All Activity

- Past hour

-

Great analysis as always @Viking. What’s interesting to me is that most professional active managers are using the “lost decade” as a basis for avoiding the stock. It’s the right strategy for most cyclical businesses as margins are more likely to mean revert to the last cycle lows. For Fairfax it means assuming interest rates go back to decade lows i.e. below the mean which is closer to where we are now and the equity portfolio which is filled with entirely different businesses has the same poor performance. Another wrinkle, that these managers miss is that along with the hedges, in 2012, Fairfax started adding more equity positions where they owned more than 20% which impacted the accounting returns negatively. Now that this strategy has matured, I believe it means structurally higher equity returns as investments that are sold book large gains and investments that are not contribute to ROE above 15%. Another headwind that has turned into a tailwind. I have a lot of confidence in predicting a floor for BVPS growth over the next 5 years. I have less confidence in predicting the P/B multiple but I suspect it will be difficult for it to go and stay below 1.2x for over a year. I also don’t think the multiple can get much above 1.4-1.5x unless we have another hard market. The good news is this will mean a lot of buybacks and strong contribution from the TRS as there will be no need to retire them.

-

This is going to take years and also only works for crude not the other goods that go through the SOH both ways. Also the pipeline and storage facilities are still vulnerable to attack. Just look at what happens in Russia. Mitigations can be developed but can only partly solve the problem.

-

Actually, you are not. That's how they got rid of the screwworm in the 1960's. It was essentially eradicated for the last 60 years. It infects open wounds in cattle, as well as humans. It could drive the cost of beef up significantly and has made its way up from South America over the last few years. It finally arrived in the U.S. about two weeks ago. It is a legitimate scourge and problem! Cheers!

- Today

-

Thanks as always, @Viking, for these fascinating posts. I am relatively new to FFH, but do remember being impressed at the time when Prem took off the hedges in 2016 after Trump got elected. I think we can all think of fund managers who became bearish, not unreasonably, but who have struggled to concede they were wrong, and have just stayed stuck with their convictions, underperforming. So while it was a painful decade, it is a great credit to them that they managed to recognise their mistake, and how things had changed, and reposition themselves. Cheers

-

Thanks for posting the interview

-

Whose troops are we talking about? Can’t be US since total service members across all branches amount to 1.35 million and latest estimates are that only 10 to 20% of that total actually serve in combat roles. Taking the high end of the estimate puts the current number of US combat soldiers worldwide at 270,000, far short of 1 million. And this includes combat members in all branches including the navy and the Air Force, meaning the available number of ground troops has got to be less than that. We could always reinstitute the draft and build up the combat force to a million, but that would take years and trillions of dollars to quadruple the current force and then send them all over to the Iran Iraq border. There’s a reason we only have 50,000 troops in the area. We can’t afford to send many more without denuding force levels elsewhere in the world. If the air and naval war doesn’t do the trick, I don’t think we have any good options to put significant numbers of boots on the ground in a country of 90 million.

-

@Maverick47, here is where the story gets even more interesting… 1. You lose $500 million for 11 straight years. 2. Lots of the equities purchased from 2014 to 2017 underperformed. 3. Interest rates are also very low for much of the time. And you still deliver a compound return of 4% over the 11 years. How did they do it? Fairfax has an exceptionally powerful business model. Just imagine what it is capable of if the company was firing on all cylinders?

-

Put 1 million troops on the Iraq - Iranborder and then ask for the enriched Uranium, see if they still like playing stupid games. I don’t even know if you need to go in, I think their own people might chase them off.

