hedgehog knows one big thing.") – I've never understood hedgehogs – and they are dangerous, too.

-

In July, you could have bought VRTV (IP spinoff) for as low as $32.50. It's at $47.25 today. 45% return in just over a month. EGL when it was spun-off from LLL – this worked out great. LE/SHLD – still running (SHLD is several special situations in one stock). Later this year probably LINTA. Lots of activist investments result in spin-offs (e.g. McGraw-Hill or BKN). There are still great opportunities out there.

-

For me Greenblatt, not Buffett, is the authority on this because of his track record in investing in special situations. I don't think this is correct. Joel Greenblatt's public track record for the 10 years he had his hedge fund, which did exactly the type of investing he describes in You Can Be a Stock Market Genius, was 50.0% per year gross/40% net of incentive fees. I don't think that Buffett beats this in any 10 year period.

-

In most cases they exist because the parent companies can't sell them for the right or any price. Sometimes it's simply a way to sell a division tax efficiently. If you want to know whether they work you simply have to look at what John Malone has done for the last decade. Every single one of those Liberty spin-offs did very well. However, not every spin-off works out – they work on average. You have to do your homework. But it's a very good place to start looking for cheap companies and I think this Greenblatt's message.

-

I'm totally the opposite. I feel like by starting out with the set of names a guy like Buffett has been interested in, I'll have a less polluted lake to swim in. It doesn't seem like a good idea to me to ignore his behavior and instead look over every stock in the market and only go with the names that I think are best (instead of peeking at the list of stocks that a few shrewd investors own). I'm aware of his experience and wisdom and... more importantly, mine! +1 A big part of the fun for me is reverse-engineering great investors' buying decisions – and becoming a better investor myself along the way.

-

Agreed, Eric. Sorry, obviously I edited while you posted. Problem is that this works only short term. In the long run it's like fighting gravity. What I'd love to see is more CEOs who even think about tax as a cost for shareholders. John Malone does this and it pays in spades. He'd never pay you a dividend outright, because he thinks it's stupid. And he is right.

-

Yes, there would certainly be a difference unless your costs basis is zero. Example... I buy BAC at $15 -- that's my cost basis. dividend: they pay a $1 dividend. I pay 33% tax on that dividend. I'm left with 67 cents on the dollar. repurchase: Management decides to repurchase $1 of stock for $15. I sell an offsetting amount of shares at $15 price point (same as my cost basis). I'm left with $1 in cash. No taxes whatsoever! I have roughly 50% more cash. With the difference that in case 1 you're left with a stock price of $14 and in this way get $1 of tax free price appreciation (potentially).

-

Exactly. However, you have to factor in capital gains tax for the ownership adjustment after the buyback. If you assume the same tax rate on capital gains and dividends and if you don't want to reinvest the cash, there wouldn't be a difference. Reinvestment is my point, though (and therefore the valuation of the company matters for the buyback). I don't want the company to decide for me when to cash in parts of my ownership. If I wish to have cash, I will sell part of my shares. The standard assumption that for some reason most shareholders want to receive 2% or so of their holdings' worth in cash every year and don't mind paying tax on it just doesn't make any sense. Not even then, because I'd also have to buy at a higher valuation then.

-

whenever I read a report by them, it seems very well thought out and makes a lot of sense. Are there more interesting reports of them floating around out there? Maybe it's also no accident that Michael Mauboussin seemingly feels comfortable at CS.

-

I agree that top notch capital allocation isn't as important in every company, but it's never a bad thing to have. Even a company as focused on products and organic growth as Apple became a better investment for shareholders when they stopped just sitting on their growing cash pile and started doing buybacks, dividends, raising some debt, etc. And I wasn't saying that it's a mistake for most companies to pick internal candidates that might not have capital allocation experience. Life is all about tradeoffs and doing the best with what you have. Especially in tough businesses, having good operations is crucial above all else. But it's still a shame that most companies are not structurally built to foster that kind of talent explicitly (there's a few companies that I like that train their managers to use all kinds of ROIC, cashflow, and capital intensity metrics and tie their compensation to those, and over time that makes them think in very clear real-economic terms that I think does help with company-wide capital allocation). I agree 100%.

-

I don't know if I'd go so far. It's certainly critical to have a good capital allocator at the top of any kind of conglomerate. Normally, though, operations are much more important for a company – you have to collect the cash before you can allocate it, after all. So, I think it makes sense for most companies to choose the salesman, engineer etc. to lead the company. What you want in any case is someone who thinks independently and for the long term. If he does that, he's going to make the right decisions on average – maybe also the right capital allocation decisions – but independent thinkers are very rare at the top of companies they didn't found.

-

But you would certainly agree that paying taxes – which is what I'm talking about – is not on the list of these goals you mentioned? Call me naive but it bothers me to no end that paying a dividend is still the standard capital allocation policy in nearly every large company. This is simply a waste of money. Warren Buffett got me really thinking about this in his 2012 shareholder letter (page 19-21). It just doesn't make any sense, neither short nor long term. I don't think it has anything to do with CEOs being greedy. They just don't think about it. Buffett thinks about, Malone thinks about it – every single CEO in Thornton's Outsiders book thinks about it – but most of the CEOs don't. And what amazes me is that even most of the investors don't.

-

There are two decisions most companies make that I don't understand at all: [*]They pay a dividend instead of investing the money or buying back (undervalued) stock; [*]they optimize for high earnings – which normally get taxed at a high rate – instead of optimizing for cashflow that is immediately reinvested into growth (think John Malone). There is no doubt in my mind that over longer periods of time both decisions have huge detrimental impacts on shareholder value building up within these companies because of the law of compounding. A. Why do they do it? B. Why do shareholders demand it (if this is your answer to A.)?

-

Oh. You should overthink that! I really enjoyed the one with Levitt, too – not from an investor point of view but from a philosophical angle, especially towards the end of the interview. In my opinion, Ritholtz has proven to be a great interviewer in the first four interviews.