thepupil

-

Posts

5,004 -

Joined

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by thepupil

-

they are very different. a 10 yr bond at 5% yield ($100 with 5% coupon) loses 8% in price if the required return goes up by 1% and will make 5 points of coupon, so in a 12 month period loses 3% on a total return basis. A 1 or 2 or 5 year bonds (or floating rate) has even less risk of nominal loss. CLO AAA right now has no duration and lost like 3% in MArch 2020 and in Summer 2022. A mediocre company at 20x EPS growing 6% / yr and using all its cash to do so loses 20% if required rate of return goes up by 1%. stocks are far longer duration investments and subject to much greater changes in value upon multiple changes. it's intellectually consistent to prefer bonds to stocks in a rising rate/high inflation,decreasing valuation environment. bonds have generally greater degrees of coupon to reinvest and are lower in duration. they also get paid first. so if you're worried about margins, preferring bonds also makes sense. I don't think it's ironic at all. of course over LONGER term time horizons, stocks will kick bonds ass in most cases over most but not all long term (defined as 10+ years) time horizons.. We all have different time horizons. if you told me inflation was going to be 8% over the next five years and everything else will be the same, I'd increase my allocation to bonds/cash versus stocks/RE.

-

https://www.cmegroup.com/markets/interest-rates/stirs/eurodollar.html I think what you’re looking for is futures and options on futures related to short term FI. they are accessible to the everyday Joe on interactive brokers. I have never traded them in a personal or prod context, therefore don’t want to provide any more specifics, but if you want the purest form of short term rate speculation, it’s somewhere in there.

-

Can you show the data to support this? I love my bones and duration more than most but this doesn’t strike me as true (though I couldn’t find a good index for this type of thing that went that far back…and the 30 year tsy didn’t exist for the entirety)

-

PE backed companies w/ floating rate debt and certain RE borrowers will absolutely care. I do think an extended period of 4%+ short term rates (and 7-8% all in 1st lien rates and more for worse credits) should hurt more than a few levered borrowers. Feel like we haven't seen that stuff play out yet. Note this isn't a "stock market" view. Because anyone who has actually looked at the "stock market" knows that it is mostly comprised of extremely high credit quality companies and not a bunch of levered floating rate borrowers. I'm more just pointing out that extended periods of "high" short term rates brings about real pain for a select few. For me it brings about safe carry/yield.

-

congrats! true conviction!

-

you buying the stock...or did you actually buy property in JOE land.

-

Just to try to put some rough numbers on it. Let's say you expect a portfolio of stocks to make 8% nominal over the next 20 years. if cash/bonds/whatever bonds yield 1.5%, putting 30% of your money in that stuff, leads to having 31% less money in 20 years (this assumes no monetary benefit from rebalancing/decrease in volatility). That's the equation everyone did when deciding to be 100% stocks. if the safe stuff yields 5.5%, then having 30% of your money in that stuff leads to having 13% less money in 20 years (this assumes no monetary benefit from rebalancing/decrease in volatility). If you assume just a teensy bit of benefit from rebalancing, then the drag becomes even less. If I can get 90%+ there with <70% of the gyrations, it becomes more interesting to me to own some cash/fixed income etc. The events of the past year have made bonds/cash/spread products great again and decreased the opportunity cost of holding them substantially. Of course it's different if you're a baller and can maker 15% (or more or whatever) nominal on your risk assets. then carrying 30% in cash/bonds/safe stuff at 5.5% is going to lead to you having 40% less money than being fully invested.

