FiveSigma

-

Posts

93 -

Joined

-

Last visited

-

Days Won

1

FiveSigma's Achievements

")

-

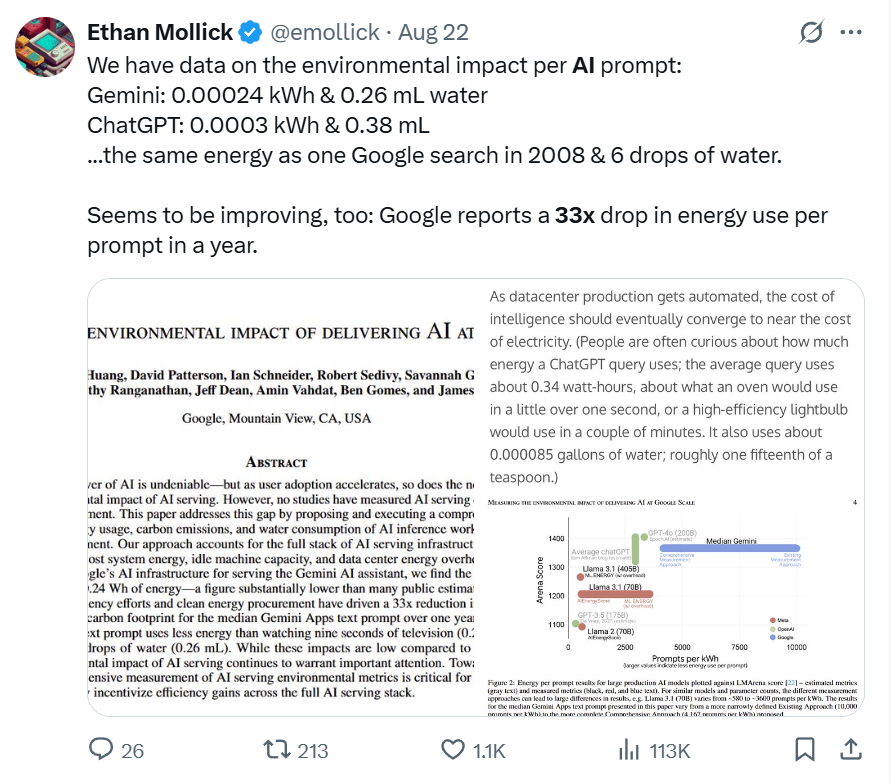

Pay attention. Words of caution are for you, when you say and I quote "with likely lower future returns on capital". When a business can lower a key input costs by 5x in a single year (source below) and another key one (power) by 33x, it should give a prudent person pause when assuming ROIC declines. You move the goal posts again, now claiming the argument is about whether AI being "the next big thing" is consensus. Also, nowhere did I state that "sky is the limit". I'm saying it's a very difficult question to throw uneducated takes on. Source: https://www.seroundtable.com/google-sge-ai-answers-cost-80-less-37326.html

-

In general - maybe. In technology world - too hard, even with a great deal of domain knowledge. Not every market is the same either - chances of another 200K rail miles built in the US (let alone the same ROIC) are not the same as AI becoming the next $1T market. My point is it's foolhardy to throw unresearched (and observably false, like the AOL comparison) analogies the way you did. Investing game has evolved and many value investors that got stuck in "Mr. Buffett" quotes and "buy low P/E" formulas have not a great time. Yet you snidely reduce my words of caution to relying on fantasy. This does seem to be the MO of this board (together with Politics section ranting), which is why a lot of thoughful posters left it for X FinTwit community.

-

The screenshots you posted are in no way a counterargument to my replies to your points: 1) You cannot compare AI stack economics to that of an internet cable 2) Claiming that ROIC will be lower (which you did explicitly and implictly) is arrogant even for someone with domain expertise, and a lot more so for someone without Thanks for the wishes, not all investing edge is in 10Ks and the last 15 years abundantly demonstrated that, so I choose to evolve with the world.

