giulio

-

Posts

146 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Posts posted by giulio

-

-

2 hours ago, Cigarbutt said:

They used to compare (in older annual reports, in the CEO's section) their relative investment outperformance compared to bond indices and large stock indices and the results were impressive (Graham-Doddsville type)

It would be great to see them post this again!

-

12 hours ago, Viking said:

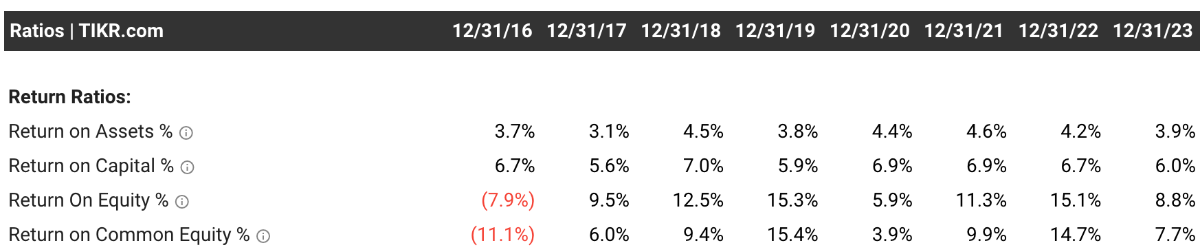

@Dinar If Fairfax has performed so poorly on the investment side, how did they compound book value at 18.4% over 38 years? Insurance/underwriting?I cannot claim to be an expert in the field so any input is appreciated, here is my 2c:

An insurer would need to write @85% CR or below to achieve those results without a strong performance on the investment side. Some lines of insurance could allow you to achieve that CR. Or a combination of niche expertise and strong technology (i.e. low loss ratio and low expense ratio).

For example, Kinsale has a "standard" $3b portfolio but excels on the uw side.

I am not sure if an insurer can scale and still maintain such a CR.

Another example would be Francis Chou at Wintaii: both strong uw and investment expertise, but he write $50M in premium on $150M of equity.

@Parsad correct me if I am wrong here.

What does Watsa mean when he says that to achieve 15% ROE FFH needs a 95% CR and a 7% return on investment portfolio?

The math is simple: a 7% ROI (both interests, dividends and gains realized and unrealized) translates to 5.1% after tax (26.5% Canadian rate). At 3x leverage (thanks to float and some debt) this equals 15% ROE.

UW profits would more than cover FFH other expenses (overhead, interests, run off).

Now 75% of the portfolio is fixed income in nature (A) and 25% is equities (B).

If (A) earns 4% and (B) 16% you get 7% ROI.

This is my extremely simplistic view and the way I would look at an insurer with demonstrated uw discipline and a focus on investment performance.

It is not easy to find both these elements. It is even more rare to find an investment team that aims for superior returns in BOTH equities and bonds!

Most insurers just park float in bonds and match liabilities. At FFH we benefit from an incredible astute team that looks for bargains even in bonds. Do not underestimate this.

I think the above equation completely melts down in a world of 0-2% return on bonds and an equity portfolio "drowned" in hedges, shorts and some bad investments. Still, Over the last 10 years, FFH BV has compounded at 10%.

I remain optimistic about the future and believe that they will achieve their stated goals.

G

-

FFH did not need higher interest rates to work out well as an investment in 2020-2021.

If you held everything the same, the stock was easily worth 2x.

When I was building my position the market cap was around $10B and I thought that in 5 years time FFH's shares of Atlas + Digit + FIH could easily be worth $5B. I was able to get ALL the rest for $5B.

IT WAS A NO BRAINER.

The subsequent outperformance was surely due to not just one factor but multiple ones working in the same direction:

- no more shorts,/hedges

- fih investments surfacing value

- equities portfolio recovering from covid

- better uw results

- hard market

- buybacks

- higher interest on fixed income portfolio

and I am sure I am missing others.

4-5% rates are not an anomaly. 0-1% was! My assumption in 2021 was rates would go back to 2019 levels, 2% at best. Still, FFH was so undervalued.

