dwy000

-

Posts

2,349 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by dwy000

-

-

4 hours ago, Xerxes said:

I think the pro/con of DRIP is well know for the investor point of view (less/no transaction, a bit of discount)

What is the pro/con for the company that has the DRIP program.

If company has $2 in assets, funded by $1 of liabilities and $1 of equity, and a 50cent dividend that is paid out as cash dividend.

Scenario A: investor takes the cash and walks away. That will reduce asset and equity by 50cents. increasing financial leverage. Simple enough.

Scenario B: if the hypothetical investor participated in the DRIP program, that 50cent stays in the company coffers as cash. Company issues new shares (dilution) to back those would-have been dividends.

What happens to the right hand side b/s ?!?

Scenario C if the hypothetical investor takes the 50cent dividend in cash and him/herself buys is more share (no DRIP no dilution). Like scenario A, this will reduce asset and equity by 50cents. increasing financial leverage. Simple enough. But shareholder balance sheet has now more shares.

I am struggling with Scenario B ?

easiest way to think of it is if every shareholder was in a DRIP. For newly issued shares the right side of the balance sheet is unchanged but the share count increases (equity reduced by dividend and increased same amount by newly issued shares). It's basically a stock dividend and is dilution for everyone. I think generally DRIP's are so small relative to shareholders taking cash it doesn't matter much.

-

2 minutes ago, Ulti said:

C'mon man, give some context. Where is this?

-

3 hours ago, Dinar said:

Actually, it is very easy to show to US taxpayers why we should stop funding Ukraine. Ask US citizens - would you prefer $300 tax reduction for every person in your family or send that money instead to Ukraine and see the results! I would be that if a nationwide referendum was held, not even 40% would vote to help Ukraine rather than their own pocket. Ukraine was derelict in its duty to build an army that could deter Russia, instead its politicians were busy pillaging the country. Responsibility for Ukrainian defense rests with Ukraine, not the US!

It's not actual cash funded. It's the value of weapons, most of which are dated and simply sitting in an aging stockpile.

-

On 7/31/2023 at 8:47 AM, HubbadaPow said:

I did the in-person version of this course several years ago when Bruce Greenwald was still teaching it. It was a week long and covered all the material he does in his semester long course for MBAs. I liked it. These types of things are very expensive and it's difficult to tell whether they are worth the money, but I've done a few of them at Columbia, HBS, NYU for continuing education stuff and to bring a few people on my team up to speed on specific subjects. For me it's better to dedicate a few days to take the course seriously rather than peruse it at my leisure. Going through the exercises during and between lectures and then getting interrogated by Bruce crystalized the principles in place better than reading his books did for me. It was also really helpful to meet ~100 value-oriented investors in my cohort for networking etc.

I've taken a bunch of these (including for MBA and after). By FAR the best and most effective part of them is not the teaching per se but the discussion and interaction. More learning comes from the other students and the prof reacting than anything you can read or watch.

It's kind of like this board. Regardless of your view on a stock (or issue) you will learn more about it, the industry, your thesis and you will ultimately understand it better by discussing and disagreeing than anything you can watch or read on your own.

-

12 hours ago, longterminvestor said:

First on Ryan, then Kinsale.

