All Activity

- Past hour

-

No offense, but I’m guessing you didn’t invest during the financial crisis.

-

What’s that situation here? How much would the stock have to be down before they couldn’t come up with the cash to cover the margin? I might be naive but it seems improbable and my guess is that’s what they think too. They might have taken some off but I would be disappointed if that’s the case.

-

In extreme situations they wouldn’t have the cash to buyback stock when making significant TRS payments. I’m likely influenced by the extremes during the financial crisis when everything became correlated, but I’m also not naive enough to think this won’t happen again.

- Today

-

Negative feedback loop is useful when trying to buy back shares cheap.

-

Exactly. It has the potential to become a negative feedback loop if the share price starts to decline significantly, which is a possibility for reasons beyond their control. I’d like to see them slowly unwind it over the next year or two.

-

Yeah, you can still buy the print editions of these with the long history as you showed here. I buy them every 7-8 years on the promo price as they’re a useful quick reference.

-

Explained a few times already why I don’t think that’s the case but we’ll find out for sure when they report.

-

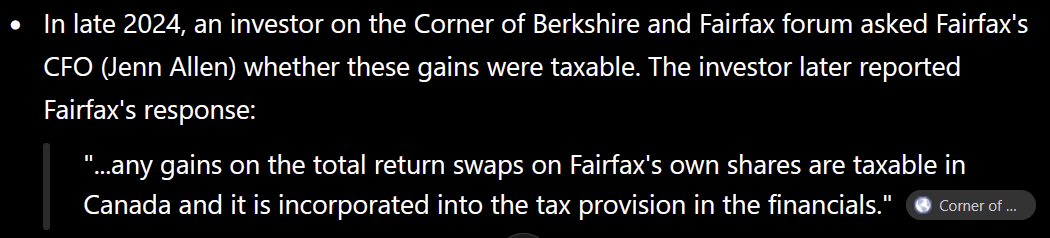

I asked ChatGPT how the Fairfax TRS on its own shares is taxed, and it took the answer from posts by @gfp on CoBF. https://thecobf.com/forum/topic/16427-fairfax-stock-positions/page/87/ If the massive repurchase in June was from the TRS counterparty, I trust there were good reasons. Wasn't the whole reason for the TRS that they were liquidity constrained at the time? If liquidity is not a problem now, closing it out partly at a low price is tax efficient. Or maybe it just was the counterparty asking them to reduce it.

-

I am preparing a pre-view of Q2 earnings for Fairfax. Part of the process is listening to the prior quarters conference call. The comment below from Wade Burton, President and Chief Investment Officer, from the Q1 2026 call caught my attention (again). It is stuffed full of important and useful information (this is becoming typical for Wade's comments on the calls). Public versus private (advantages of each) Criteria used (profitability, balance sheet, management) Value investing (price paid matters) Update on recent investments (Meadow, Peak and Sleep Country) The advantage of partnering with Fairfax The strong team that has been built over the past 10 to 15 years at Hamblin Watsa (mirroring what Andy Barnard has said happened at the insurance business). How the company is positioned today: "especially important now" Welcome to "new Fairfax." ----------- Wade Burton: Fairfax Q1 2026 conference call ... I thought it would be a good quarter to give a discussion about how we look at investments in publicly traded common stocks versus investing in private companies. The underlying process is the same. We work to uncover true economic profits and or profit capacity. We think about where those profits are going. We focus on balance sheet and balance sheet flexibility. We think about the price we pay for those profits. The same underlying process for both public and for private. In both cases, we know management is a key factor. As Buffett pointed out, a great manager can’t save a leaky boat, but what we have learned is that they make a huge difference paddling boats that do float. The advantages of buying public common stocks is: the ability to capitalize on the moods of the stock market and liquidity. The ability to enter and exit an investment quickly is a good thing. The advantages of making direct investments in private companies is we control the profits. That is, we can choose to reinvest the profits in the businesses we’ve invested in, or we can take the profits out and invest them elsewhere. In general, the flexibility to invest in either public or private companies is a huge advantage for us. It allows us to be opportunistic, agnostic, and truly seek the best possible investments. For example, today, with the Shiller PE at all-time highs, you would not expect we’d find a lot of fifty cent dollars in the stock market, and we aren’t. We have been able to make outstanding acquisitions on the private side, including Meadow Foods, Peak Achievement, and Sleep Country. We have the advantage of a history of being terrific long-term partners. 40 years of fair and friendly transactions with a long line of very happy partners, along with permanent no call capital, makes us an attractive home for many companies. To do all of this well takes a skilled and focused investment team, and I’m so proud of the team we’ve built over the last 10 or 15 years. Our people are decision-makers. They are analysts and value investors. We have skilled defensive players and skilled offensive players. All have experience in public and private investments. You know, having the independence to make decisions is so important, and they’re all doing it. We call them in where we need them on the bigger investments. With that, it is amazing to watch them come together as a group. Having this team in place is especially important now, given how big and globally spread out we are and how big we hope and plan to be in the next 50 years.

