mengan

-

Posts

125 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by mengan

-

There is a fix fee component as well. Nothing prevents the managers from coasting on that fee.

-

This is how I look at FFH economic earnings. Example for 2024: Cash from operating activities before changes in working capital 4,509,700,000.00 Depreciation, amortization and impairment charges (551,400,000.00) Amortization of share-based payment awards (164,900,000.00) Other, incl. depreciation of right of use assets Interest Paid Interest paid on lease liabilities Free Cashflow to Firm Before Change in Working Capital Allocated to Increase of Working Capital Free Cashflow to Firm (FCFF) (202,400,000.00) 508,800,000.00) 57,300,000.00) 5,224,200,000.00 (1,067,100,000.00) 4,157,100,000.00 Applied to multiple years, you get the following graph per share. This assumes no adverse (huge) insurance event that undermines the reserving. Reduce Interest Payment to get to FCF to equity owners.

-

Those are one-time events. If you do a DCF, you will see that the perpetual cash generation over the long term overwhelmingly determines the intrinsic value of a company, not short term fluctuations.

-

huh? Insurance has been around for thousands of years. As long as there are humans around, there will be a need for insurance.

-

People remember you being cheap. Sooner or later, that will impact deal flow in a negative way. Deal flow over the long term is much more important. So if there is any reason to be "fair and friendly" that is aligned with shareholder interest, that would be it.

-

Getting hilariously bubbly. Looking forward to the inevitable implosion.

-

I'm sorry, but I wouldn't trust Grok with a 10000 foot pole, especially on its predictive capabilities.

-

This is an oversimplification. You cannot "remove" risk, only shift it through different parts of the value chain. If robots are driving instead of humans, the risk doesn't disappear, it falls to either the manufacturer, owner or operators of the robots. Change in insurance pricing will depend on the difference in probability for an accident to occur between a human driver and a robot driver. Not all scenarios will have robot drivers be drastically safer than humans.