To say that FFH worked out as an investment ONLY because JPow hiked rates is UNFAIR to the great work done by Watsa and the team.

G

-

7 hours ago, Hoodlum said:

It looks like the loan to IIFL is for 3 years @ 9.5%

https://economictimes.indiatimes.com/industry/banking/finance/fairfax-arm-infuses-rs-500-crore-into-iifl-finance/articleshow/109323304.cmsThanks for sharing. Interesting because Odyseey is providing the loan, not fih.

I guess fih will subscribe their portion of the rights issue.

-

What stood out to me:

-

Their expertise in India and how well the bial team is executing

-

Buffett and Jain tried to set up an insurance operation in India and gave up. I am sure they tried to invest there and found out it was too difficult. This is of course from 2010, before Modi. I would say that Watsa has been highly successful instead and it does get enough credit for this. He saw the opportunity and positioned fairfax to succeed.

- Bial becoming a hub for airlines in the south of India is a great accomplishment

-

- Sokol made me jump from my chair: I was not expecting that kind of growth from Atlas

- "we don't forecast, we react and we are fast": great line and great example with the $1B issuance not being possible today

-

The fact that FFH might be less dependent on investment gains going forward and their improved ability to absorb cat losses: I liked that whole segment.

- I don't think we are there already but it is a promising start especially if they tilt their investment strategy in that direction

G

-

1

1

-

Their expertise in India and how well the bial team is executing

-

I got the same impression wrt Anchorage which is strange because 1) they said that Anchorage will own the entire bial stake eventually, 2) if they are going to bid when other infrastructure assets get privatized they should have a structure in place.

Iirc they should list bial by September 25, but given their partner in Anchorage I guess they can renegotiate that.

On the sib. Watsa said "we are buying shares in the market" numerous time. Truth is they haven't bought any in 2024 (while ffh has been more active). Last purchase was in November.

They are preserving cash, maybe something good will happen in H2.

-

Here are my notes on the 2024 FIH agm that just finished:

- Something worth keeping in mind -> in 2023 they bought back 2.9M shares, the share price was up 24%; yet, $14.9 is exactly the same price at which they completed a SIB back in 2021. A lot has happened in 3 years...

- slide 28 is a nice summary of the impact of fees on returns

-

BIAL will see "explosive" growth in the next years

- huge number of aircraft ordered by indian airlines (1200?)

- number of operating airports expected to roughly 2x to. 250 (?)

- Air India established its 2nd HUB in BIAL -> increase in international flights (EU/US) + other flights from other parts of India

- Watsa said that there are lots of structure that you can set up to raise money for big opportunities; seemed very confident that money will not be a problem for FIH

- Sold NSE because valuation was too high and they saw downside risk given that NSE makes a lot of profit from options trading

-

IIFL gold loans issues -> founder said there were minor "lapses", IIFL was used to set an example for others. He said they addressed all the issues raised by RBI and hope that RBI audit will confirm this (April 12th start)

- no fraud, no money laundering

- Lots of emphasis on the financial sector opportunity -> 7% real growth, 12% nominal, financials should grow at 1.5-2x the nominal = 18%

- I am not sure I got this correctly but Watsa said something like "we are targeting 20% rate of return, not 10-15%, need to offset some fx risk"

-

Sanmar had a terrible year with PVC prices down 30-60%

- improved efficiency in Egypt

- focus on specialty PVC

- growth ahead -> China has similar population to India and uses 20M tonnes per year vs India's 4M tonnes per year

- Maxop and Jaynix -> "unlimited growth", their only constraint is capacity and they are expanding, huge demand

- Anchorage still stuck in regulatory approval, nothing will move before the election (I would expect nothing before 2025)

- Privatization opportunities will unlock after the election

all in all, great enthusiasm as always. focused on integrity.

Deepak Parekh (founder of HDFC) is their consultant for everything and this is a HUGE plus in my view.

Curious if any of the guys who attended in person were able to gain other insights.

G

-

1

-

Will he give up when Digit goes public? The COBF should make a bet with him wrt Digit value/valuation.

