realassetsvalue

-

Posts

108 -

Joined

-

Last visited

realassetsvalue's Achievements

")

-

Your excitement and slow Friday is my gain! Thank you for the detailed response.

-

What are potential issues that can arise from getting credit exposure through ETFs as opposed to owning the underlying directly? For example, with the talk of TIPs above - what should a complete novice to the fixed income world be aware of if I would buy, say, the iShares TIPS Bond ETF (https://www.blackrock.com/us/individual/products/239467/ishares-tips-bond-etf) instead of actually buying TIPS?

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

realassetsvalue replied to thepupil's topic in General Discussion

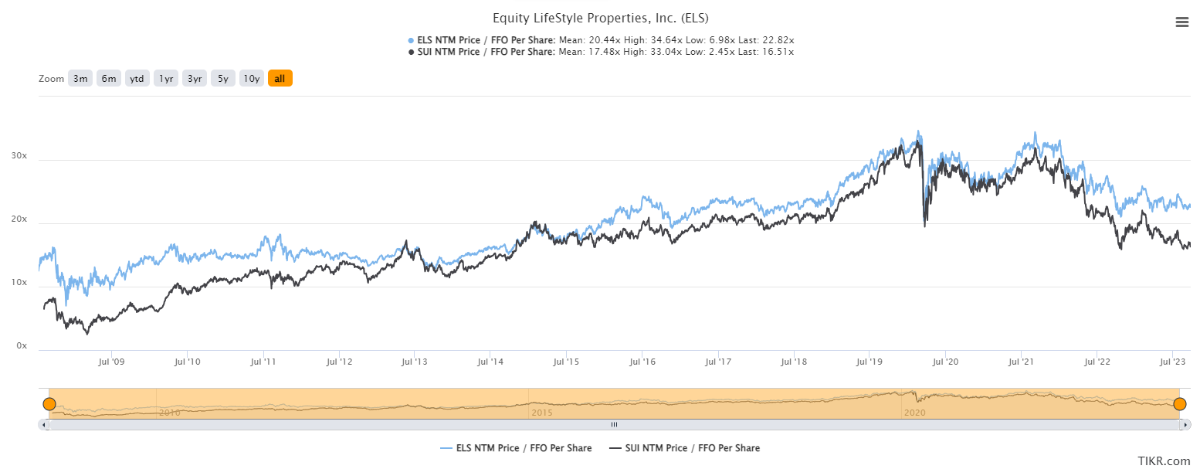

I think this view is going to help improve potential REIT returns over the next decade as the sector is going to screen terribly and is already looking very unloved by generalist managers. After this sell-off the backward looking returns are definitely bad and most REITs will look like they've added no value. A good exercise, which I am stealing from Rob the REIT guy at Hedgeye is to look at NAV per share over time based on a static cap rate. I haven't done this for ARE vs. VNO but I imagine it will reveal the difference in value creation between the two names. I suppose what I am grappling with is how to evaluate buying the smaller, less efficient, less well-manged but deeply discounted REITs today vs. the highest quality, slightly discounted REITs. ELME vs. the blue chip MF REITs is one example but there are many. If we are U/W ELME to a HSD / LDD IRR and say AVB to 100 or 150 bps inside of that is a base case, how much upside optionality from a buyout or other big change do we need to decide on the deep discount vs. the blue chip? The larger, well-managed, better capitalized REITs also have some optionality in this environment through growing externally through lower cost of capital. Also in a mean reversion to NAV or close to NAV (or slightly above based on the GS data), they're likely to revert faster than the smaller REITs due to flows? I am digging into this because buying the deeper discount has been a strategy that has worked for me but I am trying to refine my thinking and have a framework of weeding out value traps as there are many in small REIT land as we all know... This has been a thought provoking exchange and I am still figuring out where I come down. With the SUI vs. ELS debate (and there are some other smaller REITs in the space, albeit I think management and asset quality are way, way lower) - I also have come down on ELS, which I think is truly one of the few "never sell REITs" due to its regulatory barriers to entry of new supply in the MHC and to a lesser extent, RV and Marinas space. Good report on this out recently from Fannie Mae, the highlights of which are in this twitter thread. I have also not done deep work on SUI. It has gotten significantly cheaper than ELS - while has historically traded at a discount, this has widened (see below). I think their geographies in the US are not as good as ELS and the international and aggressive marinas expansion has lowered the earnings quality of their business. The international businesses in the UK and AUS are very different and don't have the same dynamics as US MHC. They made a play to be the biggest player in the Marinas business by acquiring Safe Harbor with less of a focus on annual revenue streams and including some super luxury yacht marinas that they bought for like $1m per slip. Someone who knows that business may have a better view than I but I think it's less stable and resilient (but am a tourist in the space).

