ratiman

-

Posts

825 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by ratiman

-

It's kind of funny how badly WB has misjudged the people who were supposed to secure his legacy. He no longer speaks with Gates, Sokol, Todd Combs, and Schroeder, although Schroeder did nothing wrong and Combs might get a Christmas card. It was probably for the best that he was never involved in running the business.

-

Great podcast episode recommendation thread

ratiman replied to Liberty's topic in General Discussion

Adam Wyden, former "Bombshells" investor, interviewed. I haven't listened yet but Wyden is a character. -

The confict isn't over. Iran would be wise to wait for SPR to continue to decline and strike closer to midterms in order to inflict max pain and extract more concessions. Trump and Bessent are taking the risk that they won't ever need the SPR beyond the next couple of weeks. The market might be pricing in a glut barrels from VZ and from Iran post-conflict but we have to get there first. $69 is a nutty price when new ships aren't entering the gulf for new loadings and US and Iran are still in a shooting war. The crowing of the nothing ever happens crowd seems a little early.

-

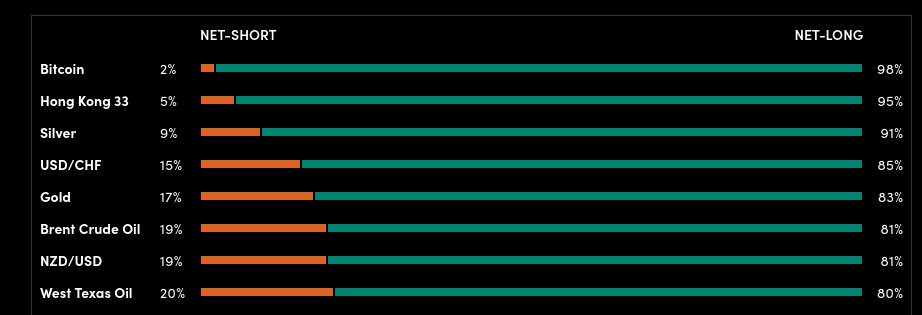

I have no idea what this means but the Oanda traders have been a good contrary indicator. Unfortunately it doesn't have historical data but right now the wrong-way retail traders are majorly long oil. https://www.oanda.com/bvi-en/lab-education/tools/sentiment/

-

The SOH is now closed but good deal for you my friend. We are in the bargaining stage where every barrel of oil comes with unlimited middle eastern haggling. The rug merchants are now in charge.

-

This oil trade might be the greatest rug pull of all time. The oil bulls are absolutely out of their minds. Cushing has now reached tank bottoms and meanwhile oil sinks like a stone. It really is hilarious (as long as you have no position). I happen to think this is not over. Real oil inventory does matter at some point and a billion barrels can't be taken off the market / Iran given control of global oil supply without the price reflecting that sea change. But for right now the "lol nothing matters" crowd is winning.

-

If we get a 60 day window why wouldn't everybody scramble to top up their inventory? We might go right back to a blockade after 60 days and presumably China and US won't be drawing down SPRs during the 60 day window, if anything they will be building them back up. So if that is the case why wouldn't oil go UP if there's a deal?

-

If it doesn't get to $6 gas I will never listen to any oil bull ever again. If shutting down ME oil for 3 months hardly moves the price then it's basically no more scarce than salt water.

-

I thought the whole post was interesting. As for ERP seat vs fee based pricing, I'm not sure a major change to enterprise software business model is great news. It's easy to count and verify seats which makes it a convenient way to structure pricing. The alternative is untested.

-

Around 130 companies were asked some version of “is AI eating your business?” and said no. Almost all of enterprise software sits here — Salesforce, ServiceNow, Workday, Adobe, SAP, Atlassian — swatting the seat-compression question away like it’s beneath them. Now, none of this is secret. The denials are in the prepared remarks for anyone to read. And the pricing changes are in the press releases for anyone to read. The interesting thing is that they contradict each other. Almost every one of these companies is, at the same time, tearing out per-seat pricing and replacing it with usage-based pricing. Sit with the logic. If your software is sold per employee, and AI agents are about to do those employees’ jobs, then per-seat revenue is the exact thing AI threatens. A company that genuinely believed AI was harmless would have no reason to rebuild its entire pricing model on a deadline. When a company’s words and its pricing point in opposite directions, the pricing is the more honest signal — because it costs something. https://autonomousresearchcorp.com/research/ai-revenue-headwind

