John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

ChatGPT : [John, Odense, Denmark, posting!] -

New Pabrai Fund : Pabrai Wagons Fund. Investor Presentation : Link. What do you think?

-

Politico [November 3rd 2023] : Ukraine faces economic crisis without quick EU aid, finance minister warns. 'The country needs Western help from the start of 2024 to fill an estimated $ 29 billion budget gap, Serhiy Marchenko says.' Well, Switzerland recently got away with screwing [at least, so far] CS AT1 bond holders for USD 17 B. **SHRUG**??

-

How much of your capital has you long Bitcoin active [make it cyptocurrency] allocated to this?

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

He is likely addicted to buying more sogo shosha for the borrowed money, too! -

Please mind and check bra straps and dentures!

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Exactly, @gfp, For the unexperienced in accouting, this may perhaps appear complicated, perhaps even counterintuitive. From the complaint itself : I personally read it as if this may be about depreciations on the building element of gas stations, some of them built when King of Clubs was Jack and over the years well maintained by Pilot. It must have been among the largest identifiable tangible assets in the acquisition, if not the largest. -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

What I meant with mentioning my feeling of confusion was related to the fact that the acquisition agreement appears [by the fact that there is an existing dispute] 'non-water proof', thereby leaving loopholes for interpretation and disputes about the understanding of the agreement. Or the filed complaint has no basis or is unreasonable. Mr. Buffett isen't exactly known for playing games with sellers, 'Arnault-style' [think Tiffany], to save a dollar, or more, ref. what @gfp has already said upstream about Mr. Buffetts word and his integrity. -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

I personally think like you, @gfp, I have been back reading the original press release of October 3rd 2017 [ Link ] on the Berkshire website, and I have been wondering if there is any SEC filing related to these three transactions over time, now that Pilot Flying J was privately held [not listed] in the first place? It isen't even in the press release from back then mentioned that NICO is the acquirer. Mr. Buffett isen't exactly a newbie and nowice into such matters, and he is backed by Mr. Hamburg as the inhouse undisputed expert in this stuff. So let's just say I feel confused. - - - o 0 o - - - Edit : No filing there on SEC, as I see things. [Disclaimer : I'm a complete incapable idiot navigating SEC filings.] -

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

Attached is the Pilot complaint, ref. the discussion above. Pilot Corporation v. Greg Abel, Kevin Clayton, Marc Hamburg, Mark Hewett, Scott Thon, Berkshire Hathaway, Inc., National Indemnity Company, and Pilot Travel Centers, LLC, 2023-1068, No. 92889746 (Del..pdf -

If in future the guy or the guys reposible for capital allocation aren't value for the money, capable of the job requirements and start burning through billions of dollars, they should be fired swiftly. If the pressure from the job is umananageable on personal level, the is not for that person, and the person should resign on own initiative. They aren't exactly working pro bono. Weshler and Combs aren't exactly spring rabbits either, and will retire some day, too. The same way the board should do the same with Mr. Buffett if signs appear of he is fading and loosing it, and starts on a spree of huge mistakes. Why on Earth should Berkshire suddenly pay an enormous deferred tax, surfacing, because of sales of stocks, after spending decades building it [the deferred tax]? The capital allocated to public listed stocks is mainly capital in the insurance companies, subject to dividend restrictions, and what may regulatory surplus insurance capital affects the underwriting capacity of the insurance subs. I want more of the same as in the past, I do not want derisking and by that diminishing returns.

-

It's not an elephant dancing, it's a crowd of elephants, dancing!

-

@Whensthepaintdry?, Is your comment above related to Apple or related to Berkshire?

-

Greg [ @Gregmal ], The book I mentioned above by Morgan Housel would actually serve your needs expressed earlier in some other topic here on CoBF by you about how to get your kids on a good path in life, but when your kids are older than now [, which I recall as <=10 years old]. Like late teen years, and in drips. The good path does not start with investing, it starts with saving, and all the math and logic related to the concept of saving.

-

The actuality of this topic seems to be permanent and never fading. If any of my fellow CoBF members has a person in own sphere near and dear to you where you may aware of that particular person with such challenges as to : Managing debt Navigating the financial marketplace Building savings Budgeting I will just say it can be a hard task to open up a such discussion with another person, so please think carefully about how to do it, because it's likely highly sensitive for that other person. Most likely challenges are about several bullets above, because they are interconnected. A way to start could be giving a book gift with some well thought out words delivered together with it : Morgan Housel : The Psychology of Money [ CoBF topic ].

