ubuy2wron

-

Posts

705 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by ubuy2wron

-

-

In case you've not yet seen this one...

L

-

A Primer: Understanding Derivatives

Heidi is the proprietor of a bar in ...

She realizes that virtually all of her customers are unemployed alcoholics and, as such, can no longer afford to patronize her bar.

To solve this problem, she comes up with a new marketing plan that allows her customers to drink now, but pay later.

Heidi keeps track of the drinks consumed on a ledger (thereby granting the customers loans).

Word gets around about Heidi's "drink now, pay later" marketing strategy and, as a result, increasing numbers of customers flood into Heidi's bar. Soon she has the largest sales volume for any bar in .

By providing her customers freedom from immediate payment demands, Heidi gets no resistance when, at regular intervals, she substantially increases her prices for wine and beer, the most consumed beverages.

Consequently, Heidi's gross sales volume increases massively.

A young and dynamic vice-president at the local bank recognizes that these customer debts constitute valuable future assets and increases Heidi's borrowing limit.

He sees no reason for any undue concern because he has the debts of the unemployed alcoholics as collateral!

At the bank's corporate headquarters, expert traders figure a way to make huge commissions, and transform these customer loans into DRINKBONDS.

These "securities" then are bundled and traded on international securities markets.

Naive investors don't really understand that the securities being sold to them as "AAA Secured Bonds" really are debts of unemployed alcoholics. Nevertheless, the bond prices continuously climb - and the securities soon become the hottest-selling items for some of the nation's leading brokerage houses.

One day, even though the bond prices still are climbing, a risk manager at the original local bank decides that the time has come to demand payment on the debts incurred by the drinkers at Heidi's bar. He so informs Heidi.

Heidi then demands payment from her alcoholic patrons. But, being unemployed alcoholics -- they cannot pay back their drinking debts.

Since Heidi cannot fulfill her loan obligations she is forced into bankruptcy. The bar closes and Heidi's 11 employees lose their jobs.

Overnight, DRINKBOND prices drop by 90%.

The collapsed bond asset value destroys the bank's liquidity and prevents it from issuing new loans, thus freezing credit and economic activity in the community.

The suppliers of Heidi's bar had granted her generous payment extensions and had invested their firms' pension funds in the BOND securities.

They find they are now faced with having to write off her bad debt and with losing over 90% of the presumed value of the bonds.

Her wine supplier also claims bankruptcy, closing the doors on a family business that had endured for three generations, her beer supplier is taken over by a competitor, who immediately closes the local plant and lays off 150 workers.

Fortunately though, the bank, the brokerage houses and their respective executives are saved and bailed out by a multibillion dollar no-strings attached cash infusion from the government.

The funds required for this bailout are obtained by new taxes levied on employed, middle-class, nondrinkers who have never been in Heidi's bar.

Now do you understand?

-

Okay they are pretty much a monopoly with a 20 year avg return on capital in the high teens and you still do not want to invest in them. Right KO just makes sugar water why would one want to invest in that no mgmt. magic there. LOL. I think Warren once said he wants companies that a fool can run because sooner or later fools do show up in the corner office. I think the concept of moats and margin of saftey are lost on some.I don't think why Canadian banks has such a high regard, my understanding is they are pretty much monopoly their in a protected market. They charge crazy fee and currency spread. Customers of them get ripped left and right.

-

There exists no perfect hedges, in a serious depression just losing money slower than the next guy is somewhat of a hedge. That said I have a higher than normal cash position I own corporate bonds in particular FFH bonds I am long a little gold have a pretty concentrated portfolio and my BAC position is thru in the money leaps and I run a pretty active hedge through inverse etf,s. Someone said that no one rings the bell at the bottom when Prem removes his equity hedge I will remove mine if I have any, his mkt timing has been pretty fricken amazing for a guy who doesn't time the mkt.So the fact that one of my largest holdings, Pepsi, has not gone down as much as the market means I don't know how to find value? I explained to you over PM that I believe it's worth $115 and it's currently selling for $63. IMO, that is no different than you buying BAC at $6 when it's worth $10 (or whatever). What has really stuck with me from studying WEB is buying wonderful businesses, and when I get the chance as I have with Pepsi, I load up - REGARDLESS of the macro environment.

FYI - Loeb is less than 30pc net long right now. He is VERY concerned about the macro and is hedging like crazy all the while loading up on YHOO. There is room for both.

Best of luck being 100pc long with leverage in this environment.

