Leaderboard

Popular Content

Showing content with the highest reputation on 06/03/2025 in all areas

-

@Maverick47 , your comment really hits the nail on the head. My goal with the poll was to highlight just how many significant exceptional capital allocation decisions the management team at Fairfax has made over the past 10 years. To your point, many were synergistic with others. It is telling that my list was missing a couple of big items - this was pointed out by other posters. Thanks to everyone on the board for voting and especially for taking the time to comment. There is lots of wisdom in the comments. But here is where things get a little crazy… Fairfax accomplished all of this when they were capital constrained. What can this company deliver/accomplish when they are all cashed up? With record operating earnings locked and loaded for the next 4 years? Their insurance business has never been better positioned. Their investment management business has never been better positioned. The quality of their portfolio of equity holdings has never been better (in terms of management, cash flow, prospects). Their capabilities as capital allocators (and as a company) appear ideally suited for the current economic environment (lots of volatility). As fun (and profitable) as the past 4.5 years have been, I can’t wait to see what they do the next 5 years. ‘Time is the friend of the wonderful company.’ ----------- Below is a summary of the results with 73 people having voted.

1 point

1 point -

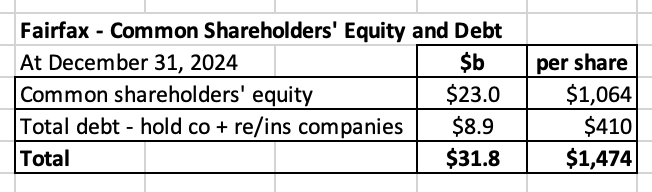

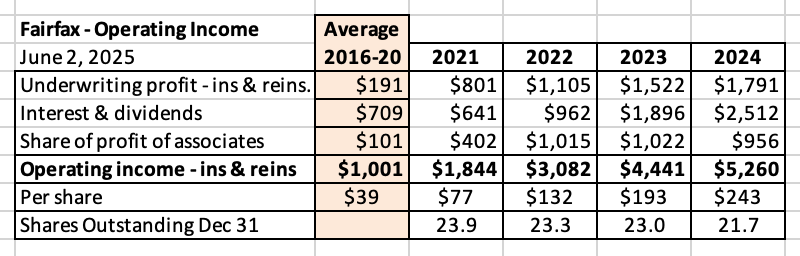

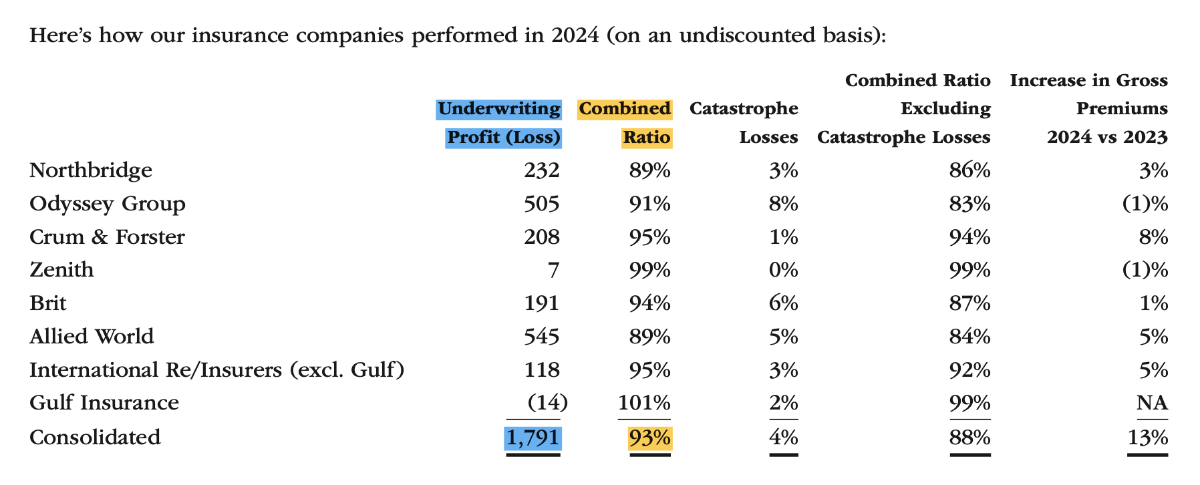

Leverage and Fairfax - A deep dive - Part 1 Introduction “Give me a lever long enough and a fulcrum on which to place it, and I shall move the world.” Greek philosopher Archimedes The fulcrum needs to be rock solid and well placed. The longer the lever the more power it can exert. Used properly, leverage allows one person (or a company in our example today) to figuratively move the world. ————— Leverage In our post today we are going to explore the concept of leverage. And what it means for Fairfax. To see what we can learn about the company today - and what it might mean for the company looking into the future. Getting back to our picture above… The fulcrum is Fairfax’s business model. (Company structure. P/C insurance business. Investment management business. People. Culture.) The lever is a sum of the various forms of leverage that Fairfax uses. Let’s get started. ————— Definition of leverage We are going to define leverage in a very broad way: Using other people and/or their money to boost returns and/or improve the quality of the company. The expectation is the return achieved will be greater than the cost involved. This definition allows us to include both financial and non-financial aspects of leverage (financial capital AND human capital). When investors think of leverage they tend to focus on/think only about the financial piece, and debt specifically. That is true (debt is one kind of leverage). But that is also a very narrow way to think about leverage. Especially when it comes to a company like Fairfax. There are many different kinds of financial leverage. Like float. There are also many different kinds of non-financial leverage. Like having access to a large network of exceptional capital allocators/entrepreneurs - outside of Fairfax (think deal flow). In this post we are going to review the many different ways that Fairfax uses leverage. We are going to stretch the definition - so much so that you might even disagree with us. I hope that happens - and you share your thinking. After all, engaging in constructive debate is how we all learn and get better as investors. If we want to make people uncomfortable, a good way to do it is to challenge conventional wisdom. —————- Buffett and leverage “If you’re smart you don’t need leverage; if you’re dumb, it will ruin you.” Warren Buffett “My partner Charlie says there is only three ways a smart person can go broke: liquor, ladies, and leverage. Now the truth is, the first two he just added because they started with ‘L’ – It’s leverage.” Warren Buffett Before we go any