-

still at it.

Looks like mw is on a crusade now against Watsa.

-

Small consolation.

I still have mixed feelings about FIH selling their NSE stake. I hope they can put the money to work in even better opportunities.

-

Since I updated my FFH valuation, I'll share it here just in case someone wants to add anything.

I use 3 methods to value FFH

-

Investments + capitalized underwriting profit

- Starting from the investments portfolio ($65B), I subtract debt (excluding debt @ consolidated equities), preferred shares and NCI

- I capitalized avg uw profit @ 14x (7%)

- NAV = $2500

-

Look-through earnings excluding run-off

- this part relies on more work, estimates and assumptions (e.g. earnings yield on MTM equities of 6%, cash tax rate rather than statutory one, excluding investment gains, ecc)

- for 2023 I get $5B of EBIT, $4.3B of EBT and $3.2B of net income (a 25% increase YoY)

- ROE of 16.7% in 2022, 15% in 2023

- @ P/E of 14x the shares are worth $2000

- I think 2023 numbers represent a fair, conservative estimate of earning power over the next 4 years (lots of moving parts but they should balance out)

-

P/B

- if FFH can earn 13-15% on book value, an investor buying @ 1.5 P/B would be paying roughly 12-10x earnings for the company

- everyone fair multiple would be different but 12x would not strike me as expensive

- @ 1.5 P/B shares are worth $1500

Overall, I think FFH intrinsic value is closer to $2000 per share and I hope this will prove conservative thanks to strong uw discipline and good capital allocation in the next 4 years.

Book value is probably understated as well.

G

-

Investments + capitalized underwriting profit

-

Here are a couple of things that came to mind while reading your post @Viking. While I agree with parts of it but not all of them, I certainly enjoy the discussion!

12 hours ago, Viking said:There is no standard definition of ‘quality’ that can be applied to all companies and industries

Looking at average ROE, ROIC, ROTCE is a way to measure quality. It's important to understand the normalized earning power over a cycle; more important is ROIIC, that's where the compounding happens.

To answer these questions an investor needs a deep understanding of qualitative aspects (competitive advantage) that cannot be found in reported numbers or excel spreadsheets.

This is at the business level. What happens at the "investment level" depends on the price you pay. Here I agree with you and particularly liked the Howard Marks quote.

Overall, I would say that FFH has done better by identifying cheap opportunities (low price) in so-so companies (not great, high-quality companies).

FIH on the other hand, was able to invest in better companies (i.e. NSE, BIAL, IIFL finance, companies that can earn 15%+ ROE and grow long term).

When I look at FFH top holdings table and the comments from the AR, it does not flash "quality":

- BDT might be a great relationship to have, but the return from 2009 are sub par. FFH could have easily made 4-5x its money by investing elsewhere (15 years time frame, starting from a low point);

- ShawKwei 12% is not bad at all if they can achieve it consistently;

-

Poseidon is probably ok? Double-digit ROE but it takes a lot of debt to get there; it reminds me of BRK investments in utilities (no homeruns but ok profile with contractual cash flows);

- Eurobank, like all banks, may be a good investment if they do business conservatively and don't need to be recapitalized when the next crisis happens. Maybe their scale and the small number of big banks left in Greece is an advantage. This a perfect example of what I said earlier: by paying a very low price FFH might come out fine with a good CAGR;

- EXCO and Stelco are cyclical and probably enjoyed the good part of their industry cycle, I have no expertise in the area. I recognize Stelco's CEO as a good capital allocator and their lowest cost advantage might help them better navigate a bad industry overall.

CONCLUSION

The question I ask myself more often is how is money going to be invested going forward?

