UK

-

Posts

1,838 -

Joined

-

Days Won

14

Content Type

Profiles

Forums

Events

Posts posted by UK

-

-

4 minutes ago, Spekulatius said:

I think the US and the western world needs to build some surge capacity to increase the military industrial complex (ha) output when needed. I think one thing we learned is that conflicts could be more protracted then assumed resulting in much higher consumption rates of material and consumables.

Right now, the defense contractors are not capable of providing capacity, beyond what is planned in the budgets and even that isn’t a sure thing with all the political shutdowns. So, there is no surge capacity whatsoever. COVID-19 has clearly showed this with secondary impacts on external supply chains, even though the defense contractors and their suppliers were never shut down (deemed essential work). Yet, the whole supply chain snarled and there wasn’t even a war going on (until 2022 that is).

Talent also is leaving due to retirements and difficulty replacing the jobs because the younger people are not exactly keen on getting this sector for good reasons, imo (economic mostly ). It is not the 60‘s any more and what you read in the book about Lockheed/ skunkwork book.

Some political decisions will need to be made for the longer term.

It seems this is the direction everything is going. The question though, as Buffett used to say, how well this will translate into shareholder returns with defense companies?

-

23 minutes ago, whatstheofficerproblem said:

I don't ever recall brushing my teeth to keep them healthy, I do so to keep them clean and there is an aftertaste in the mouth after waking up anyways and after a day of eating (irrespective of food quantity) I would want my mouth cleaned from all the residue, so brushing is kind of a refresh button.

To me this doesn't seem like a case for less toothpaste sales, but your point is totally valid. I would be worried if I ran a Sweets Business or a Dentist Clinic.

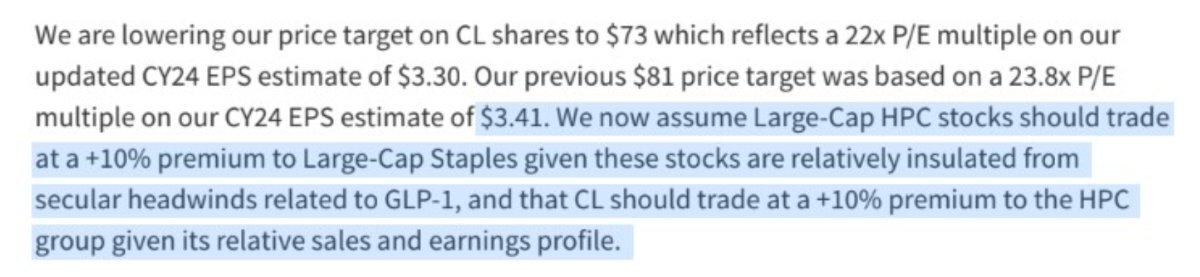

So I was joking, but really, why they downgraded CL?

EDIT: found it, it seems some kind ofmisunderstanding:)

-

6 hours ago, whatstheofficerproblem said:

Sell-side 'analysts' are losing it again. Barclays downgraded Colgate on fears of disruption from GLP-1. Didn't know Mounjaro makes you wanna brush less, bath less and clean your house less. Maybe people shit less which should lead to a decrease in toilet paper sales, but us civilized folk use bidets anyways so I can't speak for them.

More healthy teeth because of less sweets:)?

Lets just hope these drugs will not also work to cure stupidity...

-

-

10 minutes ago, Gregmal said:

We’ve had these rates and higher before so shouldn’t be impossible to model real stuff

True, I always forget this, and than begin to think of it like some kind of end of the world / binary situation.

-

12 minutes ago, brobro777 said:

Oh yea? Well I sold MSFT for mediocre gains before the massive cloud computing take off (too dumb to understand the potential)!

Well, at least you have tried:). Btw, ValueAct, who initiated these changes for good, sold out in 2017 for something like 60 or 70 USD:)

-

2 hours ago, brobro777 said:

Yea I remember taking a shot at MSFT in 2011 when its free cash flow yield was over 10%, while short term Treasuries were 0% and 10 year was around 2%. I understood the negativity with MSFT at the time, with Ballmer as CEO and Windows phones but the company was printing money (and stuff like MS Office were not going away) and what was my alternative, get 0.25% in my savings account?

Now MSFT is $2.5Tril 30X PE because of AI and the cloud, even though Treasury Bills are 5%...

Haha

I passed on MSFT and followed Buffett into IBM!