-

CLOA is Blackrock's new one, but only has a market cap of $30mm right now. I own JAAA which has a market cap of $2B and a fee of 0.26%. So CLO AAA Index yields 5.5%, minus 0.26% fees minus 0.25% for shits and gigs (who knows if there's some reason you don't get the exact index yield) = 5.0% floating rate yield. Not bad parking spot. Important to keep in mind for taxable though that it's state taxable so that may take away bulk of the advantage over a 2 yr note. https://www.janushenderson.com/en-us/advisor/product/jaaa-aaa-clo-etf/

-

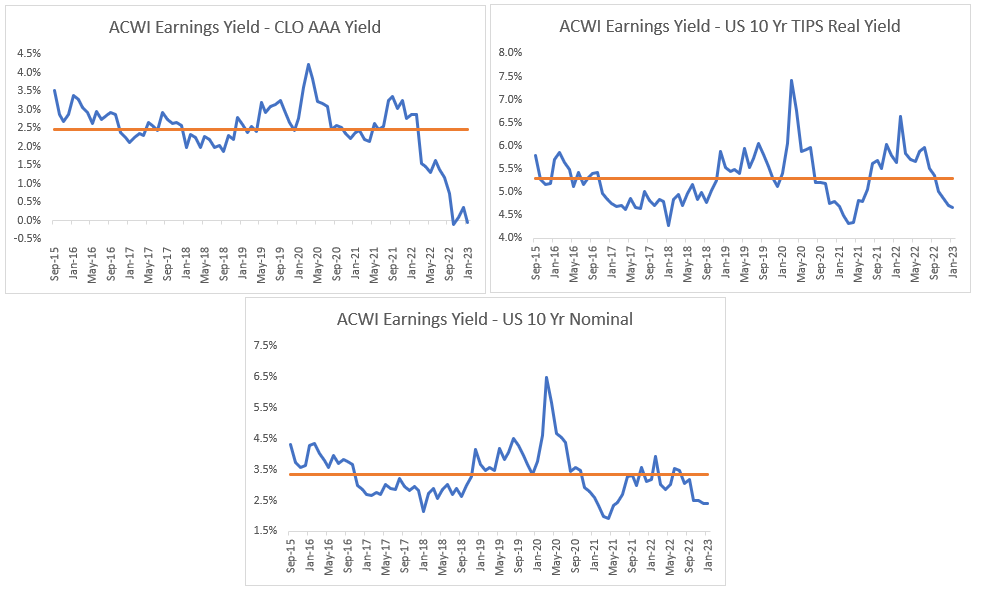

I tend to avoid the macro threads, but I'll contribute this as my overall view re stocks vs other alternatives. The global stock market trades for a reasonable P/E and offers an earnings yield of approximately 6% which is about in line to slightly higher than the past 20 or so years. I think the past year or so took a fair bit (potentially not all) of the excess valuation out of the stock market. Below are charts that show the global stock market's earnings yield vs CLO AAA yield, 10 yr TIPS, and 10 yr Nominals over the last 8 years or so (I went back as far as there was data for CLO AAA). You can do the 10 yr govvy one for a far longer period. It will show very high risk preems in the early '10's and very low ones in the late 90's / etc. Despite a de-rating over the last 12 months, the global stock market yields a below average amount relative to risk free bonds over the last 8 years or so, but not crazily so. We're talking an equity risk premium of 240 bps vs 330 bps (using the nominal 10 year) or 470 bps vs 530 bps (using the 10 yr TIP). The stock market is moderately more expensive than it has been because rates have gone up. What is most stark (and illustrated in the top left graph) is that one can invest in 2-3 year "risk free" floating rate securities (CLO AAA) and earn a yield in line with that of the global stock market's earnings. This is what's most unusual. The return on cash and short to intermediate duration spread products is unusually high relative to the stock market. By this metric the stock market looks very expensive relative to the most recent past. So for me from a valuation perspective, you have to choose your risk. You can choose to hide out in short term stuff and earn an equity like earnings yield BUT take lots of reinvestment risk, because the second rates/spreads fall you're just gonna have cash/whatever yielding 1-3% and not have made any money. Or you can choose to invest in stocks/risk assets and bear the risks of declines in earnings/valuations. If we saw very low risk premiums against the longer terms FI (which was happening last fall, for example when you could buy 20 yr Phillip Morris bonds for 7.5% for a hot second), I'd be more bearish of equity risk and more inclined to put even more incremental $$$ to bonds/FI. I for one love that you can get decent cash yield in low risk stuff these days. It's great. Probably won't last forever. it's a nice tool to have in the toolkit though. Carrying 5-10-20% cash is less costly today than it was 1-2 years ago. this is a boon to conservative savers. It's also a bit of a zero sum phenomenon. Conservative floating rate lenders are sucking up earnings power / taking greater percent of pie than they were. Just ask RE guys w/ 3 yr floating rate debt or PE guys w/ 5-6 yr floating rate debt. for now there's a pretty giant sucking sound in favor of the lenders. And of course you can buy individual stocks and stuff and ignore overall market levels, but I think about this stuff in part because own assets that only have index options and for other reasons as well. EDIT: Overall, I'm more conservatively positioned than I was to begin 2022. I didn't make/lose much money and took the opportunity to earn a little more in AAA, bonds, etc by shifting a little more toward that stuff. I'm still ~80% long. All incremental $'s still flowing to fixed income via 401k but probably stop soon. Also some personal matters at play. I'm not super bulled or beared up and don't see clear reasons to be either.