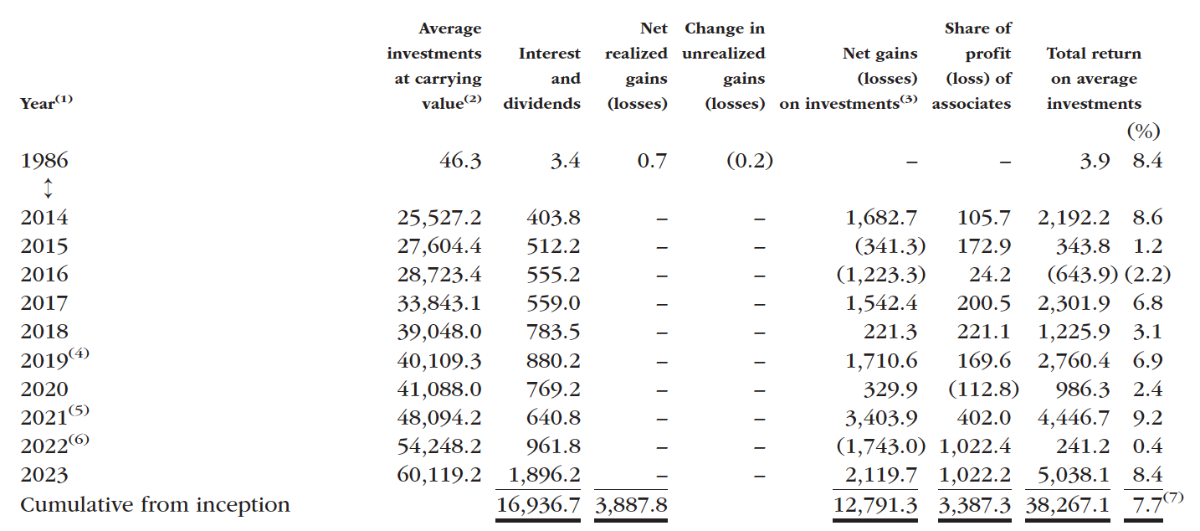

FFH will have a huge amount of capital at its disposal. Higher than any point in the past:

- 1986 to 2022 they received roughly 15B in interest and dividends. over the next 4 years they will receive c. 8B, i.e. more than half of what they got over 36 years!

- the same goes for profit of associates/gains on investment.

Buffett taught us that it's easier to invest bigger amounts of capital in high-quality companies and don't touch them.

When fishing in a lower-quality pool you NEED a low entry price and you must NEVER forget that at some point you must exit the position. You cannot stay indefinitely, or risk doing a round trip with your gains.

This is easier with small positions, way harder if you invest big money and your position is large (% of ownership not portfolio weight).

There is a lot to like in the way FFH manages its equities portfolio, e.g. the international exposure, their expertise in foreign markets, strong local relationships, their opportunism in tough times (Templeton's heritage I suppose).

We'll see what happens next, will they tweak their style a bit and adapt? Will they reduce capital via buybacks and higher dividends?

G

-

https://www.joincolossus.com/episodes/83022007/hansen-the-long-short-of-investing

interesting discussion on India, around min 50.

It shows the advantages FIH has by being on the ground.

-

Swapped some MO shares for BTI.

-

@SafetyinNumbers this is what I understood from last year AR.

The amount is fixed, like debt. If you keep the P/B unchanged and the insurance subs increase BV then FFH would have to pay a higher price.

The call option allows FFH to repay the same amount they received instead. If BV increases they record a gain on the value of the option.

This is what happened last year with Allied and Eurolife purchases. I am halfway through this year AR and I'll write an update when I am done.

Hope this helps.

G

-

3 hours ago, Haryana said:

IIFL goes to bankruptcy

Do you think that's a risk? Could you explain why?

Also, why are you mentioning corruption?

I thought this was a lack of control problem.

A couple of years ago rbi banned hdfc bank from issuing credit cards. The issue was resolved in 9 months.

I am trying to understand the extent of the issue here.

Worst case scenario, fih completely misjudged the founder profile which would be bad.

Thanks

G

-

Increased position in JKH through debt conversion. FFH now owns close to 20%.

https://www.ft.lk/top-story/Fairfax-converts-Rs-14-3-b-worth-debt-into-equity-at-JKH/26-759025

-

3 hours ago, gfp said:

surprising

I was a bit disappointed honestly. A part of me wished that they could hold on to it for a very long time.

Anyone here share the sentiment?

