dartmonkey

-

Posts

642 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by dartmonkey

-

In TDW I buy the more liquid FFH shares with my CAD currency and then journal them over to the US side uniquely because the annual dividend is paid in USD and I don't want TDW to do the currency conversion at their very unfavourable forex rate, with a loss of about 2%. For most of my accounts which are with Interactive Brokers, I don't have this problem, I just buy the FFH shares in CAD and the USD dividend stays as USD unless I decide to do the forex conversion myself, at the exact current exchange rate for a commission of about $2.

-

«Greg Abel is an extraordinary executive who in my opinion is far more talented than I am and is at the correct age for such a challenge,” Sokol said in an email. “I wish him nothing but great success.”» Berkshire’s loss is our gain. It is indeed odd that the WSJ would say he’s low profile, buying a few houses and managing his family’s investments, without mentioning that he is chairman of Atlas Corp, the owner of Seaspan, which is the world’s largest independent charter owner and operator of containerships. I wonder how much time he spends on Atlas, compared to his other investments?

-

I got mine on Thursday from Interactive Brokers Canada, just in time for the sale. (I bought another 2% but far from the bottom price, $2310 I think.)

-

I think book value is as important as ever but it needs to be used in conjunction with ROE to come up with a P/B that reflects intrinsic value. If you are at 1.4x book and you are getting 15% ROE (both of these numbers are on the conservative side for Fairfax), then you are really getting an earnings yield 15%/1.4=11% for every dollar invested, which is just another (perhaps better) way of saying you have a stock with a P/E of 1/11%=9. IOW if you need the ROE to make sense of the P/B (which I agree you do), then you are really hankering after P/E, not P/B. And it’s a bit hard to see why we should care about P/B if we have P/E. Do you agree with this line of thinking?

-

Possibly. On the other hand, we’ve had these obvious problems for ten years and, although 1-2 years ago it looked like we might deal with them, there’s very little hope of that now, it is just more b.s. with a little less of the moronic look of the previous government, but basically the same values and policies. So our political situation is depressing from a Canadian citizen’s standpoint, yes, but from an investing standpoint, it is nothing new, and in any case, the vast majority of Fairfax’s business is not here anyway, so it doesn’t change the investing case very much.

-

Given how conservative they are, if they booked a gain it was probably a success. Given the fact that we don’t know how much real estate they kept nor what percentage of revenues nor for how long they expected to collect those revenues, it is impossible to say, but if Fairfax said they bought it for $237m in 2018 and sold it in 2021 for $90m while booking gains of $86m at that time, it seems the value of what they retained was $237m+$90m-$86m=$241m. A $86m gain on $237m represents about 11% annualized. We don’t know how that value has evolved since 2021 but I haven’t seen any write-off, so I think it’s safe to say that this was actually quite a successful investment. Would that all my not great investments should be this bad!

-

Can they do it by swapping dollar-based holdings for the non-dollar based holdings of US persons, e.g., a UK holder of U.S. treasuries swaps assets with a U.S. holder of gilts? That would reduce the gross amount of foreign dollar-based holdings. Foreigners AND non-foreigners can influence the price of bonds is a lot of them (unlike myself) have lost confidence in the long-term perspectives of the US economy, and wish to reduce their holdiings of US treasuries. Obviously this does not affect the number of treasury bonds that are in circulation, but it could conceivably reduce the price where a a willing buyer can be found to take up the bond from the willing seller. However, if the US govt looks like it might be in for a run of inflation (for instance, because a Fed president who is relatively hawkish monetarily is being replaced by one who will drop short-term rates and let inflation get out of control, or just because there is no end in sight to huge fiscal deficits), you might also get longer rates going up, not down. We are probably not going to be able to figure this one out, nor much less change each others' minds about which direction rates are going. Fortunately for us, we don't have to !

-

I don't know that we can take much comfort from this, but the Fed being in a cutting cycle or a tightening cycle makes little to no difference to what long-term rates will be. Those are set by market forces, not the Fed. Here's what Grok has to say (and I agree with it): "yields on 10-year or 30-year government bonds like U.S. Treasuries, which serve as benchmarks for mortgages, corporate bonds, and other borrowing costs) are shaped by market forces rather than direct central bank control (unlike short-term rates set by policy tools like the federal funds rate or ECB deposit facility rate). Ultimately, long-term rates are going to be what the market expects interest rates to be in the long term, and so if the Fed cuts rates a lot this year and sets off a bout of inflation, and rates have to rise afterwards, we should expect that long-term rates will not be impressed by those Fed cuts.

