Matthew Lembo

-

Posts

39 -

Joined

-

Last visited

Matthew Lembo's Achievements

")

-

Not to be too bullish, but would an ancillary benefit of share repurchases be that it extends the runway of potential compounding at FFH. By returning capital to shareholders it limits the size of the company’s capital base and allows FFH to continue to invest in smaller and perhaps higher returning opportunities and therefore delay the drag a larger capital base has on its investment universe as Buffett has warned about for years?

-

Fair points, and yes I agree the insurance subs are where much of the investments are held. However those subs are controlled so that FFH fully controls distributions and investments. Perhaps i am thinking about it incorrectly but was thinking that since Digit is going public and prolly wont be taken private anytime soon (at least that’s not the plan) it wont be fully controlled the same way Odyssey, Brit etc.. are so therefore FFH will not be able to spread its investments in Eurobank like equity securities across Digit’s capital. Would have thought Digit equity investments if any would be controlled by Digit which may have different desires than FFH. It might work for large market cap public investments (eg Micron) but it wont work for Atlas for example, b/c there is no public market for Atlas’ shares. Plus would think Digit would want the majority of its equities portfolio to generate their earnings in Indian Rupees. Maybe i am over complicating it

-

Anyone have any insight into if once digit starts writing insurance at < 100% CR if it will start to invest its profits in equities (both public and private) and slowly morph into a conglomerate with a similar business model to brk/ffh/mkl over time? would seem like a logical next step given BRK/FFH success. Separately, Prem mentioned that FFH manages float of majority owned insurance subsidiaries. I don’t think this applies to Digit but don’t know for sure. Does anyone know?

-

I think argument that Buffett is making is that if one were to borrow money (float) with a zero cost or negative cost with an infinite or very long term ie 50-75 years than the npv of that liability today is can get pretty close to zero, depending on discount rate used.. Yes we are restricted in how we can invest that liability but that liability should not be valued at par. Agree tho that it all comes down to expected Roe of the business over time irrespective of the inputs to get there.

-

Bought the book! Thank you for doing this. Happy new year.

-

Agree the hard market may reverse but at that point the insurance subs would no longer need the capital and Prem said on the conference call that that is the time FFH would increase the volume of share repurchases price dependent of course. So sorta tho not exactly a bit of a built in hedge / outlet for incremental capital allocation. is that a plausible scenario?

-

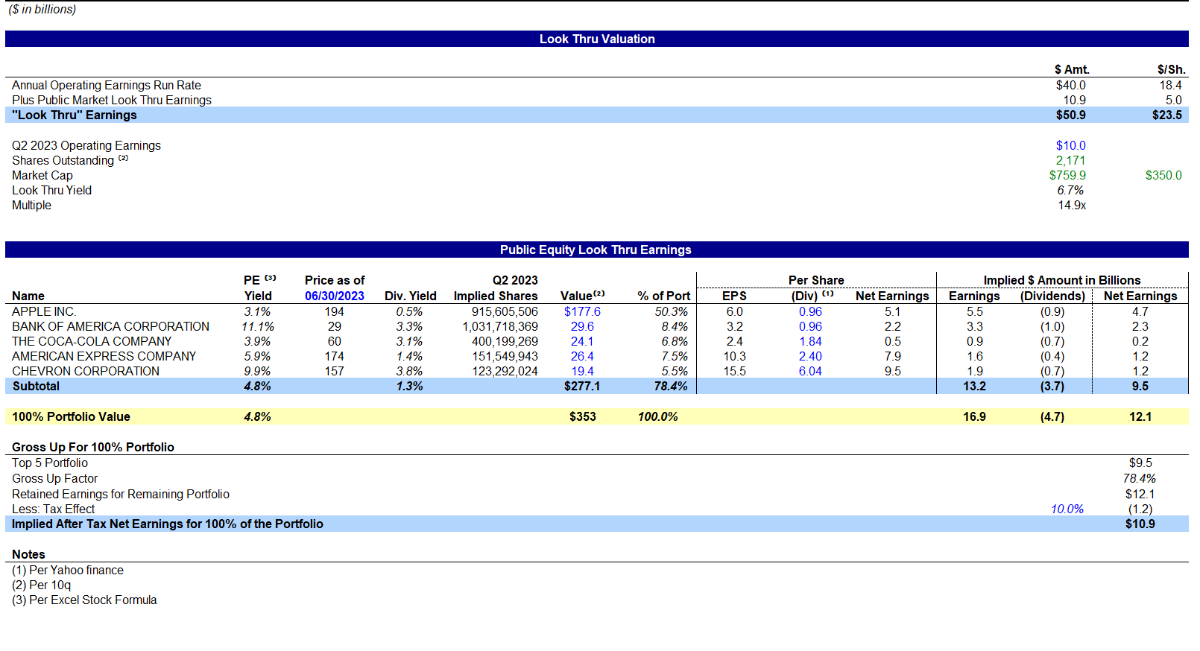

Below is my look thru earnings calculation, I am at a similar earnings yield of 4.8% on $353bn (i get to the portfolio yield by grossing up the top 5 holdings as indicative of the portfolio at large) or ~$16.9bn but think we have subtract dividends paid to BRK of about ~$4.7bn as those are already in operating earnings. Therefore I get to an incremental pre tax look thru earnings of $12.1bn apply a 10% discount for some taxes and I get to $10.9 of incremental look thru earnings to BRK. If we annualize the $10bn of operating earnings to $40bn and add the $10.9bn then perhaps run rate total look thru earnings maybe ~$50.9bn on a market cap ~$760bn equates to a look thru earnings yield ~6.7%. See my calculation below. Please rip it apart as I am guessing I missed something.

-

Viking, thank you for all of your thoughtful analysis. I truly appreciate it. Newbie question for you b/c I dont understand exactly how it is working, on your earning estimate below I believe #4 represents the new IFRS discounting of reserves. If so I thought that might have been a one time adjustment but the below projects this recurring albeit at a smaller amount into the future. Was wondering if that is to capture the delta b/w the old way of reserve accounting and the new IFRS mandated way of discounting or am i totally missing it.

-

Buffett/Berkshire - general news

Matthew Lembo replied to fareastwarriors's topic in Berkshire Hathaway

20% makes sense to me. Thanks for the input. I’ve always struggled with the fact that selling outs exposes one to black swan events for little premium. Is that a fair analysis? -

Buffett/Berkshire - general news

Matthew Lembo replied to fareastwarriors's topic in Berkshire Hathaway

Thank you. what do you think is an acceptable premium? Sorry for the basic questions, haven’t ever considered this strategy before. -

Buffett/Berkshire - general news

Matthew Lembo replied to fareastwarriors's topic in Berkshire Hathaway

interesting, how does one get paid for a standing limit order? By selling puts? -

Another way to look at the pref equity investment is that it is covers all of the capital KW needs to invest in this deal (5% x $3bn = $150mm) plus $50mm. So fairfax is funding 100% of the purchase price and getting less than 100% of the returns. However fairfax is also getting ownership in KW which mitigates its dilution on this deal and is profitable and valuable in its own right.

-

if you have it, could you also share the Fairfax Financial annual meeting transcript?

-

much appreciated!

-

agreed, thank you Viking for sharing your work with the board. It is highly appreciated.