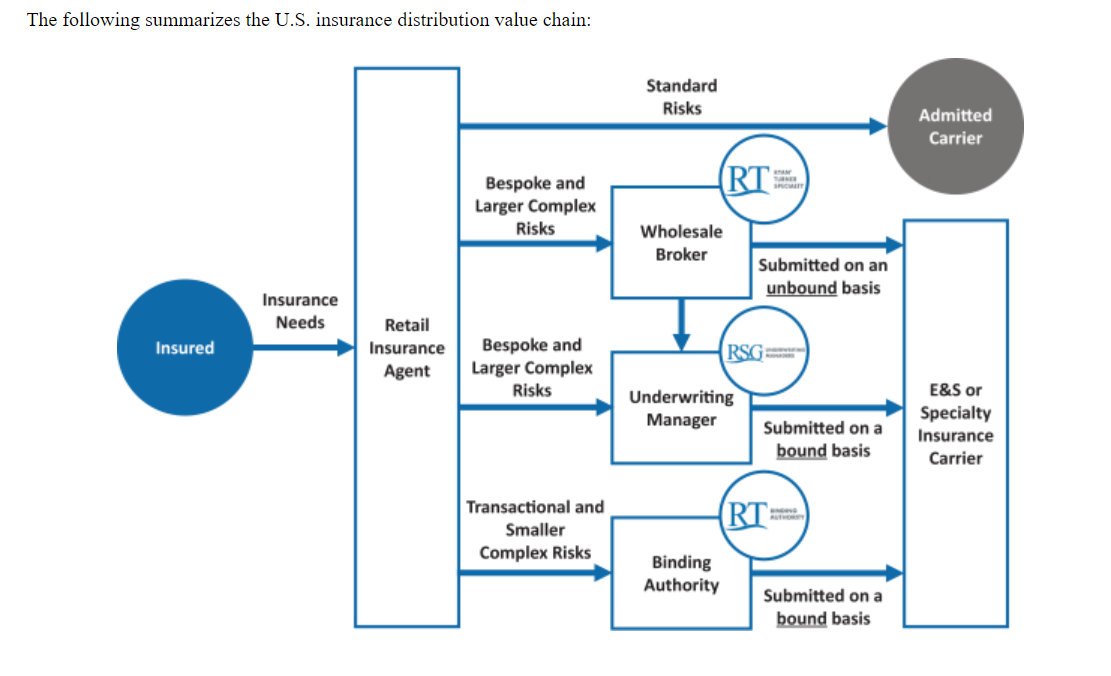

This is what RYAN are building (see below - taken from Ryan's S1). Actually pretty good for the thread on what the actual insurance distribution landscape looks like. Efficient in some ways, others not so much, but insurance is just hard to put in a portal and spit out a quote - case in point look at Lemonade (LMND).

The chart shows how vital the retail facing insurance agent is to the distribution system. Pat Ryan owns too much of AON so he couldn't be a retail facing agent, so he just took the wholesale segment by storm. The underlined "bound" terminology is SUPER important. When you as the MGA/MGU can bind, it means the insurance company has given you the underwriting authority. In the trade, its called "the pen", meaning you can write it. This is where the MGA/MGU does all the work and really the insurance company just sits back, manages the book, collects checks and pays claims.

Wholesale Brokerage is where a retailer needs help placing a portion of an account the admitted market wont write period or wont write competitively. In my region, wholesale is a huge part of the business. When ever people refer to the E&S market or Non-Admitted market, a wholesale broker is involved. Pat Ryan put it best, E&S is freedom of rate and form. Meaning carriers can charge whatever they want and throw down whatever coverage they want. Versus the admitted market where the carriers have to sit in front of the insurance commissioner, get the coverage language approved and file the rates they want to charge for approval.

EVERYONE that Ryan hires is like 25 and super Type A. Young and aggressive. You can call a random number at Ryan in a region you need to place a risk and get an immediate pick up or call back in like 2 hours. Never fails, they dont know who you are but they are ready to talk about a deal. Its pretty incredible. I'm sure there are lots of folks who call back but it is seriously a culture thing at Ryan. And the older folks who are there were bought in a acquisition. I'm long RYAN and probably should have bought more. I bought some more when it tanked after earnings a like 2 Quarters ago. Pat Ryan was buying big chunks himself. Which I loved. The story of how Ryan got started is pretty awesome. For another time.

KINSALE

2nd tier risk bearing insurance company who writes the stuff no one else wants to write. They will quote things no one else will. I have not looked at the business as investment, but we trade with them and they will turn things quickly. Gonna be on the tougher classes of business for sure with some language that is favorable to them, not the insured. Doesn't make them a bad market, this is just how companies grow up into bigger risk bearing companies. Gotta get your start on stuff no one else will write. There are worse insurance companies than Kinsale so they are not bad, they just are a carrier who doesn't have any polish. Markel started this way, and actually Markel and Kinsale compete on business in my market.