-

He doesn't exactly have the prospects of soft house arrest either. ['Soft house arrest' defined as : 'Your package from FedEx is expected to arrive 8 - 18'.] Using leverage to invest in 'assets' generating no cash flow at all while holding the assets - what could possibly go wrong?

-

Yeah, I've been puzzled lately there is so little information in MSM about what's going on. The most logical explanation : Not much is going on.

-

Tass News Agency Press Release [October 30th 2023] : Nothing can justify bombardments of civilians in <fill in the blanks your self> — Putin. Isen't this person just something very special and truly outstanding - here, hardly holding back tears.

-

Thursday, James Dimon was called by his wife, that he should bring home some toilet paper from work, while the household was running low on it, which - together with other tings - , caused him to decide to sell a bit, which again generated yet another market leg down [you heard it here first] : JPM 8-K [October 27th 2023] : Report of unscheduled material events or corporate event.

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

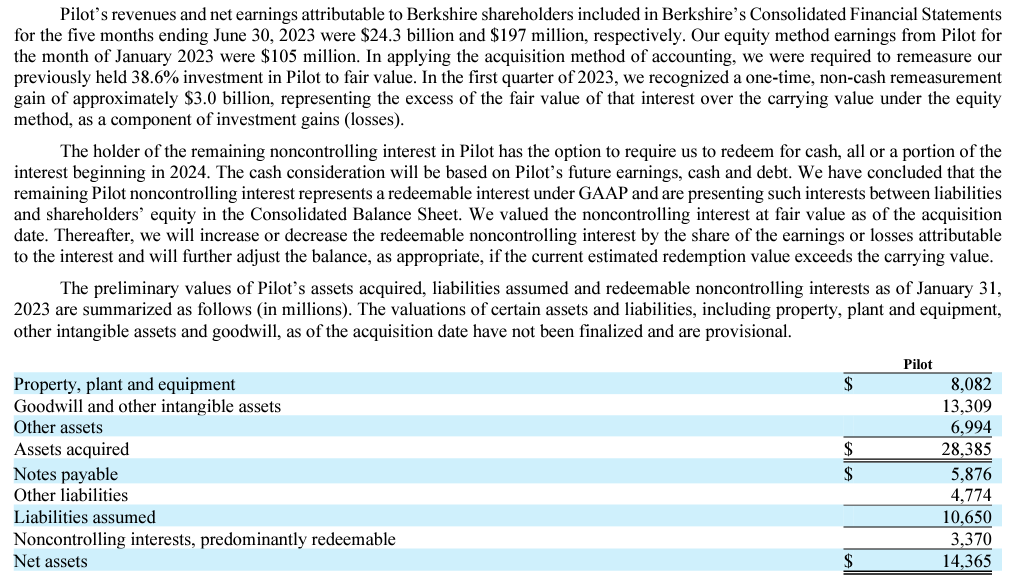

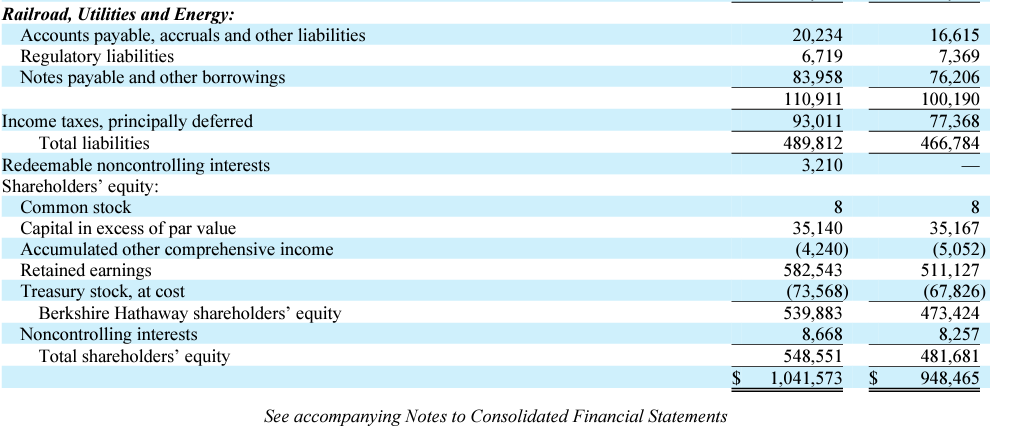

Thank you for sharing your analysis here, @gfp, After spending just a bit of time revisiting this acqusition again, your analysis appears to connect the dots in my opinion to perfection : Stepwise clean-up process. Pilot Company Press Release [April 10th 2023] : Pilot Company welcomes two new executive leaders. For the sake of the proportions of it : From Berkshire 2023Q2 10-K : So the item at hand for dispute is measured at USD 3.370 B end of January 2023 by Berkshire, and we are talking about goodwill and other intangible in total of USD 13.309 B, while the item at dispute at EOP 2023Q2 was measured at USD 3.210 B by Berkshire :

