dartmonkey

-

Posts

642 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by dartmonkey

-

The owner of Britain's oldest Indian restaurant has been acquired by a Canadian private equity house as it seeks to expand internationally, amid an ongoing legal battle over the historic venue's future. MW Eat, which operates the Michelin-starred Veeraswamy alongside restaurant chains including Chutney Mary, Amaya and Masala Zone, has been bought by Toronto-based Fairfax Financial Holdings for an undisclosed sum. Funny description of Fairfax, I didn't know they were a private equity house but I like it.

-

I also love this table and the analysis. Even if you plug in a more conservative 95% CR (not for this year, but for an average year), so 5.5% from underwriting, and the same 7% investment return (which they will way exceed this year with their asset sales), with the same cost of debt and tax rate, you get an ROE of 16.4%, and with an equity of about 1200 right now, that would give us $196. This year will be better because of a CR<95 and better investment returns. And one of the nice things about trading at 7x earnings is that the accumulation of the next year's earnings will increase the equity base by 15%, so staying at around the $200 earnings level will not even require such a good CR or such good investment returns. Safety, do you have a variation of this model that breaks down that investment yield into fixed income and equity investments? This table must have gotten the 7% by adding the 2, and it seems like an important enough detail to break that one line into 3.

-

I don’t think there’s much point in worrying about book value, the important thing, for a long-term investor, is how much value they have created. Despite the fees paid, they have increased book value by a bit about 107% (6.5%/yr) which is disappointing, but anyone investing in this company believes that the airport is at least twice the reported $2.5b, meaning FIH’s value is at least $30, conservatively assuming that the other half of FIH’s book value is fairly valued. If this is so, then FIH has returned about 200%, or let’s say 180% considering that FFH will take another 1/5 of the increase in book value from $20 to $30. That means we have a 10% annual return, net of fees. Still not great, but perhaps acceptable. More pertinent to me, going forward, that would mean we should expect an increase from the current share price of $16 to something like $28, once the value of BIAL becomes clear and if the shares trade up to book value, i.e. a 75% ‘catch-up’ return, which I don’t care to miss out on. And the airport and other holdings may well be worth more, and we may get CSB, and share repurchases way below value will help in the meantime…

-

I don't think it matters much whether they are equity accounted or not - the principle is that, if there's a sale of a bond or of a company that has already paid interest or a dividend to Fairfax, the sale is of the company ex-dividend, so the sale price will be lower as a result. In other words, whether income is paid out or retained, if a security is sold, the gain on sale will already account for the previously paid interest/dividend, so there's no double accounting.

-

Very nice summary, thanks. In last year’s annual report, Watsa predicts 4 more years of $5b operating earnings, translating into $150/share (or about $3b after “taxes, interest expense, corporate overhead and other expenses.” That sounds like a minimum, so it squares well with your prediction of just under $6b in operating earnings. In round numbers, assuming expenses of $2.2b because of $0.2b extra taxes on the extra $1b, that would give us about $3.8b in earnings, or $190/share, assuming 20m shares, meaning the P/E ratio would be just under 9. And I still think that that $5b in operating earnings for the next 4 years may be conservative, as it probably doesn’t take into consideration the compounding that should happen as that 11% earnings yield gets reinvested into new productive assets.

-

Yes, the whole North American equity portfolio reported in the 13F, at about $2b, is worth less than half the Eurobank position. And 3/4 of that $2b is in longstanding positions we know about like Orla (30%), OXY (14%), Cleveland Cliffs (9%), Blackberry (8%), KraftHeinz (6%) and Kennedy Wilson (5%), whether we like them or not. New investments like a bit more KraftHeinz or a new stake in LULU represent about $5m, so for a $36b company like Fairfax, with a lot of little investment portfolios buried deep down, like in a pension plan somewhere, they’re not worth worrying about.

-

I vote 3). If you assume $200m in earnings for 2026, as far as I can tell you have no line in your table for earnings from whatever Fairfax will hve bought with that $200m, potentially bumping up 2027 eanings from $200m to $225m, if all else remains the same.