-

"Sell off the big stocks, the small stocks, the value stocks, the growth stocks, the U.S. stocks, and the foreign stocks. Sell the private equity along with the public equity, the real estate, the hedge funds, and the venture capital. Sell it all and put the proceeds into high yield bonds at 9%."

Listened to Marks memo, all this sea change / higher for longer thesis, it is so tempting to take firmer view, not nesessarily regarding eguities vs bonds, but just in equities, one could make very different bets (in terms of duration and rate sensitivity, kind of AMZN vs FFH), IF was sure that rates really will stay higher for longer. I am positioned much more into this direction vs a year ago, much more than 50/50 currently, but just not sure if it is prudent to get into 100 per cent this time is diferent side. My gut still feels like it is better to stay 50/50 or n9 more than 70/30 on this:)

-

27 minutes ago, thepupil said:

2011.

real and nominal yields are drastically higher and ERP's much lower today than in any time of my career (which is short and does not at all comprise the numerous scenarios both backward looking and forward which might occur).

from my college graduation to present the 10 yr TIP has yielded 500 bps less (on average) in real yield than SPX, for the first few years that number was 800 bps. That's now 238 bps (2.3% real 10 yr TIP, 4.66% nominal earnings yield, SPX)

Using nominal 10 yr tsy's, the average has been -300 bps, with the first few years** (2011/2012) being -600 bps. Now its 5 bps (10 yr yield and SPX earnings yields are the same).

I'd therefore say that on a simplistic yield comparison using broad liquid indices, that bonds are more attractive than they have been over last 12 or so years (post GFC era).

of course there are individual securities of both types that will be better/worse than anything over this time frame (your greek bonds being a nice example).

** I remember lots of Jim Grant (and Jeremy Grantham)** articles from the 2011/2012 time frame talking about buying blue chip high quality widow and orphan stocks for like 11-14x earnings (think WMT, JNJ, LMT, GOOG even, MSFT even, UNH, etc). Back then it was very clear to me as a 20 something to be all stocks. and you got paid handsomely for it. I use those folks because they are often painted as permabears. even with there bearish value oriented bias, they couls see risk/reward much better in stocks. I think the picture is far more murky today.

Thanks. Interesting! I somewhat agree with this view on relative attractiviness of averages between equities and bonds, but if, like you said, one can go after individual securities and has required return of at least 8-10 per cent, it seems to me it is still easier to find such things in equities. Or maybe this is delusional and influenced by some biases. Maybe if choice was only between bonds or snp, 30/70 or 40/60 already would make sense today. Sure, today is nothing like 2011/2012, but this period was extremely attractive, perhaps even more than 2008/2009, at least for me, because in 2008/2009 it was like REALLY scary (especially if you listened to almost anyone except for Buffett and Co:)) and in 2011/2012 it was more about EUR, but US was fine, rates low, equities, even on average, still very cheap.

-

34 minutes ago, thepupil said:

I don’t think he’s marketing to wealthy individuals, but rather (mostly) non tax paying institutions.

non wealthy to moderately wealthy people have 401ks/IRAs/annuities etc. very wealthy people have private placement life insurance that remove the tax friction.

regarding defaults, agree completely the common practice of quoting gross yields in risky credit is somewhat misleading, but I’m not sure of a good alternative because everyone will have dofferent default rates/LGD.

I agree that 6-8% pre-tax is more or less what’s on offer at this time, most safe stuff I’ve seen being closer to 6 on the long end and 7 on the short end. Extreme safety being ~1% lower then going up from there with credit risk.

pre-tax seems pretty competitive with stocks, when get at computer, I’ll run what % of 5 year rolling periods >7% for stocks, my guess would be like 60%-80% or so but not sure. If you’re starting from “with no knowledge, strictly backward looking, this has 30% chance to beat stocks” and overlaying a little bit of bearishness/caution/relative value judgement, think it’d make sense to own some bonds (and would be dumb to own all bonds /no stocks).

it at least makes more sense now than any time in my short time as an investor.

Since what year you expierience starts? I only owned local government 10 year bonds yielding 10 per cent in 2008 (currently at 4.4) and later was looking, but not invested, at long term Greek bonds, yielding some 30 per cent (currently 4.3) at the time of the crisis:). These Greek bonds ended up a very good buy for some who did it:)

-

1 hour ago, Viking said:

@Thrifty3000 and @UK and @SafetyinNumbers (and others), thanks for wading in on this topic. It is great to be able to get others perspectives and debate ideas. Slowly I am learning (yes, I hate that when it happens!).

