Gmthebeau

-

Posts

427 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Posts posted by Gmthebeau

-

-

4 minutes ago, gfp said:

I think you have me confused with somebody else. (and, no, I cannot invest anything in a tax deferred account and have never had one)

ok, well good luck with your math skills. i will be muting you now.

-

3 minutes ago, gfp said:

Ah yes, I see, the Morningstar chart was not properly accounting for the reinvestment of all dividends (or deducting any tax on those dividends). Ignoring the tax that would have been owed, the S&P 500 with all dividends reinvested at the time they were paid did 600% over my holding period of Berkshire. (9/2001 - present). Berkshire did 777.5% so only 177% better than the index.

You'd be surprised how well 10% tax-deferred over a long period of time can do for ya.

still wrong. see post right above from @thepupil for accuracy. from 2013, your reference period, $10k invested in BRK would be worth $42,780 vs $41,483 in SPY. Of course QQQ would have massively outperformed both and been worth about $70,652. All of them could be invested in a tax deferred account with no taxes due.

-

2 minutes ago, gfp said:

Mr. Thebeau only makes killings. He doesn't get out of bed for 10%. Get it straight

when you are wrong on the facts just make up stupid shit. see how far that gets you in life

-

24 minutes ago, sleepydragon said:

No point of arguing unless you actually have bought a stock and hold for a decade and it made you richer than you would have if u had bought brk. Or, simply put, are you about 5x richer from 2013? But Brk shareholders are.no point in arguing about something when you just change the discussion. the comment was a "killing". i am showing BRK has barely beaten the SPY since 2013, your reference point. Do you guys even bother to check facts? fucking clueless.

-

7 minutes ago, gfp said:

I don't know when you were in pre-school but the Berkshire shares I manage have almost exactly doubled the total return of the S&P500 with dividends included since 2001 which is when I bought them (I was not a big trader in pre-school so this was after my schooling was complete). And over that entire period, unlike the index, the shares were rarely over-valued or worrying.

not a killing by any measure, but yea its low risk

-

23 hours ago, vinod1 said:

What killing? It barely kept up with S&P 500 over the last 20 years! An index fund is a better holding especially at size for holding periods measured in decades.

I sold BRK in 2012 timeframe to buy BAC and other financials and again during Covid to free up cash to buy other things including BRK calls. So I did not make a lot of money in BRK but the alternatives ended up giving higher returns. Definitely paid lot of taxes.

With Fairfax, I actually segregated it into accounts where I have long term holdings like index funds. I think selling Fairfax in the next 10 years would be a mistake. Forget about valuation, keep holding it. There are enough good things in the pipeline that positive surprises are likely to outnumber the negatives. If nothing else should give decent results comparable to market. So why mess with that?

Of course, this assumes Prem does not again start "Protecting the shareholders from economic headwinds...."

I was wondering same thing, killing? I guess if you go back to the start of it when most investors today were in pre-school or not born yet. It is basically just a closet index fund now and has been for a couple of decades.

-

Yes, Bill is a Saint. ROFLMAO. It was proven that shutdowns were in fact the dumbest thing ever, and greatly damaged far more it helped. In line with his Valeant call I suppose.

-

2 hours ago, thepupil said:

the timeline of this incident is inaccurate.

the narrative around the "hell is coming" interview is false.

Ackman was aggressively getting longer of stocks in March and monetizing his hedge (half of which already had been sold by the time of the CNBC interview). as someone who was buying his fund monitoring the net exposure, I was a little taken aback at how quickly and aggressively long of restaurants and hotels he had gotten in March and April.

The 28 minute interview , where he talks about buying stocks can be found here

The details regarding the hedge monetization here.

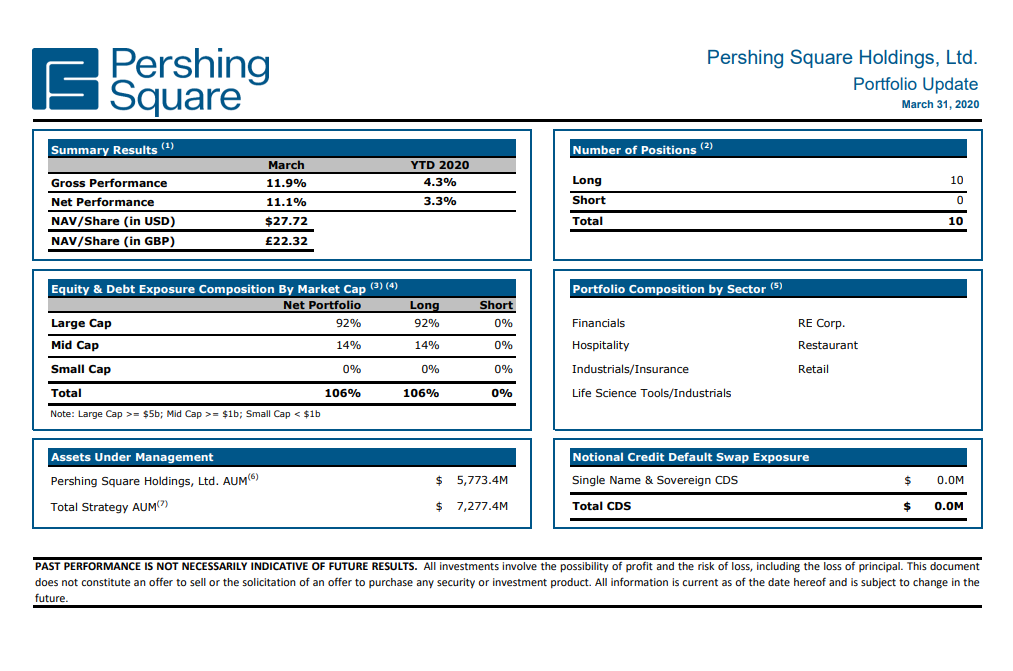

At March 31st 2020, PSH was long and strong

Bill's story that he didn't make much more money after his interview. This is corroborated in the data by the spread on CDX IG which widened from 40-60 bps in February to 140 on the 18th. It peaked at 152. on 3/20/2020 and ended the month at 113.