-

I don't know if I agree with this (well i agree with it, but don't really see any other way/don't fault mgt for it). The bigs (CVX and XOM) do tend to ramp up buybacks when times are good / stocks are high, but that's really the only time they can. Simply too capital intensive of a business to invest heavily in megaprojects AND buy back loads of stock and pay a consistent and substantial divvy, all concurrently. It puts it on the shareholder to choose when to monetize the buyback, which is when times are good. It's not like they're hoarding. They've paid out 130%+ of FCF over the last decade. they just smooth the capital return w/ the divvy and then buy back more when the money gushes (at least from the cheap seats) 2012-2022 $305B of OCF $222B of Capex $82B of Free cash flow $94B of divvies $18B of buybaks $112B of capital return 136% of FCF returned to shareholders Net debt went from about -$10B to +$10B. It doesn' all match up perfectly, but kind of ties. I mean they could be more countercyclical w/ buybacks if they got rid of the dividend, but there's decades of shareholder culture/expectation to fight with that path / would probably derate the stock/increase cost of capital. https://twitter.com/thepupil11/status/1601700941887328256?s=20&t=R5-yUabl16638PZJpW1iWw

-

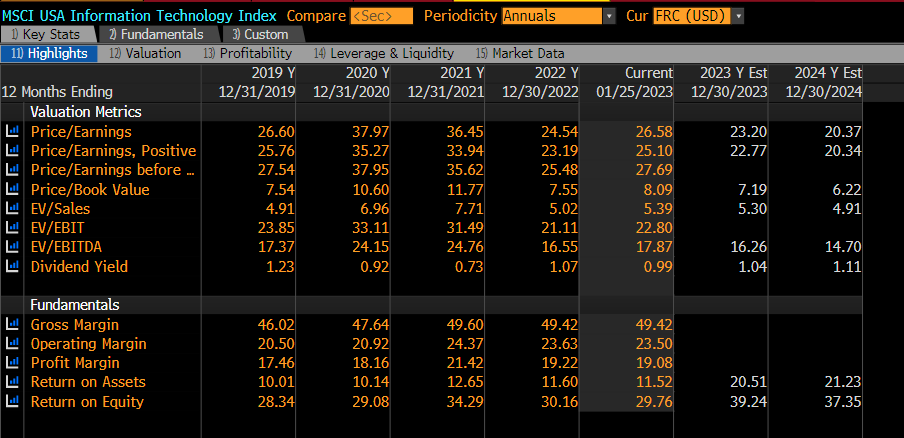

without expressing a strong view as to whether or not "tech stocks" are dead, I would like to take this opportunity to point out that "tech stocks" as defined by the MSCI USA Technology index do in fact make lots of money.

