Cunninghamew

-

Posts

155 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Cunninghamew

-

I very much enjoy the guy who posts under Bluegrass Capital. I am not willing to pay the multiples he pays for many of those businesses, but have found him to be a good resource for making lists of companies that are (a) fun to read about like TDG and (b) might be worth having a basic understanding of in case they ever trade at rock bottom multiples. Also, enjoy reading the stuff TrenGriffin posts as well as PlanMaestros charts

-

I know a lot of people on here also have twitter. I recently killed my account and created a new one, because overtime it had turned into noise. Many "fundamental" investors suddenly turned into timing experts when the market decided to sell-off. The remaining fundamental investors seem like they only want to talk about "platform" companies. I am all for having a great capital allocator at the helm, but soo much value seems to be placed on what a company will be rather than what it is today. I am not smart enough for that. It might have been easier to just un-follow people, but I wanted a clean start. In an ideal world, I would love to have the underwriting discipline of Graham, but also an appreciation for what makes a good biz. I don't want my underwriting to require a competitive advantage to extend well into the future. I want a competitive advantage to exist, but who am I to underwrite it 10 years out. This is turning into a diatribe, but are there any true value investors out there whose approach could be described as have your cake and eat it too? Recommendation on who to follow and what they are good at welcome

-

starter in SSRG

-

Prem Watsa Takes 3 New Small Holdings (Steel Partners)

Cunninghamew replied to LowIQinvestor's topic in Fairfax Financial

FYI... looks like they are doing a reverse/forward split. He did pretty much the same thing at DGT Holdings. I have no clue, but I am guessing liquidity will dry up a little after considering anyone holding 500 shares or less will be cashed out I might be off base with that comment -

[amazonsearch]The Frackers[/amazonsearch] Just finished reading this book and it is a fun / slightly informative read. Great beach book Profiles various players in the O&G industry over time - Harold Hamm, Mclendon & Ward, Mitchell, Papa, etc Can't help but think every E&P exec is a pretty big gambler after reading

-

People commonly mentioned on this board... i.e. current outsiders Nick Howley - TDG John Malone - LMCA LBTYA LINTA and for other million things Mike Pearson - VRX (maybe Rajiv De Silva at ENDP) Buffett, Gayner Potential new idea I am working on... have not seen on the board Ayman Asfari - PFC (Petrofac Ltd on LSE)

-

Sorry for the lack of clarification... my investments I normally label as 1 of 3 types Compounders category: example would be TDG... great company / great economics / great management / good tailwinds... but the valuation isn't cheap (at least on face value)... it typically trades for a mid to low single digit free cash flow yield... despite the price I am willing to hold this company and periodically add to it when it becomes reasonably valued Deep value category: this is my terms for stuff that is just ridiculously cheap at face value, but not necessarily a great biz. For example, I might be willing to buy a really crappy house in a crappy neighborhood if the price was just stupid low, but only at a certain price that is super discounted. Examples... I owned yellow media for a time. Despite the management being great, Fiat falls into this bucket for me. Special sits category: I didn't mention this earlier, but sometimes I will put on risk arb plays and/or other investments that are impacted by corporate events. I guess you could also call this event driven. I hope that makes more sense now. Yes it is redundant, but it is simply how I label/breakout my portfolio when I am thinking about it. I agree on TDG. I am thankfully that so far it has worked out even though I bought it a while ago at a somewhat expensive price. I assume you have also looked at Wesco Aircraft Holdings as they are kinda similar? Why do you like TDG more than WAIR? Thanks. I actually haven't spent much time looking at Wesco, so I can't give you a thoughtful answer. The honest answer is I didn't compare the two when considering a purchase. However, here is my quick thought (without talking about valuation). Both companies sell and/or distribute small parts that are all over the plane and relatively low cost in the grand scheme of things, which is nice. Additionally, they both get to take advantage of a planes long life cycle by selling and/or distributing replacement parts. That said, TDG is in a better part of the supply chain as they are generally selling product for which they are the sole provider. I don't follow Wesco, but I always thought of them as a distributor or middle man. Net Net I would think TDG should have better pricing power. You can certainly see large differentials in their margins. So TDG appears to be a higher quality biz that is benefiting from the same structural tailwinds I too had to close my eyes to purchase the shares, because the multiples be it EV/EBITDA, P/FCF, etc did not scream bargain. Hope that is helpful and I would love to hear your thoughts about Wesco and/or any critiques of mine

