Leaderboard

Popular Content

Showing content with the highest reputation on 10/21/2025 in Posts

-

Good question, @Viking…and the answer has to be that it is much better for Fairfax to buy out minority owners of the high quality insurers they already know and trust than to pay higher multiples for partial or total ownership of insurers that might be acquisition targets in external markets, but of whose management and reserving practices they are not as familiar with. Think back to when Buffett owned half of GEICO’s common stock, and had to pay a market price plus a premium to gain full ownership of the company whose reserving practices and operational and investment management were all known and trusted by him. Fairfax is in an even better position than Buffett was given the prices at which they are able to take out their trusted minority partners. And if for some reason Fairfax stock looks to be an even better investment than buying out minority partners, we can trust that Fairfax will find a way to balance their reinvestment opportunities as they did when they sold 10% of Odyssey to enable a Fairfax stock buyback. I think we can all agree that doing that was better for us as remaining shareholders than if they had borrowed funds externally (probably at an even higher cost?) and used it to take out some minority interests instead. Bottom line, I don’t need Fairfax to make the exact reinvestments that I, with my lack of direct knowledge of their opportunity set, think they should make. They have more than earned my trust that they will continue to treat me as a partner and that the reinvestment decisions they make in the future will be those that are likely to benefit us both.2 points

-

Chuck Akre - How to Find a Compounding Machine Chuck Akre is one of the investing greats. He delivered very good returns over the long term for his investors. He also was a very good communicator and teacher. In our post today, we will explore Akre’s wisdom. To see what it can teach us about Fairfax. Over his lifetime, Chuck Akre tried to answer two questions: What makes a great investment? What makes a great investor? ————— Akre’s north star: rate of return “The bottom line of all investing is rate of return.” Chuck Akre Early in his journey, Akre focussed on understanding the power of compounding and how it should be incorporated into an investment framework. For Akre, the answer was rate of return. The goal of an investor was to earn an above average rate of return (high return on equity). For an investor to earn an above average rate of return they need to invest in businesses that earn an above average rate of return. Investors should only fish in the ‘above average rate of return’ pond. What makes a great investment? What is it about the business that allows it to earn an above average rate of return over the long term? Akre found an answer to this question. The investment framework he developed he called the 3 legged stool The 3 legged stool Akre’s investment framework describes the characteristics of a great business. Leg 1.) Exceptional / high quality business. High rate of return business. Generates high returns on invested capital. Leg 2.) High quality management Demonstrable skill (able) at running the business (operations). Long track record. Integrity (honest) - Treats shareholders as partners. Management (results) should be evaluated using per share metrics (to ensure no dilution is happening). Leg 3.) Good reinvestment opportunities This is what allows high return businesses to keep earning high returns into the future. Creates long term value by unleashing the power of compounding. Want to see both a history and a long runway of future opportunity. Of the three legs, the third is the most important. Find a stock that checks all three boxes and your have found a compounding machine. That is investing nirvana. One more important input. Purchase price Don’t overpay. This will allow you to earn higher future returns (this results in better compounding). Summary “Everything should be made as simple as possible, but not simpler.” Albert Eintstein Yes, this is a deceptively simple framework. Here is how Chuck Akre summarizes his approach: "The three areas of analysis – business, management, and reinvestment – are the key components of what we call our ‘three-legged stool.’ When we find a business that satisfies all three of our requirements, we refer to it as a ‘compounding machine,’ and we seek to purchase shares at a modest valuation." Chuck Akre ————- Additional comments: How to think about risk When you find a company that checks all the boxes: Exceptional quality Strong management Abundant reinvestment opportunities Purchased at a discount Investing using this framework exposes an investor to below average risk. (Akre did not define risk in terms of price volatility.) When to sell The hardest part of investing is being patient and holding a winning investment for the long term. You will be tempted to sell it. It will probably be a mistake (according to Akre). It is very difficult to find a great investment - it takes years. So when you find one it should be held. Even if it looks overvalued at times. Not surprisingly, Akre had a concentrated portfolio. That had low turnover. How to measure the performance of a management team The change in the share price over time. Per share metrics are the ones that matter. On the importance of making (and learnings from) mistakes “Good judgement comes from experience. And experience comes from bad judgement.” An old saying often repeated by Akre. Markel Akre was a fan of Markel (the historical performance of the company back when it was a compounding machine). It would interesting to get his thoughts on the company today. ————— Trying to solve the investment puzzle - Chuck Akre - Talks at Google https://youtu.be/O38I7QIc_eQ?si=diFIZa5m16SmmwfE ————— How does Fairfax look using Akre’s investment framework? Leg 1.) Exceptional / high quality business? Fairfax has compounded BVPS at 19% for the past 39 years. The model it uses is similar to the one used by Berkshire Hathaway in the 1980’s and 1990’s (when it was more leveraged to P/C insurance). Leg 2.) High quality management The management team at Fairfax is exceptional. They are equally good at: Running the business (P/C insurance and investment management). They have a long track record of excellence in both businesses. When it comes to capital allocation over the past 5 years, their performance has been best-in-class compared to P/C insurance peers. High integrity. Shareholders are viewed as valued partners. The communication is very good. Management is focussed on driving per share value for long term shareholders. Leg 3.) Good reinvestment opportunities Fairfax has developed an amazing range of capabilities across both P/C insurance and investment management businesses. With P/C insurance, the company now has a global platform. This gives it a large opportunity set to continue its growth (organically or by acquisition). With investment management, the company has a diverse set of capabilities. Traditional asset classes: fixed income and equities. Alternative asset classes: private equity, venture capital, commodities, real estate. Global reach, with specialty in India. Built (earned) over decades, Fairfax has an extensive network of external partners. OMERS (funding). Kennedy Wilson (real estate). These relationships help enormously with deal flow. In short, the opportunity set today for Fairfax has never been better in the company’s history. Capital will be allocated to where it is able to earn the best return. This should allow the company to continue to earn above average rates of return in the coming years. In turn, this should create enormous value for long term shareholders. Fairfax checks all three boxes of Akre’s three legged stool - it looks like a compounding machine. But we need to look at one more important input - valuation. How is the stock being valued today? Before making any adjustments, Fairfax’s stock looks cheap. Make adjustments for excess of FV over CV for associated and consolidated holdings and the stock looks even cheaper.