He made the bulk of his money on the move from 40 to 140 (and had already taken off over half of it) before the interview, not from 140 to 155, even if you think he widened out CDX with that interview. .

well maybe he did it to drive prices down as he was buying, either way there was a profit motive. to think otherwise is foolish.

-

Ackman is no saint so I would not feel sorry for him because some other cutthroats went after him. This is the same guy who went on TV, cried hell is coming, while trying to crash the markets to profit.

-

I have used it and was impressed also. For a new product it is really good, will only get better.

-

52 minutes ago, Gmthebeau said:

short sale SMCI, probably close the position today or tomorrow.

closed small loss, not working

-

1 hour ago, maplevalue said:

Don't sell too much as the hopeful breakout past 800 will be epic

I am not really negative on it, I just have enough tech exposure right now and wanted to lighten up.

-

short sale SMCI, probably close the position today or tomorrow.

-

SMT.L paring some tech exposure. still have more

-

XOM leaps, JD, BABA, CLF, INTC

===========

Selling JD and BABA here after nearly 5% short term gain in less than 1 week, also had short term calls on BABA closing for larger gain.

-

12 hours ago, james22 said:

In an election year?

I'm sure they don't want to but if inflation picks back up they will get forced to, but again this is just a lower probability.

-

Tickets to AC/DC European tour on sale today. Get them before they are gone!

-

8 minutes ago, TwoCitiesCapital said:

I'm open to the Fed hiking again. I think it would be a mistake. I don't think the data will support it especially now that we're seeing outright deflation in many goods/real assets. But I can believe that their motivations may be something other than "stable employment and inflation".

Powell has basically said, in other words, that their intention is to drive the economy into a recession. Whether he does that by raising rates, or leaving them too high for too long, I can't say. But I've been pretty confident for awhile that 4% was too high and have been buying duration every time its available above 4%.

I'm in a lot of things in fixed income at the moment. Started off in cash and iBonds when rates were basically zero in late 2021. Then started accumulating short-term spread products and agency mortgage expopsure as rates rose and certain spreads blew out in 2022. Then started adding intermediate government duration and core bond type products. Then I started adding TLT calls when rates were on their way up to 5%. In recent months I was adding fixed income CEFs at sufficient discounts to NAV to make me want the low-quality credit. 10+% cash yields.

At this point, I don't really care what rates do. Lower rates benefits my duration exposures and can give me ~10+% while likely giving me attractive opportunities in stocks. Flat rates let me collect a yield that probably YTMs that are 6-7% in aggregate. Higher rates hurts my duration, but likely help my spread products - so maybe ~5+% while setting me up for even juicier returns next year.

I'm ok with any of those scenarios.

The FED typically leaves rates to high to long, but I still don't see a lot of evidence they are really that restrictive. Inflation came down rapidly but has pretty much gotten stuck, and I think there is a lot of evidence to suggest it will pick back up. Unless the employment market cracks consumers just keep spending.

I add duration at 4.4% and above, but I don't think the risk/reward is great below that area. Of course if you hold till duration it doesn't matter. I have a similar structure and return profile in fixed income as you.

-

-

1 hour ago, TwoCitiesCapital said:

If long-term, rates go from 4% to 5.5%, which do you think will likely lose more? Stocks or bonds?

I like floating rate a lot better in the bond area. You can get 8% and FED stuck having to stay higher for longer despite Powell wanting to cut. The folks on the committee with some common sense won't let him.

-

SNOW. Would have preferred to buy it around $200 but missed that, will add it if drops back to 200ish.

-

1 hour ago, Gregmal said:

Lol I remember being told we were all idiots for not having massive Tesla and Moderna positions in November 2021…then having our friend totally disappear and return a couple years later accusing me of being long SF real estate….and claiming he was retired and in bonds. Only to then switch bonds to cash when he was told bonds did poorly. And now he’s long Uber and Chinese tech stocks….

You were bullish on SF real estate. Own it. I am retired, and I trade a lot. Own, stocks, bonds, cash. Sorry for not updating you daily on all my trades. I put some out yesterday and got push back that going long Chinese stocks was not contrarian. That has to be the dumbest thing I read on here in a long list. I am a bit of loss for how some guys on here view things and have to think they been blown to shit from their holdings. Good luck.

-

16 minutes ago, TwoCitiesCapital said:

If long-term, rates go from 4% to 5.5%, which do you think will likely lose more? Stocks or bonds?

Stocks. I still think there is say a 25% chance the FED will be forced to raise rates even higher.

-

54 minutes ago, thepupil said:

lol, BND is at $71.80. It peaked recently at $73.5, after which it paid $0.2. so it's down about 2% in terms of total return from recent peak. $TLT is 7% off peak, less a little coupon.

For something with a little more duration I have some Caltech 2119 bonds that I bought at $58 in October, think they got to $72, and are now at $68.

In what world is that blowing up?

a bit dramatic

Well maybe, and if you hold them you will get the coupon. It just wasn't a good time to be buying bonds IMO when the 10 year was 4% and less. I don't know if J Pow intentionally tries to mislead the market or is just that incompetent, or can't communicate, but he is a disaster every time he speaks.

Why did so many smart investors miss making a killing on BRK stock?

in Berkshire Hathaway

Posted

lol, he cant do basic math. you are now muted too. most of you are clueless. this much is obvious.