-

Cdn residential real estate especially Vancouver is in a bubble that said the risk lies not with the banks but with the tax payers of Canada through CMHC and through the one public mortgage insurance company. The Province of BC also has a huge contigent liabilty as they have guaranteed the deposits of all the credit unions in BC which will likely implode if the bubble bursts. If I had to make a bet against residential real estate in Canada I would short Genworth Canada but please do not do it on my say so as I have no clear understanding as to what their exposure is.A look at Canadian house prices relative to income and rent:

http://valueinvestorcanada.blogspot.com/2011/11/canadian-home-price-likely-considerably.html

The Economist's take on housing valuation

http://www.economist.com/node/21540231?fsrc=nlw

So there are still a few countries with housing more overvalued than Australia ;)

-

Japan's negative population growth probably a factor

How much longer can they finance their debt internally? At some point external debt financing will be required and then it could turn nasty very quickly.

[/quote Why do they have to borrow outside and as long as its Yen demoninated what difference does it make. China has to buy US treasuries or allow its currency to rise, China and the US are joined at the hip with the level of trade that exists.

-

I think the unknowns for BAC are the lawsuits and Euro counter party risk. It appears that the other major players in the CDS mkt in North America have at least as much exposure to counter party risk but perhaps have had a better track record on handling the risk. The litigation risk is not IMO definable with any certainty I have invested because I assume that putting Country wide into bk was always a hole card for BAC if the litigation risks ever get out of control. The operations of the bank are getting stronger and they are the only major bank which has been raising capital which I think is a good thing if we do enter a period of high capital mkts instability. If BAC weakens materially next week I will be adding. I was lucky enough to purchase some BAC in 2009 under 4.00 the firesales this time will be in Europe in October the entire mkt cap of the Euro banking industry was below the mkt cap of the Cdn banking industry Euro banks have to raise 300- 500 billion the rights offerings which is how they raise capital are particularly brutal to exisiting shareholders.The fixed income market is pricing in a minor risk premium with BAC. Tells a very different store then the equity markets.

Yes, and I think this is saying after Lehman and 2009 TARP preferred/equity infusions, no bondholder in JPM, C, BAC, WFC is ever going to have to take a haircut. Equity on the other hand...

Well, fwiw, I think the equity markets are wrong about wfc, jpm, and BAC now.

Someone mentioned lawsuits earlier. I think you will find that nearly all large public companies continuously have lawsuits against them. To a point it is part of business and modern complexity. I mean Apple and Samsung are suing one another constantly, and Samsung is a major supplier to Apple. Now, if that isn't sick, I don't know what is. The size of lawsuits against BAC may seem greater but they have the ability to drag them out and mitigate them in various ways. Also, many of them were filed this fall, just at the end of the statute of limitations for the mortgage claims.

-

TD made some large acquisitions of US regional banks in the 2006 2008 period paid > 2.5 times book and clearly this was a mistake which is not reflected in their income statement or mkt price. BMO has large US exposure but they were have been much more circumspect in when they bought and what they paid. CIBC which was the bank which had the gunslingers in charge changed mgmt in 2007 and the CEO who I have known for 30 years as we both started our careers 30 years ago @ Merrill is determined to have the strongest balance sheet in the industry. The CDN banking industry is in an very interesting position if they could create firewalls between their CDN operations and their foreign subs they could become world leaders and replace the Swiss. The govt. is rightfully afraid of the CDN banks becoming too large as any failure of a CDN bank would be of the too big to bail category if their foreign exposures are not ring fenced.What I like about the Canadian banks is that no one sitting on the executive floor in a corner office is trying to be a hero with perhaps the exception of TD. We have 5 Wells Fargos in Canada the last gung slingers were fired in 2008 .

Could you elaborate a bit on why you think TD is different? It's not a sector I know much about, but I'm always trying to learn :)

-

What I like about the Canadian banks is that no one sitting on the executive floor in a corner office is trying to be a hero with perhaps the exception of TD. We have 5 Wells Fargos in Canada the last gung slingers were fired in 2008 .

-

I got it from Investing the Templeton Way chapter 6 page 161.

Packer

I read the same thing and I thought what a bookend on an amazing investment career as I believe he started his investment career by buying the 10 cheapest stocks on the NYSE in the 30's and ended up shorting the most overvalued stocks at the peak of the high tech bubble.

-

Japan, Is a very interesting case study. Its debt to GDP ratio is higher than any of the PIIGS more than twice as high as the US and yet because its debt is almost entirely internally financed it shows no signs of crises. Its stock mkt has lost 75% of its nominal value in the last 20 years but its economy has shown real growth in the same period of time. It experienced the largest real estate and stock mkt bubble in modern history but refused to experience ANY of the short term pain that has been the conservatives recommended nostrum for all economic problems. they have had zombie banks for decades but their culture has allowed them to continue, for getting close to a generation, to admit to mistakes and take losses. The Olympic scandal is just one manifestation of this cultural difference, no one loses face in Japan and very few ever question authority. When was there last a hostile take over in Japan. When was the last time a major corporation announced a large lay off of employees? Has the Japanese model given worse results for its average citizen than the Western worlds?

