mengan

-

Posts

125 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by mengan

-

Yuck. This clearly incentivizes stock promotion. You will likely see him running around different news channels promoting HHH. Very on point Ackman. This type of attention is in his comfort zone.

-

There's three reasons for this discrepancy. 1) The triangle does not consider effects of reinsurance. 2) The triangle does not consider currency effects. 3) The triangle shows individual years, not aggregate change to reserves for all prior years. Add these three, and the number will likely match Prem's comments about reserve release. So Prem is using a very optimistic reading of the above triangle.

-

Even 10x will unfortunately still be a small footnote compared to Fairfax as a group. And 10x in a decade is a 25% CAGR. Ambitious but not unreasonable.

-

Interest and dividends are from non-consolidated and non-equity method accounted holdings as well as fixed income investment. Fixed income interest is calculated as coupon rate times par value.

-

consolidated non-insurance earnings (before tax) is Non-insurance revenue minus Non-insurance expenses. Just the sum is not stated.

-

Diluted per share is also not well defined, since there are many ways to structure share based comp, some of which aren't considered in the diluted share count. An example is already authorized and clearly allocated capacity of RSU/Options for share based compensation but which has not yet been issued. Those are NOT counted as part of diluted share count, even though realistically, those RSU/Options are all but certain to be issued in the near future.

-

A normal SBC-program where shares are "printed" also runs through compensation expense. So it works similarly. One is cash other is non-cash.

-

The government is probably out of touch with market reality. From my experience, uninformed sellers tend to ask for fantasy prices. Especially private sellers of real estate.

-

Sounds like Barrack engineered Erkan to be on the Fairfax board. Question is who is benefiting from her installment on Fairfax, Fairfax, or Barrack.

-

There is nothing preventing managers from selling shares the moment they are granted (and vested). Which has been the case. Options, RSU and shares function the same from an incentive perspective. It's mainly cashflow and tax treatment that is different among them.

-

Same, it's unfortunately a bit too expensive to justify flying out to Canada as well as book accommodation when there is an online version.

-

Risk is opportunity cost.

-

Backward looking worksheets never end well. I hope he is also adjusting them based on forward looking IRR expectations based on conservative "projections".

-

Lmao, Warren is adjusting limit buy/sell orders every day before market opens.

-

https://pdl-iphone-cnbc-com.akamaized.net/7000408353/29ad3e00-2d02-11f1-8f86-c1d0de0e2279/1774962249-44934765529-hd_L.mp4 Nvm, found it

-

any got a copy of that 1h interview?

-

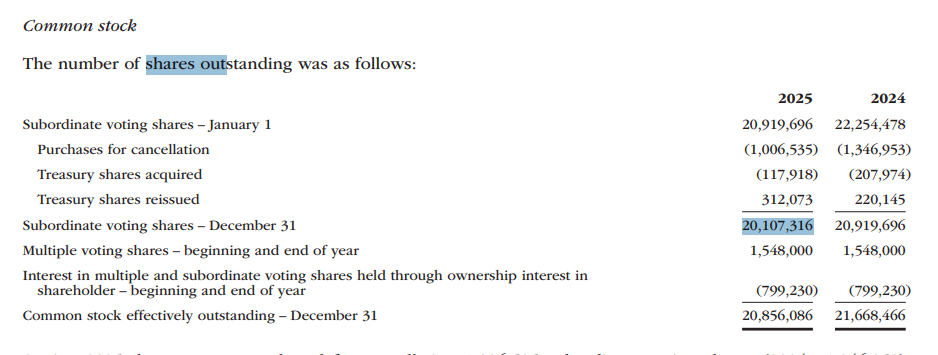

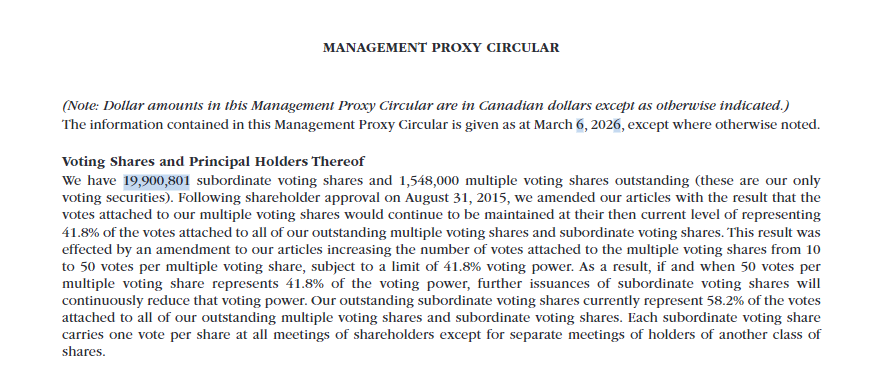

From the Proxy statement: From the annual report: Am I correct to read that they cancelled 206,515 shares by 06.03.26 compared with 31.12.25?

-

I bough MGY late December last year.

-

FYI, going through the last call (Q4 2025). This below jumped out as the weakest part of the call. The charitable interpretation is that runoff asbestos/environmental truly is messy and hard to forecast. The less charitable interpretation is that they still do not have a crisp way to explain why shareholders should feel confident the bleeding is near an end. ---- Daniel Baldini Thanks. Thanks for taking my call, and thanks for the wonderful results. So with that said, my question is: Is there any end in sight to these losses from the runoff business? You've disclosed them separately for, I believe, the last 10 years, and when I add them up, it comes to almost $1.6 billion. Now, I understand that there are reserves associated with this business, and they produce investment gains, but I can't imagine that when you sort of entered into these deals, you expected losses of this magnitude. So a little bit of color there would be great. Thank you. Peter S. Clarke Sure. Sure. Good question. A lot of these liabilities, we inherited through acquisitions, back in the late 1990s, early 2000s, and they're really latent liabilities. There are asbestos, environmental pollution claims. And, you know, we have a specialized team that we've segregated these claims, and they're focused on it. We would, I would say personally, they're best in class. They've been managing these liabilities for a long time, but they're very difficult claims. And, you know, in the United States, it's very litigious and, you know, there's continuing, especially on the asbestos front, you know, some of these claims are 30, 40 years old, and, we look at them every year. You typically, you can't use general actuarial techniques to come up with the reserves. It's a matter of reacting to what happens. Hi, hi, Denise? Denise, are you there?

-

nvm, found an audio only versionhttps://www.youtube.com/watch?v=YKGqOS0kE3Q Starting at 13:28

-

https://www.cnbc.com/video/2026/03/05/watch-cnbcs-full-interview-with-berkshire-hathaway-ceo-greg-abel.html Can anyone re-upload this to vimeo or youtube?

-

I just want to add that book value is itself a flawed metric as it is a capitalized value. This means that someone made a decision on how much the underlying assets are worth, either based on deterministic formulas (for non-listed assets) or the crowd's collective idea of the value (for publicly listed assets). I think in both cases, that value is likely to be completely wrong relative to your individual "discount rate" based on your individual risk tolerance and IRR expectations. A better way to look at the value of a company (any company) is to go directly to free cash flow, including any look-through cash flow from associates and publicly listed assets partially owned by the company; then capitalize it yourself to arrive at a personalized market value that you are willing to pay.

-

Mainly due to IFRS accounting related to Net finance income (expense) from insurance contracts and reinsurance contract assets held. Also due to a giant "one-time" addition to life insurance run-off. One-time = likely recurring.

-

Says all:

-

https://www.easterneye.biz/fairfax-financial-acquires-veeraswamy-owner/