KCLarkin

-

Posts

2,454 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by KCLarkin

-

Buffett's Berkshire takes stakes in four major airlines

KCLarkin replied to KCLarkin's topic in Berkshire Hathaway

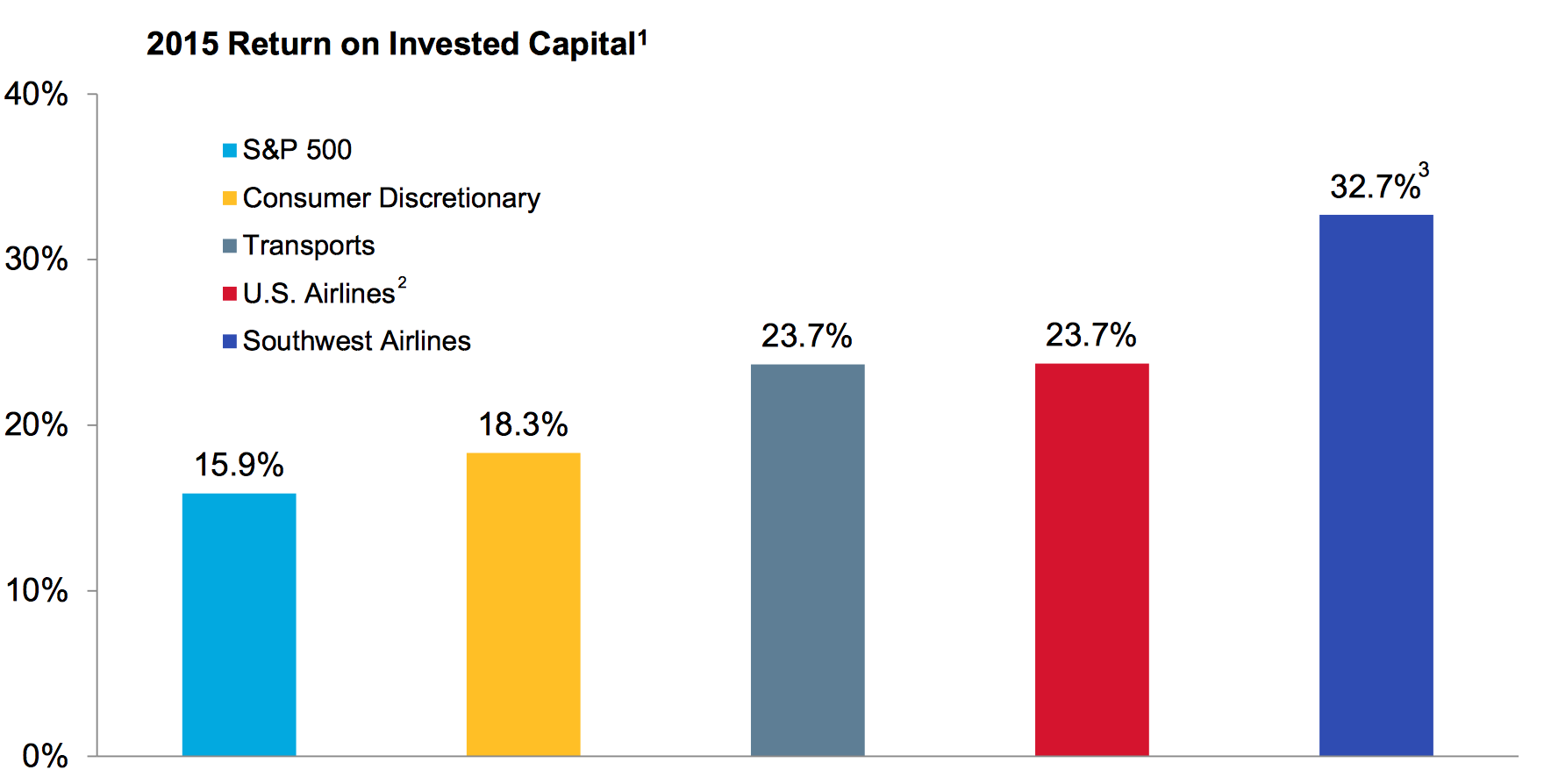

Yes, I should have been clearer when I started the topic. I'm interested in a discussion on why they bought the US airlines now. I actually disagree strongly with your assertion that the economics of US airlines haven't gotten better. They are significantly better. The issue is that airlines are very expensive. Southwest, for example, trades at over 4 times tangible book (GuruFocus). For most of the last decade, it traded closer to 1.5 TBV. The airlines look cheap based on earnings but it's doubtful that Southwest and Delta will be able to earn 30% ROIC indefinitely. Maybe 10-15% is sustainable. -- Actually, the strongest thesis for investing in airlines is that Buffett hates them so much. Even when they are cheap, most value investors won't touch them. So they have limited appeal at the bottom of the cycle. You can find some real bargains before the MoMo guys get in. Unfortunately, the time to buy was 2012.

