Equity Hedges and Shorts: Fairfax’s The Lost Decade (2010 to 2020)

This is the sister article to the one I wrote yesterday. Fairfax's Version of The Big Short. Scroll up to read it.

When Risk Management Became a Macro Bet

“Those who cannot remember the past are condemned to repeat it." (George Santayana)

What was Fairfax’s largest investment mistake?

The equity hedge and short positions it maintained for much of the decade following the financial crisis.

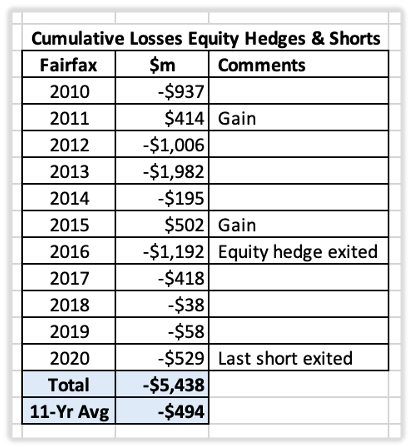

Between 2010 and 2020, Fairfax lost approximately $5.4 billion on its equity hedge and short strategy—roughly $500 million per year. To put that in perspective, Fairfax's shareholders' equity was about $7.7 billion at the beginning of 2010.

The losses were significant. The opportunity cost was even greater.

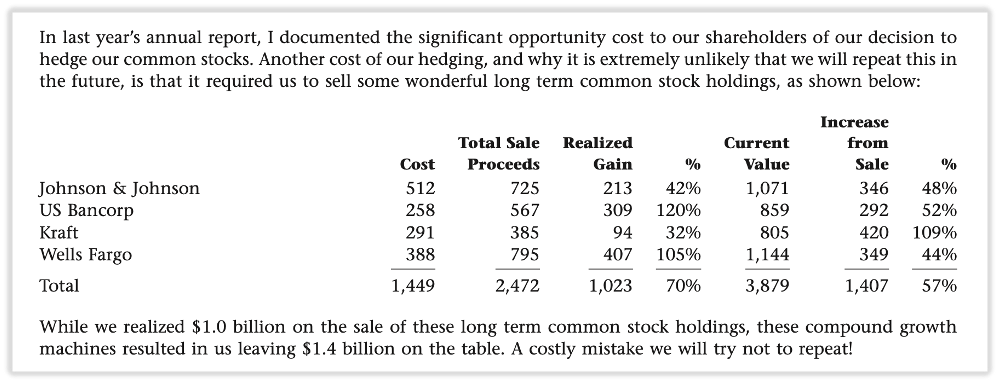

Capital remained tied to a bearish thesis while global equity markets enjoyed one of the strongest bull markets in history. Along the way, Fairfax was forced to sell some successful investments, limiting the benefits of long-term compounding. In Peter Lynch's language, some of the flowers were cut while many of the weeds remained.

For shareholders, the result was a lost decade.

Prem’s comment from Fairfax’s 2017AR

Why Fairfax Put on the Trade

To understand the mistake, it is important to understand why it was made.

The roots of the strategy can be traced directly to Fairfax's greatest investment success: its credit default swap (CDS) position during the financial crisis. Between 2005 and 2009, Fairfax generated more than $2 billion in profits by correctly anticipating severe problems in the global financial system.

That experience shaped management's outlook.

Following the crisis, Fairfax became increasingly concerned that developed economies faced a future of excessive debt, weak growth, and deflation. In Fairfax's 2010 Annual Report, Prem Watsa wrote:

"We worry that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990."

If that scenario unfolded, equity markets could struggle for many years. To protect shareholders, Fairfax steadily increased its equity hedges until much of its common stock portfolio was effectively insulated from a major market decline.

Viewed from 2010, the concerns were understandable.

The financial crisis was still fresh. Government debt levels were rising. Economic growth remained sluggish. Central banks were experimenting with unprecedented monetary policies. Many thoughtful investors shared similar concerns.

The problem was not identifying risk.

The problem was what happened next.