-

Announcement of TSX 60 inclusion: Friday Dec 5 after market close, closing price was US$1679, and it was was $1758.79 at Friday's close, with US markets closed today. In C$, FFH was $2321.37 on Dec 5, closed last Friday at $2436.42, and is down to about $2413 right now. So the price is still about C$100 higher than before the announcement, and the share price was a bit lower than today's price during the first trading day after the announcement (it was between C$2390.50 and $2439.60 on Monday Dec 8, as the market took a day or so to digest the information). But it is quite true that, apart from that first trading day after the announcement, the price has not been so low. My bold predicition is that today's price will turn out to be the lowest of the year. Oh, to not already have a 46% stake - but maybe another 2-3% would be a good idea...

-

Fairfax’s stake is now worth over US$5.5b, on top of possibly more realized gains from sales last quarter required to keep them from going over 33%. For context, Fairfax has a market value of US$39b. At 14%, Eurobank does not represent quite as large a proportion of Fairfax’s market cap as Apple did for Berkshire at its peak (about 25%), but (a) it may eventually and (b) at 8.5x earnings, it’s not as worrisome as far as overvaluation.

-

We have talked a lot about the unrecognized difference between carrying value and fair value, and that is likely at least $2.5b, and probably more, and about 20% of that represents future tax on unrealized capital gains. But Buffett is talking about the much larger unpaid taxes on ALL the capital gains on holdings, including those that are marked to market. In Fairfax’s case, this would include things like the Orla holding. In the 2024 AR (p.41), Fairfax puts this at $514m (deferred income tax liabilities), and I believe this does not include the deferred tax on gains beyond carrying value. So the total may be about a billion last year, and with the market gains this year, substantially more now, perhaps $1.5-2b.

-

Yes, it’s another form of share repurchase by Fairfax, when its shares are cheap. In addition to the shares it repurchases with the intention of retiring them, it also purchases the shares it will need to hand over to employees in a few years.

-

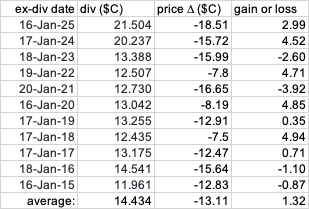

This is one possibility. The other possibility is that it is just almost random fluctuation of the share price. The day to day average move in the last year is a surprisingly high 1.0% (I calculated the FFH $C price), and the dividend is about 1% too. So while you would normally expected a 1% drop in the share price on the day after the dividend, a 0% change or a 2% drop would both be completely unsurprising, just because the stock tends to move around so much. I also looked at the share price change from the close, the day before going ex-div compared to the day of going ex-div. The share price change was roughly as you would expect, with a share price drop about the same as the amount of the dividend. You would have made a bit more in 2024 or 2025, but if you take the average of the last 10 years, you would have made an average of $1.32 every year by buying the day before going ex-dividend, or less if you paid taxes.

-

I believe FFH owns 40% of FIH shares, why not repurchase most of the other 60% (but not ours, of course) and then, as the squeeze comes, bidding for the final non-FFH shares (ours), the price would rise up close to fair value. At that point, they could start issuing small numbers of shares to reestablish a public share base, having generated a ton of value for remaining holders and having provided an opportunity for us to sell a few shares if we needed the liquidity, no?

-

I think you could call this either way. On the one hand, these insurance companies are occasionally sold for a humongous profit (First Capital, Petco) even when they were consolidated, so unlike Berkshire, everything is probably for sale at the right price, and this is an additional 'grove' of earniings that Fairfax occasionally taps into. Digit is a special case because they are co-investors with Kamesh Goyal, with FFH owning 49%, and while they would probably love to own more, that's probably not going to happen. In the 2024 AR, they list it as a 'Consolidated Insurers and Reinsurers' on p.14 (and not as an Asian insurer and reinsurer in the same table). I guess the fact that they did an IPO in 2024 makes it look a bit more like an equity investment, but I doubt they would give it up easily. Ki is not in the table, because it was part of Brit, but since Ki has been separated out from Brit, it appears in quarterly statements under 'Global insurers and reinsurers'. I think they own about half with Blackstone owning the other half.

-

Just to make sure I'm understanding you, do you mean that despite the very substantial buybacks, the discount has not closed on ELF?

-

Oh, of course you're right, I see now the Dec 31st 2025 number in both your text and the chart, I just looked too quickly and thought this was today's values. Eurobank has been a fast-moving target!

-

I'm just wondering about the Eurobank stake, 1178m shares at Eu 3.8080 seems a little low, at EUR:USD = 1.1667 I get the rather stunning figure of US$5.233b, about 10% more than the $4.740b in your table. What am I missing?

-

I think you're probably not suggesting this is a real strategy, but in case you are, there's no quick 0.8% free lunch. If you buy FFH or any other stock just before it pays out a dividend, you will have that 0.8% dividend in your investment account, but you also have a stock that is now worth 0.8% less and probably has an ex-dividend share price that is about 0.8% less. Since share prices fluctuate anyways, dividend or not, the correlation with dividend payment and commensurate stock price drop is not 100%, but on average that will be the amount, as it should logically be.

