racemize

-

Posts

2,831 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Everything posted by racemize

-

could they do it via swaps and it not be reported?

-

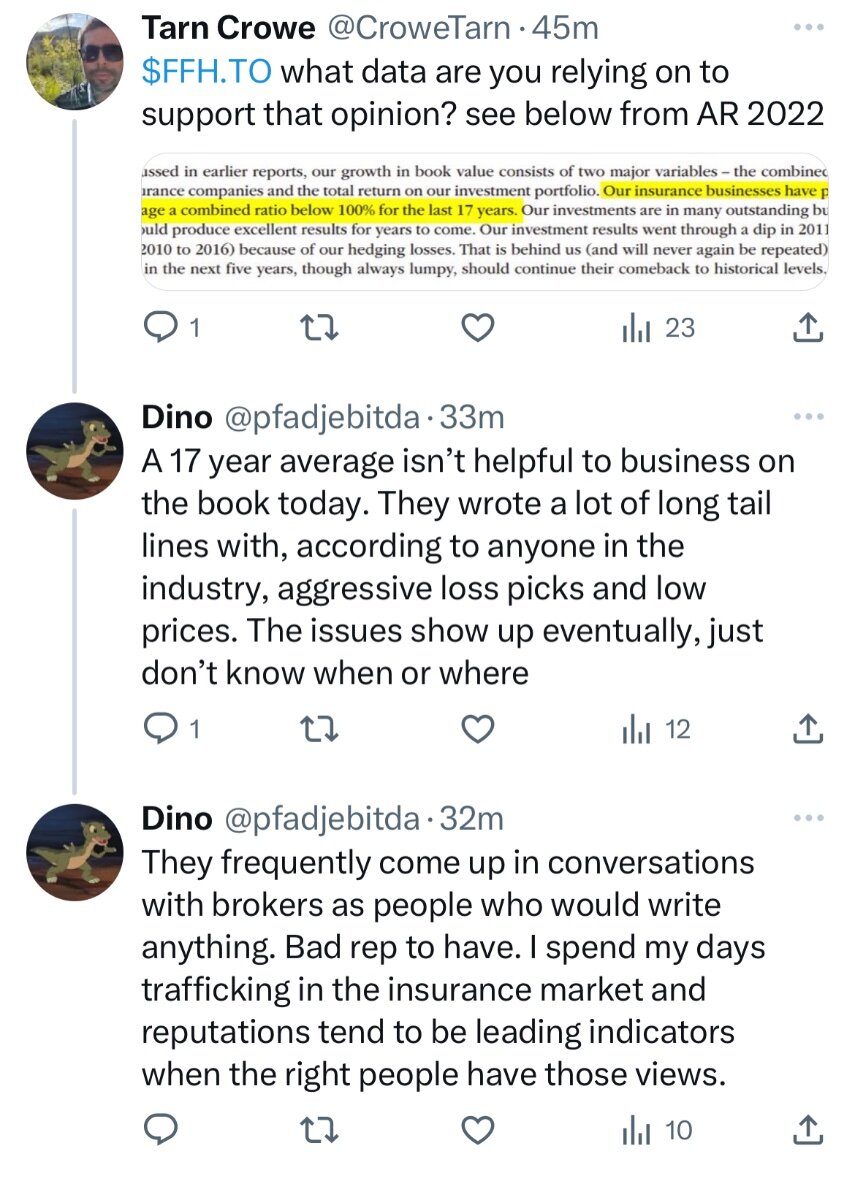

Saw this on twitter—any insurance insiders have any comments?

-

I guess getting back to the multiple of book value trading question. In all honesty, if you are a permanent holder, you don't want it to trade at 2x book value. In fact, you want it to trade as low as possible for as long as possible, so they can buy back shares. Trading higher does nothing good for you, unless you 1) want to sell; or 2) want them to issue shares to buy other companies I guess.

-

I mean the real issue is that if anything like the last 10 years happens again, it should not trade at 2x book value.

-

This is by far the most important metric to track.

-

The problem with these very high IV calculations is that it really kills growth generally. I.e., you had more growth when using BV/share because you were getting the leverage from the investments/share. If you calculate IV at investments/share, then you have lost leverage, and it grows more slowly. I've found that the added IV but lower growth pretty much offsets. Happy to be wrong here though.

-

Let's not start talking about them shorting equities again please. PTSD for all of us.

-

I’ve got a word searchable compilation that will have it if they said it in an annual meeting (or some other places that were transcribed). Link to compilations: austinvaluecapital.com/resources

-

interesting that the same time, the mortgage spreads are very high.

-

Good point, yes, have not had any withholding from the annual dividend in that account, so probably would work for this.

-

It is not clear to me what the tax implications (e.g., Canadian withholding) if this is sold via a U.S. IRA. Any thoughts from board members?

-

If they were basing it on the patent value, I wish they had talked to me. That was peak wireless patent price when those previous transactions went down (nortel and motorola). Experts would have known that at the time. Also everyone out there saying “patent value” is a thesis (for virtually any stock) who isn’t in that specific patent space—don’t put too much weight on it. Patents are very tricky and fickle things.

-

Refused to comment on BB, several questions on it. All shorts closed.

-

What was said? Rough version: Called in and told him he needed to step away, he wasn't paying attention anymore, and had lost his touch. Continued by saying that Prem didn't understand any of the companies he was investing in and wasn't doing any detailed analysis on microeconomics, his partners agreed but were Canadian so too nice to tell him, and the bankers were cowards not asking hard questions because Canada doesn't have enough good companies.

-

wow, which one of you just went off on Prem on the call?

-

Pelosi didn’t ask for $2k checks?

-

Apparently BB is making the rounds on various YOLO places, e.g., WSB, TikTok. (This is what I hear anyway)

-

I believe BAM was in warehousing/logistics first and sold it to BX or others. 2018 investor day transcript:

I believe BAM was in warehousing/logistics first and sold it to BX or others. 2018 investor day transcript: -

At least according to ycharts 2010 eps was around 13$ which would be a cagr of ~14%. Don't know about ycharts. I used the 10-k. See attached. Missing the stock split--in today's numbers it was $13.16

-

+1 pupil, surprised so many people reacting to the sale of less than 1% of a company that doesn't meet his requirements in the first place.

-

Would you ever expect them to trade above par, given how low rates have gone? I need to look at the terms again. No, just trading back to where they were in 2019 is sufficient. Meantime, 8% yield or so.

-

Viking, what's your short-term trade target here? Getting back to book value? One idea, and I've switched to it, is just buying the preferreds. If you are aiming to get to book value, I'm assuming they will get back to $20-$25 (depending on the series) at the same or better pace than common.

-

Sanjeev, I'm curious as to what you think of the fact that insiders all all buying preferred shares rather than common shares? They seem to have quite a bit of upside themselves these days...

-

MKL has a lot more specialty policies than BRK I believe. And that's where language gets a little weird, as those are not standardized. I for example, have a policy from MKL (only 5%, as it was a lloyd's syndicate) that specifically covers business interruption when the government shuts you down for "an occurence of an identified human disease", with no pandemic exclusion language or addendum.

-

Companies still buying back their shares

racemize replied to undervalued's topic in General Discussion

BPY was up until black out.