“2010 was a disappointing year for HWIC’s investment results because of the two factors mentioned earlier. Hedging our common stock investment portfolio cost us $936.6 million or $45.61 per share in 2010. Our hedging program masked the excellent common stock returns we earned in 2010, of which a significant amount was realized ($522.1 million). We began 2010 with about 30% of our common stock hedged. In May and June, we decided to increase our hedge to approximately 100%. Our view was twofold: our capital had benefitted greatly from our common stock portfolio and we wanted to protect our gains, and we worried about the unintended consequences of too much debt in the system – worldwide! If the 2008/2009 recession was like any other recession that the U.S. has experienced in the past 50 years, we would not be hedging today. However, we worry, as we have mentioned to you many times in the past, that the North American economy may experience a time period like the U.S. in the 1930s and Japan since 1990, during which nominal GNP remains flat for 10 to 20 years with many bouts of deflation.” Prem Watsa – Fairfax 2010AR

What Happened

The feared outcome never arrived.

Instead, the U.S. economy recovered. Interest rates remained exceptionally low. Central banks injected massive liquidity into financial markets through quantitative easing. Governments ran large fiscal deficits. Corporate profits expanded. Technology companies flourished.

The result was one of the longest and strongest bull markets in modern history.

Fairfax, however, remained largely committed to its bearish positioning.

Over time, what began as a risk-management tool gradually evolved into a large macroeconomic bet.

That distinction matters.

Risk management seeks to protect against adverse outcomes. A macro bet depends on a specific economic forecast being correct. As the years passed, the line between the two became increasingly blurred.

What Went Wrong?

Many of Fairfax's concerns proved reasonable.

Debt levels were high. Economic growth was sluggish. Central-bank policies were unprecedented. The world did face meaningful risks.

The mistake was not recognizing those risks.

The mistake was position size, duration, and flexibility.

The hedges eventually became so large that they dominated Fairfax's investment results. The positions were maintained for more than a decade despite mounting evidence that the original thesis was not playing out. Most importantly, Fairfax underestimated the willingness and ability of governments and central banks to support economic activity and financial asset prices.

The result was a decade of disappointing investment performance.

The direct losses totaled approximately $5.4 billion between 2010 and 2020.

The indirect costs were equally significant:

Missing much of a historic bull market.

Prematurely selling successful investments.

Slower growth in earnings and book value.

Significant damage to Fairfax's reputation.

The loss of many long-term shareholders.

The impact on shareholder returns was dramatic.

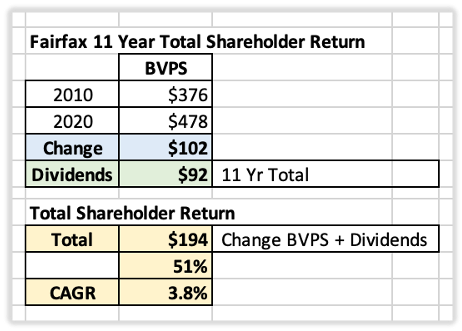

Book value per share increased from $376 in 2010 to $478 in 2020. Including dividends, Fairfax delivered a total return of approximately 51%, or 3.8% annually.

Over the same period, the S&P 500 generated a total return of roughly 332%, or 14.2% annually.

Exiting the Trade

Fairfax exited the strategy in stages.

The broad equity hedge program was removed near the end of 2016 following the U.S. presidential election. In Fairfax's 2016 Annual Report, Watsa explained:

"Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions..."

Several individual short positions remained, however, and continued to lose money.

By 2019, Watsa publicly acknowledged the mistake:

"Shorting is dangerous, very short term in nature and anathema to long term value investing."

After another $529 million loss in 2020, Fairfax finally closed its remaining short exposure.

The decade-long experiment was over.

A Turning Point

The removal of the hedges and shorts eliminated a significant drag on Fairfax's earnings power.

For more than a decade, the strategy had cost shareholders roughly $500 million per year. Once the positions were closed, that headwind disappeared.

The improvement in Fairfax's results after 2020 was driven by many factors, but the elimination of the hedge program was undoubtedly one of them.

Investors evaluating Fairfax after 2020 were looking at a different company—one no longer burdened by a large and persistent negative carry.

Why Did It Persist?

No outsider can know with certainty.

My best explanation is that Fairfax's extraordinary success with credit default swaps reinforced management's confidence in its broader macroeconomic outlook.