-

The topics which have received the most attention here are those dealing with investments which have not been rewarding investors. BAC RIMM LVLT etc have received the most posts. FD disclosure I am long BAC and briefly owned RIMM and will buy LVLT if it hits my order next week. These are all investments which have tested investors patience greatly at what point do you through in the towel my personal experience has been that averaging up has been a better strategy that averaging down. The Dhando investor which I highly recommend ,dealt with this, and said that a 3 year hold on average was required for a turn around investment.

-

I frankly just do not get it as I have said before thinking macro makes my head hurt. Italys largest bank Uni credit announced a 10 billion loss and a rights offering which will dilute by 50% and has basically asked the ECB to change the rules to keep them alive and the mkt is unchanged as I type this. Italy can not bail out Uni-credit and Europe can not bail out Italy and the rest of the world is basically saying to Europe its your problem and Uni credit is within 48 hours perhaps of having to shut down and Uni credit is NOT a little bank its huge. I bought a little gold today because it is looking more and more that Europe has just two choices crash or print.

-

What has been the historical precedence re European vs North American recessions, I would think that economic activity in one economy would always result in similar results in the other. It would seem to me that unless Europe prints a contraction in the economy is a certainty with the contraction in credit which is comming.

-

Bill Gates does both and he is the first most of the time.......

Alot of great people are toolbags, but you dont have to be a toolbag to be a great person.

Gates was often a jerk in his younger days as well.

Agreed about not having to be a tool bag to be great but it does seem to the case that nice guys are not likely to finish first. (I hope that is not my envy speaking) Regarding Bill G I think that he was saved from dirtbagdom by Belinda and Warren.

-

I think if you study the lives of most great men and women and I define that as being individuals who have reached the absolute peak of what ever their field of endeavor may be. You will discover a common thread and that is they had some pretty glaring short commings in many areas of their lives. To achieve iconic status you by definition have to have an obsessive focus on what ever it is you are striving to achieve. It never surprises me when GREAT MEN have glaring character flaws it would greatly surprise me if they did not.

Warren Buffet would not be the 2nd richest man in the US if he had spent time with his kids and paid attention to his wife.

-

I think there would be a great deal of interest in a short thread perhaps a little controversial given the long bias here but still a lot of interest. Has anyone paid much attention to Einhorns insurance co. I have only glanced at it.

-

I find myself seldom agreeing with you Yankee but I sure do here. This refusal to say no to his base when they are clearly wrong shows incredible lack of cojones on Obamas part. The most disappointing decision which he has made or in this case avoided.Wow! Why do I keep being reminded of the Lion in the scene from "The Wizard of OZ", when he is tearing and holding his tail while Dorothy rips him a new one!

(could anyone imagine McCain/Palin punting like this? The one with the balls would have made the old man make a decision!)

Absolutely pathetic!