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

realassetsvalue replied to thepupil's topic in General Discussion

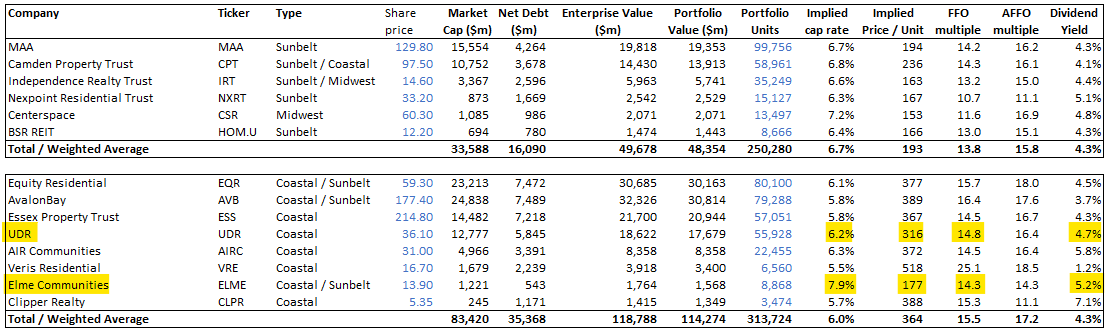

Have been thinking about ELME because when @thepupil gets serious about a real estate name, you should too. I have been thinking about this and the discount to NAV / peer set thesis here. It feels like relative to the private the assets, while not of the highest quality (we all know this) are undeniably cheap both on an implied cap rate and price / unit basis. The metrics below exclude the 600 Watergate office, which I value at an 8% cap rate so we can try to get closer to an apples to apples comparison for the multifamily assets. When comparing across the peer set, ELME is also cheaper from a portfolio point of view but a good amount of that cheapness is reduced by the scale of their business vs. their operating costs. For example, while not a perfect comparison, UDR trades at a 6.2% cap rate (~170 bps inside ELME) but a 14.8x FFO multiple / 4.7% dividend yield vs. ELME's 14.3x FFO multiple / 5.2% dividend yield. I'd argue that UDR has a better operating platform and you don't have to believe that UDR's same store rent growth / OPEX / CAPEX is much better than ELME's to make up that difference. Continuing the arbitrary comparison, there's also a cost of capital difference between the two companies. ELME doesn't have balance sheet issues and is arguably underleveraged but UDR has a very good balance sheet and greater access to lower cost capital through both debt and JV markets. I'd guess they have a better opportunity to play offense in the current cycle vs. ELME. This is a long-winded way to get at I think one has to take a view on the potential for either some sort of change in the market's evaluation of the company, its assets, markets, etc. or more likely, M&A to close the valuation gap between the portfolio valuation and private market / peers. I am not sure I am positive on management's desire to do this given they've staked their reputation and investing a lot of time, energy, and money into moving towards a pure play multifamily platform but the board may decide they've run out of rope at some point. A major reason I've gone through this exercise is trying to think through listed real estate positioning in this environment as opposed to the pre- and post- COVID low interest rate environment... As a recovering "NAV boi" who saw success seeing discounted small REITs get acquired by PE, now that the spigot of very cheap debt has been turned off, maybe the better hunting grounds are in larger, higher-quality (and as a result, more expensive) REITs with an operating platform / cost of capital advantage instead of deep discount to NAV / M&A targets. Definitely not arguing for all one or the other - and the best opportunities can offer both - but wanted to try to refine my thinking on this a little through the multifamily lens.

-

Where are you getting high yields on cash?

realassetsvalue replied to shamelesscloner's topic in General Discussion

Apart from money market funds I use the AAA CLO ETFs as "near-cash" equivalent. I park excess liquidity in CLOA - Blackrock's AAA CLO ETF but Janus Henderson has another one as well that is larger, JAAA I believe. Bears some credit risk but would have to be an apocalyptic scenario if the AAA tranches took losses (effectively never have historically). CLOA pays a ~6.5% yield and is floating rate with effective duration under a quarter and average maturity of ~3.7 years. -

The Swedish Corporate Real Estate Crisis [2022 to ?]

