dartmonkey

-

Posts

642 -

Joined

-

Last visited

-

Days Won

3

Content Type

Profiles

Forums

Events

Everything posted by dartmonkey

-

that’s great, I was really looking forward to those Q3 earnings!

-

Interesting that Watsa owns just over 2 million shares, or just over C$4b. Last October, Watsa didn’t quite make it onto McLean’s list of the 40 richest Canadians, with #40 (Jack Cockwell) at $3.4b, but he’ll probably be in the list this year.

-

This, exactly. If you do any significant amount of trading, or converting between USD and CAD, or paying interest on margin loans or receiving interest on cash balances, I think IB is hard to beat, although I am not familiar with Questrade. The bank brokers like TD or RBC or CIBC will take a serious bite out of your returns if you do any of these things, and IB will take a tiny amount. It's not zero - any company has to pay the bills somehow - but it seems like most brokers will offer you some things for free, like free trades or free cash if you deposit funds, or great customer service (which you won't get from IB) but it comes at a high cost, as they will kill you with hidden fees like poor interest rates, terrible forex exchange rates (at TD you will lose >1% each way) or bad execution prices on trades. IB also gives you way more access to foreign markets than the other brokers, and a bunch of trading tools that you might or might not use. I have a big investment in IBKR (FD) because I think it is the Costco of brokers. They charge a fair price for its customers - not zero, and not opportunistically large either - which is why they have been taking market share for decades and will hopefully continue to do the same for decades more. The only thing not to like is the desktop trading interface, which is great if you're a pro, but which takes a little getting used to. But the phone app is pretty simple to use and it becomes quite intuitive once you're used to it.

-

Great question, obviously the valuation of BIAL is the central element in valuing FIH, so how much is its 64% stake worth? They just bought 10% 2 months ago for $255m, so $2.55b is a good first step in how much the whole thing is worth, if they paid a fair price. 64% of that would be $1.632b for FIH, or $12.05 per FIH share. Obviously, we hope they got a fantastic deal for that 10%, and that it is worth a lot more. For instance, FIH bought a 10% stake the previous year, at the same $2.5b valuation, which is also the price they mentioned in Sept 2021. And in last year's AR they acknowledge that this valuation is conservative: The valuation of Fairfax India’s 64% interest in BIAL increased to $1.6 billion in 2023 from $1.2 billion in 2022, implying an equity value of approximately $2.5 billion for the whole company. Excluding cash flows from the 460 acres in Airport City, BIAL is carried on our books at 9.5 times normalized free cash flow, which we consider to be conservative. Bangalore is one of the fastest growing cities in the world and air passenger traffic in India is expected to have robust growth with increasing business and leisure travel, and the improvement in air connectivity to tier II cities. The valuation is supported by future cash flow estimates driven by the growth in capacity, non-aero revenue and real estate monetization plans described above, but does not reflect apparent market interest. Given the fact that they still wanted to buy that last 10% from Siemens, they have probably been lowballing the price with this $2.5b number. Also, in the same report, they use VERY aggressive discount rates to get this number, and VERY conservative EBITDA growth rates: At December 31,2023 the company estimated the fair value of its investment in BIAL using a discounted cash flow analysis for its three business units based on multi-year free cash flow forecasts with assumed after-tax discount rates ranging from 12.4% to 16.9% and a long term growth rate of 3.5% (December 31, 2022– 12.4% to 16.1%, and 3.5%, respectively). At December 31, 2023 free cash flow forecasts were based on EBITDA estimates derived from financial information for two of BIAL’s business units prepared in the second quarter of 2023 and for one business unit, the fourth quarter of 2022 (December 31, 2022– second quarter of 2022 for two business units and fourth quarter of 2022 for one business unit) by BIAL’s management. What EBITDA multiple is appropriate, for a rough valuation? A $2.5b valuation for BIAL implies a multiple of about 12. European multiples in recent years have been about 16 ( https://airport-world.com/buying-into-airports/ ), but that is in a region with much slower growth than what we are seeing in India. Given recent growth rates, far in excess of the 3.5% that FIH has been using in its accounting, 25-30 may be closer to the real fair value than 12, and 30x would give us a $6b for BIAL, or $28.35 per FIH share. But I would love to hear how you and others go about putting a number on FIH's crown jewel.