- Yesterday

-

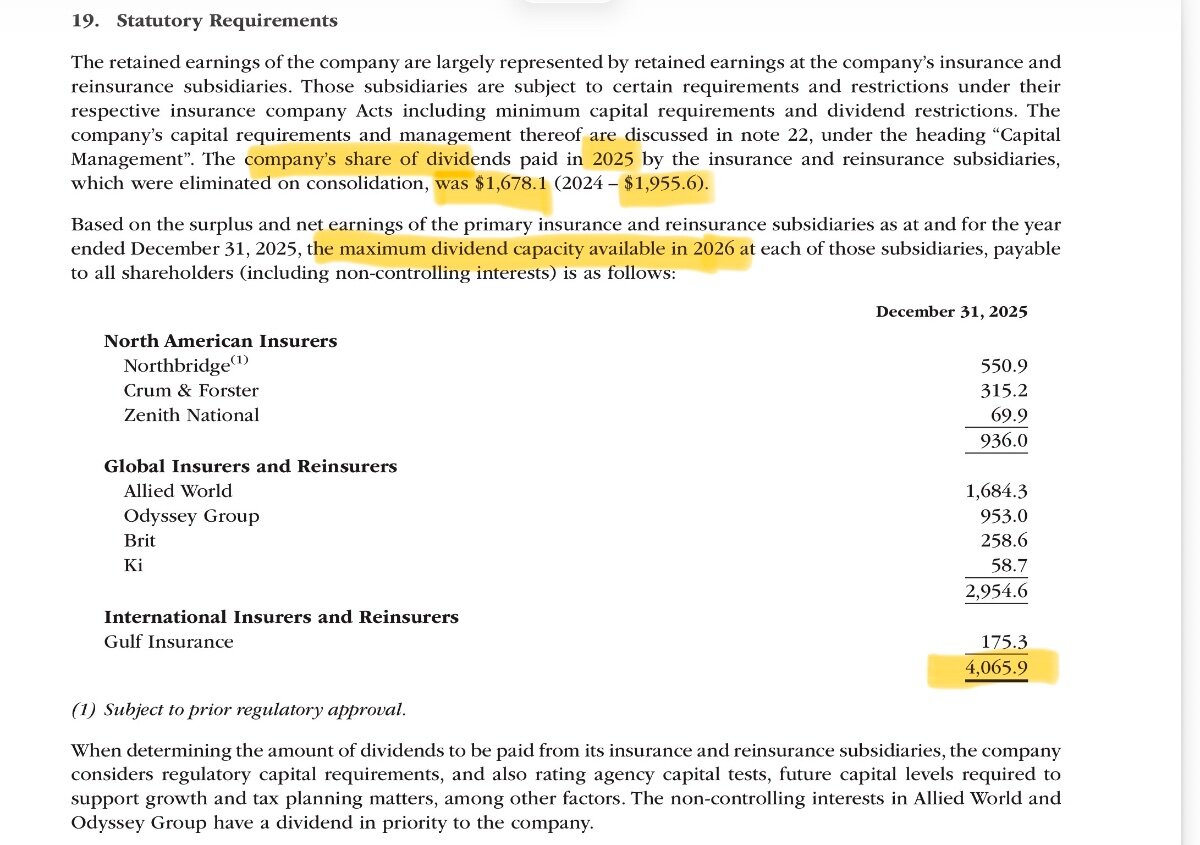

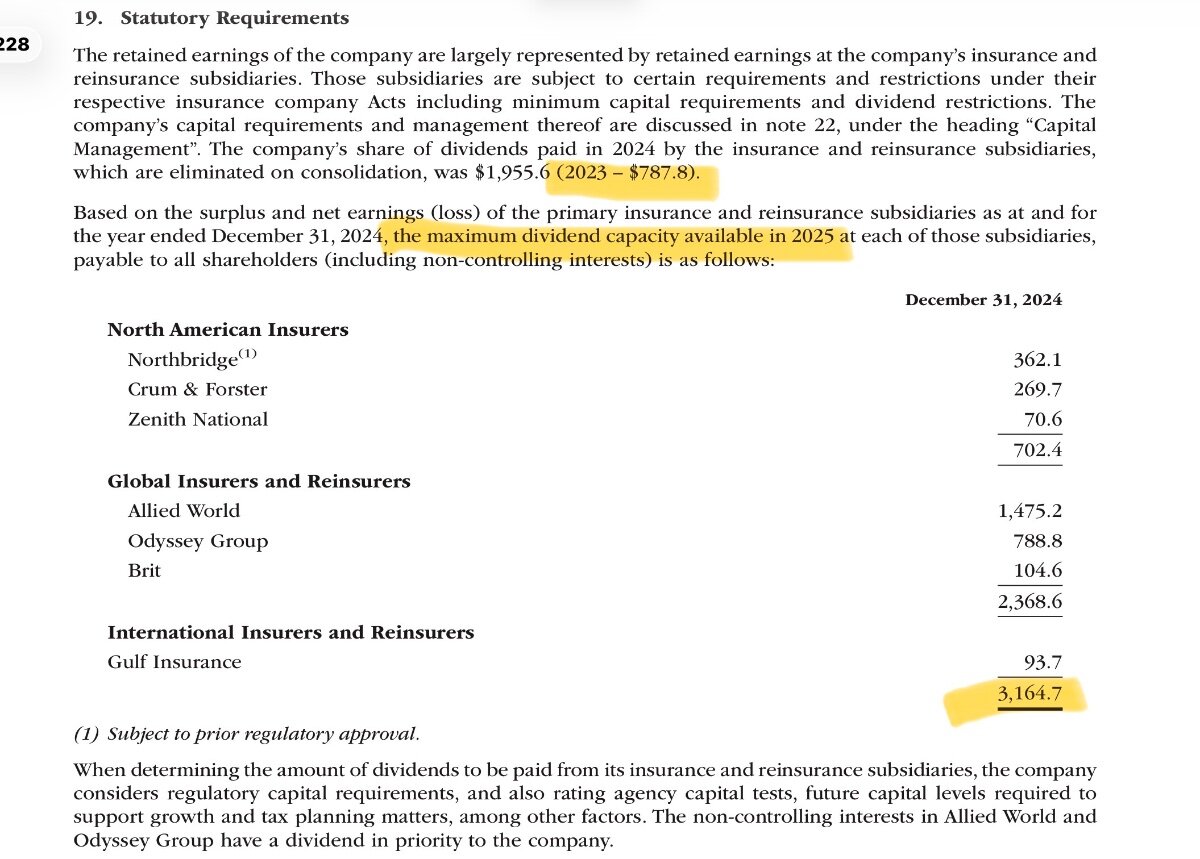

The $2.5b includes Q425. I don’t think it’s helpful to look to try to match the source of earnings. This is another attempt from me to consider the holdco operations differently from the insurance subsidiary operations. In this case, the holdco did own $400m of Poseidon at the holdco at the sale price so I suspect that is capital available for buybacks. The rest of it would come from new debt like the recent $750m 30-year issue and mostly dividends from the insurance subsidiaries which have a lot of cash on hand to pay dividends.

-

Agreed. I like the idea of a stable company like Berkshire buying highly cyclical businesses that generate significant free cash flow at the top of the cycle, and over earn on average across the cycle. They’re almost uniquely positioned to own businesses like these given the stability of the energy assets, the strength of the balance sheet and the constant need to put float to work.

-

It doesn’t matter he will be pardoned.

-

Of the 2.5 billion or so in buybacks, how much of it can we estimate came from FCF? Is most of it from the Poseidon sale?

-

Much to your chagrin, you just earned a MAGA cap...ha!

-

Yeh some dudes have lost their mind, but need to remember that Trump is a vaccine for woke. It wasn’t too long ago that men were women, you were a bigot for not agreeing so, kids should be injected with hormones, white privilege means you can’t have an opinion, can’t talk about immigration without being a racist, discrimination in college admissions…. Pretty long list. And I’d say that many of the aforementioned ills haven’t really gone away either, Trump is great in some ways but terrible in others too.