-

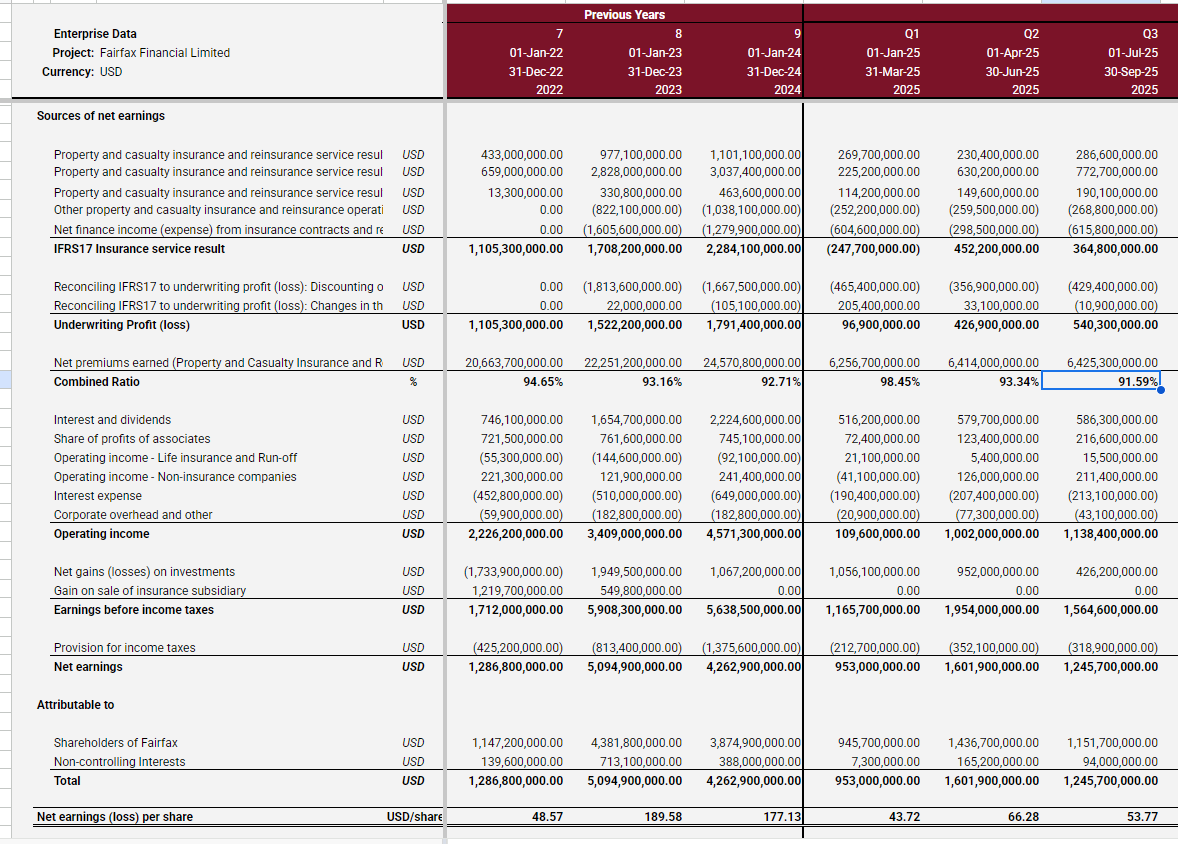

Also combined ratio is 91.59% for Q3, not 92%. Not sure why it was rounded up to 92% instead of 91.6%

-

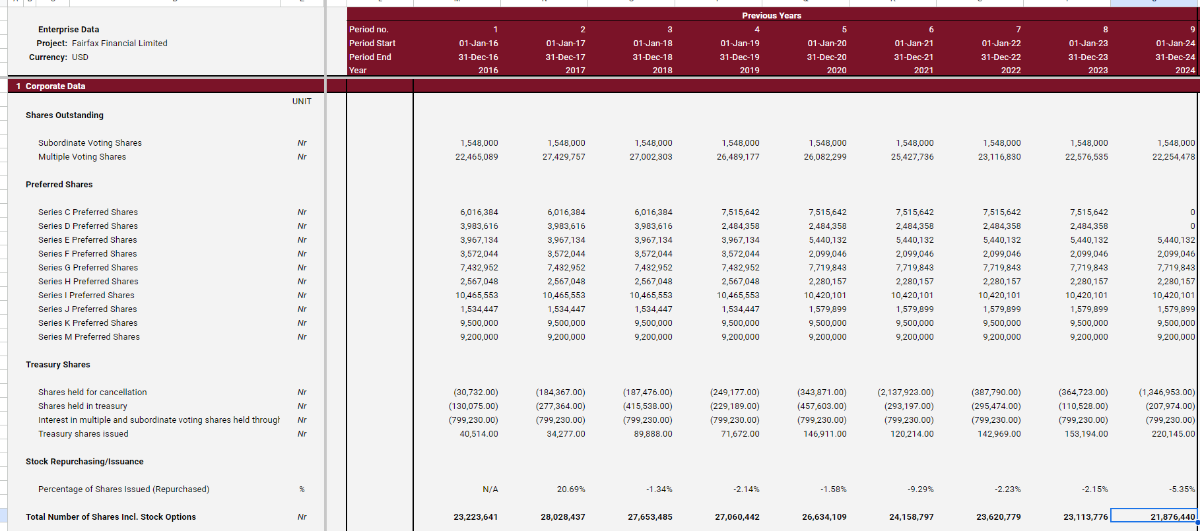

Back to 2016

-

https://www.theguardian.com/business/2025/oct/16/us-regional-bank-stocks-fall Financials in free fall today.

-

This. Buying government bond is by default a macro bet.

-

It is a bit like BRK playing chess against itself. No doubt BRK will benefit from this acquisition, but not as clear as if they didn't own all the common.

-

I would almost bet Brad is thinking along this line. If the yield curve would be steeper, there would be a larger incentive to increase duration.

