Leaderboard

Popular Content

Showing content with the highest reputation on 09/02/2023 in all areas

-

This is one of my favorite things to rant about so let me apologize in advance. This isn't a comment about Brett Horn in particular - I don't know him, and maybe he's great. But what I strongly recommend is to look to the broker analysts as a gauge of popular sentiment (if even that) or to understand how brokers drum up business. Nothing more. It is not a coincidence that companies reliant on capital raising tend to get the widest coverage and the best ratings. But since the ostensible separation of research from investment banking (and the removal of skin in the game - analysts ability to actually buy stocks in their coverage universe - in the name of removing conflicts of interest), the job is basically a glorified sales job for trading volumes. And many of them, if they do get a real nugget of information or have an actual insight, share it behind closed doors with whichever client trades the most through their bank. In other words... I wouldn't think that hard about it. The analyst incentive is to not stand out in a bad way and keep making ~$1-2mm/year to keep their kids in fancy schools. Even if one is actually bearish, he/she almost certainly won't stick his/her neck out and risk embarrassment and losing that cushy gig. Sorry, I've done that job as a bright eyed and bushy tailed junior analyst and unfortunately saw how the sausage is made, so maybe I'm too cynical now. Maybe the general takeaway is to keep your expectations low and allow yourself be pleasantly surprised, but the clear and simple fact is that @Viking and others with real insight and skin in the game do a 10x better job than any broker analyst. Maybe this wasn't the case in Lee Cooperman's days at GS (though it was probably even sketchier then) but it is now. At the bare minimum, the pay and prestige aren't what they used to be. The real talent is elsewhere. Expect the sell side estimates to keep climbing higher as Fairfax executes.2 points

-

With all due respect, Brett Horn has been a well acclaimed analyst at Morningstar for a long time. https://www.morningstar.com/authors/708/brett-horn "Horn holds a bachelor’s degree in business administration, with a concentration in finance, from the University of Wisconsin and a master’s degree in business administration from the University of Illinois. He also holds the Chartered Financial Analyst® designation. He ranked first in the business and industrial services industry in The Wall Street Journal’s annual “Best on the Street” analysts survey in 2013, the last year the survey was conducted." Recently, however, Brett Horn has been a polarizing figure among the Fairfax investor community. While most other analysts turned bullish on Fairfax, Brett has stood sturdy holding as a pillar of strength at the opposite pole. He has been publishing one report per quarter on Fairfax (FFH), within a few days of quarterly results coming out. This is what he said after 2023 Q1: https://www.morningstar.com/stocks/fairfax-earnings-both-sides-business-show-strength "Fairfax FFH reported a strong first quarter, with attractive results on both the underwriting and investment sides of the business. As a result, book value per share, adjusted for dividends, increased 7% from the year-end figure. However, we see nothing to alter our long-term view, and will maintain our CAD 730 per share fair value estimate for the no-moat company." After reading this, it appeared that the fair value estimate is too low as it is in CAD. I was wondering how will he able to save face if the actual results are too far off. What kind of tricks will be used? That is what I was wondering at that time. This is what he said after 2023 Q2: https://www.morningstar.com/stocks/fairfax-financial-earnings-strong-underwriting-margins-partially-offset-by-investment-losses "Fairfax Financial FFH reported a solid second quarter with relatively strong underwriting margins. However, this was partially offset by some investment losses. While the second quarter was weaker than the first quarter, Fairfax is having a good year so far, with book value per share up 11% since year-end, adjusted for dividends. We will maintain our CAD 790 fair value estimate for the no-moat company and see the shares as overvalued at the moment." So he quietly changed that fair value estimate to an apparently strategic number of 790 from 730 while maintaining that the fair value estimate was being maintained! I suppose in future he could change CAD 790 to USD 790 and still continue to "maintain" the fairness of estimate or Morningstar would simply assign a different analyst to cover Fairfax.1 point

-

Still not past the peak. I wonder if and by how much it effects the price of FFH in this period?

1 point

1 point -

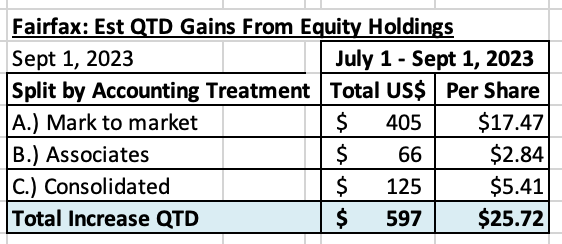

Fairfax's equity holdings (that I track) are up about $597 million so far in Q3 (9 of 13 weeks = 69%). Shaping up to be another quarter of solid performance. Split by accounting treatment can be seen below. I have attached my Excel file if you want a closer look. Top Movers? All up this quarter: Thomas Cook India = $156 million FFH TRS = $154 million Eurobank = $110 Broad based gains: 6 different equities are up more than $20 million Stelco = ($43) million: the largest decliner Fairfax Sept 1 2023.xlsx

1 point