-

Sorry for the lack of clarification... my investments I normally label as 1 of 3 types Compounders category: example would be TDG... great company / great economics / great management / good tailwinds... but the valuation isn't cheap (at least on face value)... it typically trades for a mid to low single digit free cash flow yield... despite the price I am willing to hold this company and periodically add to it when it becomes reasonably valued Deep value category: this is my terms for stuff that is just ridiculously cheap at face value, but not necessarily a great biz. For example, I might be willing to buy a really crappy house in a crappy neighborhood if the price was just stupid low, but only at a certain price that is super discounted. Examples... I owned yellow media for a time. Despite the management being great, Fiat falls into this bucket for me. Special sits category: I didn't mention this earlier, but sometimes I will put on risk arb plays and/or other investments that are impacted by corporate events. I guess you could also call this event driven. I hope that makes more sense now. Yes it is redundant, but it is simply how I label/breakout my portfolio when I am thinking about it. One more point... ideally I could find compounders at just stupid cheap valuations (i.e. they would fall into both categories, but that seldom happens). But if you ever see TDG / V / MA / CHD / VRSK / or the like trading at a high teens free cash flow yield let me know

-

Sorry for the lack of clarification... my investments I normally label as 1 of 3 types Compounders category: example would be TDG... great company / great economics / great management / good tailwinds... but the valuation isn't cheap (at least on face value)... it typically trades for a mid to low single digit free cash flow yield... despite the price I am willing to hold this company and periodically add to it when it becomes reasonably valued Deep value category: this is my terms for stuff that is just ridiculously cheap at face value, but not necessarily a great biz. For example, I might be willing to buy a really crappy house in a crappy neighborhood if the price was just stupid low, but only at a certain price that is super discounted. Examples... I owned yellow media for a time. Despite the management being great, Fiat falls into this bucket for me. Special sits category: I didn't mention this earlier, but sometimes I will put on risk arb plays and/or other investments that are impacted by corporate events. I guess you could also call this event driven. I hope that makes more sense now. Yes it is redundant, but it is simply how I label/breakout my portfolio when I am thinking about it.

-

I am pretty young, so I am curious how today's stock picking environment compares to others (mentally not in terms of past valuations, which I can look up)? Obviously, it is harder to find stocks with compelling upside today than it was last year. What I would be interested to hear is (1) How does today stack up in terms of opportunity set? How long you have been investing? (2) What is your style (short description)? For example, my portfolio is usually split between super deep value stuff (typically not great companies) and what I would call compounders (great mgmt. / high ROIC names / etc). The reason I am asking is I am finding it incredibly tough to generate good ideas. I also feel like several of my holdings (while not overvalued) are only compelling if you compare them against the what the rest of the market is offering. My fear is that more often than not it will feel this hard? My more core positions: GY / MKL / FIATY / BRKB / ENDP / GNCMA / ALSK (this has a lot of random option trades around it) / RJET / ACN / AIG / DVA / TDG

-

Yes it's in the 10k. As a general rule, you should always look in the notes to the accounts because what's recorded in the balance sheet is the net operating loss (or net deferred tax asset, net DTA) -- that is, net of allowances. The notes will show the gross figure, the allowances and the net. The allowance means that, in the view of management / auditor, not all losses will be used. There are many reasons why this may be the case -- losses not transferable across jurisdictions or businesses, or simply the company won't make sufficient profits in the future to use up the losses. However, in some cases significant value can be "hidden" if management / auditors takes an overly conservative view. So in the case of SDOI, there was a net deferred tax asset of $37k as at year end 2012. Note 11 breaks this out. The gross DTA was $9,962k, the allowance was $9,925k. Your call as to whether there is hidden value here, but relative to a current market cap of $24 million, the gross DTA is large. I think that in some cases the DTAs are transferable to an acquirer in an acquisition, who may be in a better position to utilise the gross DTA. However, this area of tax is very complicated. Hope this helps. Not sure you're right here -- where are you getting $11m? First, thanks everyone... I was looking in the 10qs for this info, but I guess it is only in the ks (or at least for this company). So note 11 has two tables: (1) Breakout of the DTA and (2) breakout of NOLs by year of expiration As you pointed out, the DTA shows $37k net and $9,962k gross. This company is currently a shell of cash that has no operations, so the allowance of almost 100% makes sense. The board is using the shell to find an acquisition target (or so I think). In the meantime, until such target is acquired the company will have no operations (or income) to offset anything. The DTA table also has a breakout that shows its components. In it is shows $4,930 of NOL carry forwards. However, the second table of NOL expiration by year shows NOLs of $10,978k. Question 1. How do they arrive at the number in the DTA table of $4,930k (or why isn't it $10,978k)? Question 2. Assuming they were able to use these NOLs for anything they wanted (i.e. forget about jurisdictions, etc) would I look at the DTA table to find out how much they can offset or the NOL table? My inclination would be that they have $10,978k they could use to offset taxes. I guess the answer to the first question will inform the answer to my second. Also, thanks everyone

-

I was wondering how you go about finding how many NOLs a company has? In the past, I have seen it explicitly stated by mgmt. in filings. To be specific, I am trying to find the amount of NOLs that Special Diversified Opportunities (SDOI) carries. As far as valuation, I assume you just take the amount and discount it overtime... Thanks in advance for any help you can provide.