-

Excellent summary and overview of the “lost decade” for Fairfax @Viking! The discussion of trust between a company and its shareholders was apt as well. I think it was Richard Feynmann who said that the first principle of scientific analysis is “not to fool yourself”, and that one must also keep in mind that “you are the easiest person to fool”. It’s too easy as human beings and investors to remember evidence of our own superiority and outperformance and to ignore evidence of mediocrity and failure in assessing our own capabilities. I really enjoyed the juxtaposition of the two posts, first cheering the CDS episode with over a $2 billion positive return, followed by the decade long foray into shorting equity indexes and buying protection against the possibility of global deflation which resulted in a loss of more than twice the CDS gain, even before considering the opportunity cost connected with having to sell equities earlier than would have otherwise been the case. Had the $5 billion loss over a decade not occurred, and if the company had not been forced to leave over a billion of additional equity gains on the table by selling shares early, then we might consider that the purchases of companies such as Allied World and Brit could potentially have been funded by the lost profits and potential positive investment returns on those lost funds instead of requiring the issuance of about 7 million of common shares. We have all been happy that the repurchase of shares has essentially returned us to the same share count as before the Allied World acquisition, but imagine if those shares hadn’t needed to have been issued in the first place…. But if no mistakes had ever been made, the opinion of Mr. Market on the relative valuation of Fairfax shares would likely have been sky high…at nosebleed level prices for the entire period up until this very day, leaving me and others on this board with precious little opportunity to purchase shares again and again over the last 5 years or so at quite attractive prices. So as painful as the lost decade was, it sowed the seeds of a solid investment for me personally in the years since. I don’t have to bemoan the fact that I wasn’t around to buy Fairfax in 1986. Instead, I can be happy that I was able to buy it at reasonable prices for the most recent 5 years or so….

-

Well, I think the key point for a successor is that they now know that USA can't actually win a war against Iran without putting boots on the ground. Knowing it's all or nothing ought to impact their decision-making.

-

I’m not an expert in solvency regulation or insurance portfolio strategies, but an internet search did provide some indication that there may be perceived value in convertible bonds for insurer investment portfolios: https://aamcompany.com/wp-content/uploads/2022/08/Convertible-Bonds-A-Compelling-Investment-for-Insurers.pdf I don’t personally recall the insurers I worked for in my career having a significant (or indeed ANY) investments in convertible bonds. I do think that with Fairfax we see the benefits of long term relationships between management and the folks they partner with for investment purposes. What kinds of convertible bonds have we seen with Fairfax? Orla, Poseidon? Off hand I can’t think of other examples. But these are probably deals made directly between Fairfax and the companies themselves as opposed to convertible bonds that are publicly traded and which any investors, including ourselves, could purchase on the open market. The only other significant use of this sort of creative financing that comes to mind is with Berkshire when they provided investment support to companies after the Great Financial Crisis. With Bank of America, for example, I think Buffett provided something like $5 billion in capital structured something like a preferred stock earning a fixed dividend rate at 6% annually, but which was convertible into common equity at the then market price of $7.14 per share. At some point years later, when the dividend rate on the common stock had risen to roughly equal the $300 million per year that Berkshire had been enjoying on their preferred, they exercised their conversion rights, and they now hold $28 billion or so worth of BAC common shares earning $560 million per year of dividends. But other insurers and investors did not have the same ability as Berkshire to make these sorts of investments, which depended solely on the credibility Buffett and Berkshire had to make a financing deal directly with Bank of America. This is one more reason why I am happy to own shares in Fairfax, which has been run by Prem Watsa for over 40 years now. He has been building relationships with investment partners all over the world and thus has opportunities to make the sorts of creative financing agreements and investments with those partners that I can participate in vicariously as a shareholder.

-

-

There's a reason deflation hasn't happened since the Great Depression and that inflation was the escape valve (devaluing against gold and then mass austerity of personal consumption to rebuild savings and investment in the war effort). Once we found Keynesian religion, and realized we could just print our way out of any mess (or default against the obligations of a hard currency), we did. I used to think along the same lines as you - that debt was deflationary. And it is - for anyone who can't print their own currency. But we're the latter and currently have forced buyers of the USD regardless of how much we print (at least for now), so deflation aint going to happen. Not to mention that other infrastructure in the area has been damaged/destroyed by Iran and nothing says new infrastructure wouldn't be under similar threats. I don't know what the right price for oil is - but if we could hit $150/barrel in 2008, I don't see why $150/barrel today is out of the question. It would still be a significantly lower inflation adjusted top from 2008, comparable to the Russia/Ukraine episode, and reflects the ongoing supply shock, the increased insurance premium, AND that nations will need to rebuilt some level of inventories even if traditional drivers of demand fall off. If oil wasn't going to head higher, I don't know why we're doing all of these reserve releases and jawboning trying to prevent it. I think it's clear that the price has been artificially suppressed and the only questions are by how much, and for how long, and how high will it go when that suppression stops.