-

Yes, that would be a very Buffettonian way of thinking about it, and I think it's the right way. Not sure about the $9.50 as baseline, but since the 50c listing costs would represent a one-time cost of setting up the company I guess that makes sense as a baseline. And if you put BIAL at a price that compares with other airports, I think you get to $25/share pretty easily, which would represent (25/9.5)^(1/10)-1= 10% annual return. To get to 15%, you would need intrinsic value to be over $38 (as 9.5*1.15^10=38.43), which is maybe a bit of a stretch, but by no means impossible. So there's probably still a margin of safety with a $19 share price.

-

Up again today, over $19.38 as I speak. In 1st Sept 2017 it got to $18.94, which was a great start from $10 in 2014, but as far as I can tell, that's the highest it got until yesterday and now again today. The company was founded in 2014 (Modi was elected in the Spring) but only started operations in 2015, when it completed its $1.1b in funding, and buying a variety of stakes in public and private companies, mostly in the next 18 months, so it's been almost exactly 10 years. Going from $10 to $19 with no dividends is about a 7% annual return, which sounds terrible, but it was at 5% a month ago, so in 5 weeks it has gone from terrible to just bad. Of course, gains in book value are better, since it is still trading at less than 90% of book, and book value probably understates the gains in intrinsic value, which I think are probably much higher still. But a little good old share price appreciation is overdue and welcome, especially as they may have the opportunity to plough a lot of cash into IDBI if they win that auction.

-

Ok, maybe I'll jinx it but this is turning into an impressive run for FIH, touching $19 today and closing at $18.75. Up from $10 ten long years ago, under $14 last summer and $16.01 at the end of 2024, so $19 is giving us half the return in one month that we got in the preceding 10 years. And on basically no news. Volume is way up too, about 100 000 shares a day, which is about 5 times the normal volume. Understandably so, as people like me are sorely tempted to take some off the table - but I haven't done so yet. Maybe there are some bureaucrats in India that know something about the IDBI acquistion? Or the BIAL IPO?

-

Yes, it is no coincidence that all the banks you can name in Canada, without googling it, are Canadian. Canadian banks have significant operations in the USA, but American banks do not have significant operations in Canada. The "16 banks with $113b in assets operating in Canada" is a talking point of, guess who?, the Canadian Bankers Association. The same FP article goes on to say that: Because Schedule I banks are true domestic banks and not subsidiaries of a foreign bank, they are the only businesses that are allowed to receive, hold, and enforce security interest as described in the Bank Act. Ok, I don't fully understand the restrictions placed on schedule II banks (incidentally, the Canadian government abandoned this terminology in 2001, but it is still widely used. But clearly, the restrictions have not allowed US banks to pose any competitive threat to Canadian banks, and I think no one seriously believes that the Canadian government would allow any Canadian bank to be taken over by a US bank. And the impressive sounding $113b in assets number is less than a quarter of the size of the smallest of Canada's big 6, the National Bank of Canada. More generally, I think if Canadians look honestly at the situation, the USA has plenty of beefs against Canada's protectionism (which in addition to banking - and maybe to insurance - also applies to telecoms, air transportation, poultry, eggs, dairy products, construction, etc. We want access to US markets, but we are not so happy about the US having access to our markets. The irony is that allowing better US access to Canadian markets would also be very beneficial to competition in Canada and could save Canadian citizens a lot of money. For instance the extra cost of dairy/poultry/egg because of supply management represents 2.3% of poor Canadians' incomes, according to one estimate: https://financialpost.com/opinion/supply-management-is-literally-driving-tens-of-thousands-of-canadians-into-poverty

-

I doubt Trump would pull back without having first obtained some concession from Canada, and since he hasn’t really asked for anything particular, I don’t see how he would have gained anything by pulling back now. But I agree that there is probably a large element of negotiation here, so maybe after some major disruption on both sides of the border, he could convene a peace conference, and obtain some major concessions, many of which would actually be good for Canada anyways. My list would be: -ending the already very high tariffs Canada puts on many US imports -ending supply management on eggs, poultry, dairy -opening our markets to investments and acquisitions in air transportation, banking, telecoms, media, etc -spending our fair share on defence -tightening our immigration and refugee policies Canada would have said no to all of these 6 months ago, and would probably say ok to all if the choice is between that and 25% tariffs. There’s nothing like staring disaster in the face for actually realizing we could compromise on less important things, most of which would actually help our economy anyways.