Do you think they will treat the airport differently?

-

41 minutes ago, Xerxes said:

Maybe (just maybe) MuddyWater folks are actually geniuses. They are actually long the stock, but they know just putting a bullish call doesn’t do the trick on a dormant volcano.

"Congratulations Prem on a very strong quarter" would be a dream intro!

-

Thanks @SafetyinNumbers, i did not consider this optionality actually.

Still, it's way easier to hold the stock now. If the stock ran way higher than the actual business results/prospects it would be harder to hold on. What do you think?

-

1 hour ago, MMM20 said:

Don't we want them buying back as many shares as possible (without stretching too thin from a liquidity POV) at the current discount to intrinsic value - even if it makes them a bit less likely to get into the TSX 60? Would getting into the TSX 60 be so meaningful as to push the stock well above IV, giving them a good opportunity to issue shares? Does that tend to be the effect of TSX 60 inclusion? Idk what to root for.

I would not care about index inclusion as long as you plan to hold the share for the long term, which I assume you do given your estimates of fair value.

Imo, Best thing that can happen is that shares remain undervalued, they keep buying back 2-3% pa and invest to grow the business.

Think about the money they can deploy in India, or grow the insurance in this hard market or take advantage of a widening in spreads if something unexpected happens.

The cash coming from their bond portfolio probably offers a sufficient cushion in case of a bad year.

Share price will follow the cash generation capability of the business, regardless of accounting standards or the trs position.

G

-

-

13 minutes ago, StubbleJumper said:

No. Say what you want about Prem's investing skills, but he is not a particularly clear and cogent communicator. When he answers a question, he doesn't really provide a response, but instead tends to do what I call the "Prem fuddle" where he mumbles around in circles about something that is only tangentially related to the original question. If he only did this for the questions he wanted to avoid, I would understand and I would admire him for being so crafty. But he does it for EVERY question, even the softballs.

What we need is for Jen Allen to give a 2 minute spiel about the rules for writing down assets due to permanent impairment, and FFH's annual process for doing this. There's a legitimate reason that Farmer's Edge or Digit have not yet been written down as much as Muddy Waters would contend should be done, and that reason is the actual accounting rules and the annual internal evaluation process. There's nothing nefarious there. So, we need Jen as the expert (and as a solid communicator!) to briefly walk through the rules and the process. After she gives a clear and cogent explanation, then perhaps Prem could chime in with his usual indecipherable "Prem fuddle."

And so it goes with the IFRIS adjustments. Jen is a solid communicator and should walk us through the reason why FFH is now using IFRIS, how the rules work, and the outcome. She has already done this on past calls and did a great job of it. Well, it seems that she needs to do it again in the context of yesterday's report. And then after a compelling explanation from Jen, perhaps Prem can chip in with his usual few comments that go in circles.

This CC is actually important. The only response that Prem should be making should be something that he reads word-for-word that was written by Jen and the rest of the C-suite. Keep the extemporaneous comments to a minimum and preferably have the stronger communicators provide technical explanations where they are appropriate.

SJ

1000% right.

Brad Jacobs discussed how he reacted to a short attack on XPO. I thought it was brilliant.

https://www.joincolossus.com/episodes/19966134/jacobs-think-big-and-move-fast?tab=transcript

-

Here are my notes after digesting the news. Sorry for the errors, I just wrote down my thoughts.

****

I don't think the report highlights anything new for members of this board.

- We knew that the transactions with OMERS were essentially debt in nature.

- Grivalia and EB issues? discussed already

- APR, farmersedge and Fairfax africa were dogs and investment mistakes? agree.

- Fairfax cash starved in 2020? sure

I thought the AVLN was similar to guaranteeing the reserves level. It allowed FFH more time to come up with cash needed as well. Is this bad behavior from Prem?

Also, isn'it a bit stretched to say that EXCO has a market value? Not an expert but this is extremely illiquid and no financials are available.

Gulf Insurance purchase price is spread over 5 years! 200M at closing and 165M over the next 4 years which is close to what the company recently earned. Does not seem an inflated price to me.