realassetsvalue replied to John Hjorth's topic in General Discussion

An Ilija Batljan domino has dropped - his HoldCo (Ilija Batljan Invest AB) sold the entirety of its interest in publicly-listed Logistea AB to Slatto, a Swedish real estate private equity manager focused on residential and logistics / industrial real estate. Logistea is a logistics-focused small-cap propco. The shares were sold at SEK 10.79 per share and the shares traded up ~3% - 5% on the news (A and B Shares respectively - differ often as both are pretty illiquid). Sale is subject to an 18 month repurchase option for half of the shares on the part of Ilija Batljan Invest AB. Press release: https://www.ilijabatljaninvest.com/en/forsaljning-av-aktier-i-logistea-ab/ Other major Swedish RE interconnected shareholders - M2 (Rutger Arnhult), which has significant debt issues, and Dragfast, which does not - are significant owners of Logistea so there may be more shoes to drop. -

The Swedish Corporate Real Estate Crisis [2022 to ?]

realassetsvalue replied to John Hjorth's topic in General Discussion

As an investor focused on listed real estate, I did some poking around a bunch of these Swedish property company names over the weekend. I tend to be more interested in smaller companies in sectors where the fundamentals are easier to get comfortable with, which I see as being industrial and residential for Sweden as vacancy rates are low, rents are stable and / or rising, and there aren't existential threats on the horizon that you have to get comfortable with. You do have material new supply in each of these sectors, which has to be taken into account... Across the board, the biggest issue for all these cos is that commercial property debt seems to have 3-5 year terms - both bank debt and bonds. This results in a 2-3 year average maturity with most companies seeing material maturities in the next 12 months that will have to be addressed. On the plus side, some of these smaller companies have sensibly eschewed dividends to focus on external growth, which provides for some capacity to delever over time. The question in my mind is how to think about where the opportunities will emerge given (A) the listed sector looks to be significantly over-leveraged and (B) the cross-holdings of these Swedish property tycoons). Focus on babies getting thrown out with the bathwater - smaller listed propcos not tycoon controlled that are selling off as investors flee the sector? Look for consolidators - larger firms that have the capacity to gobble up distressed properties owned by other overleveraged listed propcos? Develop a short-list of cos with good assets but broken balance sheets and be ready to potentially buy opportunistically as they recapitalize their balance sheets (already seeing a number of firms buy back bonds, initiate equity raises )? Feels like avoiding the battlegrounds - the SBBs, Castellums, Corems, etc. - is worth it for a non-Swedish investor like myself who will always be behind the informational curve... -

Green Streets materials, methodologies, and webinars (they do many for free) have been very formative for me as I have learned about investing in REITs. I have attached a couple of documents of theirs - their explanation of their valuation framework, how its changed, and a glossary of terms - I have found useful through the years. A controversial and perhaps counterintuitive starting point is that in my expiernce investing in REITs with high dividends usually leads poor total returns. I find "high yield REITs" to be an unattractive pool to fish in. Oh and follow @thepupil, @Gregmal and @BG2008 on here and twitter for ideas and the pragmatic side of REIT investing. Good hunting! green-street-advisors-glossary-of-commercial-real-estate-terms.pdf IntrinsicNAVModelExcerpt_GreenStreet.pdf RE-07-07-Green-Street-NAV-Methodology.pdf