-

Yahoo is even providing the transcript, via Quartr, for free as far as I can tell: https://finance.yahoo.com/quote/FFH.TO/earnings/FFH.TO-Q3-2025-earnings_call-369659.html

-

Yes. Their NCIB, in place for the year from Sept 30, 2025 to Sept 29, 2026, allows them to repurchase up to 10% of the current float, i.e. 2.187m shares, which would represent 9.7% of the subordinate shares. Yesterday, the company said that they had repurchased 107,525 of its subordinate voting shares for cancellation. Since there have been 27 trading days since the announcement of the NCIB, they have repurchased an average of 3,982 shares every day, compared to the maximum approved amount which is 11,371. So they are not maximimzing their repurchases. But if they were to continue at this pace for the whole 12 months (about 251 trading days), they would have repurchased 3982*251 = 0.9996m shares of their subordinate shares, a hair under a million, representing almost 5% of the total. Seems like a good target; at current prices, that would represent about US$1.56b, and at their current rate ($2.9b in earnings in the first 9 months of 2025), that would leave them enough to this year pursue other opportunities like buying out the remaining Allied World stake ($1-2b probably) and pursue other acquisition too, if they wish, given their $2.8b in cash at the holding company level.

-

I am frankly amazed that people think that Fairfax's 'fair and friendly' doctrine would also involve protecting shareholders because they have followed Fairfax into an investment or are members of these boards. In any minority investment, you can have your shares taken away by someone who swoops in and takes it away from them at a good price, and it is neither a moral failing of Watsa nor a contradiction of his fair and friendly approach that he looks out for his shareholders' interests and offers to buy something a good price, even if not everyone wanted to sell it at that price. As for Fairfax India, I don't think the same is true. Watsa DOES have a fiduciary responsibility to protect FIH shareholders, different from his lack of responsibility towards shareholders of Fibrek, Atlas or Kennedy Wilson. FIH is an investment vehicle set up by Fairfax with a controlling stake held by Fairfax from the start. Fairfax is involved in managing the company and communicating with shareholders about its value, and supporting that value by repurchasing shares. I think it is obvious that it would not be fair for Fairfax to take investors assets at $10 a share and to then turn around and take them out at $6 a share because Mr Market is not seeing the value. In addition, who would ever invest in a future Fairfax investment vehicle if they behaved that way? Whereas this concern does not exist for external companies like Fibrek/Atlas/KW. Perhaps Watsa has never explicitly promised to never take FIH private, but I bet he would answer this way (has this question ever been directly asked of him?), and I think the fact that he has not taken FIH at even lower prices than today (like the sub-$10 price 3. years ago) is some confirmation that he has no intention of doing so.

-

McMorrow owns about 25m of the company's 138m shares, a bit over 18% of the company. He paid himself $16m last year, $14m the year before. Total revenues $532m, so his pay represents over 3% of revenues. Other execs were the (now ex-) president Mary Ricks, at $11m, current president Windisch at ~$7m, general counsel In Ku Lee at $5m, and CFO Justin Enbody at $4m. Total for these top 5 was $44m, while the company had EBITDA of $216m. Seems excessive for a company with a market cap of about $1b yesterday ($1.3b today).

-

I can't remember the details but they granted 4.8 million, 3.4 million and 2.8 million shares of performance based restricted stock units, during the years ended December 31, 2024, 2023 and 2022. Share counts are pretty steady, because they repurchase a lot of stock, and I figured this is why they are not profitable in most years, most of what could be profits being expensed on compensation, and a lot of that to the top execs. They do well on their lending before exec compensation, and I presume this is why Fairfax is involved, but not so well for shareholders. I could be wrong, maybe I panicked too soon and I don't have all the numbers iin front of me to prove it, but that was my back of the envelope impression, maybe someone else could confirm or reassure us if this is not the case. Yes, the CEO is part of the financing on the takeover, but maybe he will now start behaving like an owner, not an employee getting rich at the expense of the company, and I presume FFH wouldn't be making this deal if they didn't have a plan to make the compensation make sense for them.

-

I bought some a few months ago piggy-backing on FFH and Watsa’s admiration of the company and partly because a FFH take over seemed likely, but sold quickly when I realized the outrageous level of executive pay. So I really like this idea, giving Fairfax the opportunity to find higher fixed income returns and, presumably, correcting the pay problem.