This was really interesting (something I never thought I'd say about insurance!!).

Two questions came up reading it: a) if the broker "has the pen", who is doing the actuarial work? It seems the broker can just underpriced non-standard risk to win business. How does the risk taking company control the pen if it's not off the shelf stuff?

B) on the wholesale, who is taking the risk and doing the pricing while the book builds to something big enough to pass along as wholesale? And if they aren't standard risks how are they grouped and packaged as wholesale? It feels like a fine line between wholesaling and actually being an insurance company that can hang onto risk to make the quarter if necessary.

Thanks as always!

-

12 hours ago, longterminvestor said:

According the Lloyd's Chief of Markets, Patrick Tiernan - 50% of the business written at Lloyds is US Based, 10% Canada, and 40% is the rest of the world. Decent stat but tough to really use because of the regional nature of insurance and the risk bearing companies being localized.

Tough to say what foreign markets are growth markets. If trying to handicap where growth markets will come, my hunch is where ever there is a growing debt market for real estate/business in general - insurance will follow. Where ever there is a contractual obligation, insurance will follow. No debt, no contracts - no insurance. That's true in the US at least. Client might purchase super cheap insurance but not like what a bank or a contract will require. Its gonna come from where you think it comes from, maturing economies, growing GPD's.

Other item is the non-competes - just don't know how well they stick internationally (never did the work on it). They have to be decent or guys like Brown wouldn't be playing. The non-compete is one of the most important parts of the brokerage business in the US. (Forgive me if I already said this), When a retail facing agency, the one who gets the paper work signed and collects the money from the insured/the buyer, signs an agreement with a carrier/wholesaler/MGA/MGU (we will make up some more acronyms soon enough), the agreement says the AGENCY owns the expirations of the book of business with the carrier/wholesaler/MGA/MGU. The AGENCY is the one who owns the relationship, individual producers will not have agreements with carriers, the agencies do. Now, the actual broker/producer may have ownership in their book, the actual accounts - could be a split where if the producer leaves, they can buy it at a price from the agency - usually pre-determined in the producer agreement with the agency, or like in the case of the big publicly traded brokers - the producers don't own a darn thing, zero, zilch. That's the asset. The book is the asset. Important to note contractually, the carriers do not own anything, theoretically the carriers/wholesalers/MGA/MGU's serve the retail facing brokers, if the broker wants to move it (tells the insured hey lets move from this carrier to that carrier) they move it. I'm sure the set up is similar internationally but just never seen one. Theoretical because it is supposed to be a symbiotic relationship. But sometimes it is not so sympatico, brokers threaten carriers all the time "if you dont do this for me, im gonna move my book" bla bla. I've never done business that way but people totally do. Or the inverse, there is only 1 carrier who will quote, so that carrier owns that particular market/line of business in that class of exposure.

Had a call just today where we were trying to negotiate some language on an endorsement and the wholesale counterpart said "We are one of MunichRe's largest money makers, they will do what we say". I was like, ok, thats fine with me.

I have placed accounts internationally and its usually a paper work/clerical nightmare as a US based Broker. For example, the Bahamas really makes it tough to write business there if you are a US Broker (Bahamas Insurance Commissioner wants the money to stay in the Bahamas). Probably similar in other countries as well. Again, the regionality of insurance is important - each region of the world has their own set of unique things and when a broker shows up in that market, they are probably gonna get smoked because they dont know the players.

I tried to place a deal in Hong Kong once, made 1 phone call to a friend, referred me to the Asia team, and immediately got told they had seen this account 3 times in the past 3 years. They did quote for me but was impressed how easy it was to get someone who could help me. Placed a deal in Mexico and just found a broker in Mexico who specializes is placing Mexican risks for US Brokers, we just split the commission.

