Phaceliacapital

-

Posts

1,004 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by Phaceliacapital

-

-

-

Marlin, you have quite the life experience it seems!

-

I was kidding, sorry, maybe a message board is not the ideal place for sarcasm..

-

Oh so you were the one who took Stephanie with him to his hotel room!!

-

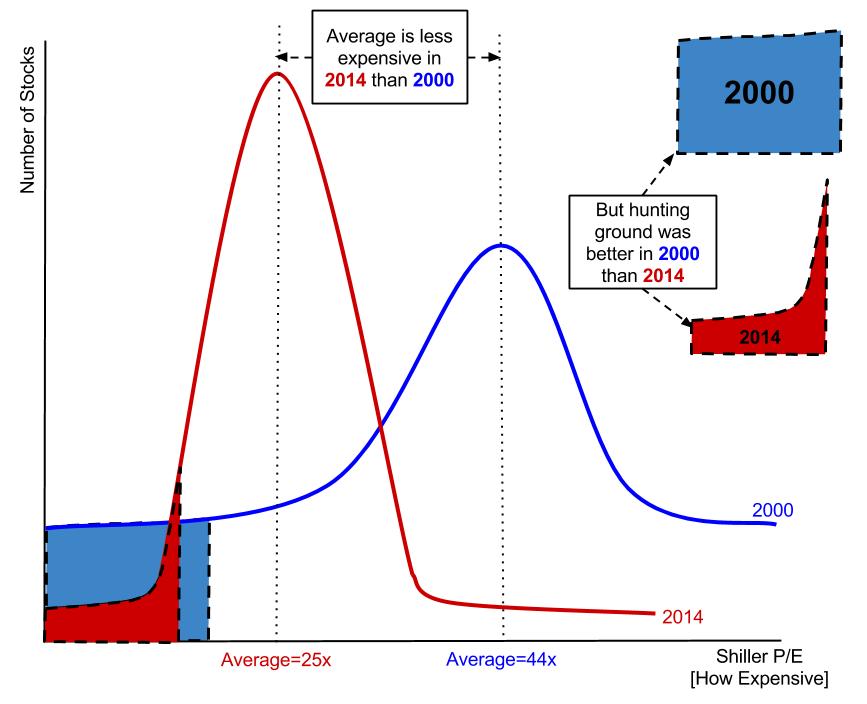

He makes the case that it isn't the same:

http://ftalphaville.ft.com/2014/04/01/1817912/hello-alphaville-this-is-rock-n-roll/

http://ftalphaville.ft.com/files/2014/04/Deutsche-on-state-controlled-1-272x421.png

-

Smith argues Russia deserves a frontier market status, or a class of its own, not because of geopolitical risk. Rather, Russia faces a broad-based corporate governance issue: Enterprises forgo corporate profits at the bidding of the politicians.

-

Carnival.

I thought Morningstar had calculated that it takes an average of 18 months to wash out reputational blunders.

-

Regarding Gazprom, it's not a good company to invest in because it's Putin's "playground" and he raises/lowers prices whenever he wants.. However, it's fair to assume that he will always target good overall profitability, right?

So as a shareholder, does this really impact us? Is it not more the case of having a company that either makes some money, or a shitload of money?

If you look at Gazprom's position, it's incredible, right?

1) Their proven gas reserves are 10x (!!) ExxonMobils and PetroChina (fun fact, they're 30x Lukoils)

2) Their total pipelines length is 168 thousand km! (including a shitload of compressor stations, distribution stations etc etc). How do you replace this?

-

CTC is currently yielding a 11% FCF yield and +/- 8% dividend yield.

-

The only leasing I am familiar with is Aircraft leasing. For air leasing the age and models of the aircrafts can be a moat. Many airlines are not interested in leasing an old 737-400 when they can lease a larger, more fuel efficient 737 800 or 900. The make and model is very important to airlines as well. For instance, Southwest only uses Boeing 737's. Management and size is very important as well. A smaller leasor is not going to have the clout to order 125 Boeing aircraft on credit necessary to fill big contracts.

Yeah but the planes in portfolio are chosen by management right?

-

I think this was posted in another thread but can't find it so credits go to original poster:

I thought the following findings were insightful:

Would love to see this analysis from a EV/FCF and/or ROIC perspective.

-

Wondering the same thing!

-

I think most of the moat comes from the capital allocation skills from the management.

-

c'mon man, this is a value investor forum - a lot of us do this for a living and almost every other waking hour of the day. Aviation enthusiasts are often into simulators. Investment enthusiasts spend the weekend devouring annual reports. To each their own. Even rookie F1 drivers use simulators/games to learn tracks they've never driven.

well if your job is flying a plane, i would think that you would be sick of it after work. So why continue in your basement?