-

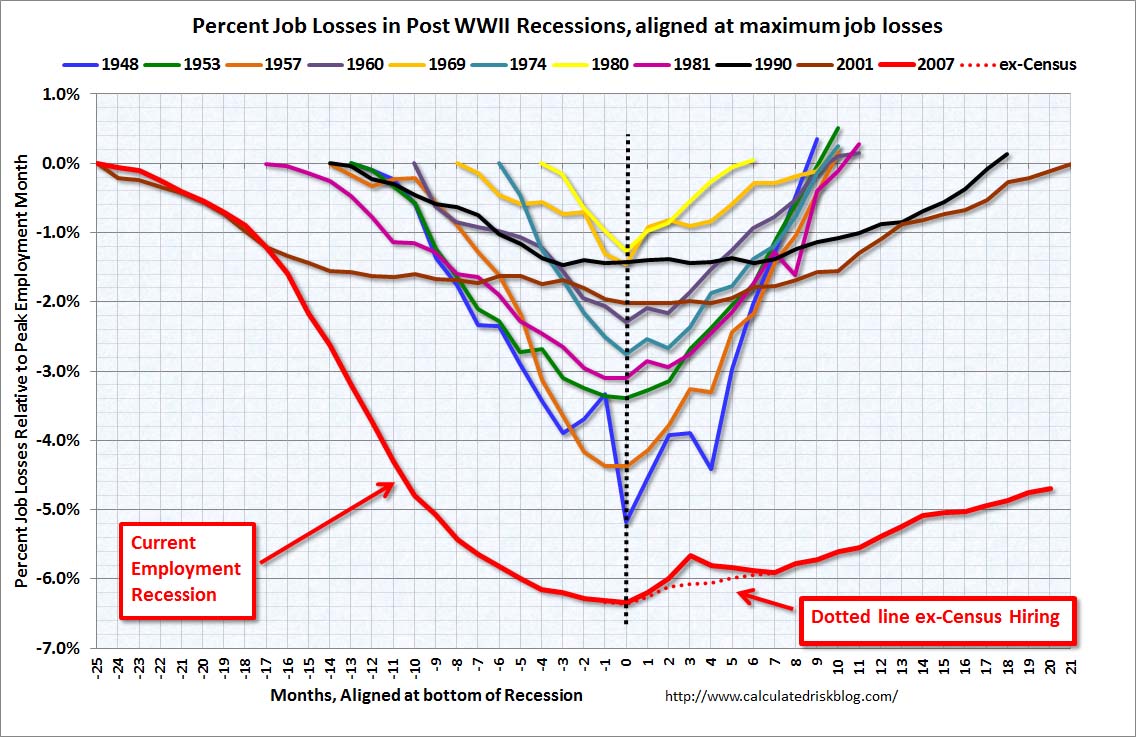

It has been posited by some that the housing cycle is the economic cycle in the post WW2 period there is a ton of evidence on this point if you want to search it out. For all but the the 1% the largest outlays are for housing and cars well perhaps for the bottom 5% this is not true. Autos have started to come back its houses that have not when we are building 1 million new homes a year unemployemnt will drop like a stone. Housing will come back its already started. IF Europe falls off a cliff which it may we will head into a double dip but the recession will look a lot like the recovery job losses will be modest and economic decline will also be modest. This is the price we pay when no fails. If their aint no bust their aint no boom. And for all of you who are hankering for the bust just remember that it just might be you who gets it wrong and becomes the dead body on the beach.Here is an interesting comparison of this recession compared to many previous through the lens of employment. I don't think we will see any downturn this severe again in our lifetime.

Only if we have another real estate boom/bust. Look at the labels on that graph. It is percent job losses relative to peak employment month. Construction/home building related jobs were huge;I have read that half of the 9% unemployment rate comes from construction and related. Those aren't coming back anytime soon. Housing employed a ton of people. Peak to trough would be a big number, and you can see it on the graph.

-

It stopped being about Greece about 12 months ago the attention of the bond vigilantes has transfered to Italy this is a problem of the "too big to bail" category. The banks will not be allowed to fail under the current plan and enough liquidity will be provided to roll over Spanish and Italian debt for the next 12 to 18 months. The hope is this will provide enough time for realistic plans to be put in place for the too big to bail countries to reduce demands on the credit mkts or alternatively credit markets to stop requiring out sized risk premiums for Italian debt. The fact that the spreads on Italian bonds has never come in HAS to be of concern. For the few banks that are able to tap the mkts their pfds and debt are prolly VERY attractive currently for the banks that can not it is likely that creditors are going to be required to provide equity capital so they are definately at some risk. I think one can assume the divy is gone on almost all of the Euro banks for the next few years. Euro banks are delevering and the ECB is helping by buying PIIG debt but how many failed auctions can the ECB underwrite the ECB is also insolvent at this stage. We are in a situation where the the ECB cuts interest rates and bond prices are falling this is not one expects to see in "normal" mkt. Gold is trading like a risk asset on steroids these days. Was the low made in October THE low we will see in the mkts for the rest of the year perhaps but I am not willing to go all in on that bet. Did any one notice that Greece replaced the heads of all their armed services yesterday coincidence maybe but do you want to make a large bet on it.

-

They want customers to lapse their policies, I understand that lifecos build in a lapse policy factor when pricing product. What are the drivers that cause policy holders to lapse. If we look at a GIF as an example which MFC has a greater exposure than most. Does the poor performance of the policy cause an increase of the lapse rate obviously if you are 80 years old and have terminal cancer you are not going to lapse however if you are 50 and healthy you very much are.My understanding of the lifecos is that their business is affected by:

1) The level of interest rates as they use: a) bonds to invest premiums received, and; b) current rates to discount policy liabilities.

2) Competition: the business is very competitive and each new policy incurs large initial costs (think commissions to salespeople).