-

Smart man turns into moron...MAGA to blame! They need to create a MAGA vaccine, but I doubt this administration will since they don't believe in them unless there is a world-wide pandemic. Another of the mighty who have fallen after associating themselves with Trump and his beliefs! Literally went from brave soul conspiracy nut to right wing loser conspiracy nut...the chart looks nearly identical to Giuliani's fall except replace the underaged hotel room sexcapade with a Russian double-agent girlfriend scandal! Cheers! https://www.yahoo.com/news/politics/articles/judge-awards-hunter-biden-1-153923367.html

-

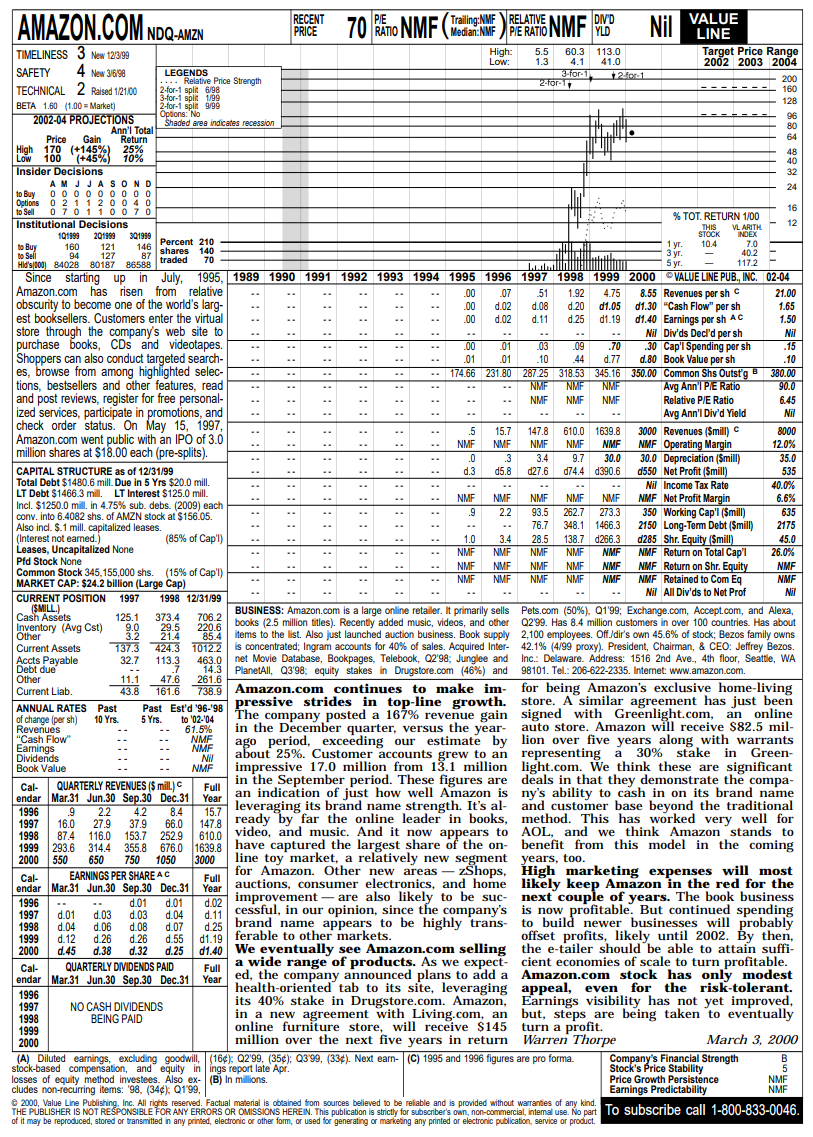

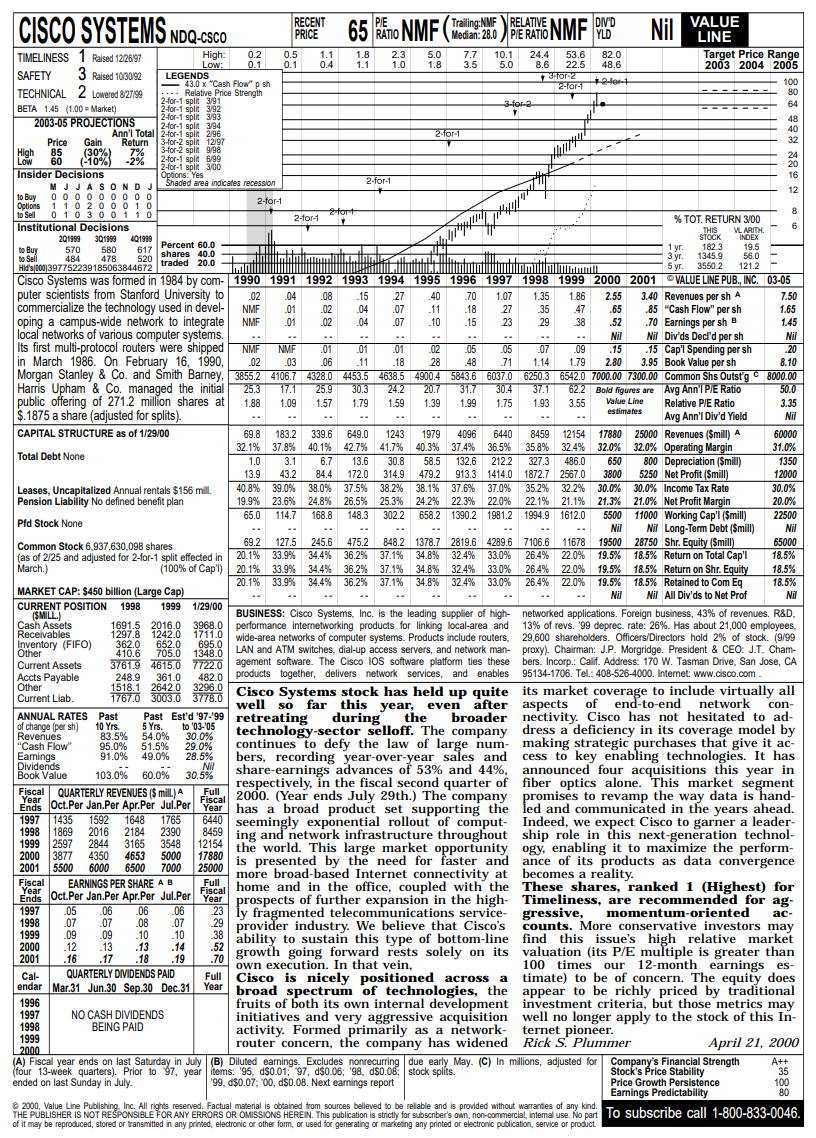

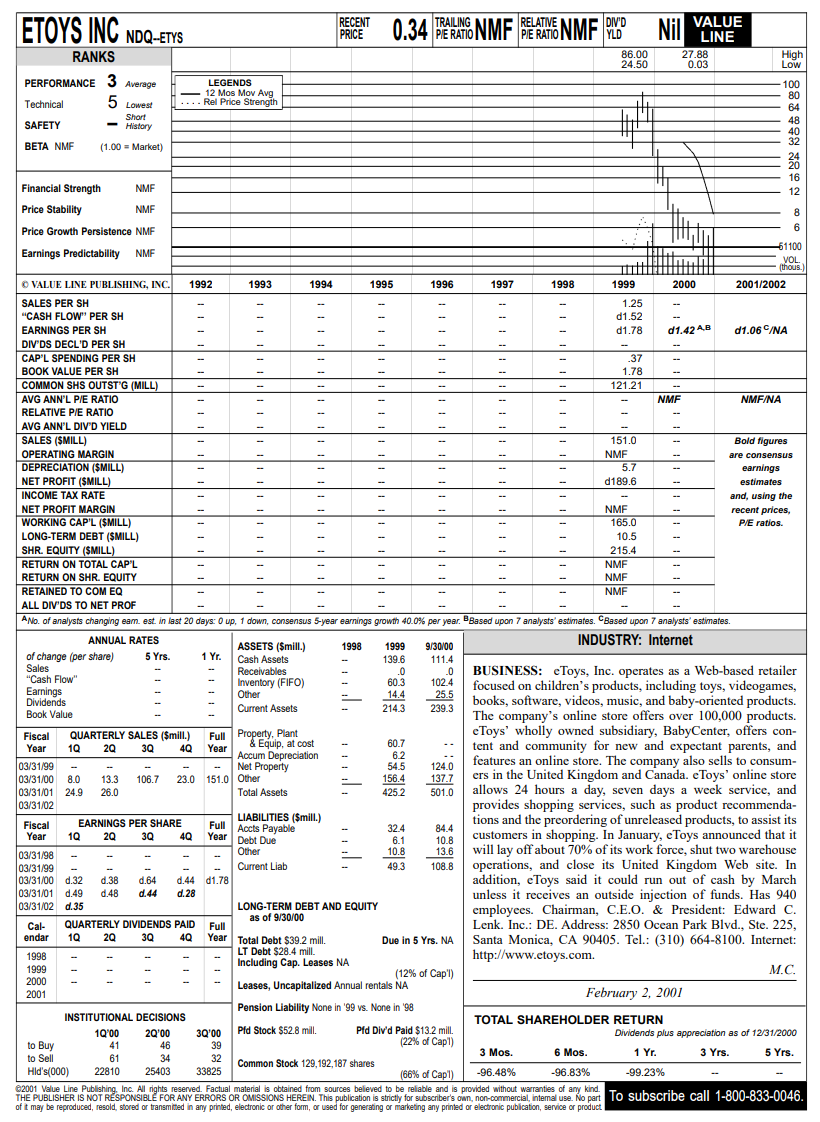

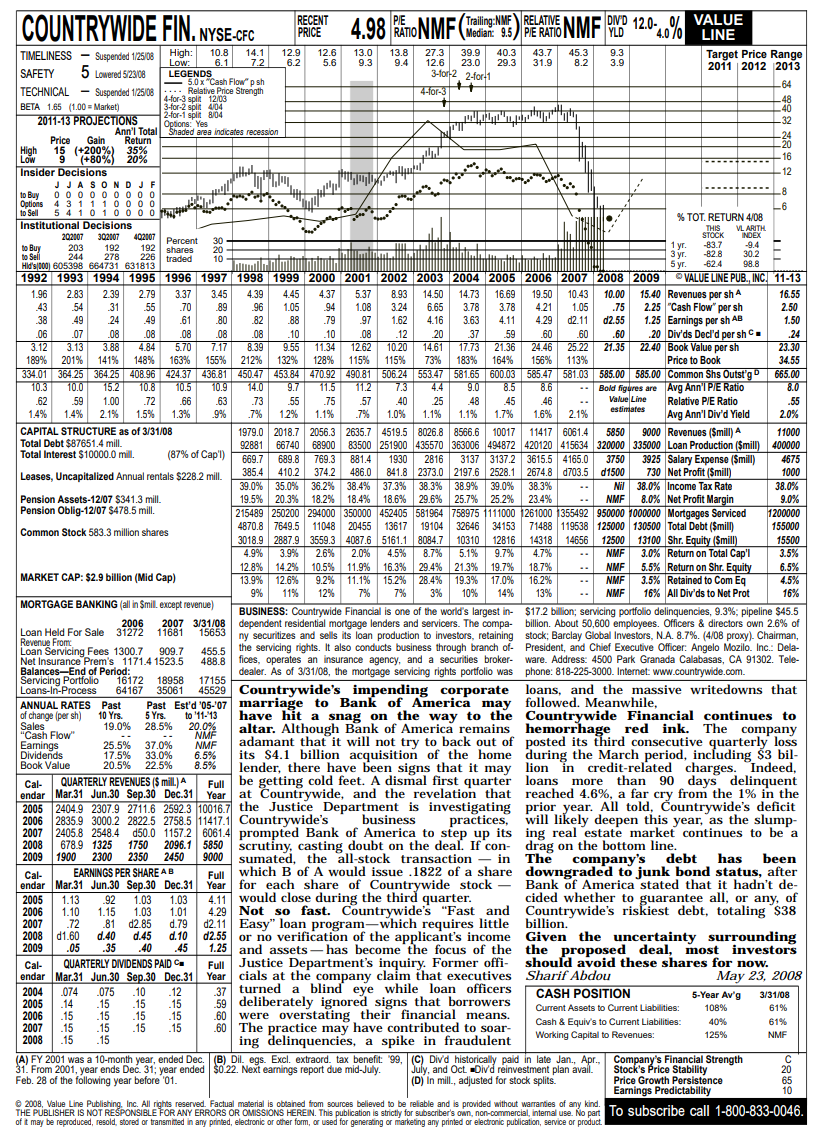

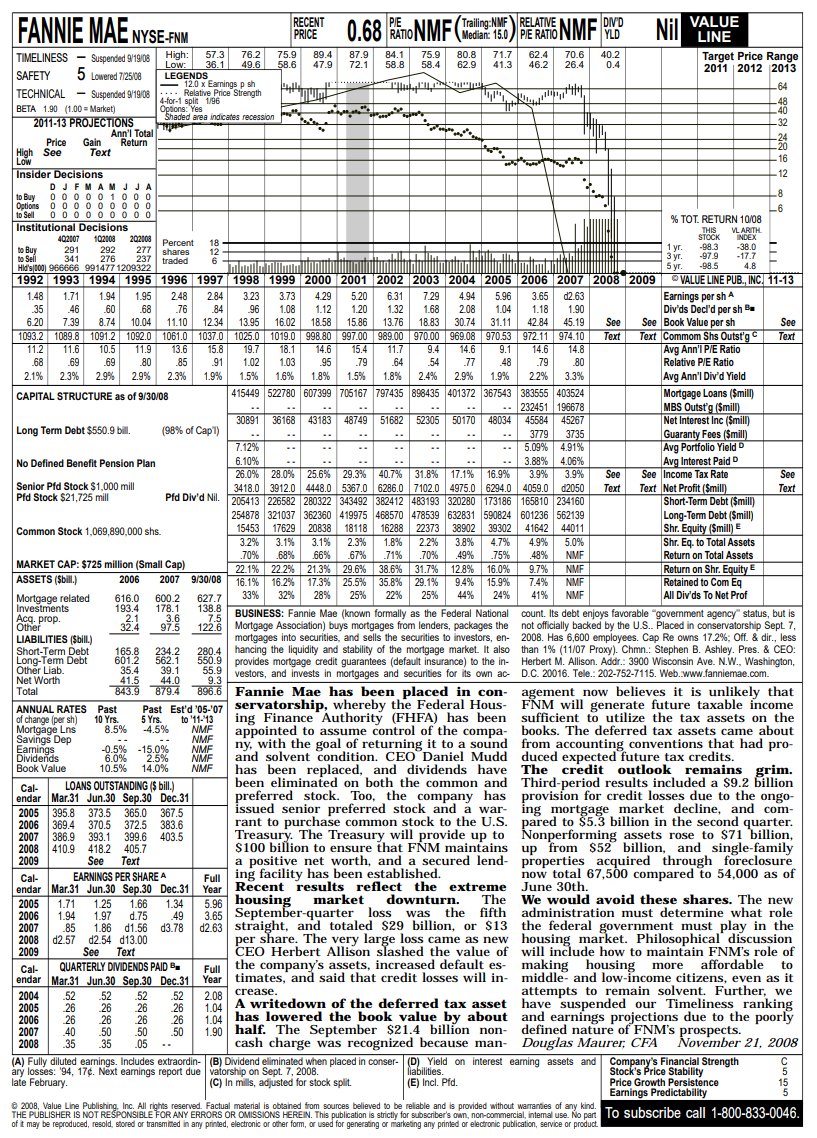

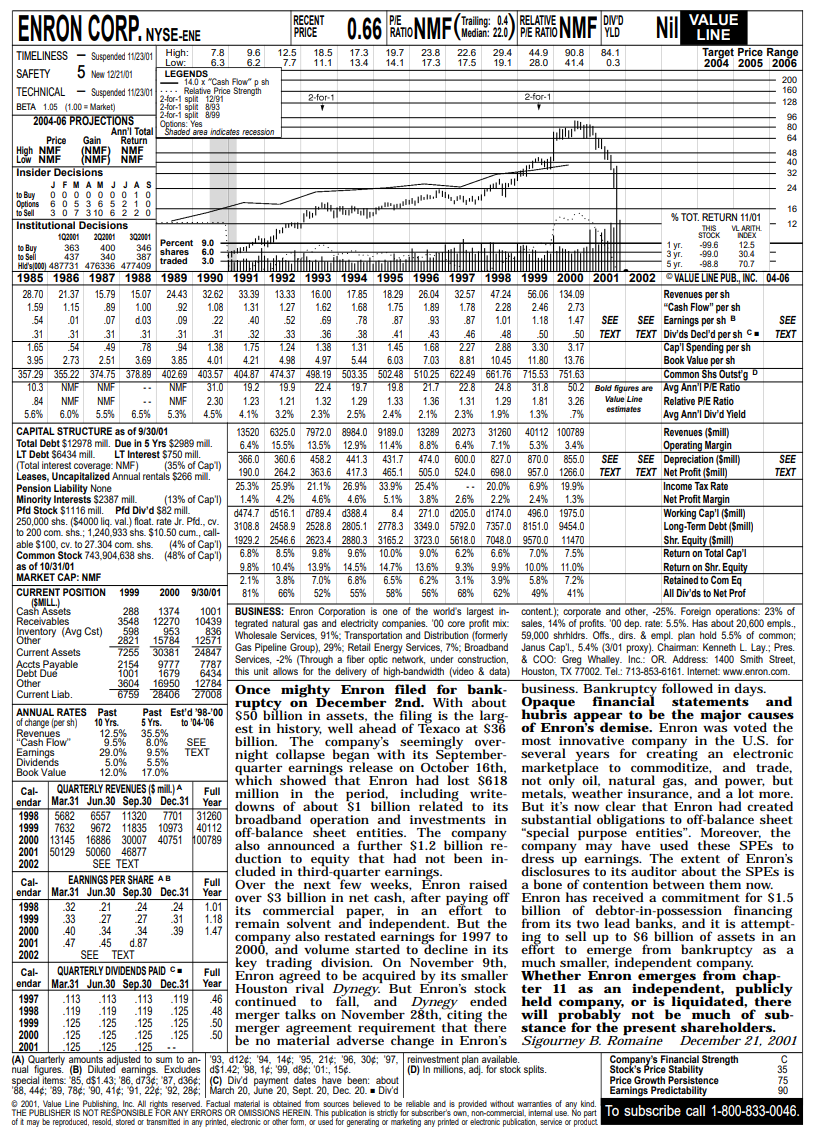