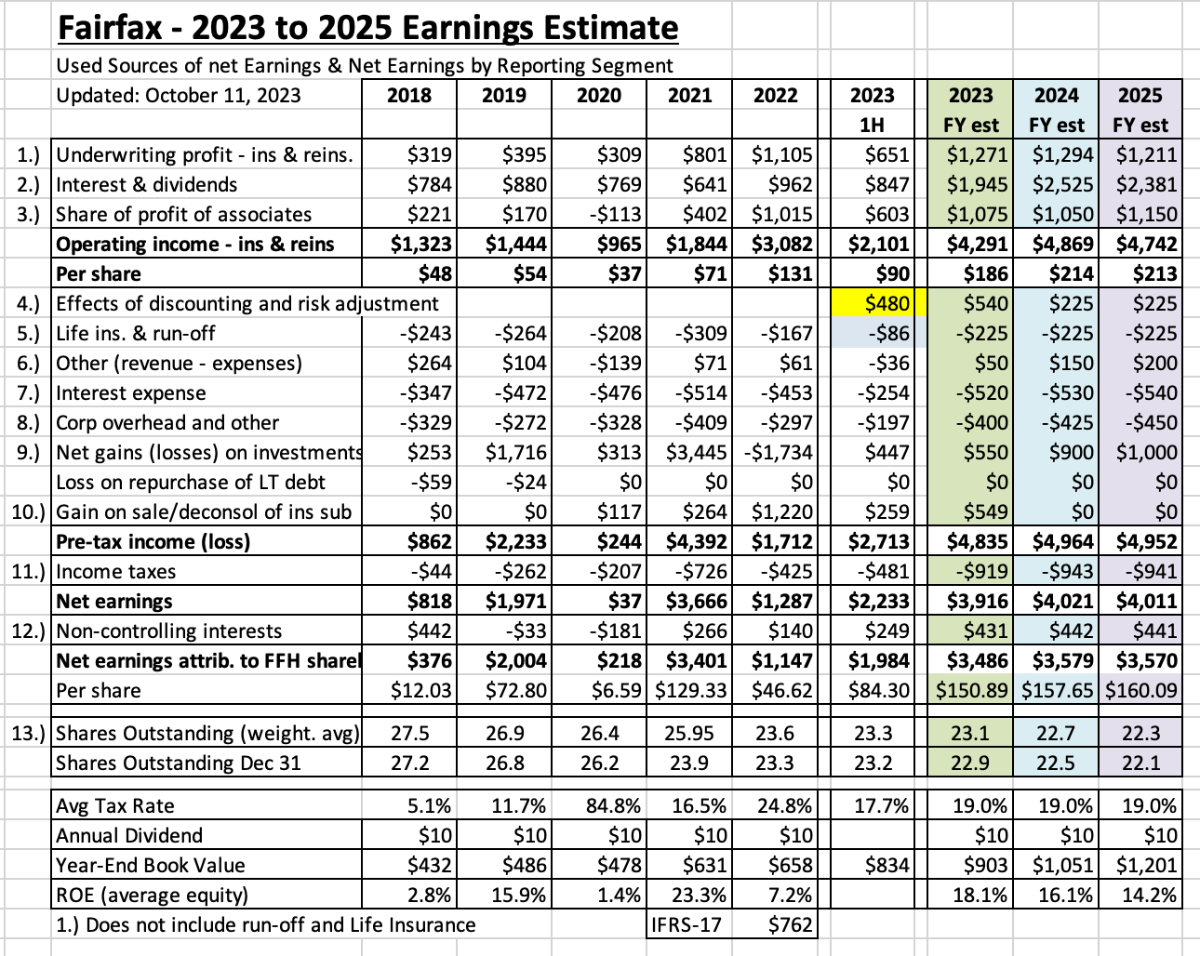

I have made a few changes to my 2023-2025 forecasts for Fairfax, based on the feedback I have been getting from my last update (just a couple of days ago). I think I have said before, I am constantly updating my model to reflect 'new news' (usually weekly). Please keep the questions and comments coming... I will keep making updates to my model and I will keep the updates coming. Continuous improvement is out goal...

1.) For 2024 and 2025, I adjusted 'Effect of discounting and risk-adjustment' down. The 2023 number has been increasing as interest rates rise. My assumption for 2024 and 2025 is interest rates stay roughly where they are today - of course, this will likely not be the case. So, I think it makes sense to go with a lower number for 2024 and 2025. Is this number still too high? Too low? Not sure. Like all the other numbers in the spreadsheet, I'll keep an open mind and adjust as needed moving forward.