The simulator thing, in and of itself, does not overly concern me, based on a couple of observations. 1) My next door neighbor is a commercial pilot. He has a number of books about airplanes, photo books like "Chicago from the air", and, in the eight years I've known him, looks up at every airplane that comes overhead...every single time. 2) I bartended at a hotel years ago. We had a number of Rail Road employees (Soo Line for those who are interested) who would stay there. It was remarkable....after an 8 hour day they would come to the bar and, for 6 hours, drink beer (not excessively, mind you) and talk about trains, the entire time, day after day. Many of these guys have elaborate model trains in their homes.

Exactly, one of my friends is a pilot and he is sincerely disappointed if he sees a plane but it is too far off to see what type it is..

-

-

From the other thread:

Thanks,

I always do this using Word, you just copy the two files you want to compare into two word files and use the compare function. So should you ever want to do this when not connected to the internet, you can do it this way.

-

I used it a couple of years ago but quit after a while, for no particular reason now that I think of it

-

I am arriving the 7th, and staying at the Intercontinental Toronto Centre hotel!

-

Another option is to click the "print" button. You will see it in a thread...just below the last post of the page. This puts the entire thread into one page.

Are you kidding me?! I put the entire Fiat thread in a word document to read it over the weekend a few months ago. Thanks! I feel a little stupid for never looking for a print all button earlier...

:D

-

Yes, only US equities list there.

It has been rumored on many occasions (but never confirmed) that Fiat is one of Pabrai's multibaggers, along with ZINC.

Guy Spier is also invested in Fiat.

-

BN) Billionaire Ross to Sell Part of Stake in Bank of Ireland

+------------------------------------------------------------------------------+

Billionaire Ross to Sell Part of Stake in Bank of Ireland

2014-03-04 08:08:31.841 GMT

By Dara Doyle

March 4 (Bloomberg) -- Wilbur Ross, the U.S. billionaire investor in struggling industries, is selling a portion of his stake in Bank of Ireland Plc, after the value of his investment more than trebled. The bank’s shares fell in Dublin trading.

Deutsche Bank AG said in an e-mail today it’s acting as a placing agent of “an accelerated bookbuilding to institutional investors” of about 2 billion Bank of Ireland shares on behalf of Wilbur Ross and Fairfax Financial Holdings Ltd. That’s 6.4 percent of the Dublin-based bank, Deutsche Bank said. Davy, Ireland’s largest securities firm, is also placing the shares.

“Given the appreciation in the bank’s share price and its current premium valuation, we are not surprised to see some of the original North American anchor investors move to take some cash off the table,” said Ciaran Callaghan, an analyst at Dublin-based Merrion Capital. “In some sense, they have done their job and made their return.

In 2011, WL Ross & Co. was part of a group of investors that paid about 1.1 euros ($1.5 billion) for a 34.9 percent stake in the lender. The invetsors paid 10 cent a share. The lender lost 490 million euros last year, its loss narrowing 73 percent from a year earlier. Bank of Ireland is now trading profitably and generating capital, Chief Executive Officer Richie Boucher said yesterday.

Bank of Ireland dropped 4.9 percent to 34 euro cents as of

8:02 a.m. in Dublin trading.

Pat Farrell, a spokesman for the bank, declined to comment on any sale of shares.

-

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/0dc7b03c-992e-11e3-b3a2-00144feab7de.html#ixzz2uT8QS800

For an Asian agribusiness that spent its first two decades impressing western rivals Cargill and Archer Daniels Midland with breathtaking rates of growth, the past two years have been anything but smooth for Wilmar.

The Singapore-listed company, the world’s biggest producer of palm oil, a key ingredient in processed food, has seen its share price fall by 44 per cent, making it the worst performer in the Straits Times index and dragging its market capitalisation down to about US$17bn.

By the numbers: Wilmar

By the numbers: Wilmar

Revenue exposure, debt and profit before tax

More

ON THIS STORY

Wilmar commits to ‘sustainable’ palm oil

Comment Wilmar joins the sugar big league

Wilmar falls more than 10% after profits drop

Wilmar to deepen investment in Africa

ON THIS TOPIC

Slow farmer corn sales hit trader profits

Australian drought bites into beef trade

Key Wilmar partner provides western link

Coffee jumps 10% on fund buying

IN BASIC RESOURCES

Stemcor to restructure $1.3bn debt

Alcoa closes key smelter in Australia

ThyssenKrupp edges closer to recovery

Tata Steel profit raises turnround hope

But there are signs that Wilmar could be on the mend, just as the fortunes of fellow Asian agribusiness, Singapore-listed Olam, are also starting to recover after the company’s bruising battle last year with US shortseller Muddy Waters.

Investors had fretted over the one thing that helped drive Wilmar’s growth for years: China.