further we need to deal with the elephant in the room - yes, that guy named Warren Buffett. Buffett is the GOAT. Many P/C investors worship at the altar of Buffett. I am (generally) one of them. What does Buffett have to say about leverage? If you do a search online, Buffett probably has more great quotes on leverage than just about any other topic - and he is almost always telling investors that it is the devil and should not be used. Is this true? Does Buffett really dislike leverage? No, of course not. Buffett loves leverage. Buffett has said repeatedly that P/C insurance was the core engine that drove the fantastic returns that Berkshire Hathaway was able to deliver over the past 59 years. What was it about the P/C insurance business that Buffett liked so much? It was the low cost and growing float that it provided. And float is leverage. Context matters The lesson is leverage is not a four letter word - it is not inherently good or bad. Yes, leverage can be bad. But it can also be good. Obviously, which one it is (good or bad) depends on how it is being used. I know it sounds like blasphemy, but as investors there are some things we need to unlearn when it comes to Buffett’s teachings. How to think about leverage is one of them (in the context of our post today). Readers should try and keep an open mind as they keep reading… ————— A (short) review of the different types of leverage that Fairfax uses The goal of this post is to provide readers with an overview of the topic. I am also going to try and keep this post to a reasonable length (having said that, it is still going to be long). As a result, my review of each type of leverage that Fairfax uses is going to be very top line. This post will be broken into the following pieces: Financial Debt - At the holding company & re/insurance operating company level Float - From P/C insurance Equity - Minority partners (2015-2017) Fairfax total return swaps (late 2020/early 2021) Dutch auction (late 2021) - Minority partner Debt - Held by the equity holdings (public and private) Non-financial (human capital) External relationships/partnerships Fairfax has cultivated We are going to tackle the topic in three posts. This is the first and it introduces the topic and goes into the first two items listed above: debt and float. The second post should be out in the next week or so and will review items #3, 4 and 5 on our list above. The final post will review the remaining items and summarize what we have learned on the topic. Let’s get started. —————— Debt - At the holding company & re/insurance operating company level Fairfax borrows money to boost the returns it earns for shareholders. At December 31, 2024, Fairfax had borrowed a total of $8.86 billion - at the holding company and re/insurance company level. This does not include the debt of the non-insurance operating companies (like Recipe or Thomas Cook India) as Fairfax does not guarantee this debt. We will come back to this topic later in the post. What is the cost of the debt? In 2024 total interest paid by Fairfax on this debt was $456.6 million. My very rough guess is Fairfax is paying an average interest rate on its debt of around 5.6%. Importantly, the total amount of interest paid is tax deductible. So the after-tax rate paid by Fairfax is lower. Common shareholders’ equity (CSE) and debt Common shareholders equity at Fairfax totalled $23 billion at December 31, 2024 or $1,064/share. By using debt, Fairfax now has $31.8/billion, or $1,474/share it can use to generate a return for shareholders. What return is Fairfax delivering on its investments? Fairfax is current generating a total return of about 7.5% on its total investment portfolio. This return is well in excess of its cost to borrow (which I estimated earlier at about 5.6% pre-tax). Should an investor in Fairfax be worried about the amount of debt Fairfax is carrying? For help here, we can lean on the ratings agencies. Specifically AM Best (they are focussed on the P/C insurance industry). What does AM Best think? They have upgraded Fairfax’s credit rating twice in the past 2 years. Why? “The outlook revision to positive for Fairfax reflects the improved earnings profile of the