-

YouTube - Bloomberg Originals [October 26th 2023] : Documentaries : RUIN: Money, Ego and Deception at FTX. Better than Netflix, I would say. What a scoundrel, hack, distance aperture and empty suit [, while in T-shirt and shorts]. Just a wicked thief. My class teacher in high school sometimes used the term and talked about 'rich people's stupid and dumb children'.

-

I still don't get it. And I won't. Novo Nordisk A/S CEO Lars Fruergård Jørgensen is totally zipped in his public communication. Ely Lilly doesen't [even] have an approved product [in any country] yet. In short, please get real and please make up your own mind, based on your own work on fundamentals, not this rubbish and *BS* about the behavior of sell-side analysts, downgrading, tailwinds, adversily affected ownership, combined with statements about a lot of stocks will become ridicously expensive, while the others wll be [reasonably] cheap.

-

What makes you think this is important?

-

KAL's cartoon October 21st 2023 :

-

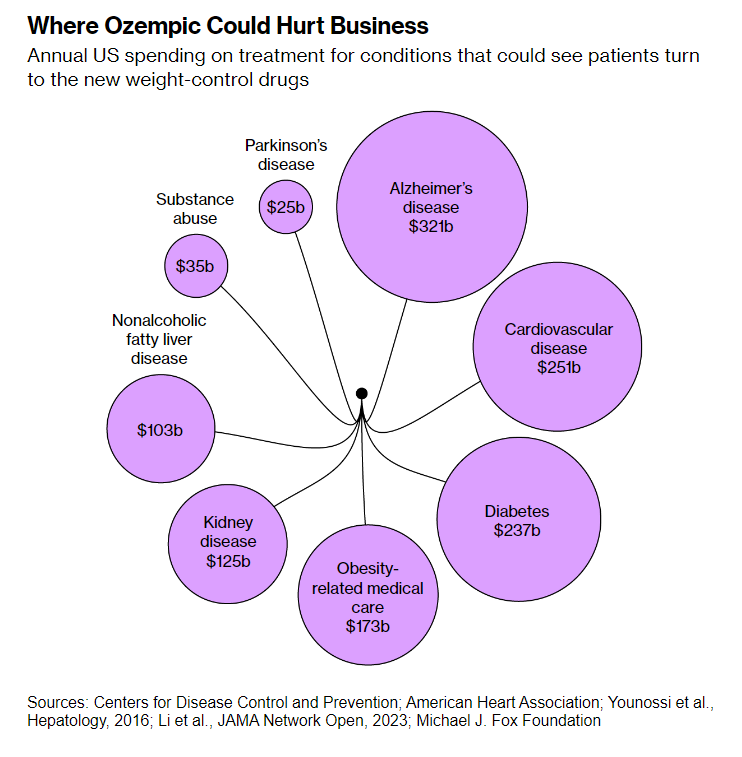

To me personally, this has gone totally overboard in the MSM, and likely much of it highly speculative, simply because the speculations are undocumented and not founded in realia. - - - o 0 o - - - Here is one of the latest ones : Bloomberg BusinessWeek [October 18th 2023] : The Ozempic Effect Is Coming for Everything From Kidney to Heart Disease Treatments. It appears and looks realiable and trustworthy on surface, and contains a lot of links to 'socalled sources'. These sources are - most of them [- I haven't checked them all, so can't say for sure it's all of them - ] are other Bloomberg articles, released earlier on the matter or about adjacent topics. Then you can check the sources in the underlying 'source'-articles, and you find other yet earlier Bloomberg articles as sources, that also do not contain any factual news or information about it from an outside Bloomberg source with some professional credibility. Then you start scratching the top of your head, asking your self : "Where did it actually come from?", going back / returning to article that linked to that particular place, and you realize that there aren't any links to or specific guide to basis for the written statements in the article for its central statements, generating the actual headline of the article. [<- Translation : WTF?!] Journalism at its finest. - - - o 0 o - - - The article is partly subscription protected, and contains this [, which I don't know what to think about - also thinking Novo Nordisk and Eli Lilly should focus on ramping up on production capacity and on work for approval, instead of 'chasing everything'] :