Ironically, the same mindset that produced one of the company's greatest investment successes may also have contributed to one of its largest mistakes.

That pattern is common in investing.

Success builds confidence. Sometimes it builds too much confidence.

Lessons for Investors

The equity hedge and short strategy offers several important lessons. In many ways, they are the mirror image of the lessons from Fairfax's highly successful CDS trade.

First, risk management can become dangerous when it evolves into a macroeconomic forecast. What began as a hedge gradually became a large bet on a specific economic outcome.

Second, position size matters. The hedges eventually became so large that they drove Fairfax's investment results.

Third, duration matters. Even a sound thesis can become extraordinarily costly if maintained for too long.

Fourth, investors must adapt when facts change. Fairfax was slow to adjust as markets, economies, and policy responses evolved.

Finally, trust matters.

The strategy did more than cost shareholders billions of dollars. It damaged confidence in management's judgment and led many long-term investors to leave. Financial losses can eventually be recovered. Trust usually takes much longer.

As Buffett has observed, companies tend to get the shareholders they deserve. Fairfax has long said it wants long-term shareholders. If that is the case, management must uphold its side of the relationship. From 2010 to 2020, it failed to do so.

To management's credit, the mistake was eventually acknowledged, the positions were closed, and the company moved forward.

Fairfax's performance since 2020 suggests the lessons were learned.

That may be the most important takeaway.

Every great investor makes mistakes. What separates the best from the rest is their ability to recognize them, learn from them, and avoid repeating them.

------------

Comments from Prem and other notes from Fairfax’s 2016AR.

Prem discusses the reasons for exiting the equity hedges.

He also provides a summary: from 2010 to 2016, total losses from equity hedges were $4.4B. These were offset by net gains on stocks of $2.7B and bonds of $2.2B. Fairfax’s investment portfolio had been performing very well.

"Unfortunately, the presidential election on November 8, 2016 changed the world for us, so we reacted quickly by removing all our index hedges and some of our individual short positions and reducing the duration of our fixed income portfolios to approximately one year – all of which resulted in a $1.2 billion net loss on our investments in 2016 which, in turn, resulted in a loss in 2016 of $512 million or $24.18 per share."

"When we removed our hedges near the end of 2016, we realized a loss of $2.6 billion in 2016, but that included $1.6 billion which had gone through our statements in prior years. As discussed earlier, since 2010 we have had $4.4 billion of cumulative net hedging losses and $0.5 billion of unrealized losses on deflation swaps (which we still hold), offset entirely by net gains on stocks of $2.7 billion and net gains on bonds of $2.2 billion. The volatility of our earnings caused by our hedges and long bond portfolios is over – and as I said earlier, we are focused on once again producing excellent investment returns." Prem Watsa – Fairfax 2016AR

Equity contracts: “Throughout 2015 and most of 2016, the company had economically hedged its equity and equity-related holdings (comprised of common stocks, convertible preferred stocks, convertible bonds, non-insurance investments in associates and equity-related derivatives) against a potential significant decline in equity markets by way of short positions effected through equity and equity index total return swaps (including short positions in certain equity indexes and individual equities) and equity index put options (S&P 500) as set out in the table below. The company’s equity hedges were structured to provide a return that was inverse to changes in the fair values of the indexes and certain individual equities.”

“As a result of fundamental changes in the U.S. that may bolster economic growth and business development in the future, the company discontinued its economic equity hedging strategy during the fourth quarter of 2016. Accordingly, the company closed out $6,350.6 notional amount of short positions effected through equity index total return swaps (comprised of Russell 2000, S&P 500 and S&P/TSX 60 short equity index total return swaps). The short equity index total return swaps closed out in 2016 produced a realized loss of $2,665.4 (of which $1,710.2 had been recorded as unrealized losses in prior years). The company continues to maintain short equity and equity index total return swaps for investment purposes, and no longer considers them to be hedges of the company’s equity and equity-related holdings. During 2016 the company paid net cash of $915.8 (2015 – received net cash of $303.3) in connection with the closures and reset provisions of its short equity and equity index total return swaps (excluding the impact of collateral requirements).” Fairfax 2016AR