-

Way to shift the goal posts from 'commoditized' to 'much more capital intensive'. They are not, but it's arrogant, IMO, to insinuate that margins and ROIC will definitely be lower at Cloud and AI markets' maturity. The cost curves are extremely dynamic and even the foremost computing/AI experts are not making such prognostications. Case in point - Google lowering power consumption for their GenAI queries by 33x in just one year! CapEx side is easy to see for a value investor used to flying by 10Ks, but the revenue side requires imagination and mental exertion.

-

Tell me you don't understand technology moats without telling me. It's not a valid comparison and DeepSeek showed nothing. Enterprise customers are not deploying DeepSeek, they are deploying MS Copilot (integrated into the Office suite) and Google's AI Studio, not some bare LLM. AI revenue growth of hyperscalers has not slowed down one bit. AI software stack is not a commodity in the same sense as cable/fiber to one's home. AI is being sold as a bundle (models + compute + orchestration + customizations + application APIs + support) and as such is closer to enterprise IaaS/SaaS and will have comparable future/economics. The moat will once again (like with Cloud 15 years ago) come from a combination of scale, distribution, proprietary data, being the lowest cost provider (e.g., Google with TPUs), and bundling/integration into hyperscalers' other products.

-

Has anyone looked into estimating Sleep Country sustainable owners earnings. They have ~$63M in depreciation expense per year, but invest only ~$15-20M in capex. Are they underinvesting in the business or is sustainable maintenance capex much lower than depreciation?

-

Bamsec.com is nice.

-

If you use Google Finance, now might be the time to...

FiveSigma replied to Liberty's topic in General Discussion

You don't need to shut down a legacy product and deprive users of its benefits to build a new product from scratch. It's not that there is no additional 'land' (servers) to build the second system on. I'd believe that whatever they replaced old Google Finance with had atrocious usage decline and they decided to do a v3. -

Hedonic adjustment killed inflation expectations

FiveSigma replied to RuleNumberOne's topic in General Discussion

See the following paper by BLS: https://www.bls.gov/opub/mlr/2006/05/art2full.pdf "While hedonics is an important technique for particular categories, it is important to emphasize that it is used for only a small part of the total index. Moreover, research from the CPI-U Research Series (CPI-U-RS) shows that its impact on indexes often has been modest and of uncertain direction. The CPI-U-RS was created to provide a methodologically consistent index; to this end estimates were made of the quantitative index of methodological changes in the CPI since 1978.34 These included changes to quality adjustment procedures. The estimates in the research series are taken from simulations described in the research for each item category for which hedonics was implemented." "In table 5, a negative sign indicates that the change to hedonic adjustment has caused the index to rise more slowly (or decline more rapidly) than it would have if previous quality adjustment procedures had been used. The inconsistency of the effect is exemplified by the fact that the impacts for washers and dryers have the opposite sign. While the switch to hedonic adjustment had a significant effect on several of the individual item categories, it is important to note that the net effect on the All Items index was negligible. This is because the direction of these effects varied and the items in question had such a small weight. (The total relative importance of items for which hedonics have been implemented since 1998 is less than 1 percent.) Indeed, the net effect of hedonics from 1999 onward (which excludes personal computers, but includes televisions and all later categories) on the All Items index is estimated to be less than 1-hundredth of 1 percent per year, specifically +0.005 percent." -

I did that and muted Gregmal - paradise! ;D

-

‘Tis but a flesh wound ;D

-

Why would China have to approve this deal?

-

Uccmal, how did you get TD to give you a HELOC up to 80% of total LTV with your first mortgage NOT being with TD (i.e., with First National)? In my very recent experience, every big-5 Canadian bank refuses to go second on a property with first mortgage that is not with them, including TD (had a phone conversation with them). The only firm that agreed to do it was Home Capital group, but they cap total LTV (first+HELOC) at 65% of appraised property value.

-

Charlie Munger and the Daily Journal Corporation (DJCO)

FiveSigma replied to a topic in Berkshire Hathaway

+1 +1 +1 -

That's panic. Central Bank of Russia lost control of the currency market. Expect a wave of defaults within 3 months.