-

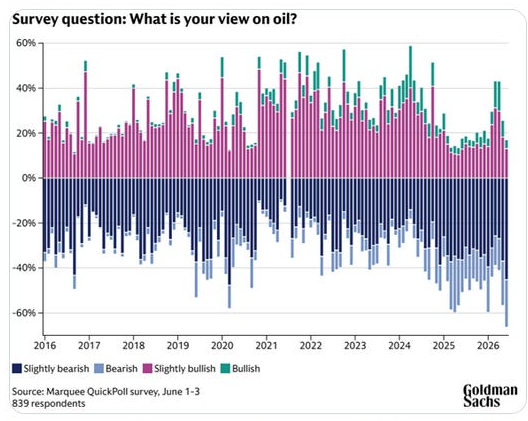

It seems like the overwhelming consensus is that oil is headed back down after a transitory spike. Institutions are bearish while professionals are alarmist. (via Paolo Macro on X)

-

Value Don't Lie has a lot of free posts. I think he posts here sometimes. https://www.valuedontlie.com/p/vdl-home-base

-

If this were a stock chart, it sure looks like a inverse head and shoulders and it points to price target of $180. Oil chart goes sideways for decades and then a big move establishes a new range. And before I get accused of being an oil permabull, I think I've posted once before on oil and it was a bearish thread on Exxon.

-

If conservatively estimating 10mm barrels a day is missing and assuming $5 per barrel of elasticity and assuming $65 price (WTI) before the conflict we would expect at least $115 but price should price in that this does not seem to be ending any time soon. Consider that US senators on left and right are both against a deal, as far as I can tell. This is nowhere close to being solved.

-

There's been some speculation that the futures are manipulated. Usually talk like that is just sour grapes but I might believe it in this case. If so you might expect price to go higher not lower after a deal. I continue to think that real pain is the only way we get a deal. Trump is still in the bargaining stage.

-

Neil Chapman, SVP of Exxon today at the Sanford Bernstein Strategic Decisions Conference (via Eric Nuttall)

-

You're asking the wrong guy, I have no idea. All I know is that Iran has not budged an inch and there is no sign that the two sides are close at all. It's like the Commanders negotiating with Terry McLaurin.

-

This is Iran military on X: I have no way to evaluate that, maybe it's posturing etc but I don't know, Say hello to $200 oil doesn't sound like somebody about to compromise.

-

I'd say greater than 50% chance of Brent over $150, not that anybody is on the edge of their seat waiting for my predictions but nothing I've seen so far makes me think Iran is ready to blink or Trump is ready for a humiliating climbdown.

-

At what price of Brent would you be wrong?

-

This period reminds of that time before March 11 when everybody realized COVID was a big deal but few were willing to go short. I can't really see how there is going to be a deal before the market crashes. Until then there won't be the urgency.

-

Restaurant stocks (MCD, PTLO, WEN, CAVA, CMG, etc)

ratiman replied to ratiman's topic in General Discussion

CAVA results came in strong with 10% SSS. Looks like the $20 lunch havers are still going strong, 2nd quarter also running at 10%. CAVA looks like the strongest of the restaurant stocks. -

Restaurant stocks (MCD, PTLO, WEN, CAVA, CMG, etc)

ratiman replied to ratiman's topic in General Discussion

SBUX SSS were pretty good at 7% but tnathan above seems to think SBUX is also facing margin pressure. I have never understood Starbucks, total mystery to me why it is popular but I am not their target customer. -

Restaurant stocks (MCD, PTLO, WEN, CAVA, CMG, etc)

ratiman replied to ratiman's topic in General Discussion

Dutch Bros is facing some fierce competition in Texas and the south. This might explain Dutch Bros margin problems last quarter. I don't think one restaurant category has ever seen this much capital deployed as quickly.

-

Todd was running Geico and running a big portfolio? That seems unlikely. The reason to shunt him off to Geico was to get him out of managing money. Ted's days are numbered.

.png.95b2b5c6a10de9ef6693fc57b4c6eafb.png)