Other item I have heard a ton about, specifically in South America, is the stamping of policies - specifically in Reinsurance. Important because when there is a stamp, the premium is noted and the taxes/fees are collected by the regulating insurance body. In South America, and other international countries, where the stamping is not really regulated, the carrier might quote $100,000 for a risk, and the broker tells the client its $120,000. So in addition to the commission, broker pockets an extra $20K when they collect the money from client. Again, much easier in re-insurance but I am sure it happens a decent amount. Would have to assume (famous last words) with big public brokers this doesn't happen but....

Hope this is helpful, glad I can share something where I have some background. Everyone on site is always nice and helpful. Been selling insurance for 16 years and family been doing it since early 1930's.

I'll end with a quote a I heard, just thought it was 1000% accurate. "Insurance Brokerage business is A+ money for C+ players". The public brokers are not C+ but there are some folks who work there that are definitely C+ at best and pull down some serious cash. 2nd Best business in the world, Software I guess has to be better. Said that to someone once, and they said Churches are the best business in the world. No taxes.

Cheers!

LTI - absolutely love your insider insights into this industry. Worth it's weight in gold. Please keep it up!!

-

If he was really a Goldman employee I'm not sure he'd be bitching about $50.

-

9 hours ago, crs223 said:

I haven’t had a car in 3.5 years (my wife has one and I just use my e-bike). I like the bike but I love not paying for gas, insurance, registration, maintenance, etc. I’ve never been a car guy, and I’ve only owned cheap and reliable Toyotas.

I went for a ride in a Tesla “Plaid” yesterday and now i’m rethinking my life’s choices. It was so much fun i’m still smiling 30 hours later. The car accelerates so fast (0-60mph in 2 seconds) there were moments I started to lose consciousness (maybe that’s abnormal — not sure).

$100k. If I weren’t married…

That gets a lot of people! The reality is that you will almost never need or use that extreme acceleration and while it's fun as hell, after a couple of weeks it's just the expensive car in the driveway. Lots of reasons to go electric if you buy a car but don't do it for the acceleration

-

16 hours ago, Sweet said:

A thread for something interesting which might even produce actionable ideas.

Here is one - I’ve not verified the data:

Some of these companies I’ve never even heard of.

It implies consistent long term growth but id suspect a lot of the gains for many of these were in a single 3-5 year span. I'm too lazy to research it but I wonder how many are on the 10 and 20 year list solely based on performance in the past 5 years.

-

18 hours ago, ValueArb said:

ARKK is up 48% this year, so she's clearly feeling her oats again. We should all get out of the way of the dual steamrollers of Tesla and ARKK!

And she will market the crap out of that gain even though it is only because she dropped massively last year and its a small rebound. I don't think she is breakeven on the money she has raised to date. But she will definitely market it like a 48% gain is a huge win not a dead cat bounce.

-

14 hours ago, Castanza said:

Anyone think tech has changed the social dynamics of cities? I mean wasn’t part of the draw always the energy of people being around and interacting? People going out to clubs or bars and actually talking or trying to pick up chicks?

Just seems like with the advent of the cell phone/social media this dynamic has changed a lot (probably permanently). Specifically for the younger generations this is noticeable. They value online interaction over in person.

Throw in other dynamics like wfh, crime, increased drug addictions etc and I can’t help but think cities as “social centers” has taken some kind of permanent impairment. If those things are no longer forefront then what’s the point of living there? Just spitballing too, could be completely off on this. Cities certainly could adapt I guess?

I don't know, that could be a factor but it could also be that with most work now done from home or isolated in front of a screen, the after work social part is more important. There aren't too many large cities in the US that are shrinking and rent seems to continue going up everywhere.

The dynamic of living in the city and enjoying the social aspects while you are young and single, then moving to the burbs or more rural when you settle down and have kids, seems to be continuing. What will be interesting is to see how the rapid decline in the birth rate will impact that.