-

First thanks for adding this GIO - it is pretty interesting and I think their reports are a worthwhile read even if you are not interested in owning SPE Now to my question... SPE has gapped down yesterday bc they have a convertible pref. that is being converted into common shares. At first this made a lot of sense to me, bc it is dilution... now I am starting to wonder how big the impact actually is My question is what impact does the conversion have on NAV for SPE? At first I thought I should take the old NAV ($18.22 as of 1.31.14), which multiplied by common outstanding (7,451,042) gives you a value of $135,757,985.24. There are 734,847 converts outstanding that convert into 3.716 shares each (or 2,730,691). So the new denominator would be 10,181,733 shares outstanding. If you divided the $135mm by this number you get NAV per shares of $13.33. Obviously, there was a flaw in the above methodology, because the shares only traded down to $15.90. Then I looked at the balance sheet in the last semi-annual to try and understand where I went wrong. Looks like I was double counting, because the preferred was already being treated as a liability. I.e. NAV = Assets - liabilities - pref Can someone please help me reconcile the move in SPE? My guess is it has to do with the pref being held on the balance sheet for less than the actual obligation.

-

Industry Background of People on This Forum

Cunninghamew replied to BG2008's topic in General Discussion

Work for investment advisor/family office.... we allocate most of our client's money (about 70% of assets) to outside funds (long-only, hedge funds, private equity funds, PE co-deals) and we invest the other 30% in house (this is mostly equities and some private stuff associated with the founding family). I am a generalist, but tend to focus on individual equities (analyst and run a small portfolio) and our investments in hedge funds. Background: Econ/math... interned for a large hedge fund for a year (2008) that focused on energy (specifically MLPs and Canadian Royalty Trusts)... still learning how little I know -

Two ideas I find interesting: MVN (TSX-V) and EOX The first idea is not for the faint of heart and is not as cheap as it was a month or two ago, but still has a lot of "potential" upside. Madalena is a Canadian based E&P that has acreage in Canada and Argentina. The company is currently reworking a lot of its Canadian acreage (applying horiztonal drilling and modern fracking techniques). The current stock price 0.68 is mostly covered by the value of their Canadian production (which should continue to grow at a very fast clip). The reason the stock is cheap is because of its exposure to Argentina's Neuquen Basin (where it owns 135k total acres). Because of the YPF/Repsol debacle the market is assiging little to no value here. This gives you a cheap call option on their ability to sell that land or find a partner in Argentina. There are a lot of reports out there about how Argentina screwed itself over, because the country does not have the capital it needs to internally develop this field. The went from being somewhat energy independent to dependent. If they infact take a less nationalistic approach than maybe this call option is worth some money. This is not a sexy pick, but I like EOX... it is a Bakken E&P that trades cheap relative to its acreage holdings. The company does not look cheap on a per flowing barrel basis (unless compared to pure Bakken comps). That said, production is ramping nicely and I think mgmt's guidance is low-balled (thanks to Dedwards for doing the heavy lifting) Dedwards did a great writeup on his blog and the company presenation is also helpful. 1. http://dedwardssays.wordpress.com/2013/10/19/emerald-oil/ 2. http://content.stockpr.com/vyog/media/8106a25206d1d477060b3101ed2779ba.pdf

-

285 BCF withdraw in Natty Gas... storage levels are now well below year ago levels and pushing below longer-term averages

-

Is someone on here really less than 13 or is that a joke? I am really impressed if that is true. I had a fake stock account in junior high (I dont know what my criteria/philosophy was) and a small PA in highschool (still don't know if I had a process). To the sub-13 year old... I hope you stick with it and the adventure of learning. You are off to a much better start than I was.