-

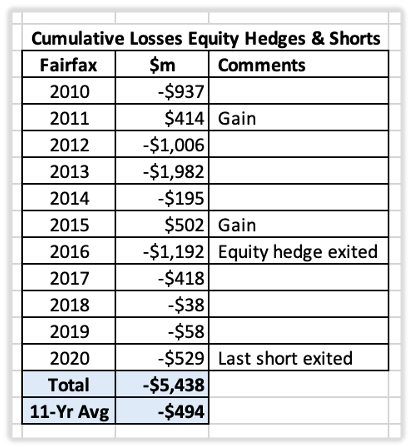

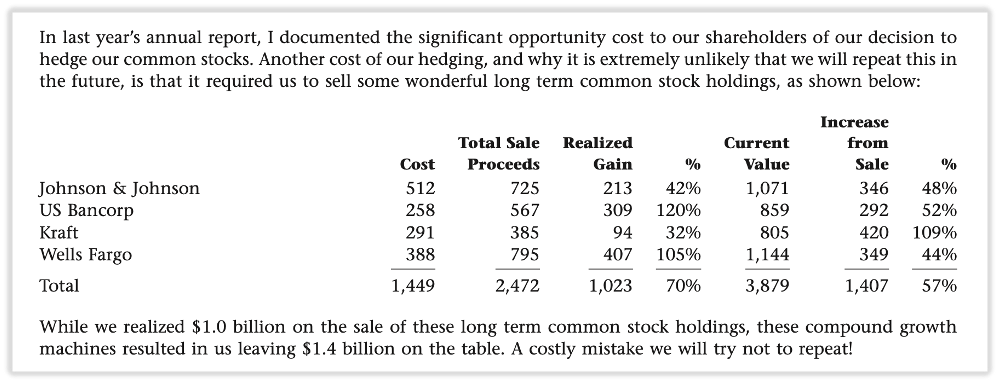

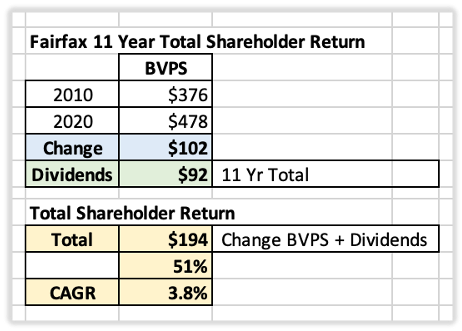

Equity Hedges and Shorts: Fairfax’s The Lost Decade (2010 to 2020) This is the sister article to the one I wrote yesterday. Fairfax's Version of The Big Short. Scroll up to read it. When Risk Management Became a Macro Bet “Those who cannot remember the past are condemned to repeat it." (George Santayana) What was Fairfax’s largest investment mistake? The equity hedge and short positions it maintained for much of the decade following the financial crisis. Between 2010 and 2020, Fairfax lost approximately $5.4 billion on its equity hedge and short strategy—roughly $500 million per year. To put that in perspective, Fairfax's shareholders' equity was about $7.7 billion at the beginning of 2010. The losses were significant. The opportunity cost was even greater. Capital remained tied to a bearish thesis while global equity markets enjoyed one of the strongest bull markets in history. Along the way, Fairfax was forced to sell some successful investments, limiting the benefits of long-term compounding. In Peter Lynch's language, some of the flowers were cut while many of the weeds remained. For shareholders, the result was a lost decade. Prem’s comment from Fairfax’s 2017AR Why Fairfax Put on the Trade To understand the mistake, it is important to understand why it was made. The roots of the strategy can be traced directly to Fairfax's greatest investment success: its credit default swap (CDS) position during the financial crisis. Between 2005 and 2009, Fairfax generated more than $2 billion in profits by correctly anticipating severe problems in the global financial system. That experience shaped management's outlook. Following the crisis, Fairfax became increasingly concerned that developed economies faced a future of excessive debt, weak growth, and deflation. In Fairfax's 2010 Annual Report, Prem Watsa wrote: "We worry that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990." If that scenario unfolded, equity markets could struggle for many years. To protect shareholders, Fairfax steadily increased its equity hedges until much of its common stock portfolio was effectively insulated from a major market decline. Viewed from 2010, the concerns were understandable. The financial crisis was still fresh. Government debt levels were rising. Economic growth remained sluggish. Central banks were experimenting with unprecedented monetary policies. Many thoughtful investors shared similar concerns. The problem was not identifying risk. The problem was what happened next. “2010 was a disappointing year for HWIC’s investment results because of the two factors mentioned earlier. Hedging our common stock investment portfolio cost us $936.6 million or $45.61 per share in 2010. Our hedging program masked the excellent common stock returns we earned in 2010, of which a significant amount was realized ($522.1 million). We began 2010 with about 30% of our common stock hedged. In May and June, we decided to increase our hedge to approximately 100%. Our view was twofold: our capital had benefitted greatly from our common stock portfolio and we wanted to protect our gains, and we worried about the unintended consequences of too much debt in the system – worldwide! If the 2008/2009 recession was like any other recession that the U.S. has experienced in the past 50 years, we would not be hedging today. However, we worry, as we have mentioned to you many times in the past, that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990, during which nominal GNP remains flat for 10 to 20 years with many bouts of deflation.” Prem Watsa – Fairfax 2010AR What Happened The feared outcome never arrived. Instead, the U.S. economy recovered. Interest rates remained exceptionally low. Central banks injected massive liquidity into financial markets through quantitative easing. Governments ran large fiscal deficits. Corporate profits expanded. Technology companies flourished. The result was one of the longest and strongest