-

I mean I only have my small circle of data points which are similar to @Dinar. We gave our nanny 4% raise and $1,500 cash bonus. she was happy. I got a 5-6% base raise (company was 4%). My wife's in medical field...medicare/insurance payors not reimbursing at any higher rate. lots of goods inflation coming down rapidly. housing/rents cooling, energy prices falling. shortage at like restaurants and stuff will abate as the layoffs pick up / and eventually things like restaurant prices will moderate. friends in tech w/ concentrated portfolios from SBC's have seen lots of wealth destruction (but seem to still be doing okay) I don't really see any crazy runaway inflation in real life (though own some things that would certainly benefit therefrom). I worry more about deflation/hard landing than inflation. I can handle moderate inflation. Just means a little derate and / bad returns. Deflation impairs capital and causes destruction (obviously at a point inflation does too). but generally my macro stance is "should i be 85% long or 105% long". so I'm a permabull.

-

agreed. lots of very similar data points. 2023's raise is you get to keep your job.

-

Dividends vs Buybacks, why not more Buybacks?

thepupil replied to Luke's topic in General Discussion

the shareholder gets to decide what to do with the increase in proportionate ownership which occurs with share repurchases (at any price, "good" or "bad"). BBY Shareholders who sold into the repo to maintain their stake, realized the share repurchases as a dividend. I wouldn't say buybacks are universally better (they are the same), but in a united states context, buybacks are almost always more more tax efficient. For a $1 of pretax corporate income a dividend realizes $0.2 of corporate tax (20%) $0.08-$0.25+ of individual tax For me personally $1 of pretax income distributed via divvy becomes about $0.56 of post tax income via the combo of corporate, state, federal taxes. If the corporation repurchases, the tax is deferred until when i want to create a dividend via sale of stock (which I may be able to offset with losses or push to a low income year etc). The share repurchase leaves the shareholder in control of choosing if/when to realize the individual tax and in the event one's basis is equal or > current price. the share sale may not trigger tax For a retired couple w/o much W2 / ordinaryh income, there's a pretty generous exemption for qualified divvies, so that type is more ambivalent b/w the two forms of capital return. Likewise IRA money is completely indifferent. -

Dividends vs Buybacks, why not more Buybacks?

thepupil replied to Luke's topic in General Discussion

yes the company is “forcing” the shareholder to realize a sale in order to take the repurchase as a “dividend”, but that doesn’t necessarily mean it will result in a capital gain because the shareholder’s basis could be higher than the current price. This is another tax efficiency thing that favors share repurchases. Your basis may be higher or close to current share price so there are instances where creating divvies via sales of repurchases doesn’t realize any tax. if the company pays a dividend, then shareholder must deal with tax consequences of that too. a dividend and share repurchase are the same thing. I like @SHDL’s point that various market dynamics may affect valuation differently b/w the two in the real world, but theoretically there’s no real difference and the capital allocation decision is in the shareholder’s hands. They just start with a different default decision. Share repurchase make the default reinvestment (the company has made the decision to reinvest for you and you must reverse it to take a dividend). Dividends make the default decision to take cash out (and you must reverse it to reinvest). -

Dividends vs Buybacks, why not more Buybacks?

thepupil replied to Luke's topic in General Discussion

with the caveat that this is a bit overly theoretical, I actually think that the responsibility ALWAYS rests upon the shareholder to decide what to do with capital return. I don't believe there are good/bad share repurchase prices and don't blame companies for buying back stock at "too high" prices. It is simply a capital return and shareholders make the decision to either "reinvest" [by not selling the amount of shares equal to the repo] or "take the distribution" by selling enough shares to maintain constant ownership. Likewise with dividends. The shareholder must choose to buy more shares (creating own buyback) or to divert the capital elsewhere (expenses/other investments). I think most people think that the shareholder only gets to decide if the company pays a dividned. But that's not true IMO. The shareholder decides every day whether he buys/sells the stock and he can decide to create a dividend when shares are repo'd (or not). Generally I have a bias toward companies which return capital to shareholders (what is the point of a company if not to pay its owners?), and a bias against reinvesting all of that back into those same companies. Instead, I like to buy other investments because dividend reinvestment (and continuing to hold share repurchasers blindly) is effectively doubling down on those companies. the world is uncertain and in most cases, I want capital return to derisk and diversify me over time. -