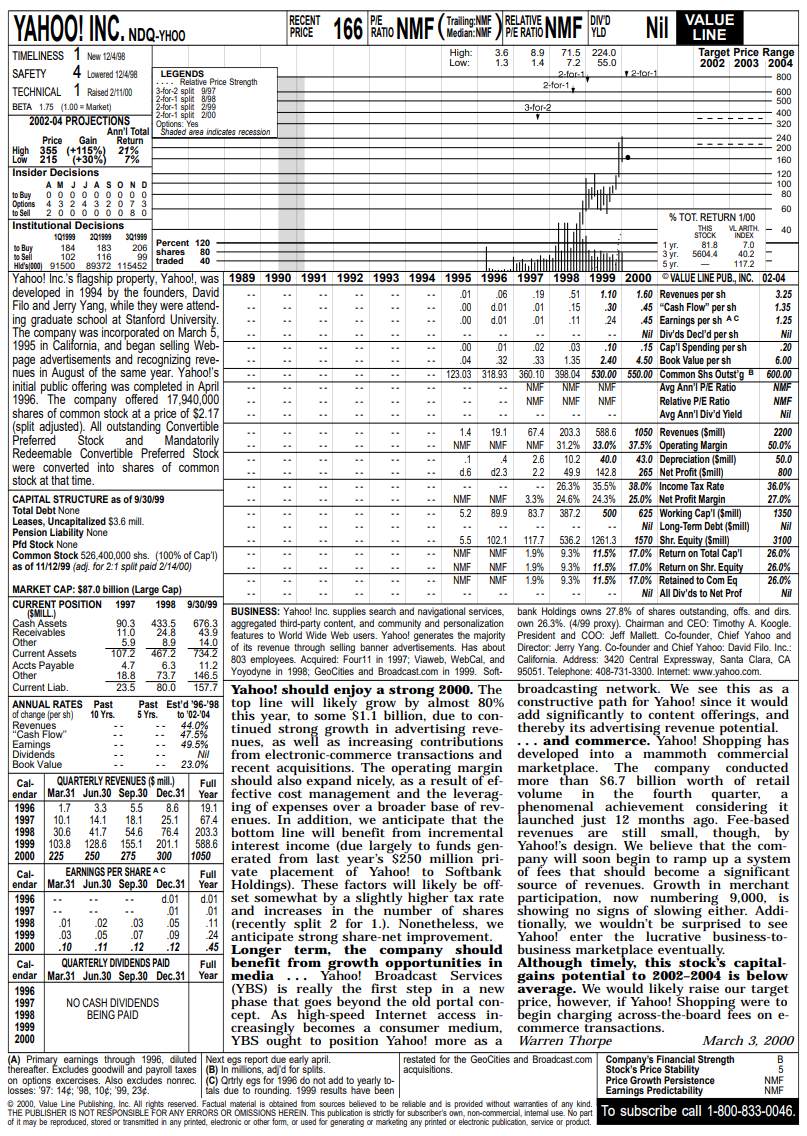

Sorry if the quality is bad. In retrospect, it's kind of amazing just how stupid the Dot Com bubble was.

-

-

-

-

Buffett/Berkshire - general news

ValueMaven replied to fareastwarriors's topic in Berkshire Hathaway

Wow. Really interesting. The last few moves have been awesome...high quality companies in depressed industries: OxyChem, Taylor, and now another homebuilder -