bull markets in modern history. Fairfax, however, remained largely committed to its bearish positioning. Over time, what began as a risk-management tool gradually evolved into a large macroeconomic bet. That distinction matters. Risk management seeks to protect against adverse outcomes. A macro bet depends on a specific economic forecast being correct. As the years passed, the line between the two became increasingly blurred. What Went Wrong? Many of Fairfax's concerns proved reasonable. Debt levels were high. Economic growth was sluggish. Central-bank policies were unprecedented. The world did face meaningful risks. The mistake was not recognizing those risks. The mistake was position size, duration, and flexibility. The hedges eventually became so large that they dominated Fairfax's investment results. The positions were maintained for more than a decade despite mounting evidence that the original thesis was not playing out. Most importantly, Fairfax underestimated the willingness and ability of governments and central banks to support economic activity and financial asset prices. The result was a decade of disappointing investment performance. The direct losses totaled approximately $5.4 billion between 2010 and 2020. The indirect costs were equally significant: Missing much of a historic bull market. Prematurely selling successful investments. Slower growth in earnings and book value. Significant damage to Fairfax's reputation. The loss of many long-term shareholders. The impact on shareholder returns was dramatic. Book value per share increased from $376 in 2010 to $478 in 2020. Including dividends, Fairfax delivered a total return of approximately 51%, or 3.8% annually. Over the same period, the S&P 500 generated a total return of roughly 332%, or 14.2% annually. Exiting the Trade Fairfax exited the strategy in stages. The broad equity hedge program was removed near the end of 2016 following the U.S. presidential election. In Fairfax's 2016 Annual Report, Watsa explained: "Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions..." Several individual short positions remained, however, and continued to lose money. By 2019, Watsa publicly acknowledged the mistake: "Shorting is dangerous, very short term in nature and anathema to long term value investing." After another $529 million loss in 2020, Fairfax finally closed its remaining short exposure. The decade-long experiment was over. A Turning Point The removal of the hedges and shorts eliminated a significant drag on Fairfax's earnings power. For more than a decade, the strategy had cost shareholders roughly $500 million per year. Once the positions were closed, that headwind disappeared. The improvement in Fairfax's results after 2020 was driven by many factors, but the elimination of the hedge program was undoubtedly one of them. Investors evaluating Fairfax after 2020 were looking at a different company—one no longer burdened by a large and persistent negative carry. Why Did It Persist? No outsider can know with certainty. My best explanation is that Fairfax's extraordinary success with credit default swaps reinforced management's confidence in its broader macroeconomic outlook. Ironically, the same mindset that produced one of the company's greatest investment successes may also have contributed to one of its largest mistakes. That pattern is common in investing. Success builds confidence. Sometimes it builds too much confidence. Lessons for Investors The equity hedge and short strategy offers several important lessons. In many ways, they are the mirror image of the lessons from Fairfax's highly successful CDS trade. First, risk management can become dangerous when it evolves into a macroeconomic forecast. What began as a hedge gradually became a large bet on a specific economic outcome. Second, position size matters. The hedges eventually became so large that they drove Fairfax's investment results. Third, duration matters. Even a sound thesis can become extraordinarily costly if maintained for too long. Fourth, investors must adapt when facts