-

1 hour ago, Gregmal said:

I mean you cant really operate fluidly as a business when hot dogs and ice cream displays need locks on them. Corporations still value having an NYC office, but not to the same degree they once did, especially in terms of size and grandeur.

I mean its been startling, even with something is fundamentally iconic and part of what makes NYC great as MSG....just how much nonsense these politicians are putting the company through for ZERO reason! Harassment for facial identity security software. Refusing an operating permit. Refusing to pay them for land they own. Demanding the company itself pay for public things. If thats how you treat your top talent so to speak, imagine being an aspiring entrepreneur? Like why would you start a business there knowing you're getting robbed on taxes. Gonna have to go through a horrendous business permitting and approval process due to the system. Safety isnt even something they care about anymore. At the end of the day the politicians and authority figures seem to have the exact same attitude as the NY Rulz Bruh! folks...like they matter of factly state "NY is awesome" like its a mic drop and expect everyone to just agree, and bow, and jump through hoops because "NY is so great"...and more and more, from corporations, to small businesses, to just normal(non homeless) people...we are seeing them just say "nah" because the mix in other places is way more favorable when all else is factored in.

When I invest, I like long and hard to disrupt tailwinds. Here you have the opposite. It probably changes again one day, thats how cycles work, and I'll be there to jump in when it does, but I gotta put food on the table and the investment case here is poor.

I agree, they do seem to shoot themselves in the foot and are their own worst enemy a lot. Many of the laws and regulations and things they try are stupid (I thought Bloomberg's "fat tax" on sodas was the ultimate big government stupidity attempt). Huge cities do dumb things largely because they can. And it will come full circle at some point as it always has - Guiliani's crackdown on crime after the Dinkin years for example. Bloomberg tacking red tape. Etc. It's funny because when I lived there some of the older residents lamented the clean up and Disney-fying of Times Square because they thought NY was losing its grittiness and hard edge.

But as a place to start a business it will always be a top draw because it is where the money and the talent accumulate. Even in WFH, the jobs, the networking, the bars and restaurants get centralized for efficiency. 25 or 30 yr old IT engineers who want to and can make an absolute fortune don't want to do it Des Moines, Iowa, they want to be where the action is.

At some point the pendulum will swing back and they'll loosen up the dumb rules and reduce the tax burden but it will take a while.

-

42 minutes ago, Dinar said:

You cannot be serious. Crime is way worse than it was for a 15 year period between 1999 and 2014. You may come up with statistics, but when police downgrade crime, prosecutors don't indict, and criminals do not go to jail, what's the point of reporting a crime?

I'm not sure how you compare if you don't use statistics.

Certainly homicides dont go underreported (you would hope). From the latest comparable stats (2021), NYC's homicide rate of 5.8 murders per 100,000 residents is way, way less than other large cities: Chicago (30), Houston (20), Miami (10.7), Oklahoma City (12), LA (10). Property crimes were 757 vs Miami at 3,716.

These could all be worse now than 2021 of course.

I think NYC feels worse because of how dense it is. Other cities have violent pockets and you can pretty much live in that city without ever feeling unsafe but in NY it's so dense it's harder to avoid even though its safter.

-

29 minutes ago, Gregmal said:

I mean sans the 20-30 year old crowd, and maybe the immature Peter Pan 30+ craft beer Brooklyn crowd, and then the 1% ers who own multiple homes or can at least afford to, how is Vegas, South FL, parts of Texas, Reno, Raleigh, Charlotte, Virginia, heck even Massachusetts suburbs not more attractive?

I don’t know any parents who like restaurants so much that they willingly choose to place dining out as a higher priory than their kids educations. Or athletics? Like oh hey Johnny, why don’t you run down to Washington Square Park and make friends with a gangbanger and a hypodermic needle lol.