Cato Institute: World Hyperinflations

-

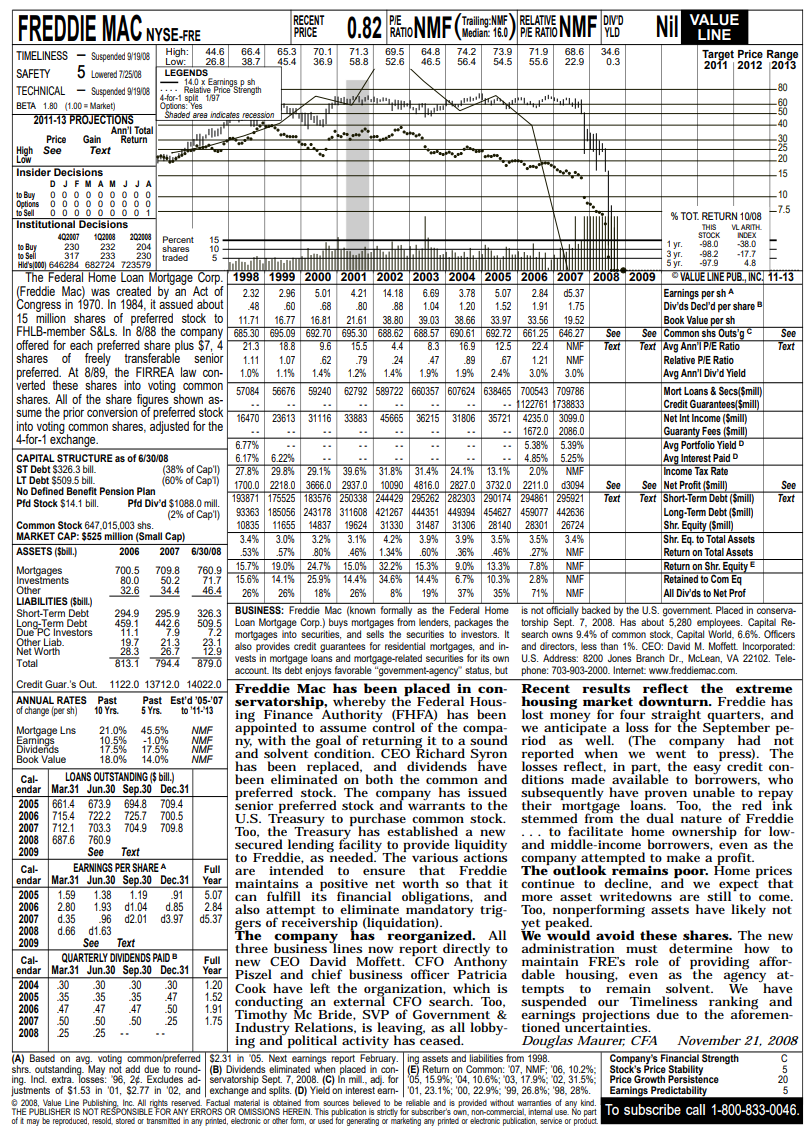

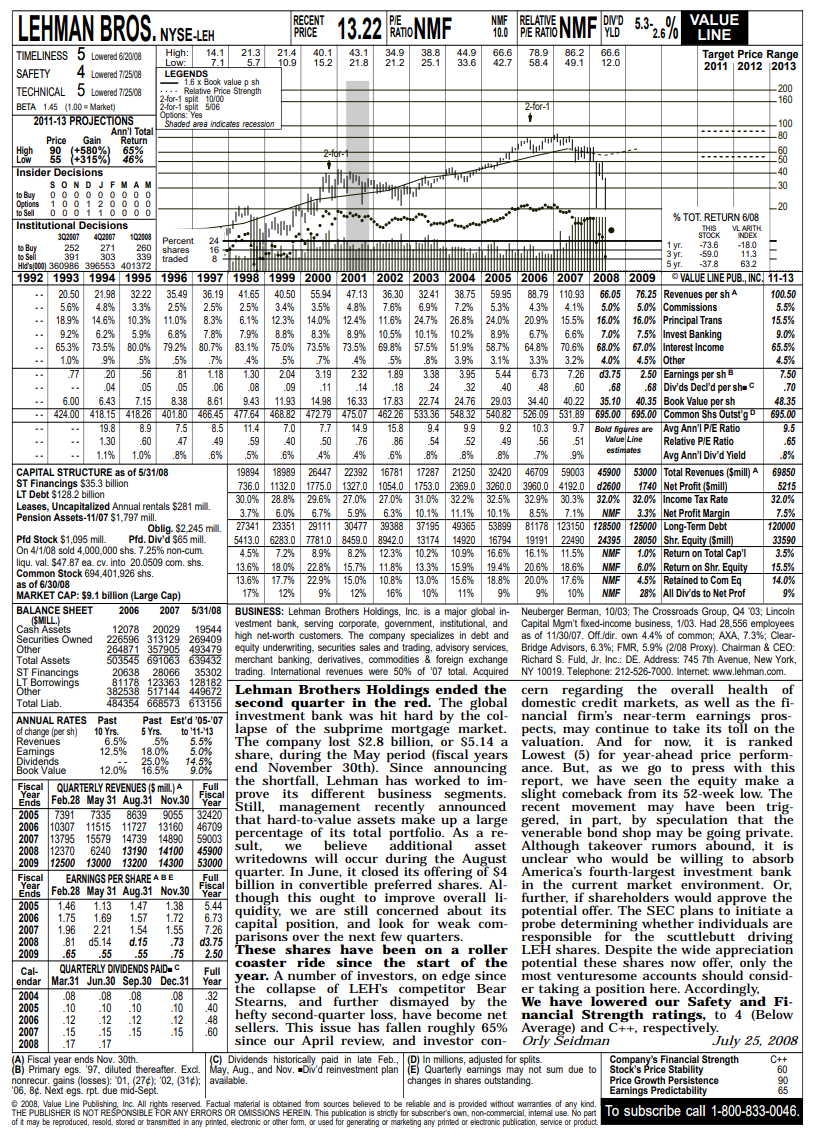

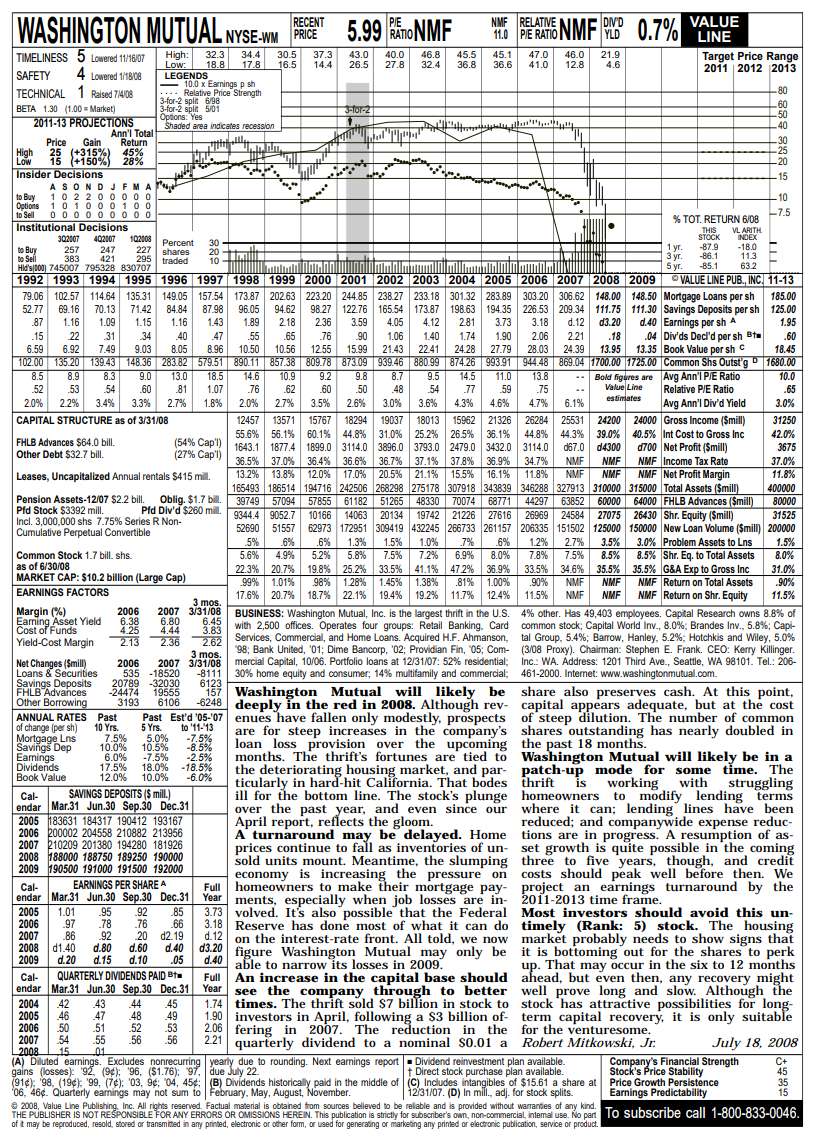

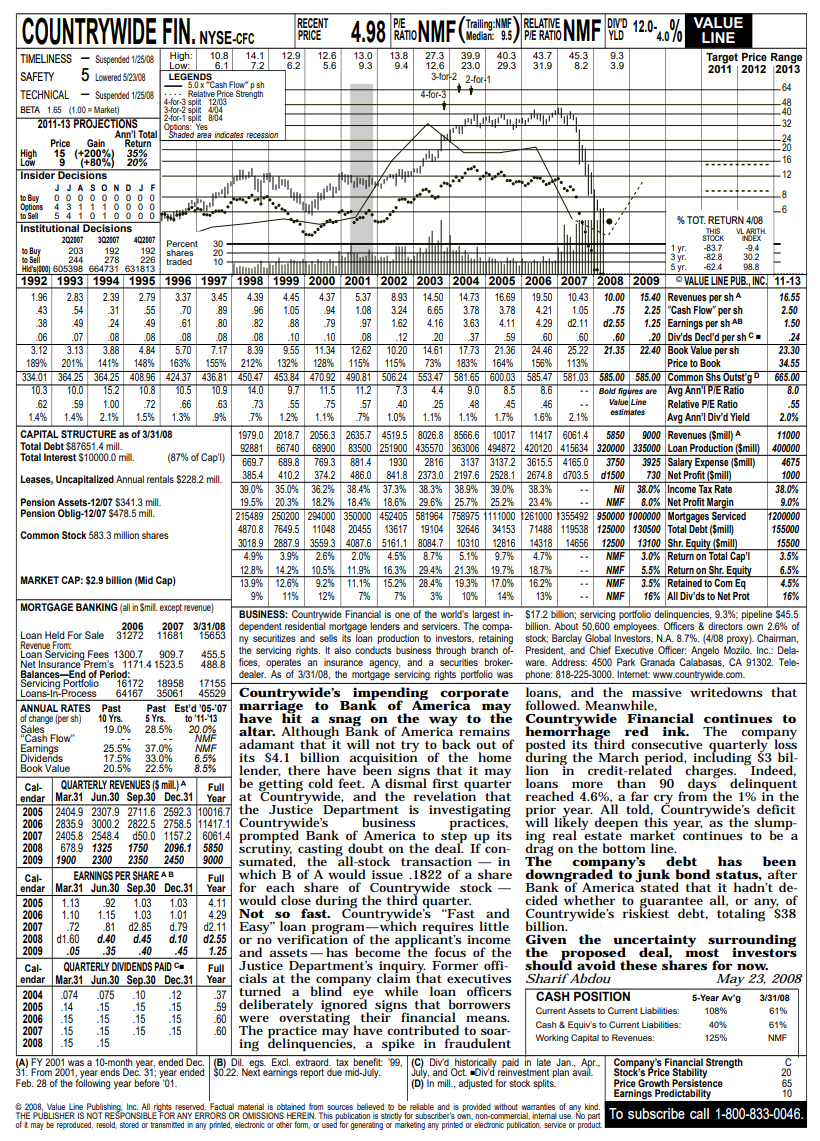

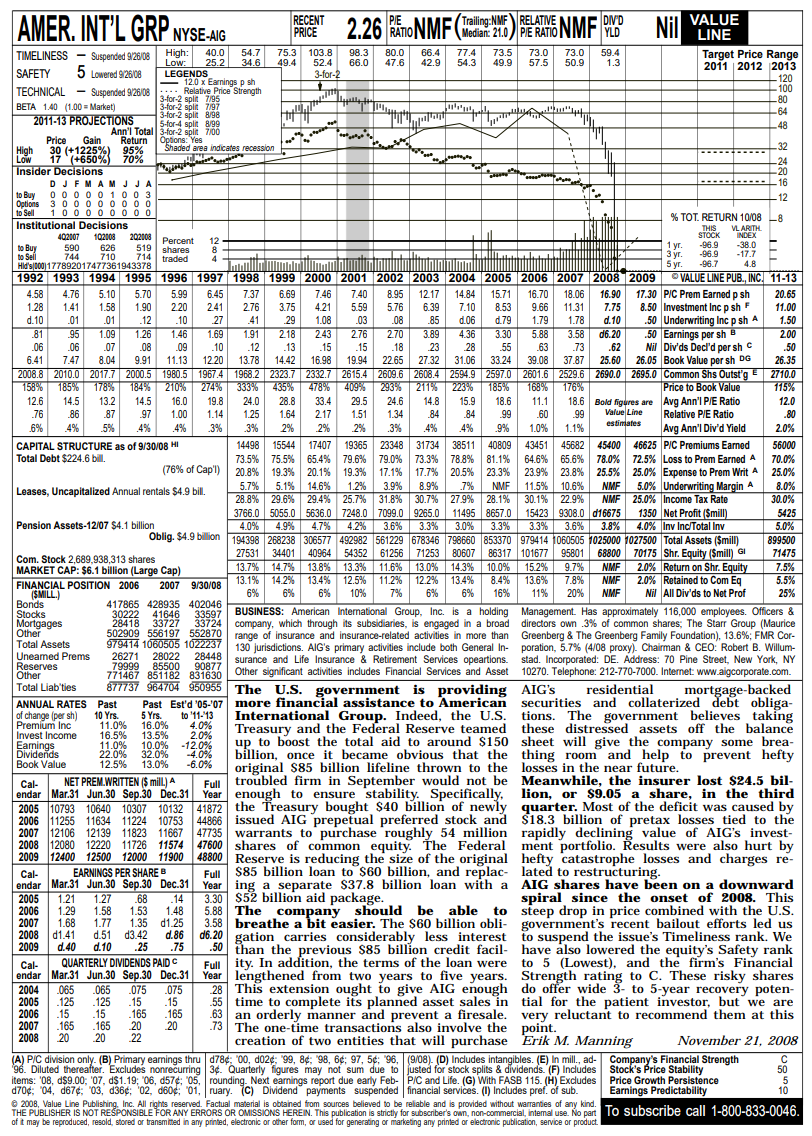

I figured out how to get ahold of some and thought they were cool. 2008 - Washington Mutual.pdf 2008 - Lehman Brothers.pdf 2008 - Freddie Mac.pdf 2008 - Fannie Mae.pdf 2008 - Countrywide Financial.pdf 2008 - American International Group.pdf 2002 - Yahoo!.pdf 2001 - eToys.pdf 2001 - Enron.pdf 2000 - Yahoo!.pdf 2000 - Cisco Systems.pdf 2000 - Amazon.com.pdf

-

Sure but it would give a certain short seller another opportunity or at least something to think about - especially if they still hold the same beliefs about the company. Just thinking out loud - you guys are great and help crystalize these issues.

-

They will get more creative. Yes, the TRS trick could always be used again.