change. Fairfax was slow to adjust as markets, economies, and policy responses evolved. Finally, trust matters. The strategy did more than cost shareholders billions of dollars. It damaged confidence in management's judgment and led many long-term investors to leave. Financial losses can eventually be recovered. Trust usually takes much longer. As Buffett has observed, companies tend to get the shareholders they deserve. Fairfax has long said it wants long-term shareholders. If that is the case, management must uphold its side of the relationship. From 2010 to 2020, it failed to do so. To management's credit, the mistake was eventually acknowledged, the positions were closed, and the company moved forward. Fairfax's performance since 2020 suggests the lessons were learned. That may be the most important takeaway. Every great investor makes mistakes. What separates the best from the rest is their ability to recognize them, learn from them, and avoid repeating them. ------------ Comments from Prem and other notes from Fairfax’s 2016AR. Prem discusses the reasons for exiting the equity hedges. He also provides a summary: from 2010 to 2016, total losses from equity hedges were $4.4B. These were offset by net gains on stocks of $2.7B and bonds of $2.2B. Fairfax’s investment portfolio had been performing very well. "Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions and reducing the duration of our fixed income portfolios to approximately one year – all of which resulted in a $1.2 billion net loss on our investments in 2016 which, in turn, resulted in a loss in 2016 of $512 million or $24.18 per share." "When we removed our hedges near the end of 2016, we realized a loss of $2.6 billion in 2016, but that included $1.6 billion which had gone through our statements in prior years. As discussed earlier, since 2010 we have had $4.4 billion of cumulative net hedging losses and $0.5 billion of unrealized losses on deflation swaps (which we still hold), offset entirely by net gains on stocks of $2.7 billion and net gains on bonds of $2.2 billion. The volatility of our earnings caused by our hedges and long bond portfolios is over – and as I said earlier, we are focused on once again producing excellent investment returns." Prem Watsa – Fairfax 2016AR Equity contracts: “Throughout 2015 and most of 2016, the company had economically hedged its equity and equity-related holdings (comprised of common stocks, convertible preferred stocks, convertible bonds, non-insurance investments in associates and equity-related derivatives) against a potential significant decline in equity markets by way of short positions effected through equity and equity index total return swaps (including short positions in certain equity indexes and individual equities) and equity index put options (S&P 500) as set out in the table below. The company’s equity hedges were structured to provide a return that was inverse to changes in the fair values of the indexes and certain individual equities.” “As a result of fundamental changes in the U.S. that may bolster economic growth and business development in the future, the company discontinued its economic equity hedging strategy during the fourth quarter of 2016. Accordingly, the company closed out $6,350.6 notional amount of short positions effected through equity index total return swaps (comprised of Russell 2000, S&P 500 and S&P/TSX 60 short equity index total return swaps). The short equity index total return swaps closed out in 2016 produced a realized loss of $2,665.4 (of which $1,710.2 had been recorded as unrealized losses in prior years). The company continues to maintain short equity and equity index total return swaps for investment purposes, and no longer considers them to be hedges of the company’s equity and equity-related holdings. During 2016 the company paid net cash of $915.8 (2015 – received net cash of $303.3) in connection with the closures and reset provisions of its short equity and equity index total return swaps (excluding the impact of collateral requirements).” Fairfax 2016AR