Kuok Khoon Hong, Wilmar’s co-founder and a nephew of Robert Kuok, the billionaire Malaysian entrepreneur, pushed into the country in the 1990s, setting up soyabean processing plants. He was betting that the growth of China’s middle class would spur demand for protein-based foods such as meat, and hence demand for the soyabean meal fed to cattle and pigs.

That bet paid off handsomely for years, until an aggressive expansion by China’s state-owned processors caused overcapacity, squeezing soyabean margins.

Now, that business appears to be recovering as capacity growth has been “more disciplined” across the industry, Standard Chartered says. Earnings last week showed Wilmar’s oilseeds division posted its sixth consecutive quarter of profits, with pre-tax profit in the three months to December of $116m. That helped drive a 5 per cent rise in group net profit for the year to $1.32bn.

Shares in Wilmar were up 2.6 per cent at S$3.48 at midday on Tuesday.

The recovery in oilseeds was also reflected in the earnings of Noble Group, a rival Singapore-listed agribusiness, which on Friday highlighted “better crush margins in China”.

Mr Kuok remains bullish on China even though the pace of its economic growth has moderated. “Every time there is a bearish [research report] on China . . . our share price will drop. But in all our businesses we have volume and margin growth and we are becoming stronger against competitors. So maybe this slowdown is good for us,” he says.

Yet Wilmar’s recovery has as much to do with expansion beyond China. The company is pushing into palm oil and edible oils in Africa, where it made its first investment in 2007 and where lower mortality rates and greater spending power are creating a new consumer class, according to Mr Kuok.

Wilmar also has been muscling into sugar, a business long dominated by Cargill, ED & F Man, Sucres & Denrées and Dreyfus. It made its first acquisition in 2010, buying Australian sugar company Sucrogen.

Key Wilmar partner provides western link

Wilmar’s business empire may have its roots in Asia but its largest single shareholder after the Kuok family is firmly planted in the vast agricultural plains of the US Midwest: Archer Daniels Midland.

The US agribusiness has a 17 per cent stake and was a key partner for Wilmar as the two expanded in China in the 1990s. Speculation persists that they may eventually combine.

Continue reading

Last week, Wilmar entered India, the world’s second-largest sugar producer, with a $200m investment in a sugar joint venture with Shree Renuka. The Indian group also has 100,000 hectares of sugar cane in Brazil, the world’s largest sugar exporter, which Wilmar sees as complementary to its Indian investment.

Sugar now accounts for 7 per cent of group pre-tax profits, while oilseeds has shrunk to account for 13 per cent, from 26 per cent in 2009.

“If you aggregate all the operations excluding the China soyabean business they have been steadily increasing their profit contribution. And those businesses are generally higher-return businesses,” says Adrian Foulger, head of soft commodities research at Standard Chartered.

At the group level Wilmar has managed to boost net cash flow by 52 per cent year-on-year, after reining in capital expenditure. That fell to $1.4bn in 2013 from $1.7bn the previous year and this year should be “somewhere around $1bn”, says Ho Kiam Kong, chief financial officer.

Yet Wilmar cannot take all the credit. Some of its improved performance is due to structural changes beyond its control, as the moderating capacity in Chinese crushing shows, and shifts in market behaviour.

Ephrem Ravi, analyst at Barclays, says that while the sugar acquisitions have been “a milestone in terms of operational and geographical distribution”, the seasonality of the crop inevitably will mean earnings volatility.

In palm oil refining, which accounts for 48 per cent of group pre-tax profit, Wilmar is facing tougher competition from refiners in Indonesia adding capacity to take advantage of government tax incentives aimed at developing local industry. Wilmar’s refining margins shrank in the fourth quarter.

The company has managed to offset that partially by expanding into higher-margin areas such as oleochemicals and speciality fats.

However, Conrad Werner of Macquarie Securities warns: “We see [crude palm oil] margins as the more important fundamental driver for Wilmar and are cautious on them [amid] rising competition.”

-

Nobody has a huge edge in operating ships. The shipping industry is largely about timing the cycles in pricing. The market for newbuilds and old ships is somewhat liquid; I don't think that anybody really gets a really good deal on ships. The assets aren't that difficult to value for those working in the industry.

I wouldn't necessarily agree with that statement, I think that those shipping titans that were born and raised in the shipping industry (for a quick summary, those mentioned in Dynasties of the Sea) are significantly more capable to assess the value of a ship than those private equity players/hedge funds that are entering the industry as they are starving for yield.

-

Viking Raid

in Books

Read it in two sessions, don't know if I agree with the plot twist but it was amusing nonetheless. You definitely notice the difference in the two books in that the author is really trying to educate the reader. Great read.

Learning from Michael Burry

in General Discussion

Posted

He has a "G7" fund, don't know what it's for..