-

Here's what Grok has to say - is it incorrect? My question: Can you provide an explanation of the ownership Fairfax by Sixty Two Investment company and how much of Sixty Two Investment company is owned by Prem Watsa and his family? Grok's answer: Ownership Structure of Fairfax via The Sixty Two Investment Company Limited1. Fairfax’s Multiple Voting Shares (MVS) Total outstanding MVS: 1,548,000 (each with 10 votes per share) All 1,548,000 MVS are owned directly by The Sixty Two Investment Company Limited (“Sixty Two”) This gives Sixty Two ~41.8% of total voting power in Fairfax (despite holding only ~10% of economic equity) 2. Ownership of The Sixty Two Investment Company Limited Owner % Ownership Notes 1109519 Ontario Limited (“1109 Holdco”) 100% Private holding company V. Prem Watsa 100% control and beneficial ownership of 1109 Holdco Confirmed in SEC Schedule 13G, Fairfax proxy circulars, and CRTC filings Conclusion: Prem Watsa and his family own 100% of The Sixty Two Investment Company Limited — indirectly through 1109 Holdco, which he fully controls. 3. Historical Context (No Ongoing Fairfax Ownership) 1992: Fairfax acquired a 49.9% stake in Sixty Two from original 1985 investors (who had backed Watsa’s turnaround of Markel) Over time: Through internal restructurings (for estate planning, tax, and succession), Fairfax’s 49.9% was effectively retired or transferred, leaving 100% ownership with Watsa via 1109 Holdco Today: Fairfax owns 0% of Sixty Two — it is 100% privately held by Prem Watsa

-

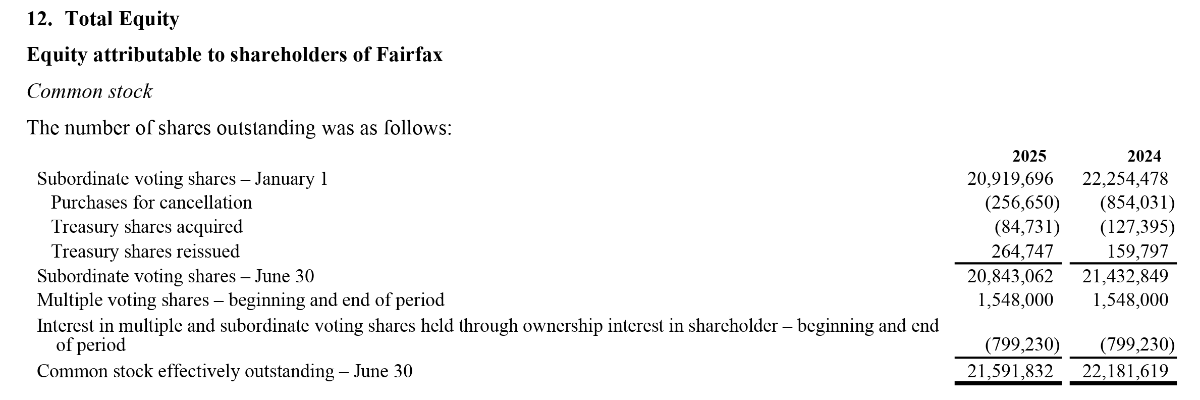

Thanks for that. Now I understand better the 799,230 subtraction in the Equity table in every report, this one from Q2: In other words, Watsa would own 748,700 of the 1,548,000 multiple voting shares, whereas the others are held by another company that Watsa controls. If it is the Sixty Two Investment Company, my understanding is that Watsa owns 100% of that company, but perhaps the 799,230 are owned by some other company that Watsa controls? If that is so, I don't really understand why these would not be part of Fairfax's equity, does anyone know? In total then, Watsa would then own 748,700 subordinate voting shares, plus the 520,000 subordinate voting shares he already owned before 2020, plus 209,000 of the shares he bought in 2020, for a total of 1,477,700 shares, or about 6.8% of the company, US$2.3b at today's US$1570 price. But it would appear that he also indirectly owns the other 729,230 shares, which would put him at 2.3m shares, or US$3.5b.