-

Please refer to my above message from Trump. Since you were not invited to the big boys table, your country is throwing a tantrum. Enjoy the muzzle

-

The muzzle has officially been secured on this rabid dog - now we can finally discuss peace.

-

Well, Trump wrote "The Art of the Deal" and knows full well that when the "spirit" of a deal is lacking by one or both parties, there is no deal. The US and Israel would happily live up to any deal that removes all threats. Problem is, the objective of the other side is death and destruction so there can never be a proper spirit by the present Regime. The only parties that recognize this are those under threat. That is why Israel's objective remains regime change and no deal with the current cast of characters will change that.

-

Totally agree. There may be some good or bad cop performance here. Bibi is going to have to do what he has to do. Trump would never stand for anyone telling him he can't retaliate if missiles were lob in from Canada. I'm convinced there is a plan B that will not be to the liking of Iran. My guess was that no agreement/MOU would be signed, precisely because the IRGC knows it is a surrender document and they would be dead. I'm still waiting for Kid's document to show up.

-

The difficulty with deals can be neatly summed up in what has taken place this morning. Hezbollah resumed its attacks on Israel and Israel responded. Trump then posts on social media that Israel should not have responded because Hezbollah's attacks were "meaningless" since they didn't harm or kill anyone. It is perfectly understandable why Trump may feel this way because he wants to sign a deal but since when are attacks on your neighbor meaningless when the intent is there to harm, kill and inflict damage, and since when is it not appropriate for the neighbor respond? The fragility of this negotiation makes a deal completely unworkable IMO for the simple reason that whoever may sign a deal on behalf of Iran has no control over what transpires next within the Regime or its terrorist proxies. To believe that everyone just packs up and goes home once the ink dries on a deal is about as naive as it gets. Trump knows all this of course, so have to believe there is an immediate Plan B for when (not if) the deal fails.

-

^^ Good enough. All I can say is that after the Berlin Wall fell, it took 2 years for the Soviet regime to fall. So economic escalation with the Soviets did the trick. Bessent is conducting a masterful plan. And yes, domestic party politics seriously limit what Trump can do.

-

I run this one tiny separate account for free for a college friend of my Wife's and it's less than $60k. She has the best cost basis of CNSWF of anywhere I looked. It's a taxable account so not much trading at all for this account. Lets play: "are you diversified??"

-

To be fair, I own 5x as many CSU shares in Canada at the 2672 cost basis than I do CNSWF shares in USD at the 1702.87 basis. But I'll take it

-

Maybe, but I think it took a non-politician like Trump to even attempt to pull this off and he still gets bogged down in politics. Trump's further advantage is no one can predict what he will do tomorrow and the next day, which frustrates everyone but his ardent supporters in this endeavor. The problem with economic strangulation is it doesn't appear to work. Liars and cheats know how to steal money when they need it and the IRGC only cares about itself, not the population at large so they don't need as much money as one might think. Applying a "Western mentality" to solving the Iran problem has long been a failing approach. We have to deal with them on their level - force and destruction, nothing less.

-

If you get JD Vance or Rubio in as POTUS, I really think Israel is in great shape. The way Trump/Bibi have conducted this campaign is masterful. We all know the limitations on the USA is "loss of American life". Much, much different than Israel, which is in a fight for its very survival. That's where the 2 countries diverge, but Israel is no doubt our greatest ally after the disgraceful Europeans. Economic strangulation is easy enough for the USA. Bombing makes things more painful- but a year or so of a US blockade, whether intermittent or not is going to inflict maximum damage on Iran. Of course, my humble opinion.

-

The issue is not so much now but more so after Trump has either left office or lost power. Skeptical (at best) that any successors will have the same gumption since none of his predecessors did. My guess is Israel will once again have to go it alone or with passive assistance from the US. Iran not only lies and cheats but they are sincerely stupid. Just ask Egypt and Jordan whose agreements with Israel have lived on for decades after an entire history of war. You just can't change stupid unless you remove and destroy them.