Dividends vs Buybacks, why not more Buybacks?

thepupil replied to Luke's topic in General Discussion

that's the theory, practically I want everything in my taxable account to buy back stock, and everything in my IRA's to pay dividends (though can always create divvy via sale). -

Dividends vs Buybacks, why not more Buybacks?

thepupil replied to Luke's topic in General Discussion

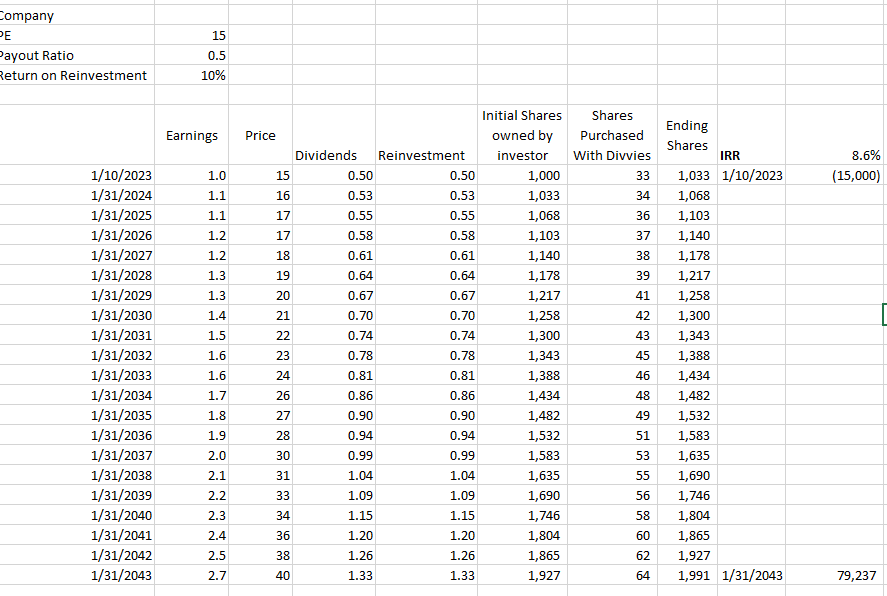

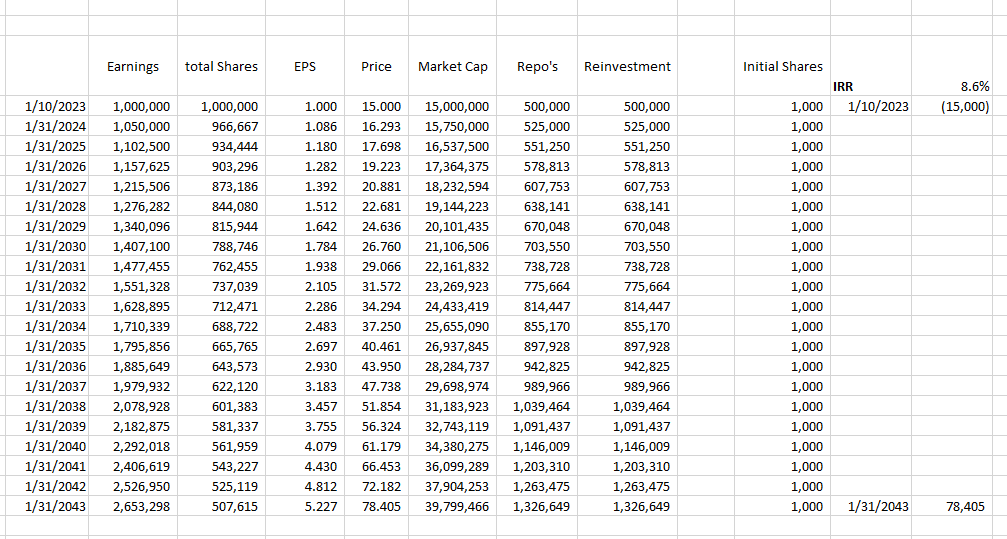

in short, they are the same thing (except for tax treatment which for US taxable investors favors buybacks). Company A distributes 50% of earnings in form of dividend and earns 10% on reinvested earnings. Company A is purchased for 15x earnings / 3.3% yield. It grows by 5% / yr and is exited at 15x earnings. Dividends are reinvested. Sold in 20 years. For a nontaxable holder: Investor makes 8.6% IRR Company B is same company but repo's instead of divvy. Same assumptions (excuse the quick and ugly spreadsheet). 8.6% IRR. Company B

-

also relevant to rising rates/ cap rates. At a constant exit cap rate (a key assumption), it is better to buy at a higher cap rate, and lever with higher cost debt, than to buy at a low cap rate and lever with low cost debt. A big landlord on twitter did a poll on this to illustrate it and 63% of people answered "incorrectly". Now it's more complex than that, but the public market allows us to buy MF at 6% cap rates with 3% in place debt (ie the best of both world's) but with too little leverage (ie overly safe). Because of this low leverage, cash flows to equity aren't as exciting as one would like (call it 6% ish) https://twitter.com/MRossG199/status/1603445100939341824?s=20&t=TwL6ugvNPveI5hNSwlhk2A https://twitter.com/c_huss/status/1603454080403357698?s=20&t=TwL6ugvNPveI5hNSwlhk2A