-

Although obviously no one has to justify what they do, count me confused as well. If it's too expensive to start a new position of any size, because of a hurdle rate of 15-20% that you're aiming for, then I could see the sense in holdiing a small position at the current if it's to avoid capital gains, but if it's just a matter of a hurdle rate, how to justify holding a position, especially if it's a huge position like 30%? In other words, apart from taxes, is there any reason to treat an existing position differently from a new position? Thanks for pointing out that Watsa reduced his share position, I missed that. To recap, he bought 486,000 shares for his personal account at around $310, or 0.7x book, in 2020. I seem to have missed the fact that he sold about 275,000 of these to the company in 2024, at around $1000, a pretty nice return on that investment (about 35% annualized). It is true that in addition to the 209,000 of these shares that he kept, he also already had 520,000 other subordinate voting shares and 1,548,000 multiple voting shares. And of course, unlike most of us, he is the founder and CEO of the company, and doesn't really need the money.

-

I think you have to go with what you know. We know it’s firing on all cylinders, with predictably strong earnings for several years, buying back shares well beneath 10x earnings, with some positive surprises with unpredictable timing (Fairfax India, GoDigit, Ki, opportunistic sales)… Buying at today’s price will look great, in a few years’ time, almost for sure. What we don’t know is whether today’s price is as low as it gets, or whether the price might go a little lower before it bottoms out. If you wait, maybe you get a few more shares and a better return, or maybe you miss the boat. There’s no way of knowing, but you don’t have to know.

-

Higher cat losses? Are they thinking of anything in particular? Grok couldn't come up with much: Basis for Projections Global Cat Loss Context: Q3 2025 (July–September) was unusually quiet for major events, with insured losses estimated at under $15 billion globally—the lowest since 2016 and well below the 10-year Q1–Q3 average of $70–80 billion. For the first nine months of 2025, cumulative insured losses totaled $105–114 billion, driven by Q1 events (e.g., Los Angeles-area wildfires causing ~$40 billion insured globally). This "top-heavy" year means Q3 contributed minimally (10–13% of YTD totals), per Gallagher Re and Aon reports. Fairfax's Historical Share: Fairfax's cat losses typically represent 0.5–1% of global insured totals, depending on exposure (e.g., higher in U.S./North American perils). In Q3 2024, Fairfax reported $434.5 million in cat losses (up from $388.7 million in Q3 2023), contributing ~3.5–4% points to its combined ratio. For Q3 2025, with subdued activity, projections align with normalized levels rather than spikes. Key Q3 2025 Events and Potential Impact: Typhoon Gaemi (early July, Asia-Pacific): Multi-billion-dollar insured losses (~$2–3 billion regionally), affecting infrastructure in Taiwan, Philippines, and China. Fairfax's Asia exposure (via Gulf Insurance Group) could yield $20–50 million in losses. Typhoon Shanshan (late August, Japan/South Korea): Moderate insured impact (~$1–2 billion), unlikely to trigger major reinsurance hits for Fairfax (minimal portfolio overlap). Minor Flooding/Heatwaves: Scattered events in Europe (e.g., Spain floods spillover) and Africa added ~$5–10 billion globally but were low-severity for insurers. No major U.S. hurricanes or wildfires in Q3, unlike Q1's $40+ billion LA fires (which hit Fairfax for ~$692 million).

-

If you plan on trading in and out...it might be of concern. If you don't plan on selling for 20+ years...then who cares about the selling. In other words, if you are a long-term shareholder, ignore the short-term noise. Cheers! What Parsad said is right, but in addition, I think the question of whether the stock always retreats after an all-time high (ATH) is because there is a built-in bias in the post-hoc question of what happens after the ATH. For instance, the highest closing price of FRFHF in the last year (from Oct 21 2024 to Oct 20, 2025) (which is also the highest price ever) was on June 24, when it closed at $1825. It has obviously retreated from there, but of course the stock can not be higher today than its ATH, or else today's price would be the ATH. A better definition of an ATH is the highest level it had obtained thus far. If we want to know whether people switch to pessimism when the stock hits an ATH, we just have to look at whether the stock price goes up or down, in the days following these ATHs, defined prospectively. Looking at the closing prices over the last 5 years, there have been 1505 closing prices, going from Oct 21 2020 at $285) to yesterday's Oct 20 close at $1650, which means the stock is up 479%, or up 534% if you adjust for the dividend (45% annualized). The average day-to-day gain was $0.91. Along the way, there were 128 days that closed at up-to-then highs, with the last one of course on June 24 2025 at $1825. In the day after these 128 highs, there does seem to be some drop-off, but it is small, and completely reversed by day 5. On the day after an ATH, the average price change was -$0.21. On day 2, it was another -$0.45, day 3 was another -$0.39, but then it's over, with days 4, 5, 6, 7 and 8 and posting changes of +$0.78, +$2.53(!), +$1.13, -$0.25, and +$0.32, with gains by ATH+8 totalling $3.56, not quite as high as you would expect on average (8x the average $0.91 gain) but they are not negative. In other words, instead of getting the average $0.91 gain, we got small losses on days 1, 2 and 3, and then a modest recoveries on 4 of the next 5 days. I wouldn't put too much weight on these calculations: 128 data points is not a lot to go by. Don't expect the big day 5 gain to be replicated in the next 5 years, for instance (athough I willl be looking out for it!) The important point is that the losses in the few days after an ATH are small and only last a few days. Hopefully we will see some confirmation of this soon.