-

Adding a Holdco on-top of two shoe companies is not necessarily better as it adds another layer of management overhead. If they are underperforming, maybe best is to restructure them rather than slapping on a holdco.

-

More Japanese trading houses

-

Seems they did. Just noticed. Converted bonds to equity and then added additional shares beginning of August. Metlen re-domiciled in the UK and did a capital restructuring, resulting in a 10% squeeze out of old shareholders. The remaining share count is 129.02M. Fairfax now owns 9.25% of the new UK based Metlen PLC.

-

Additional FYI, there are some foreign holdings not reported in the NAIC/Gen RE or Dataroma, mainly smaller foreign holdings. Not 100% sure how accurate it is: Naito: https://simplywall.st/stocks/jp/capital-goods/tse-7624/naito-shares/ownership YG-1: https://simplywall.st/stocks/kr/capital-goods/kosdaq-a019210/yg-1-shares/ownership

-

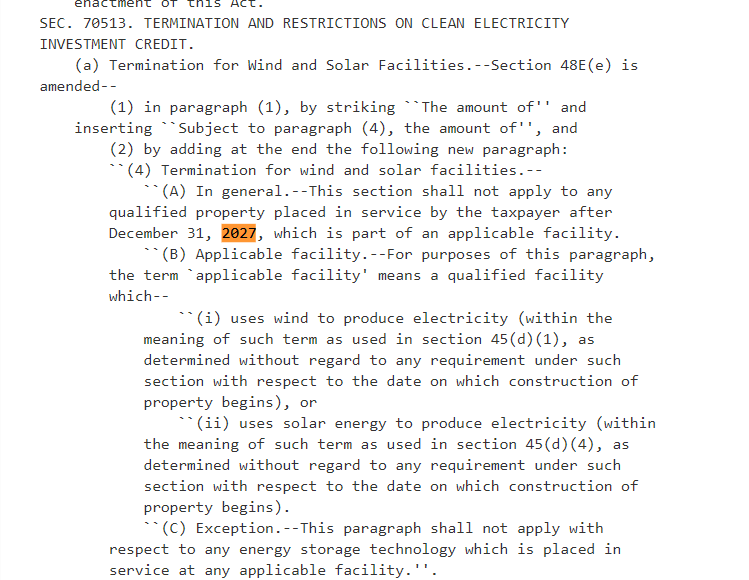

It will likely become messy over time over what is considered maintenance capex where this "grandfathered" tax credit is retained and what is considered a "reconstruction" or "upgrade" where the facility must receive a new "placed in service" date, and where the tax credit is lost.

-

Right, that point is an important distinction I missed.

-

I don't see changes in the OBBBA that would add direct tax credit from investing in non-renewable PP&E, only a permanent extension of the bonus depreciation introduced under the Tax Cuts and Jobs Act at 100%. Without direct credits, at best, BHE will pay $0.00 tax, but not negative as they do now (i.e. receive money back).

-

2027. But the bill is really hard to read.

-

Dupe

-

I used AI to help me dig out the parts of the OBBBA that could affect BHE Termination of Clean Electricity Production and Investment Credits (Sec. 70512 & 70513): The termination of the Production Tax Credit (PTC) and Investment Tax Credit (ITC) for wind and solar facilities placed in service after December 31, 2027, is arguably the most significant threat. These credits have been fundamental drivers of investment in wind and solar energy. Their removal would likely increase the cost of new renewable energy projects, potentially making them less competitive with other energy sources. Termination of Cost Recovery for Energy Property (Sec. 70509): Repealing favorable depreciation rules (cost recovery) for energy property construction beginning after December 31, 2024, would reduce the tax benefits associated with building new energy facilities. This directly affects the financial modeling and returns on investment for new projects. Phase-Out of Advanced Manufacturing Production Credit (Sec. 70514): Terminating this credit for wind energy components after December 31, 2027, would impact the domestic supply chain for wind turbines and other essential parts. This could lead to higher equipment costs for wind projects. Termination of Clean Hydrogen Production Credit (Sec. 70511): For any part of the business focused on emerging clean energy technologies, the termination of the clean hydrogen credit by January 1, 2028, curtails a significant incentive for development in that sector. New Fees and Revenue Sharing on Federal Land (Sec. 50302 & 50303): The introduction of new acreage rent and capacity fees for renewable energy projects on federal land would increase operational costs. The revenue-sharing provision, while directing funds to states and counties, represents a new financial obligation on these projects.