-

those are not the only two possibilities. there’s also “business is doing fine, share price will do what share prices do” here are the Q3 results published a week ago. they look fine to me, i wouldn’t worry… https://www.godigit.com/content/dam/godigit/general/investor-relations/financial-information/financial-results-q3-fy-2024-25.pdf

-

Wow, that is really invaluable information. Thanks a lot for making the trip and summarizing your impressions. If you have any details about the positions you would care to contribute, I’m sure I speak for everyone here in saying that it would be much appreciated. I would also be curious to know more details about the trip: do they do one every year? how long did you go for? how much did it cost? does Fairfax look after accommodations, meals, etc? did you do a lot of travelling within India? Ive never been to India, but it sounds like it might be a great way of, as they say in Quebec, joindre l’utile à l’agréable.

-

So IDBI has a current market cap of 82632 crore, which translates to $9.6b USD, and the government (Union government, i.e. Federal government) plus the Life Insurance Corporation of India (LIC, which, from what I can tell, is the government-owned company that resulted from the nationalizion of all insurance companies in India in 1973) are selling 60.72% of their 95% stake. This is actually 30.48% from the government and 30.24% from promoter LIC, so it seems it is not 60.72% of their stake (as the Business Standard article incorrectly stated it) but rather 60.72% of the company, not that it makes a huge difference, since only 5% is currently held by private investors. So the acquirer, who would obtain control of the company, would presumably have to shell out something like .6072*9.6b = $5.8b, or perhaps more, if there is a control premium they have to pay over the current market price. What are their chances? Business Standard says that there are 4 bidders: Fairfax Financial, Emirates NBD, Oaktree Capital, and Kotak Mahindra Bank, who have until the end of February to submit their final bid. But this article from October 2024 says that there are 3 (Fairfax, Emirates and Kotak Mahindra), with the latter maybe not so keen on the idea: https://www.cnbctv18.com/business/exclusive-kotak-mahindra-bank-ceo-ashok-vaswani-nothing-seems-to-be-cooking-on-idbi-bank-currently-19485224.htm If it is true that "the entire transaction poised to be completed by the first half of the next financial year (FY26)", as the Business Standard says, then we should know well before the end of June. And if Fairfax does win, it is obviously a very big deal for a company of Fairfax India's size, with its market cap of $2.4b (and considerably less than that, as little as a month ago), and book value of $2.9b (as of Sept 30). We don't know how Fairfax intends to structure the deal, but it would likely be transformative for Fairfax India, if they win the contest. They may have to sell other assets, likely higher than book value, and instead of being an airport and a few other little things, they would likely be primarily a big bank, plus an airport, and a few other tiny things. Given the uncertainty, it's not wonder the stock has been so volatile lately.

-

I dunno, count me as disappointed - I don't see why they would expose themselves to being a forced seller below market prices. Sure, a 5-10c discount on 80m shares is just EU4-8m, but that shouldn't happen. I wonder why they couldn't get a friendly partner like OMERS to 'buy' them with a deal to buy them back at some point, but maybe it's not enough money to be worth the bother. It seems like such a good deal, I have bought a few shares recently, so it kind of grates to see them selling them below market price.

-

If Fairfax had 32.89% on 2024-12-31, how did they get over 33.3%, requiring a 2.2% reduction? Eurobank repurchased shares in 2023, but not in 2024, as far as I can tell, and I don't see any repurchase announcement for 2025.