-

High Quality Multi-family REITs - EQR, CPT, ESS, AVB

realassetsvalue replied to thepupil's topic in General Discussion

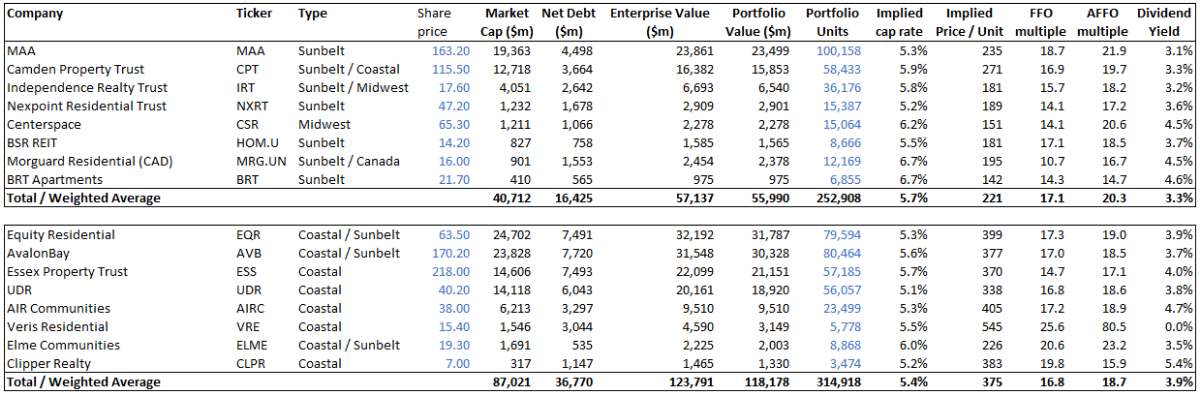

Now that all the major US MF REITs have reported, implied valuation metrics (including today's big move up for REITs) are below... Simple guesstimates for the value of other assets / property types owned so this view might be different than a more detailed U/W of Veris, for example. Camden is a noticeable outlier within the more sunbelt focused REITs from a valuation perspective and Essex is slightly cheaper than either AvalonBay or Equity Residential. MAA has probably gotten expensive relative to the coastal REITs given the lower barriers to entry in their markets. Pupil's reasoning on Essex vs. the other guys makes sense to me. Worth noting that development and other assets are 3% - 4% of EV for both AVB and ESS but ~1% for EQR.

-

Buying real assets denominated in Euros

realassetsvalue replied to Red Lion's topic in General Discussion

I think there are potentially interesting opportunities in this area as you have falling currency plus weak public market prices in general creating a double whammy. Big issues are that yields are low (private market yields for virtually everything Class A are in the 3s or lower) and while I'm macro-ignorant, the European economy is clearly worse off than the US. For example, Capital Economics have continued to say their house view for the US is no recession but very high chance of European recession. Then there are idiosyncratic issues - especially around energy - which are much publicized, but one should think how those will impact landlords and tenants. For example, Vonovia's CEO said that the hike in energy prices they will need to pass through to their tenants will be on the order of 2 months of rent - that sort of thing can really impact affordability. All that being said, sectors that look most interesting to me are unsurprisingly apartments and industrial / logistics. Office yields are super low and while market fundamentals seem to be doing better than the US, I by and large the risk reward doesn't look great. Starwood and Brookfield have taken out a couple office REITs in the last couple years (Alstria, CA Immo) so clearly they see some value / opportunity to put capital to work. Retail tends to be heavily mall centric so I haven't found anything terribly interesting there and faces the giant sucking sound of e-commerce penetration gains. In multifamily - Vonovia and LEG in Germany (with some Swedish and Austrian exposure) seem worth researching. There are a couple REITs managed by CAPREIT, the Canadian REIT, focused on Ireland and the Netherlands to check out. In industrial - I think Segro (mostly UK but some European exposure as well) and VGP are interesting for different reasons. Segro due to infill / urban heavy portfolio and VGP due to a really attractive development model. Not exactly real estate but speaking of European exposure, I think Radius Global is very interesting. Large European exposure but USD denominated so currency moves is a negative, albeit hedged to a degree by debt. What makes it interesting is ground lease to cell tower REITs and operators represent secure, long-duration income stream and their indexation terms are favorable with the majority being linked to CPI and uncapped. Have to get comfortable with what you own (land or long-term lease interests in rooftops, distributed antenna systems, edge DCs, etc.) but pretty interesting and supposedly running a takeout process. Deutsche Telekom's tower business just sold 51% at a ~27x EBITDA multiple and Radius trades much cheaper than that. Not an exact comp (Radius is senior to TowerCo CFs but doesn't have the same ability to add tenants to their towers, which has very attractive ROIICs) but a reference point. Would love to hear what other ideas people find interesting. Happy hunting! -

Oh good to know - thanks!

-

Is it a feature of being based in Canada / only accepting Canadian investors that White Falcon is able to charge an incentive fee on SMAs? This is not possible in the US I believe?