consolidated group. Fairfax deployed significant cash into highly rated fixed income instruments as interest rates increased in 2022. This resulted in dividend and interest income run rate more than tripling by year-end 2023. This improved investment cash flow, coupled with continued stabilization of underwriting earnings at various operating subsidiaries, has resulted in improved operating performance metrics relative to peers in recent years, and prospectively.” https://news.ambest.com/PR/PressContent.aspx?refnum=34689&altsrc=9 Over the past 4 years, operating earnings at Fairfax have spiked higher. From an average of $1 billion per year (from 2016 to 2020) to $5.3 billion in 2024. That is a seismic improvement. The quality of the earnings that Fairfax is delivering has never been better. And look poised to grow further from here. As we reviewed, Fairfax’s total interest cost on its borrowings was $456.6 million in 2024. This is a small number compared to the operating earnings that Fairfax is delivering ($5.3 billion in 2024). Debt is an important source of leverage for Fairfax. But it is not its most important source (by far). Float Fairfax has $36.9 billion in float. This is $1,703/share. In the last 4 years, float per share has increased by 84% = CAGR of 16%. Yes, the size of float is massive. And it is growing in size. What is the cost of float? The cost of float is measured by looking at the combined ratio (CR). Fairfax’s insurance companies delivered a CR of 93% in 2024, or an underwriting profit of $1.79 billion. This is also a measure of the quality of Fairfax’s P/C insurance franchise - like other parts of the company, it has been increasing in quality over the past 5 years. This means the cost of Fairfax’s float is zero. Actually, it is much better than that. Fairfax is getting paid to hold its float - it was paid about $1.79 billion in 2024. So Fairfax has $36.9 billion in float. And it is getting paid to hold it. Crazy but true. What can Fairfax do with its float? It can invest it. And keep what it earns. Wow! This explains the power of the P/C insurance model Warren Buffett has said repeatedly that P/C insurance (and the growing, low cost float that it provides) was the engine that propelled Berkshire Hathaway’s unbelievable growth since National Indemnity was purchased in 1967. Common shareholders’ equity (CSE), debt and float Fairfax has a large and growing float. It is getting paid handsomely to hold it. And it gets to keep everything it earns from it. Given its size (and cost), float is by far the most important kind of leverage Fairfax uses. Float is 1.6 x (larger) than the size of shareholders’ equity. Adding all three together (CSE + debt + float), Fairfax has $69 billion, or $3,171 per share, that it is able to invest to earn a return for shareholders. Investment leverage We can measure Fairfax’s investment leverage by dividing the total by CSE. $68.7 billion / $23 billion = 3.0x Fairfax has very high investment leverage. This amplifies the impact of Fairfax’s investment returns on its return on equity. What is the return of the investment portfolio? Fairfax has an investment portfolio of $69 billion Fairfax’s investment portfolio is currently generating a pre-tax return of about 7.5% or about $5.175 billion per year. This is $240 per Fairfax share. Cost of debt was $457 million in 2024. ‘Cost’ of float was a benefit (underwriting profit) of $1.8 billion in 2024. Is Fairfax’s use of leverage boosting the earnings of the company? Yes. Big time. This is a very powerful combination / result. Fairfax’s use of debt and float are examples of structural uses of leverage for Fairfax - a permanent part of the capital structure of the company. Debt and float fall on the liability side of Fairfax’s balance sheet. Next, we will review some examples of leverage that Fairfax employs that are more tactical in nature - temporary, to take advantage of a short term opportunities when they pop up. With our next example, we are going to review how they use the asset side of their balance sheet to get leverage. We will review the remaining ways that Fairfax uses leverage in part 2 of our post. It should be out in about a week.

1 point