The strain of low interest rates on float is additionally hampered by low discount rates on liabilities and high underwriting expenses if policy count is growing. The things that offset these headwinds are life expectancy and policy lapses. The lifecos want their customers to live longer than they project and lapse their policies.

In an environment of low interest rates and mature, competitive markets, lifecos have poor margins. In order to combat this, they try to reduce business growth and the high costs associated. It risks relationships with salespeople, but it is one of the only levers they have. Unless they go to markets which are growing and lack competition.

ELF has stated that they are slowing new policy growth in this environmnent in order to improve poor margins.

-

I am all for the banning of CDS. Banks love them they are highly profitable until they are not as the mkts are opaque and speads are large and the competion is slight. Plus the mkt is pretty much unregulated when did any one ever get charged with insider trading thru the CDS mkt. I believe that the real estate bubble in the US would have had a much smaller impact without the CDS mkt as sub-prime borrowers would have been unable to borrow. I suspect that the ability of Greece to borrow so much with such a spotty credit history is likely due to the availability of CDS.I agree with you completely.

It's hard to get comfortable with the CDS exposure and I sometimes wonder why the banks put themselves in the middle of the chain if they are just going to buy an identical policy from someone else. Why not let their customers buy the contract directly from the derivative dealer, that way their balance sheet isn't at risk if a credit event happens or the credit dealer disappears.

One might argue these customers are too small to purchase CDS from a dealer. My rebuttal would be that I wish these contracts were written such that the banks just served as brokers, aggregating business for the dealers.

oh well....

They should just call off this CDS thing. If u own bond, do ur homework. Greece debt got cut 50% and it's not default and thus CDS doesn't protect the creditors at the end.. why bother.

the ability of Greece to borr

I feel this way as well but think they should just ban naked CDS. Either that or make them so standardized that they can be put in big, red bold font on 10-K's. Everyone always talks about how governments and regulators are deathly afraid of a Greece default because no one really knows the ramifications for CDS.

Only in finance would people support the proliferation of weapons of mass destruction that can be hidden like this.

-

Its better than that the company is buying back shares daily through the purchase of EVT which holds about 40% of its NAV in ELF and sells at a steep discount to its NAV, actually on most days it has the highest discount to NAV of any closed end investment trust in NA. ELF is my largest holding and I am trying to buy more. Actually the only thing more soporific inducing than reading the annuals is waiting for it to trade.Pssst. ELF is selling for a shade more than 50% of BV.

Keep it secret!

SJ

-

Is not the life insurance part of the business the ultimate long tail business the float lasts an awfully long time it would seem to me that a Watsa type fixed income investor could generate some interesting returns for shareholdsers and does not a very low interest rate increase the rates for new policies written. One would have to assume that this industry is facing obstacles why else would the stocks be so cheap I am really looking for some kind of primer on lifeco,s as an invesment . I can easily look at BRK and FFH and other P&C insurance companies and see where the low hanging fruit lies. I presume with a life co it is impossible to have any real underwriting advantage it would seem the winners and loser would be determined by investing acumen and marketing prowess. I have never understtod MFC there are just too many moving parts for me to get a handle on I suspect that PWF and GWO may be cheap but I have no conviction.I sold all pwf, slf, and mfc out of my margin accounts. Still have smallish positions in my registered accounts where I have a 20 year horizon - they still pay dividends.

Lifecos have to hold liquid securities for policy holders. These liquid securites are treasury bonds. In the case of the above names the t-bonds would be in cnd and us depending on where the policy holders are. With the extreme low interest rates the bonds are often yielding less than the policy holders have been promised as payouts. With each passing Q with low interest rates the lifecos have to increase policy holder reserves. I cant speak to Gwo but slf and mfc have hedged themselves against low bond yields but this only works to a point. They dont want to overhedge due to future portfolio drag.

Add to this pending retirements for baby boomers and you start to see long horizon drags on earnings.

Then there is the mutual fund business that each has. Pwf Between gwo and igm is the largest mutual fund co. In Canada. Mfc and slf both have mutual fund business in the Us and Canada. Needless to say the mutual fund business is subject to market whims and with lower returns fee income is going to get squeezed by etfs etc.

Bright spots: mfc and slf have a growing presence across Asia. I wouldn't hang my hat on that as it is a small piece of their business, and I expect it is difficult to dividend cash up to the holdco. levels.

Finally, these businesses make Bac easy to comprehend.

-

Can anyone here point me towards a decent primer on Life Insurance companies. I have noticed that Lifecos generaly are pretty depressed in price but I have never quite understood what kind of mental construct I should be using when valuing a life insurance co.

{kind=link}

"Fairfax enters India to invest in local firms"

in Fairfax Financial

Posted