-

yea, I'm not predicting that gets repeated, nor am i incredibly excited about ESS (have about a 4% position). if i thought ESS was going to compound in teens i'd put my entire NW in it and retire lol. it probably goes lower over next few q's maybe years as tech bad news shows up in fundamentals . I think ESS did well because california doesn't build enough housing or raise property taxes and it owns a high barrier to entry irreplaceable portfolio (tech boom also helped of course). I'm not a big "this is the only geography that will do well" guy. I rolled my APTS profits into a Nashville ground-up mixed use development. Can't have a better economic outlook than NAshville, also a market that's bringing on crazy supply. I own a valuable house in suburban DC. I own JOE. I own ESS. I'm a permabull and i want some Cali, some NYC, some Nashville, some FL, some DC....all as long as it's reasonably priced. I don't have a strong view on Realty Income, other than that their model is more dependent on accretive issuance (which is fine and can work)

-

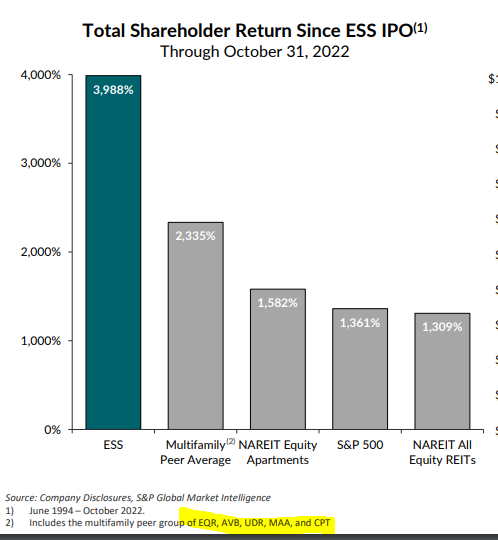

here's the chart you're looking for. The future won't be as good as the past, but long term REITs have provided returns in line with the indices, MF REITs have done better than REITs, and blue chip MF have done better than MF (and ESS has done better than blue chip because you know California). I don't know what next 10 yrs look like, but would be surprised if they can't put up solid and safe high single digit annualized returns (with some optionality to higher IRR's over shorter time frames from re-rating). Nothing crazy, but not a terrible way to preserve and grow one's purchasing power.