-

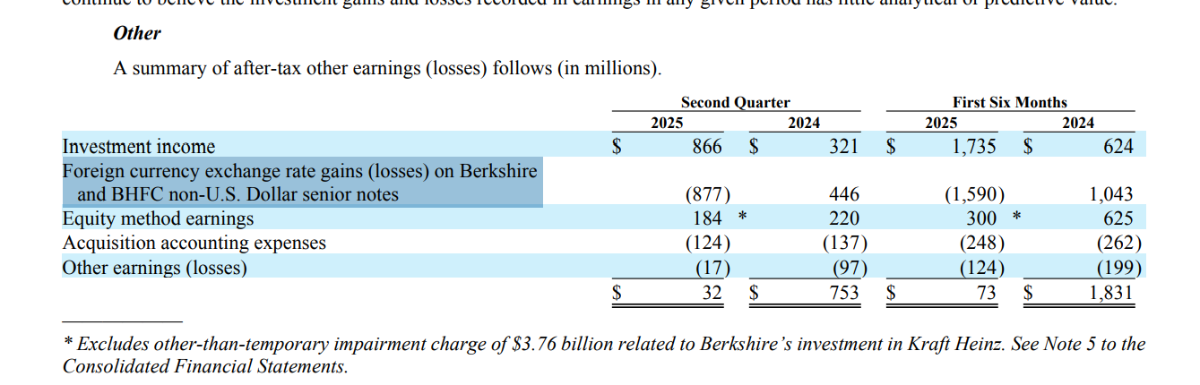

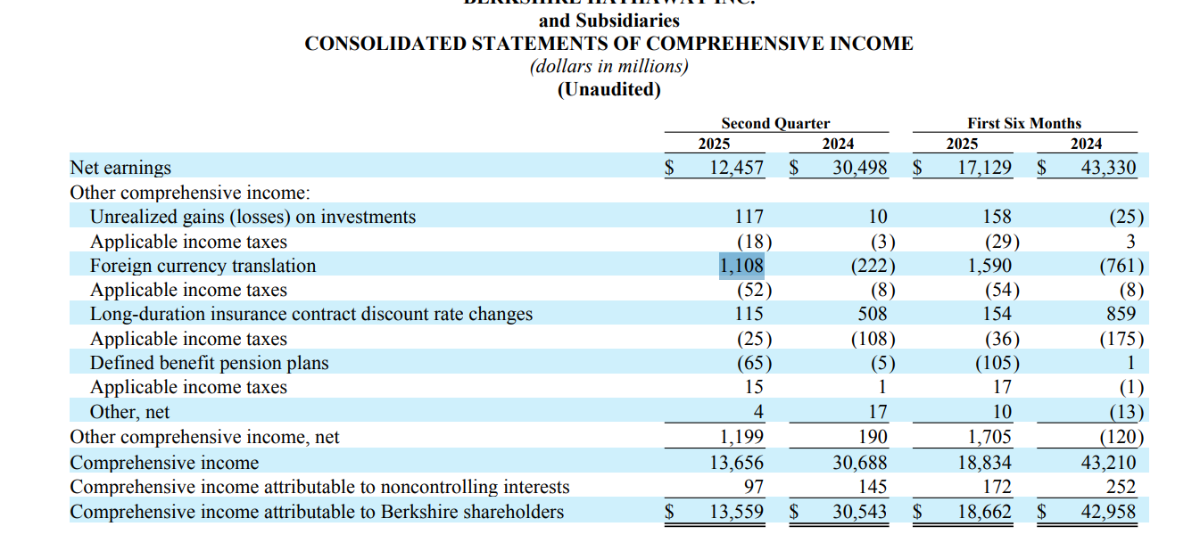

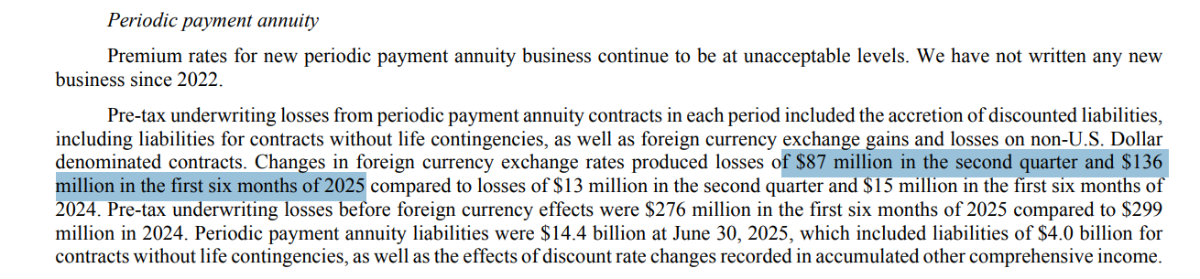

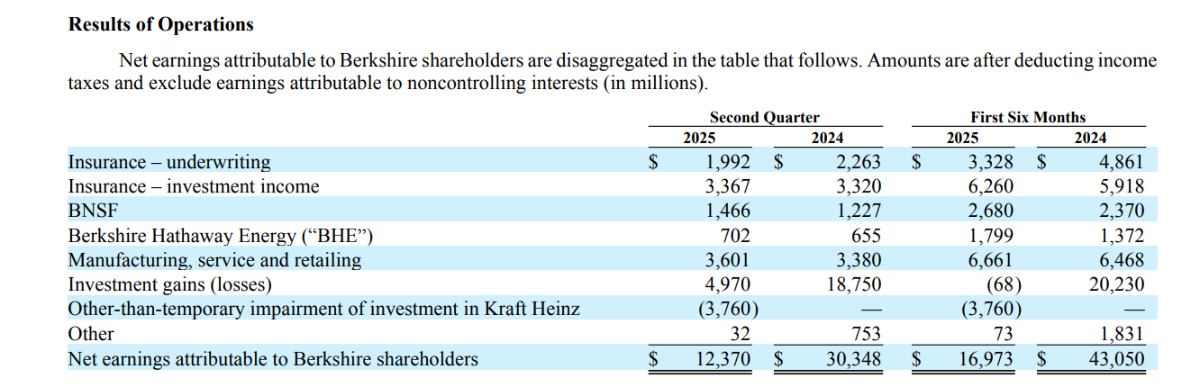

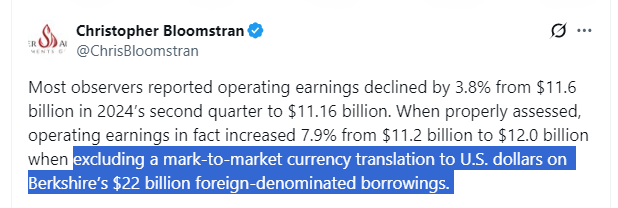

The currency movement is spread out across various line items. They are all consolidated under Comprehensive Income where losses are "added back" (positive) and gains are "reduced" (negative). Under Management Discussion, a component of "Foreign Currency Translation" under Comprehensive Income is broken out for the senior notes. Similarly, under Retroactive Reinsurance and Periodic Payment Annuity What is missing is another 56M (1,108 - 877 - 88 -87 = 56) which I assume is hidden amongst Manufacturing, Services and Retail units. Also, non-USD denominated investments are also affected by currency movement and is baked into the quarterly Investment Gains & Losses line item automatically and is not part of the comprehensive income adjustments. Bloomstran only considered the currency adjustments from the senior notes, not from the insurance operations and others. (12,370 - 4,970 +3,760 + 877 = 12,037), so he is off by 231M.