-

Buffett's Berkshire takes stakes in four major airlines

KCLarkin replied to KCLarkin's topic in Berkshire Hathaway

Yes, but then why is Buffett commenting on their position in LUV? Bizarre. -

http://www.cnbc.com/2016/11/14/buffetts-berkshire-takes-stakes-in-four-major-airlines.html Does anyone know if this was Buffett? Or T&T? Even though I have 9% of my portfolio in an airline, I am shocked by this news. Anyone have any insight?

-

No, Assuming you are responding to my post. I posted the benchmark price for detached homes. This methodology attempts to avoid the skew seen in averages. What I'm seeing is volumes going over the cliff with only slight weakness in price for detached homes. That drop in volume is possibly an indicator that there is a very wide bid-ask spread, as sellers are slow to adapt to new market realities. And buyers are willing to wait them out. This could indicate future price drops, as sellers become more desperate. If my interpretation is correct, it is difficult to predict how deep this correction will be. Calgary had a huge drop in volume but suffered a mild price correction. Of course, Vancouver is much pricier.

-

The benchmark prices I posted were for detached only. I'm not looking for agreement or argument. I'm just worried about the risks to my portfolio. If home prices are really down 20% over such a short period, I need to make some portfolio changes. If they drop 20% over the next year, I am comfortable riding out the turbulence.

-

The benchmark is down 1% from June to October.

-

I don't think it was well-written or well-organized BUT there is a tremendous amount of insight hidden in the jargon in this report. I certainly don't think the takeaway should be simply buying cheap. His definition of cheap would not be a low-multiple stock. My definition for cheap is also not low multiple stock, it is just as Buffett defines it - cheap as compared to IV, which incorporates growth, quality, etc. The concept of outside view - just having base rates in mind is something I imagine every value investor incorporates when making an investment decision, it certainly is something that is very central to my own approach. Mean reversion which is what data indicates is the very essence of Graham's 1934 book. What I did not see in this report is anything new that adds to what Graham and Buffett had already covered. I have a written investment approach - nothing fancy, pretty much what Buffett, Graham, Munger, Greenwald, Fisher, etc. have repeated over and over again and a checklist - my own mistakes and few pointers from the same gang. So when I read an investment book or article, I am primarily looking for something new to add or modify in either the investment approach or checklist. After reading this report, I did not find one thing that I can add to either of these. What I find mildly useful are the two pages of base rate data on earnings growth. Nothing new, pretty much in line with my understanding but I did not have this data before. See after all that is written, he gives examples, where quality is high and stock is cheap and returns are good. But the main thing is stock is cheap. Is that really a surprise? This is before even going into such things as expected returns over 90 day period. Vinod Perhaps not useful to you but useful to many others. Especially to investors who build very detailed models with very unrealistic expectations.

-

Clothing Companies Hitting New Lows

KCLarkin replied to Ballinvarosig Investors's topic in General Discussion

There is a very big difference between the Brands and the Retailers. Retailers have very large operating leverage. You have a, say, 20 year lease on a store. Your staff costs are relatively fixed. It is very easy to go into a death spiral with relatively modest revenue declines. Extreme caution is needed with ANF (of course operating leverage would be great if they can recover). -

I don't think it was well-written or well-organized BUT there is a tremendous amount of insight hidden in the jargon in this report. I certainly don't think the takeaway should be simply buying cheap. His definition of cheap would not be a low-multiple stock.

-

Tim, those things are true. But he also has more experience and access to many more opportunities globally. But I think you missed my point. There is no way for most people to compound at 50% because they have diversified portfolios. But a portfolio of 1-3 stocks might have a chance. More likely, he would do 30% or so.

-

According to this article, he made 50% per annum over 5 years in PetroChina. http://fortune.com/2014/10/31/warren-buffett-best-investments/ If true, I don't think it is unreasonable he *might* do similar numbers with smaller capital. I don't think you need leverage. But you'd need pretty good turnover. And high concentration. And you might need to start in 2009 not 2016.

-

I know that's what you are saying. And I know that's what you believe. I'm simply saying that the method you are using is not reliable.

-

I think it is fair to say that Vancouver house prices might drop 20% over the next year. Even though I agree with everything you said, I highly doubt house prices have dropped 20% across the board in a single month. The anchoring effect makes it very difficult for moves that big. Usually, volume dries up as sellers refuse to lower their prices even as buyers disappear. After re-listing their houses a few times, the sellers eventually find a market-clearing price. Or else distressed sellers come into the market. A much more likely scenario is that sales of high-end homes have dried up. So the mix shifts to condos. This causes the "average" price to drop 20%. Teranet uses a fairly sophisticated process to track price moves to avoid this skewing effect. I doubt the realtors and developers are as scientific.