-

First part: there is no need to manage FX risk for most people and companies if you have a long-term perspective. What goes up usually ends up coming down, at least in most major economies. If Fairfax has $2b of Canadian float and invests it all in US treasuries, for instance, there is a risk that the USD might drop 20%, compared to the Canadian dollar, and they would take a $400m loss. There is also a roughly equal risk that the USD:CAD exchange rate goes the other way, and they end up with a gain. Over a large number of economies, these risks will usually balance out. But if they feel it's important to hedge that risk, investing in local treasuries, as you suggest, would be the way to go. Second, most of their float is invested in treasuries and investment-grade corporate debt. Fairfax does have a lot of equity investments, but it has fixed income investments at roughly the amount of their float, and insurance regulators require most insurance premiums to be invested this way. So Fairfax doesn't have to find equity investments in countries where it has insurance operations.

-

No wonder FFH shares are up, their investments are on fire. Eurolife just jumped another 5% and the market cap is now over US$16b, so presuming we still own 1/3 of it, we are now up to a value of over $5.3b, plus whatever cash we have been getting from trimming shares to keep from going over 1/3. ORLA is also up another C$1 a share since the beginning of the year, after more than doubling last year. Stelco and RFP were also homeruns, especially the sale of RFP which was looking like a dog for a long time. Even Under Armour looks like it's up over their acquisition price, since it was consistently between $4 and $5 all Q4 when they bought 36m shares, in addition to the 6m they already had, and the price is now about $5.70. As for JAB, FFH sold the pet insurance business to them in June 2022, and invested $200m in their JCP Fund V, focused on the pet insurance business, along with a $250m 6% note. I haven't seen any results in FFH's 2023 or 2024 reports, which is a bit odd, it seems like a big enough investment to warrant a line.

-

My longer post got eaten up again (why does this keep happening?) but thanks, I like that approach. My only quibble is that I think the optimistic estimates (tax rate of 20%, 15x multiple of operating earnings, 0% payout ratio of equity investments) is a lot closer to being fair than the pessimistic ones (tax rate of 25%, 10x multiple of operating earnings, 50% payout ratio.), and so his high end value:price of 1.4 is probably closer than the low end (0.9). Also, it is from Q2, and there is a fair bit of good news since then,but the share price is only up 1%. The other factor missing is any accounting for growth, unless you consider that a 10x or 15x multiple already incorporates any projected growth. The company has a few good prospects from growth, most notably repurchasing Odyssey and Alliance, but also repurchasing their own shares at <10x earnings, reduced interest costs from ratings upgrades, and just the fact that they seem to be pretty good at selling things at higher prices (Resolute, Stelco) and buying other things cheap that work out well more often than not (Under Armour??), or even the odd macro call (mortgage credit default swaps, anyone?)

-

I like this a lot, but I don't completely understand it. Where is he getting, for instance, the two estimates of Non-insurance Value? Is it based on the low and high estimates of Stocks payout ratio? Is he eliminating some of the double counting this way, as non-insurance companies have already contributed to value via their earnings in the second line (Investment Income)?

-

Also, BV may go up enough to trigger more fees, without necessarily budging FIH share price, so there will be more concern about all the profit going to the mother ship. As before, I will be happier paying the fees than not having to pay them, but it is true that that makes us prisoners of this investment until Mr Market starts feeling more positive about the company. A couple more sales of positions with big gains might do it, or maybe it will take the Anchorage IPO to accomplish that.

-

I don’t think this is a good way of analyzing investment performance, divvying up the investments into top 10 present holdings, representing about half of current investments, and ‘the rest’ representing the other half, and averaging the two. The top performers will be a big percentage of current holdings just because they have done well, and the weightings are all wrong because the size of the winners will be much greater, at the end of the period, just because of their recent growth But if you want to paint a rosy picture of how Fairfax is doing, it’s perfect, so I am not too surprised that this is a popular way of doing it in a group of fans of the company. Of which I am one, for sure, with Fairfax representing just shy of 50% of my investments, after 5 years of growth. Come to think of it, my portfolio is a perfect example of how this ‘current top 10’ technique makes things look better than they really are. Fairfax has had an awesome return for the past 5 years (>500% gains), which is WHY it is now 50% of my holdings. But unfortunately, it was not 50% of my holdings 5 years ago, more like 20%. So my total portfolio is up less than 250% despite the 500% return of FFH. The proper way of analyzing my returns in the past 5 years is to look at what i owned 5 years ago, and how much that has increased in 5 years. Looking only at my biggest positions now is more pleasant, because it ignores the investments that have flamed out (we all have a Blackberry or two in our closets), but it makes things look better than they really are.