SHDL

-

Posts

689 -

Joined

Content Type

Profiles

Forums

Events

Everything posted by SHDL

-

Not to derail the thread, but I actually think you can. For instance I have like $200 sitting in my file cabinet, it’s been there for years, and it likely will be there forever. If the government takes that away and hands it out to 10 alcoholics on the street I’m reasonably sure most of them will spend it on their liquor of choice within a day or two. I guess we can reasonably call that “demand creation.” Now if the government finances the handout by printing money instead, things become a bit more complicated but more or less the same thing should happen in the end. The only difference is that my cash holdings gets diluted by the money printing instead of going down in nominal terms by government confiscation. Now whether that’s good government policy is another matter … which I guess we can all have fun talking about in the Politics section.

-

They basically take a weighted average by spending. The big picture is that services (esp. things like healthcare and education) have gotten much more expensive while goods (like electronics and such) have gotten cheaper especially on a quality adjusted basis. The trade issues have the potential to disrupt the latter trend and create an uptick in overall inflation. There are measurement issues for sure but I don’t see any evidence that supports a conspiracy theory...

-

On bonds and inflation, I’m personally seeing a number of inflationary forces building up as we speak: - The recent jobs numbers suggest that we’re now at full employment and that any further uptick in job creation will likely come with wage inflation. - The Trump tax cuts likely had a temporary deflationary impact in industries where their benefits are being competed away and passed on to consumers. This effect should diminish in the near future. - The Fed rate hikes during 2018 seem to have artificially strengthened the USD, and if that starts reversing we should see an increase in import prices. - Tariffs are obviously inflationary. - We’ll see what happens with Iran but any turmoil in that region is most likely a positive for oil prices and thus also inflationary. - There are quite a few companies (like Uber & Lyft) that look like they really need to start raising prices soon if they are to survive. If we do get material inflation, bonds will likely sell off and the Fed will probably have no choice but to raise rates. This is something to watch out for, as it is among the worst things that could happen to this market.

-

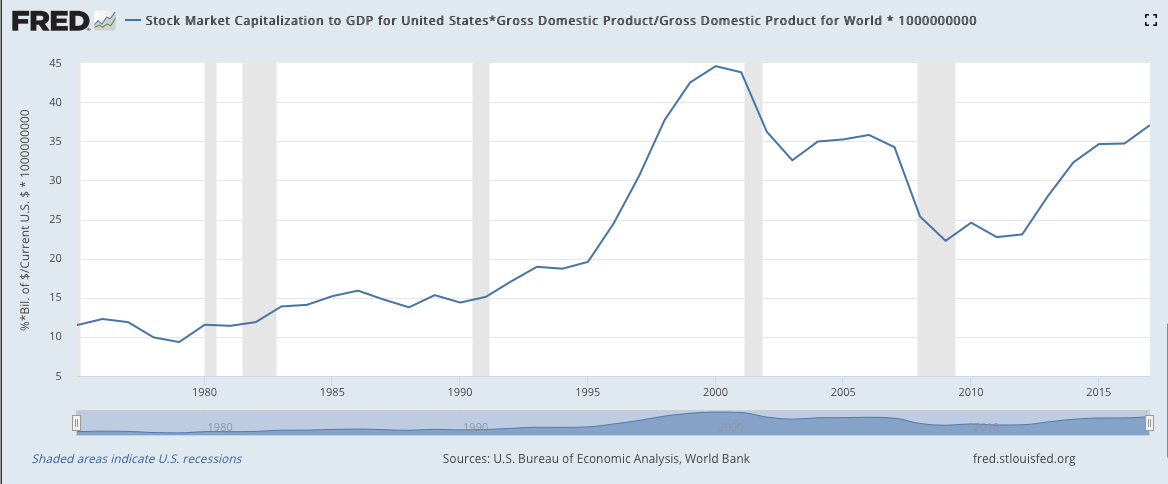

Is that metric useful? US companies are much more global than they were. https://twitter.com/teasri/status/1142201221626941440?s=21 GDP and GNP are typically very similar, which I agree is counter-intuitive. FED graph attached. The numbers on the graph are $21,285 billion for GNP, $21,048 billion for GDP. Alternatively one could divide by world GDP (instead of US GDP). In 2017 that ratio was around 37%, close to where it was in 1998. I don't have more recent numbers but my guess is that it hasn't changed that much. The 2000 peak was a hair below 45%. See the attachment for a chart.