-

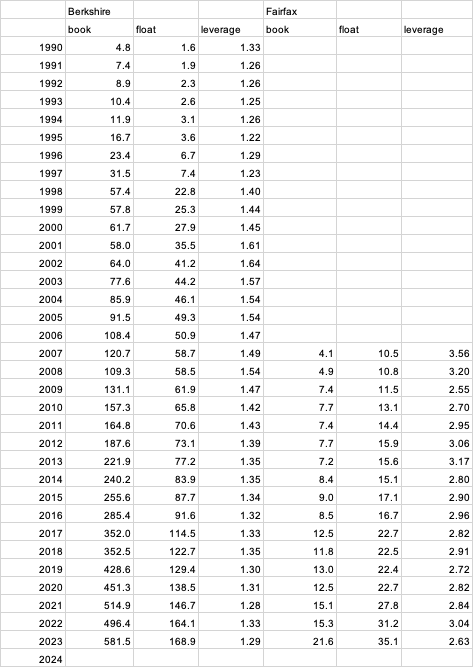

I compiled the equity and float for the 2 companies going back 34 years for Berkshire and 16 years for Fairfax. Berkshire had $4.8b in equity in 1990, and Fairfax had $4.9b in 2008, suggestiing an 18-year lag. Looking at float, in 1990 Berkshire only had $1.6b in float, or leverage of 1.3x, whereas in 2008, Fairrax already had 10.8b in float, or leverage of 3.6x. Over the years, Berkshire has maintained roughly the same float leverage, always between 1.3 and 1.6x, whereas Fairfax's leverage has actually come down a bit over the years, going from 3.6x to 2.6x now. I guess the really big difference is that Fairfax has always been primarily an insurance company. Whereas Berkshire started as a conglomerate of all sorts of different things, including a bit of insurance (GEICO), but mostly other things. It was really only in 1998, with the Gen Re acquisition, that Berkshire became more of an insurance conglomeratte. Whereas Fairfax has always been an insurance company, and is only slowly moving towards being a conglomerate with other investments, and not so spectacularly successful so far. Here are my numbers:

-

Yeah, I think it is really helpful, this comparison, to see where Fairfax might be along the Berkshire trajectory. For a few years, I have found it striking to se how much more float there is in Fairfax than there is in Berkshire, and I think you are right that this is because Berkshire has gone in for buying big, low return industrial assets like Precision Castparts but also the BNSF railroad and the energy utilities. Eventually, Fairfax will also have to go that way, as there is only so much insurance you can buy without running afoul of regulators, but for the moment, we are probably still 20 years behind Berkshire. I'll try to produce a table comparing both companies' book value and float year by year, but if someone else has this data handy, or has a compelling way of comparing them, have at it.

-

Today, investors in Fairfax are getting a trifecta of benefits. 1.) As per your numbers above, total earnings from investments are growing at around 7.5% per year. Yes, float/leverage magnify the benefits of this rate of return for Fairfax. But two more important things have been happening in recent years. They need to be added to your total figures above: 2.) Takeout of minority partners in insurance. - This has the effect of increasing the amount of your numbers that accrue to common shareholders. - Others on this board have stated that taking out minority shareholders in insurance is like doing a share buyback. In the calculation at the top, you get $5b in earnings from the $70b of capital invested, about 2/3 of which is in fixed income, and then those earnings increase the capital invested, which becomes $75b. Viking's point #2, taking out minority partners in insurance, means that some of that $5b in earnings actually goes to repurchases of insurance business, which increases the capital invested even more by way of float. As an illustration of this, we can see Fairfax's extraordinary increase in float in the last few years: 2019: 13.0b book, 22.4b float, 39.0b investment portfolio 2020: 12.5b book, 22.7b float, 47.7b inv port 2021: 15.1b book, 27.8b float, 53.0 inv port 2022: 15.3b book, 31.2b float, 55.5b inv port 2023: 21.6b book, 35.1b float, 64.8b inv port Q3 2024: 22.7b book (we'll have year end book, float and investment portfolio values in a few weeks.) The investment portfolio is probably around $70b by now, but a big part of the increase, in the last few years, is all the new float that they have added, both by expanding their insurance businesses in the hard market, and by increasing their share of these businesses by buying back shares from their passive investment partners, thus further increasing their float. In fact, Fairfax has much more float per equity than Berkshire. At the end of 2023, there was 35.1b in float for 21.6b in equity, so for every $1 of their equity invested, they had another $1.62 of float invested, what I would call 2.6x leverage. Compare this with Berkshire's $567.5b in equity and $168.9b in float at year end 2023, i.e. for every $1 of equity invested, they had another $0.30 of float invested, or 1.3x leverage. Watsa has taken the Berkshire model of investing low or negative cost float in fixed income investments, and investing equity in companies (equity in public companies and full ownership of privatized companies), but he has taken the first part of the equation to a much higher level.