1 point

1 point -

A picture is worth 1,000 words. The best performing insurance company (over the past 5 years) is available at the cheapest valuation (compared to peers). What to do? Panic, of course. I love Mr. Market. (My guess is Fairfax does too.)

1 point

-

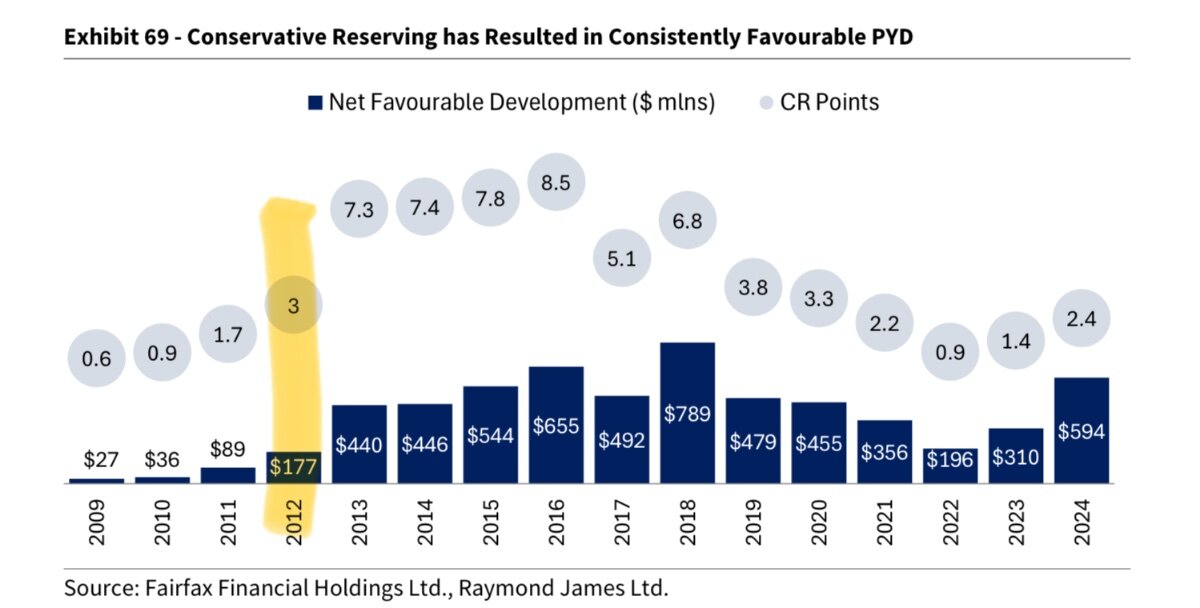

I think this chart shows how reserve releases are cyclical. It makes sense as high reserves are booked in a hard market and if there are no unfavourable developments have to be released in line with average claim duration (4 years). Premiums were growing fast 4 years ago and with slower premium growth since 2024, the reserve releases should have growing impact.

1 point

-

My original question to chatGPT was meant to show me that it didn't matter at all to Berkshire's early share price performance whether US P&C pricing was "soft" or "hard" but ChatGPT didn't do it right and perplexity didn't really get the hard and soft markets right either so it doesn't seem like a valuable exercise. But I'll keep buying Fairfax again today even though the hard market is over and it's time to PANIC! See you at $1570 USD / share!1 point

-

The NBD news certainly increases Fairfax India's chances of "winning." I can imagine a deal structure that is creative and works but who knows how it works out. I assume if Fairfax India wins IDBI they will move quickly to merge CSB into IDBI with IDBI the surviving "brand." You can bet Fairfax parent and the usual suspects of fair and friendly preferred partners will have to help out1 point