-

Market cap to GDP strikes me as one of the poorest metrics I can think of. The reason is simple, in some countries a lot of companies tend to stay private, in others they are owned by the government. The market cap to GDP would be lower, just because these companies don’t trade on the stock market. i would ja it stick with simple valuation metrics, EV/EBIT, EV/ Revenue etc, but market cap to GDP strikes me as a very poor metric. Right, that’s one of several caveats to keep in mind when looking at this metric. With regard to its implications, the general trend in the US over the last two decades has been that more and more companies have chosen to go/stay private, and so if you combine that with where the market cap to GDP ratio currently stands, it probably means that the total value of US companies (public and private combined) is higher than it’s ever been relative to US GDP.

-

Yes, this is probably the most important similarity. The second most important similarity I think is this huge wave of IPOs, which strongly suggests that insiders and other very well-informed people think this is a great market to sell into.

-

WayWardCloud, In a humble manner I will suggest that they are perhaps hard to spot because they stand behind others. If you read the last shareholder letter by Larry Fink you'll see that he is of the opinion that there is an urgent, almost desperate, endless & ever growing/expanding need for help. If you read the shareholder letter, please bear in mind what Mr. Buffett has written about helpers. Perhaps that also leads to the conclusion that those people are not optimistic, more like "un-opinionated" [<- or something like that]. That’s probably right. The vast majority of people I know aren’t necessarily euphoric but they’re not paying any attention either and they have their investments on autopilot, which for many of them means they put pretty much of all their monthly savings in VOO (or an equivalent) without even thinking. Combine that with the massive, price insensitive share buybacks by the companies and throw in a few quant/momentum traders, and you have quite a group of buyers.

-

I think your take is actually pretty close to the Fed’s baseline forecast, namely the economy does fine and they don’t cut during 2019. The reason they’re slightly more dovish than what you think is appropriate is that they now see some negative economic indicators showing up and inflation is undershooting their target. What I find pretty strange is the extreme confidence with which the bond market is predicting multiple rate cuts this year and how happy Mr (Stock) Market seems to be about all this. The Fed has pretty much indicated that rate cuts are not forthcoming this year unless the economy starts deteriorating. So if the bond market is right and rates are going down big time that means the economy is going to do pretty badly. Will stocks do great under such circumstances? I don’t think so. Either everything is good news or everything is bad news. Right now it’s a former. Lesson of the day: Mr Market don’t understand if statements.

-

I think your take is actually pretty close to the Fed’s baseline forecast, namely the economy does fine and they don’t cut during 2019. The reason they’re slightly more dovish than what you think is appropriate is that they now see some negative economic indicators showing up and inflation is undershooting their target. What I find pretty strange is the extreme confidence with which the bond market is predicting multiple rate cuts this year and how happy Mr (Stock) Market seems to be about all this. The Fed has pretty much indicated that rate cuts are not forthcoming this year unless the economy starts deteriorating. So if the bond market is right and rates are going down big time that means the economy is going to do pretty badly. Will stocks do great under such circumstances? I don’t think so.

-

I bought some hedges and trimmed/sold some of my longs. The macro setup now rhymes with 1999 for sure, but it’s not only that, there’s also a lot of financial leverage out there like there was pre-GFC (this time via corporate debt), and on top of that we have potentially large supply-side shocks coming our way like we did in the 1970s (this time via tariffs and possibly Iran). In a sense we have a little bit of everything from the worst recessions and bear markets in recent memory.