-

Another trick is to hold the shares in a brokerage account with transactions that cost $9.99 (TD) instead of $1 in Interactive Brokers. This small fee is enough to influence the behaviour of someone as cheap as me, and has surely improved my returns enormously. Some broker should market this : a lockbox for core investments you know you should never sell…

-

The simple way I understand it is that Fairfax has invested a certain amount of money in Eurobank, say it is $500m for a third of Eurobank, for the sake of the argument. At the outset, that is both the fair value (as demonstrated by the transaction, with Eurobank presumably worth $1.5b) and also the carrying value. Now after a few years Eurobank makes $150m in net income, and pays out $30m in dividends. Since Fairfax owns a third, this means the company essentially made $50m for Fairfax, and paid Fairfax $10m of that in dividends. So Eurobank has retained $120m in earnings, and this is an additional investment that Fairfax has made in Eurobank - its $40m worth of retained earnings were reinvested in the company, so that is added to the carrying value. That may also be the increase in fair value, too, if those reinvested earnings are not producing a lot of return. But in the case of Eurobank, we also have publicly traded shares that are indicating that fair value has gone up more than the $120m in retained earnings. No matter, carrying value rules say that, on Fairfax's book, carrying value is what it paid initially, plus its share of the earnings, minus what Fairfax received in the way of dividends. Eventually, if Eurobank does well enough and pays out lots of dividends, Fairfax's carrying value for its Eurobank could go right down to zero. So there can be a major divergence between carrying value and fair value. Muddy Waters suggested that Fairfax had not written down its carrying value enough, and that its book value was overstated. Most of us feel it is the opposite, that IFRS rules have increased the excess of fair value over carrying value, with Eurobank being a good example of this, and that Fairfax's book is actually understated.

-

I've just been trying to figure out the logic of dropping the carrying value based on receiving dividends, and based also on Eurobank's earnings. From Fairfax's Q3 report, I see that Carrying Value went from $2099.5 at year end 2023 to $2385.2 on Sept 30, 2024, the number in your table, and they also mention that in Q3 Fairfax received dividends worth $127.9m from Eurobank (slightly different from the number in your table.) Also, Fairfax's share of Eurobank's earnings in Q1-Q3 was $343.7m. There are also exchange rate changes in USD:EUR, with the USD up about 1% over the same time period. Can anyone explain in simple terms how Fairfax might have updated the carrying value of their Eurobank stake? We non-accountants thank you in advance.

-

I have lost my records of exactly when I bought things before the year 2020, but I probably bought my first shares in around 2008, when they would have been at about $200 US a share, meaning my returns are not really that great, 13% per annum not counting the dividend, maybe 2-3% more with the dividend, let's say 15% or roughly FFH's target ROE. I've had much higher amounts invested in the last 5-6 years, so if I could actually calculate the total return accurately, it would likely be over 20%. I found this old email I sent to a friend of mine in 2010, who turns out to be a distant cousin of Prem's :

-

Good grief. There are people that have nothing better to do than to compile lists of insurers, ranking them by the number of insurance policies they have written for companies that have or haven't published 'climate goals'. Implicit, I suppose, is that Fairfax SHOULD really be refusing to insure any oil company that hasn't followed the Investors for Paris Compliance organization's standards for recognizing how terrible their industry is and appropriately apologizing for it and planning to eventually phase out fossil fuels. personally would be horrified if Fairfax ever turned down business for such a flimsy reason. If they did, it would be a major red flag.

-

This is odd because he isn’t the president and there are no vacancies anyway.

-

Meaning that Fairfax is not really a Canadian financials exposure, given that most of its operations are abroad? It's hard for me to say whether the resignation is good for Canadian business or bad. Trudeau was certainly poisonous, but the very likely prospect of elections in the Spring or Fall, with an almost certaiin Conservative victory with Trudeau leading the Liberals, is now looking a bit less certain. Carney or someone else might do a good enough job to salvage Liberals' fortunes, or reduce the Tories to a minority. I think a Tory majority victory is still the most likely outcome, but the probabillity may have gone from 95% to 75%.

-

When was Berkshire the same size as Fairfax with its current $31.5b valuation? It's an interesting question, as Berkshire is clearly constrained at its current size, most private and public companies being too small to move the needle. In the end of 1988, before the B-shares were introduced (in 1996), Berkshire had 1.72m shares outstanding, share price $4,700, for a market cap of $8.1b, or $21.5b in today's dollars, quite a bit smaller than Fairfax today. But the share price doubled one year after, and Berkshire closed 1989 with a share price of $8675, and a market cap of $15.0b, or $38.1b in 2024 dollars. So we can say that Fairfax is now at Berkshire's size some time in 1989. We still have some room to run.