The only thing that caught my eye was what the Digit former employee had to say about the company. Digit is not lemonade for sure, I think it can stand on its own and knows how to write insurance. I am curious about its tech stack though: is it more like Progressive or GEICO?

In the end the report revolves around accounting issues and how FFH has chosen to present results.

This is why it is paramount to focus on economic reality rather than just reported numbers.

MAYBE the accounting was a bit aggressive and Prem did hide some losses during an extremely difficult Covid period. We need to contrast this with everything we know about the culture of the company and make up our minds.

On my part, I purchased more shares yesterday around $910.

Fairfax 2024

in Fairfax Financial

Posted

Hi @Hamburg Investor, I appreciate your response.

First, let me stress the fact that this is a very high-level, simplistic view of FFH. I basically assume that their uw profits make them break even on all other costs, so you are left with the portfolio returns.

That said, you are right

Could you clarify your comment on growth? I am not sure how to interpret your question. Are you referring to some kind of operating leverage?

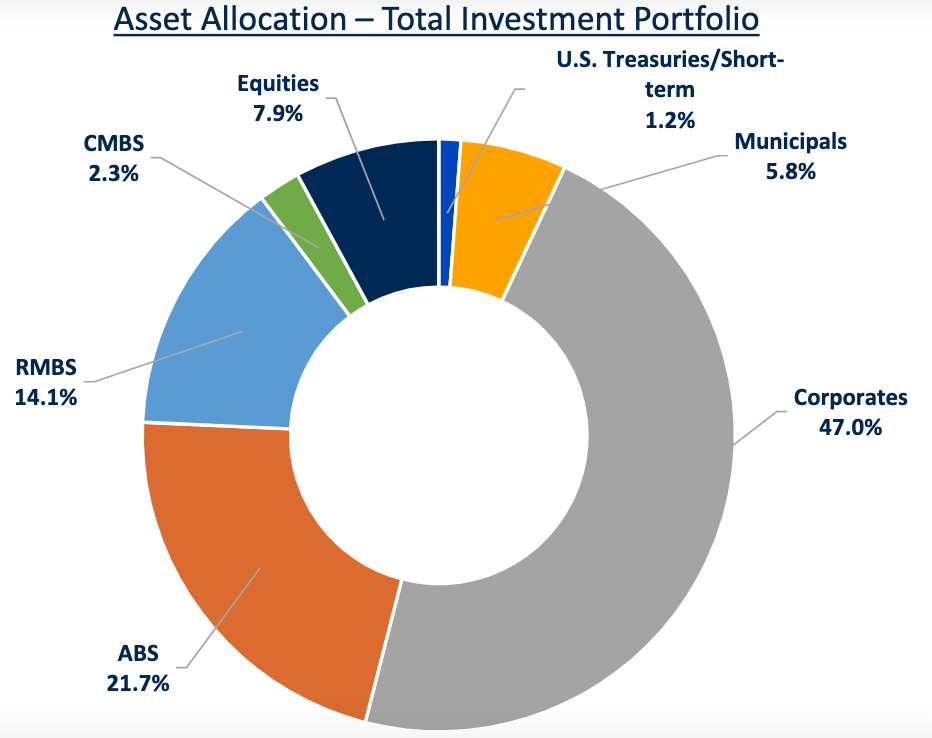

On the bonds yield, this is what FFH reported in the AR 2023

The 10% you mention, I think it refers to the IRR they expect to earn on the KW/PacWest loans, i.e. an example of their opportunism. Corporates are not yielding 10%.

Anyway, you can play around with the numbers. I just wanted to show that if Watsa can display a 18%+ CAGR it's not just leverage or uw profits. The equity portfolio, in a lumpy manner, has certainly contributed!

On the last part, I did not get your point.

The insurance segment provides the capital for the investment team to put to work. Only part of it can go to equities. During the last segment of the AGM, Watsa talked about the "transformed" FFH and the "stability" of the interest income achieved. He alluded to the possibility of tilting more capital towards equities in the future, but I guess that will depend on the premiums level and regulatory capital.

G