-

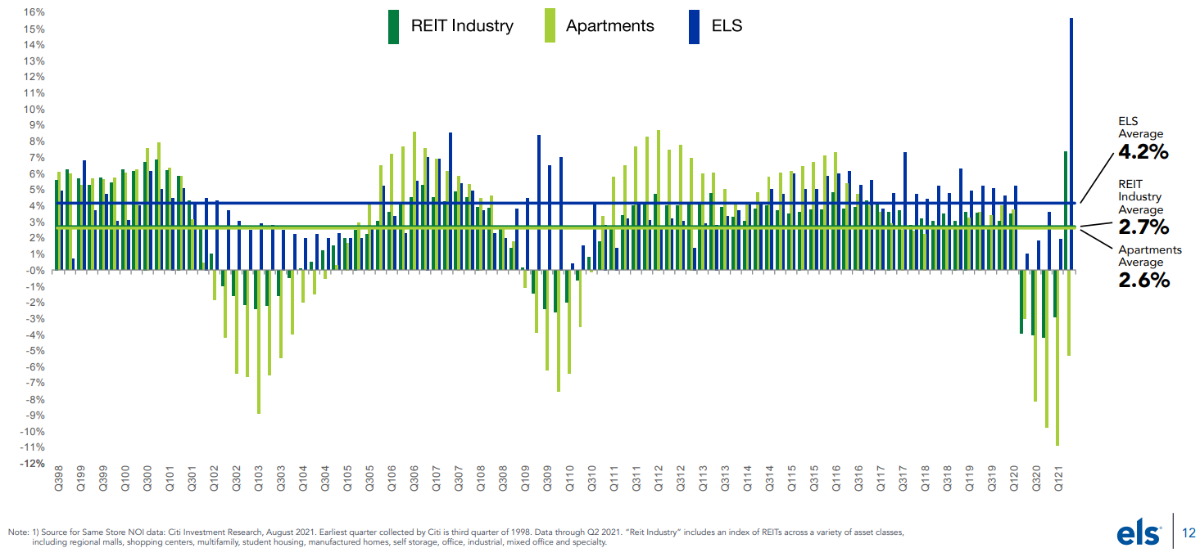

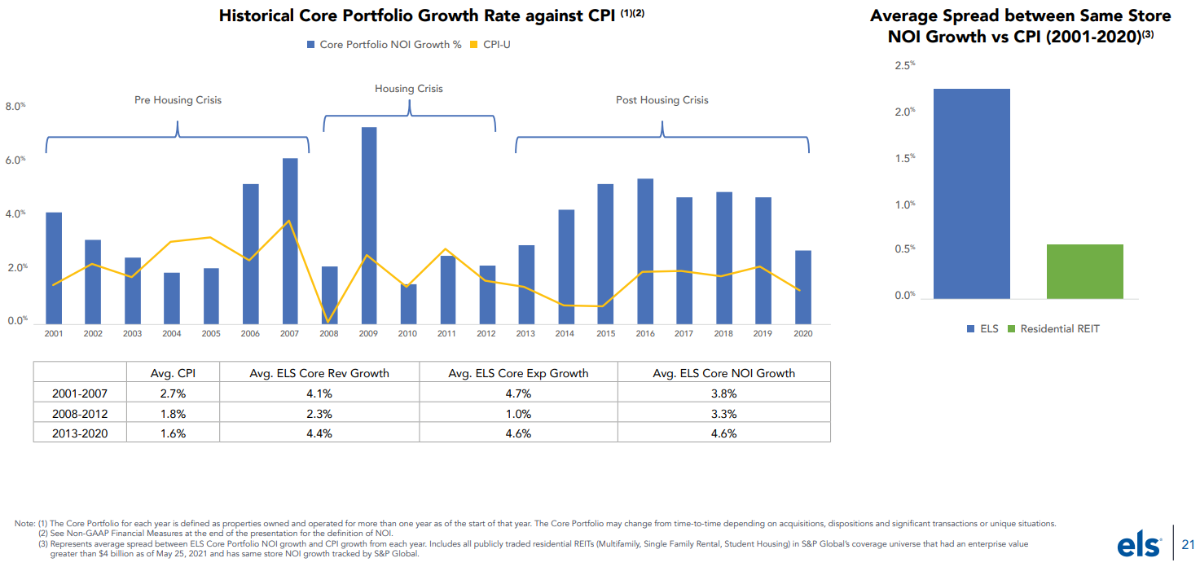

Equity Lifestyle Properties, who own manufactured housing, RVs, and Marinas, have a good LT chart of multifamily and REIT same store NOI growth. I think a base rate of ~2.5% NOI growth rather than 4% NOI growth is a better starting point. We're in a great environment now and some markets are blowing up so 4% feels conservative but historically, it is not over a full cycle. Obviously ~2.5% NOI growth over 30+ years is still good but doesn't beat inflation by a whole lot. Again, I'm leaning on the ELS data and they are trying to paint multifamily / SFR as a worse asset class so take this info with a grain of salt. I think there is a good dose of exuberance going around due to the numbers that the MF REITs are posting for rental growth - a lot of which is justified (rents are going up a lot over the next couple of years) but a lot of which is also probably cyclical. High rents and low cap rates will likely pull forward a lot of supply as developers rush to get in the game while the going is good - especially in sunbelt markets where there really aren't that many barriers to entry. I like the prospects for US multifamily a lot over the next 3-5 years and the same for industrial but think its important to watch the supply-demand dynamics in the markets you own in as these trees can't just grow to the sky.

-

Facebook buys the brand new 400,000 sq ft building in Bellevue that REI built as their HQ after REI decided not to occupy for $370m, ~$925 PSF: https://www.seattletimes.com/business/real-estate/facebook-will-buy-former-rei-headquarters-in-bellevue/