-

Yes capitalism is a bummer, with all that conpetition. Just when things were going nicely, with combined ratios in the low 90s, someone has to go and start offering lower premiums...

-

August 23, SafetyinNumbers posted a table from RBC Capital Markets (made in June 2025) with a very similar logic, based on how much leverage is involved as a multiple of equity: They get a higher ROE (18.8% instead of 15.4%), largely because they are assuming a higher CR (93%), so 7.0% from underwriting, leveraged 1.1x, so 7.8%, whereas djokovic1's calculation gives 5.0% from underwriting, not leveraged (i.e. leverage = 1x)%, and RBC are calling this 'operating ROE', i.e. not counting the cost of headquarters (around 3%).

-

Agree with gfp that this just refers to float leverage. If float is 1.6x equity, that actually means that alongside every $1 in equity, they ALSO invest $1.60 in float, so they are levered 2.6:1, not 1.6:1. Then you have to consider that they typically hold bonds in an amount equivalent to the float, so it's not like they can just leverage up 10% ROE stock investments to get 26% ROE. If they get 4% pre-tax on the float, plus 3.5% underwriting (their 20-year average), and 10% returns on their own equity, that would give them 7.5%*1.6+10%*1=22% pretax, say 17.5% ROE posttax which is great and doable. I think that is what is meant by "10-12% ROE ideas" above, the returns on the equity investment ideas, not what they can get on the overall portfolio.

-

I don't know, but they have said that if duration matches the timing of liabilities, that is just a coincidence, and Ben Watsa has said their positioning is because they see inflation coming, so I guess they think that current long duration bonds don't compensate them adequately for what they perceive as a higher risk of inflation than what the market has priced in. If I had to speculate, I might also say that current earnings are fantastic anyways, so strategically they can afford to miss out on some interest income in the short term in order to increase their chances of not taking a big capital loss on their bond portfolio, if interest rates increase (bond prices drop), and to lock in higher rates whenever that happens. In other words, taking the long view over the short view, which is what they always try to do. An insurance company with smaller underwriting gains or less income from fully owned subs (Recipe, etc.) might feel more pressure to maximize current interest returns. But that is just speculation.

-

Possibly, but which way? I think protecting downside because you're not being paid to take the risk of a possible macro outcome is a micro/pricing bet not a macro one. But I am also starting to think the argument I (re)started is rather pointless I think we probably agree more than we disagree, but we all probably have slightly different definitions of what a 'macro bet' is. To me, it seems fair to think that matching duration with obligations IS the neutral bet, but that if you have good insight into what macro phenomena like inflation or future bond rates might be, then you can develop an argument about whether current rates compensate you for taking that risk or not. For a company whose bond portfolio is largely free of default risk (US, Canadian and European treasury bonds), I guess considering those macro events is most of what an active bond investor should be doing. And part should be also considering scenarios specific to the company (like megacat risk, or when funds are expected to be needed for buying out minority partners, for instance) that are strategic, not macro. Fortunately, Fairfax's managers have outstanding track records of positioning themselves well, so this kind of active investing makes a lot of sense for Fairfax.

-

Great, thanks. I guess that settles the question about whether the duration changes are a macro bet or not. The really amazing thing is that long rates are not already higher. With signs of lingering inflation, record deficit spending in North America and Europe, and a US president pushing for lower rates despite this, it seems like a reasonable bet, unless one thinks we are heading for a recession. But it is hard to argue that it is not a macro bet.