-

the publics have nicely staggered debt making this risk pretty manageable. To illustrate let's take ESS. ESS has about $5.3B of bonds outstanding at a 3.1% WA interest rate. $600mm / $5.3B is 2048 and 2050 maturity. that's not all their debt, but I'm just going to use that for simplicity. Below is the WAIR assuming they refi'd the existing bonds at 5% and 7%. Note how it takes a full 8 years to raise ESS's debt cost by 1% if current rates of about 5% on their bonds prevail. this is despite the fact that their wgt average bond maturity is "only" 7.5 years. Each year they have $300-$500mm mature which is about the same as their current $550mm/yr dividend and about 1/2 their FFO. worse comes to worse, just go to be net neutral on shareholder distro (issue stock = dividend) and pay off debt due in a coming year, though that'd be a not great outcome. point is the big publics can handle a huge increase in cost of debt/equity capital. in that scenario, the private market would be in shambles and many owners will be handing back keys. Many MF owners have 70-80% leverage. to put some more numbers behind it, the bonds are about 80% of their debt cost and are about $166mm interest / yr. If you had to refi it all at once at 7%, it'd suck and decrease cash flow by $200mm/yr ($3.1/share vs 2023E FFO of $15) so about 20% . But that's not what will actually happen. I'd also note that increasing rates offer buyback opportunities for the in place debt. The 2.65%'s of 2050 trade for 60% of par right now. At 7% they'd be at $47

-

agreed on all accounts. another important thing for the asset class is the stability and attractiveness of financing. Fannie/Freddie/Ginnie are a large % of the financing (and increase share when banks/insurers/CMBS aren't there), and provide low cost/low spread financing to the market. While the REITs don't take advantage of this and run with very low leverage, it underpins asset pricing and allows the REITs to sell individual assets for good prices to buyers willing to put on more leverage. the low leverage of the MF REITs is a double edged sword in that they can never relaly be that exciting, but it also makes them much easier to average down into as they decline in price. they'll be the last ones standing if shit really hits the fan.

-

2022: +4.5% Historical: All rough approximations, putting the old stuff from contributions to similar threads like this, it looks something like this My consolidated IBKR accounts have returned: +248% from May 24th 2013 to December 30th 2022. SPY is about 178%. REITS +62%....Account = 13.9% / yr. SPY = 11.2% / yr My consolidated Fidelity accounts have returned +106% from August 12th 2016 to December 30th 2022. SPY is about 96%. REITS +23%. SPY: 11.2% /yr, Account = a bit better than that. My (slight) outperformance has come with much greater volatility and tax drag. 2022: +4.5% 2021: +55% 2020: +2% 2019: +20% 2018: -2% 2017: +15% https://twitter.com/thepupil11/status/1610293154871406593?s=20&t=ljxIAVKsBs5hps4Nrk7LAg

-

right, but they're actually like 1/2 of what the numbers indicated, so you're making an asusmption with bad data. No one is forcing you to look at UHAL, and in the end you can prioritize what you wish, but just think you mischaracterized the biz w/o doing any work (which i sometimes do too, and like when people correct my high level impression w/ data). About 1/2 of gross capex is purchases of rental equipment. If you net this w/ sales of PP&E (which I'm not sure one can do fully, but I think that line is them disposing old trucks), it's more like 1/3. One has a very different view of the capital intensity/maint capex when looking at the company as a self storage company with a truck rental biz. vs just a truck rental biz. Also you seem to assume higher inflation / much higher rates as fact, when in my opinion it is one scenario of many (we've had this discussion multiple times though, so no need to rehash ad nauseum)