-

Do you have a reliable source on this? The benchmarks/indices I have seen do not corroborate this. Teranet had Vancouver prices up 0.18% MoM in September. And up 24% YoY. Or are you referring to volumes? Or are you referring to "average prices" (which are skewed by sales mix)?

-

Personally, I think it is just a quirk that low PE stocks tend to outperform. There are many reasons why a stock has a low PE: - High debt load - Melting Ice Cube - Cyclical at cyclical peaks - Low quality earnings - High capital intensity - Low growth - Low ROE - Volatile earnings - Frauds On the other hand, low PE stocks also include out-of-favor, low-expectations, reversion-to-the-mean, margin-of-safety "cigar butts". High PE stocks include over-valued, fads, promotional IPOs, momentum, go-go stocks etc. But High PE stocks also include cyclical companies at cyclical bottoms, cash-rich companies, wide-moats, high ROIC, J-Curves, consumer staples etc. In the end, these things have tended to balance out in a way that favours low PE stocks, quantitatively. But it is absolutely true that SBUX at 15x is a better investment than OUTR at 10x.

-

http://www.theglobeandmail.com/report-on-business/rob-commentary/the-intended-consequences-of-new-housing-policies/article32383166/

-

To be clear, the "Nobody gets fired for buying IBM" thesis isn't mine. Someone else stated this earlier in the thread. I was just using it as an example about how to think about "brands". I will refrain from further discussion.

-

No, we're not saying the same thing. You are saying that people buy IBM because of the perception that it reduces IT career risk. I am saying that people buy IBM because it actually reduces IT career risk. By stopping at Level I, you are ignoring all the strategic and tactical ways IBM reduces IT career risk. -- For example, Silicon Valley lives with an experimental "fail fast" mantra. That allows them to innovate quickly. But if you build your bank on top of the enterprise equivalent of "Google Glass", that is extremely risky. Enterprises that buy cloud computing from Google have extreme career risk. A private cloud from IBM might be pricier, but you know that IBM will be around in 50 years to support it. -- And because you are looking at this superficially, you are missing some key investment insights. If IBM's brand promise is to reduce IT career risk, what happens when business units or developers can buy IT resources directly from AWS or the cloud? Suddenly, AWS is able to breach IBM's moat. IT professionals want to reduce risk. Business units want speed and flexibility. The relative power between these groups will determine how aggressively the companies move towards the public cloud. Banks, insurers, airlines, railroads, and hospitals are understandably risk adverse. Startups are understandably focused on speed and flexibility. And because of this dynamic, IBM is racing to make their products and services more flexible. And AWS is racing to make their services less risky. And finally, getting back to the OP, Microsoft Azure is sitting happily in the middle. It is both relatively risk-free and relatively flexible. A very prudent choice for the many businesses that are "Microsoft shops". That probably explains the wide valuation gap between MSFT and IBM. There is uncertainty about whether IBM will be able to repair the breach in its moat. Microsoft's enterprise moat is relatively unscathed (although iOS/Android have breached the Windows moat and Google Apps has wounded the Office moat).

-

This is a good example of my point: Lazy Thinking: Stupid people pay extra for IBM, because of "brand" 2nd Level thinking: IT managers pay extra for IBM to reduce career risk 3rd Level: Why does hiring IBM reduce career risk? Is this advantage eroding? You could argue that IBM's ROTE is so high because it exploits a principal-agent problem. That is a much more insightful argument than saying that people only buy IBM because of the "brand". -- I will refrain from further comment on this thread.

-

Just saying that cost isn't the only variable. And the people who buy IBM tend to care more about the other variables.

-

Ha ha. No, I don't work for IBM. But I understand how brands work.

-

A brand isn't magical fairy dust that causes people to pay more money for bad products. Your lazy thinking obscures IBM's real strengths and challenges.

-

Nobody buys IBM because of the brand. And those who buy IBM believe IT is a competitive advantage. If it was a commodity, they would just use open source software, running on chinese servers, installed by Indian IT shops.

-

How deep do you read into your annual/quarterly reports?

KCLarkin replied to InspireByReason's topic in General Discussion

To answer a different question, a good book to understand business models is "The Little Book that Builds Wealth" or "The Five Rules for Successful Stock Investing" both by Pat Dorsey. -

Not really about hedging, but I really enjoyed this book (also by McMillan): https://www.amazon.com/Options-Strategic-Investment-Lawrence-McMillan/dp/0735204659/ref=sr_1_1?s=books&ie=UTF8&qid=1473448423&sr=1-1&keywords=options+as+a+strategic+investment