2.) For 2023, I adjusted 'Effect of discounting and risk-adjustment' up and 'Net gains (losses) on investments' down to reflect the continued increase in bond yields in Q3. Currency will also be a headwind for Fairfax in Q3, given the US$ strength.

Putting it all together, my new forecast is earnings of about $150/share in 2023 and around $160/share in 2024 and 2025.

The bear market in bonds had an impact on Fairfax in Q2, 2023. It will be the same in Q3, 2023. So today I am thinking earnings in Q3 might come in closer to $20/share (unrealized losses on bonds/currency will be the headwind). That would put Q4 earnings closer to $40-$45, which seems reasonable (and assumes the GIG acquisition closes in Q4).

Please keep the questions coming... the more questions/discussion/debate the better.

Thanks, Viking! With so much moving parts and different earning streams, FFH is one of the companies, which earnings is extremely hard to model (and maybe it is a plus and an opportunity vs analysts/market), but I think you did an incredible job doing this.

-

1

1

-

-

22 minutes ago, SafetyinNumbers said:

It’s funny, I read the same post and it made me think I was right. I think to take out the IFRS17 plug, you have to assume no premium growth which isn’t consistent with the rest of the forecast.I think you are right, but the question is size of the plug, since YTD it was probably partly/mostly interest rate driven and the impact of reserve growth alone could be much lower in the future?

-

41 minutes ago, giulio said:

The accounting changed but the economic substance did not. I think it is not worth it to focus on the impact of discounting/interest rates. it will move up and down, like mark-to-market investment gains (which should be excluded from earnings and not projected forward).

I try to measure look-through earnings instead.

I try to understand if they are writing profitable business and what CR will be over a cycle.

I think Mr. Watsa said on CC that IFRS 17 will not have any impact on the way FFH conducts business, so let the equity research analysts deal with this mess in their models!

focus on the business, don't let the accounting obfuscate economic reality.

Well, I agree, but if you still want to model any future EPS/BV, as Viking does, you have to decide what to do with this item:). Perhaps to stay conservative one can omit it altogether. Look through earnings is an alternative/different way to look at investment portfolio, I agree it may be better in some respects, but maybe not for EPS estimate.

-

12 hours ago, Gregmal said:

Even Kashkari, who's made some pretty out of touch remarks, today made some very interesting comments with regards to rates. One part basically saying it was totally perplexing that people would be selling off 10y+ treasuries under the assumption that the Fed is going to be more aggressive from here. "head scratcher" think was another term he used.

May have to check out some of those Pupil2066 Floaters.....not joking.

I think they are/were selling of more not because of the assumption what is Fed going to do, but because of supply/demand issue: just to much borowing and at the same time QT and less demand from China/Japata/etc. Market obviously like Fed paying attention to this issue though:)

-

“If wage increases become clearer at the beginning of next year, and if interest rates in Japan are sure to rise, Buffett may buy in early next year,” said Masatoshi Kikuchi, the chief equity strategist at Mizuho Securities. “I think there is still potential for major bank stocks.”

-

2 hours ago, Viking said:

@Thrifty3000 I don’t think i can give a better explanation than @SafetyinNumbers has already provided. I would appreciate others providing their thoughts - that CofBF collective wisdom thing.

‘My estimate here could be a little messed up.’ Bottom line, i am still learning about this bucket. It will take me a few more quarters to better understand the build and see how this number evolves at Fairfax. As i learn more i will update my forecasts.

I think we already have discussed this before and I definitely can not claim that SafetyNumbers is not right on this, since I do not understand this myself completely (and who does?), but my initial understanding on this was in line with Thrifty3000's, meaning that large recurring gains from this item would be produced only if rates increase further substantially. But it seems it also depends on the change of net reserves, as SafetyNumbers has stated, so in the end it seems it depends on two variables: discount rate and net reserve change, and the final result for any period will be impacted by both. So I think this probably means, that such large initial benefit from applying this for the first time will not be repeated in the future, unless rates moves up substantially, despite of reserves growing at a steady pace. In such case (no rate change, reserves growing steady), my guess, the impact would still be positive, but way smaller?

From 2q CC:

Under IFRS 17, our net earnings are affected by the discounting of our insurance liabilities and the application of a risk adjustment. In the second quarter of 2023, our net earnings benefited $221 million pre-tax from the effects of discounting losses occurring in the current quarter, changes in the risk margin, the unwinding of the discount from previous years and changes in the discount rate on prior year liabilities. As interest rates move up and down, we will see positive or negative effects on earnings from discounting.