-

a beer cart that stops by my desk whenever the market closes or for our CEO to let us keep a cooler of beer next to my desk

-

There are a lot of value investor types out there. I like to think of it is a spectrum. 1. At one end, you have the G&D types who focus on the most objective measures of value - like what are the assets of this company worth today 2. In the middle, you have people who care about the value of assets today + the earnings power of those assets 3. At the other end, you have people who focus more on the future earnings power of assets and a company's ability to grow/reinvest profitably (more GARPy in nature), I am naturally wired to hang out at the start of that spectrum. I have never been good (or have even tried) to find high quality biz's trading at fair or slighlty discount valuations. When I look at my portfolio today and see junky companies trading at say 20-25% discounts to fair value it makes me squeemish. I would much rather own a great asset with a good owner operator trading at, say a 10% discount. For the past few weeks, I have been trying to find good companies at decent prices (for the first time) and replacings some of my less discounted names with those. It has been hard. Anyways... what am I getting at? I want to know if people tend to stick to one type of investment across all time horizons or do they alter their approach as the opportunity set changes? I.e. are you always a net net guy or are you a net net and GARP guy? Furthermore, does your style change as the enviroment changes? To me it seems like it would make the most sense to use my style in the early years following a big bear market, but to gradually morph into a focus on quality later on. What got me thinking about this was someone's comment on TDG. They said, that TDG was on their list to buy in a bear market (or something like that). I really like TDG as a business, but would I ever buy it in a bear market or at that time would I be able to find juicier investments? I too have a list of businesses I would love to own, but I never buy them. When this list goes on sell there is usually other stuff that seems more fun. Hope those comments make sense. Thoughts?

-

http://www.completebankdata.com/ Very cool site

-

Is anyone going tomorrow? I will be there if anyone is interested in meeting up

-

I generally dont read the stuff on seeking alpha. For every 1 good article it seems like you get 10 fluff pieces. I was wondering if people would be kind and point out a few contributors they think are worth keeping tabs on I have one I will add - Steve Zachritz - is good for thoughts on E&P names

-

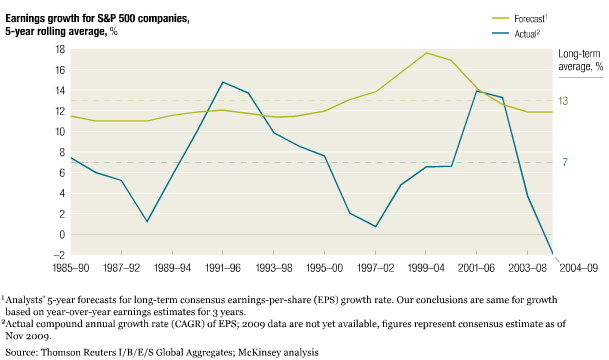

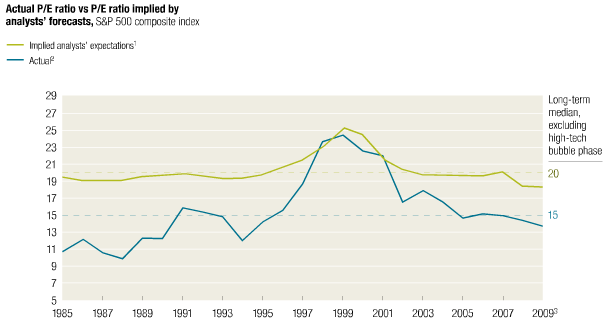

I don't really have an opinon on where we are in the market cycle. I can say that it is harder for me to find single name ideas today than it was yesterday. I can also say that I really don't like the Yardeni price to earnings charts. The guy uses forward earnings in almost everything he does. I have attached two charts related to forward earnings that I think show how ridiculous they are. Not trying to go at your post... more of a thing agianst Ed Yardeni's stuff

-

I don't really have a bone to pick here, but I thought I would play devils advocate. Right now the economy is not operating at full employment, so very little thought is given to the possibility of labor shortages. But if the economy were operating at full employment where would the marginal worker come from. Retirement ages have been pushed out dramatically in the US, bc older people cannot afford to leave the workforce. They will have to retire eventually. Over the past 100 years we have seen a lot of female workers enter the labor force... the so-called "quiet revolution." According to BLS, of the 123mm females over 16 about 59% were in the labor force. If I recall correctly the female labor force participation rate peaked in 2000 and has been gradually declining since. Immigration to the United States has been slowing. So where does the marginal worker come from? My conjecture is that if the economy were to surprise to the upside you would not only see employment come back quickly, but you might also find the marginal worker missing. Just food for thought - not sure if I completely agree with the argument, but it was fun to think about. Elijah

-

Quantum Online [ftp=ftp://quantumonline.com/]http://quantumonline.com/[/ftp] has tables of preferreds. Unfortuntely, it just lists the securities and basic features of the securities like coupon / liquidation pref / call date / conversion price if convertible / etc. You would have to look at prices separately, but it might be a good place to start.