-

A few comments: 1. As several posters suggested above, I would first focus on self studying and learning by doing (with a small portfolio). Without that background and experience you will most likely have trouble identifying who is a good mentor for you and who is not. This is important because picking the wrong guy for this job could be disastrous for your finances. 2. The other posters are right that most people will not outperform the S&P over the long haul. But I’m not sure if that means “put everything in VOO and forget about investing” is the right thing to do. It might be, but my guess is that it is not. If you’re retired your financial goals are probably more about minimizing the chances of running out of money while you withdraw $x per year as opposed to getting the highest possible CAGR over a 20 year horizon. That probably means there’s a place for bond-like instruments in your portfolio. But which instruments, exactly, and how much of your financial wealth should you allocate toward them given where interest rates, stock valuations, etc, currently stand? You probably won’t have a good answer to these questions without actually studying and thinking about this stuff — which goes back to point 1.

-

Yes, that's exactly how I feel about this. Although, my sense is that Fat Pitch knows more about this area than the modal speculator, which is why I asked.

-

I will sell my shares the moment they do that. Happy to do so - at least until someone changes my mind. ;) I'm open btw to the idea that this technology could lead to something useful, but I don't see why that makes Bitcoin a good investment. Maybe you can enlighten me and the other skeptics around here.

-

I will sell my shares the moment they do that.

-

He did another interview with CNBC today: https://www.cnbc.com/video/2019/06/07/stanley-druckenmillers-full-cnbc-appearance-squawk-box.html

-

They aren't. GDP has always been a flawed measure of prosperity because it doesn't count things that are "free" (like clean air, home cooking, ...) and this is just another instance of the same "problem."

-

I don't think you need 30% per year to justify a high turnover strategy... A > 2% "alpha" is likely enough for most people.

-

This is a very good take: https://www.wsj.com/articles/as-tariffs-bite-get-ready-for-a-1970s-style-supply-shock-11559734362?mod=hp_lead_pos7

-

Another thanks from me. There's something quite satisfying about making a big change to your portfolio and later finding out that Druck did more or less the same thing.

-

Poor Warren ;D This is probably the "What's Wrong, Warren?" moment of 2019.

-

Some discussion in print: https://www.wsj.com/articles/the-real-winners-from-trumps-tariffs-are-chinas-neighbors-11559120403

-

Why are bond yields so low and stock prices so high?

SHDL replied to Viking's topic in General Discussion

Unemployment is a lagging indicator. It normally hits the bottom right when the stock market peaks and the economy is about to go into a recession. So this data point is, if anything, a reason to be cautious. -

Why are bond yields so low and stock prices so high?

SHDL replied to Viking's topic in General Discussion

My guess is that this has to do with investor demographics. In the bond market there are the macro trader types who are seeing negative economic indicators and loading up on mid-long term treasuries. Those guys could be exiting/shorting stocks too but their trades alone are probably not enough to cause a market crash given the corporate buybacks and continued buying by investors who don’t pay much attention to macro. -

Some thoughts: I’m pretty sure these tariffs will make corporate profits go down and consumer prices go up, so it’s not something I welcome. At the end of the day, it’s a tax hike: the government takes more money from the private sector and distorts things along the way. And if things really escalate … it may be time to panic. Cardboard is right though that even if the tariffs were to become permanent the long term damage should be blunted by the fact that businesses, consumers, and other governments around the world will adapt to them over time. As to whether this will change China’s political regime and/or behavior, I’m pretty skeptical. They seem to really hate being told how to run their country, which I guess is understandable. But we'll see. Maybe one positive thing I can say about all this is that it raises some (much needed) tax revenue in a way that many voters don’t seem to mind. I think there’s some political brilliance there.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

SHDL replied to twacowfca's topic in General Discussion

Yes, there are a lot of interesting moving parts here... Like I said, I view f~U[.5, 1] as a pessimistic lower bound and I think the “true” distribution is skewed more towards 100% of par for reasons that you and others mention. I’m waiting for more evidence to come in before making a move though. If I’m reading the situation right, there should be a window of opportunity to make a profitable trade between the time the news comes out and the time the price catches up.