From 1q CC:

Tom MacKinnon

Great. Yes, Jen, I was just wondering, the things that really impact IFRS 17, the change in the risk adjustment, the unwind of the discount, the build of the discount and the change in the discount rate. So, if we kind of had a flat interest rate environment and pretty well steady state with respect to your growth. Would all of this noise be pretty minimal, like what kind of conditions would make this noise show up more to the positive or actually show up more to the negative?

Jennifer Allen

Yes. Sure. It's a good question, Tom. So, the way I think if you're in a steady state, if your underlying net reserves from a risk profile duration does not change, then as you unwind your discounting that you don't have a change in your discount rate, it should really be offset and really don't see a huge impact. The other side of it is, your risk adjustment would be steady state, you would be releasing your risk adjustment on your old book, but you would also be setting up the same risk adjustment on your new book. So it's only when your book grows, so if your net reserve starts to grow, you'll start to get that net benefit through again, if it shrinks, it would be a negative impact to your total portfolio.

Tom MacKinnon

And then on the change in the discount rate, is that just generally, if we have a flat interest rate environment, then we wouldn't get that noise as well, I assume.

Jennifer Allen

Correct.

-

14 hours ago, Kuhndan said:

Todd Combs - Investing, the Last Liberal Art, Oct 9th, 2023

Edited 5 hours ago by VersaillesinNY

That was awesome! Thanks for posting

INTJ:). Boy, I would love to know his opinion on FFH!

-

-

6 hours ago, TwoCitiesCapital said:

Higher rates/inflation HASN'T been stimulative and most people have been hurt by them

I will not argue otherwise:). But for all the fear of what would happen, when rates went up so fast so much after such long of crazy low period, so far real economic damage seems incredibly low and the fear of it seems almost disappeared in the main asset markets, after big initial scare last year. Large companies (snp500) paying less interest than receiving (and this will continue for a while) and majority of homeowners having locked their mortgage interest very low for very long, I think maybe explains a lot of this resilience, since these two are the main assets? Also, sure higher rates is not stimulative for many other reasons, especially for asset prices, but in real economy, somebody's interest costs is someone's interests gain, so partly it is only some kind of redistribution? But I am really surprised myself how well everything going in real economy and in market, despite this 'epic' rate increase and bondageddon. And even in countries without long fixed term mortgages, so far nothing really bad is happening, and in a few places, where housing did went lower more noticeably (Sweden, maybe Australia) it is stabilising or going up again, while rates are sill high. And the only large and obviously bad place in terms of all this is China, which paradoxically keeps lowering already low rates:). So I am really perplexed bu all this, but maybe it is just what a normal environment looks like? Meaning more or less normal rates, without anything bad happening. Like also, didn't we had dotcom with something like 4-6 per cent rates? Go figure:)

-

-

49 minutes ago, cubsfan said:

I said I didn't know - and neither do you. If you want to believe the numbers the US and Ukrainian government gives you - have at it - I really don't give a shit.

The war is not exactly going as claimed before the spring offensive was launched.

Hey, it sure is not going as claimed in the very begining (or almost every day still) by another side either? If one does not consider Ukraine holding (and retaking so much territory) so well against, supposedly second major military force on earth, a success, than I do not know what success is. And they achieved this even without enought equipment, aviation etc to begin with.

-

4 hours ago, MMM20 said:

Are those prefs a better risk/reward than the common at a ~18-20% earnings yield?

You know, it is very good question to ask and not only vs preferreds. But if one to agree with you yield asumption (which I more or less do), it is really hard for something else to compete with it (or even to clear this hurdle). Even such seemingly cheap stocks, like M or C or something from Oil and Gas, or you name it, they are more or less as cheap, yet I would argue, that FFH is of a much higher quality and much better for a long term holding.

-

3 hours ago, VersaillesinNY said:

Todd Combs - Investing, the Last Liberal Art, Oct 9th, 2023

Thanks!

-

42 minutes ago, mattee2264 said:

Isn't this metric a bit meaningless now that US companies are so global. Obviously a lot of the market cap is inflated by Big Tech companies but they have eaten the world.

I think it was Munger who said a while ago on this subject something like this: "just because Warren said something that was true 20 years ago does not necessarily make it true today".

Is Europe becoming uninvestable?

in General Discussion

Posted

https://www.economist.com/europe/2023/10/12/our-european-economic-pentathlon