Crime wise it is WAY better than almost any point in the past 50 years. Of course there's drugs and homeless etc but you're gonna get that in a city with 18mn people. There isn't a city without it. But NYC is also the center of the world for finance, art, theater, advertising, sports etc. That's the attraction. All the great things about Florida, Charlotte, Reno etc are what you look for AFTER you leave NYC. Or where you go for a week to relax. Nobody goes to NYC to relax or get the early bird special at TGIFriday. That's the appeal when you're young.

-

21 minutes ago, Gregmal said:

For who though? My understanding is that the migration and demographic shift is not occurring in the 20-30 or 30-40 never grow uppers, but everywhere else. Who either wants to, or properly can afford to raise a family there? Sending your kid to even “decent school in NYC requires private education and that’s $50k a year. Who’s retiring there?

The strength is obviously the young folks. But WFH challenges that. And outside of that? There’s not much other than trophy homes for the top 1% and then shitboxes for 25 year olds looking to fuck.

But that's what it has been for 50 years and likely will continue to be. Young people move in trying to make it big, then 20 years later they move out and a new crew moves in. It's the same in London.

I lived there for 12 years until I got married and had a kid and then moved to something more appropriate. All the things I care about now from schools to taxes to having a large master bedroom was completely irrelevant in NYC. At the time those were "old people" problems. We wanted to work our asses off, make a ton of money, get laid and have fun. That's NYC.

-

7 hours ago, Gregmal said:

LOL yea. Its amazing how resilient the "NEW YORK RULZ BRUH" crowd remains in defending all this. But the city is a shell of its former self and the numbers dont lie. Its just incredible that they continue to support politicians that are actively trying to make things WORSE!

You know, how bout fixing your broken and gross public transportation system instead of banning gas stoves and pizza ovens...nah. That would involve "enriching" the evil owners of those properties....so........lets just free some more criminals.....

NYC population has increased for 3 consecutive years. Rents are ridiculously through the roof. Hotel rates are through the roof.

It may not be your cup of tea but people under 50 are drawn to it like a magnet. The crowds and action and excitement that older people hate are exactly what draws the next generation crowd every year.

-

7 hours ago, Gregmal said:

This is the death spiral.

https://nypost.com/2023/06/30/new-york-tax-revenue-falls-nearly-20-while-florida-texas-gain/

Who they gonna tax next? Normal people and families ain’t hanging around and putting up with all this….restaurants and 20 something year old lifestyles be damned.

The reference is to NY State, not city. New York and California rely heavily upon capital gains tax and wall street income. It makes their revenues extremely volatile. With markets down last year they'll take hits to revenue this year.

click on table 1 for revenues for the past 30 years. Fiscal year tax collections: 2021-2022 (ny.gov) Revenues in 2022 (based upon gains in 2021) were up 47% while the previous year was flat.

-

1 hour ago, rogermunibond said:

iCloud, OneDrive, Google Drive, Dropbox. Any others? On premise hard drive that connects to your devices. I am shopping around for a solution after hitting the limit on free storage from several of the above. Is it worth the convenience and ease of paying $12/year to Apple or $24/year to Google for the convenience and ease?

What are folks using for storing that mass of photos, videos, documents that modern life seems to generate?

I primarily use OneDrive because you get up to 2Tb free storage if you subscribe to MS Office.

It works great, seamless across all devices (even Apple ones). I'm not sure how well iCloud works on non-apple devices but I assume pretty seamlessly too.

-

Okay I really know nothing about the military aspect or anything here at all. But why couldn't Putin control Wagner through the checkbook? They are a private army funded by the Russian government and supplied by the Russian government. Why couldn't Putin just stop funding? Without the money to pay the soldiers and buy everything from food to ammo wouldn't Wagner Group in Russia slowly just fall apart? It's not like they have their own funding source in Rubles and access to equipment and supplies in Russia without the government support?

-

19 hours ago, dealraker said:

Brown and Brown beginning of a write up - subscription is required for the bulk of it.

This was the writeup that got me interested to start with!

Longterminvestor - as always, thanks for the thorough and detailed info. Great to hear from an inside expert.

The part i keep struggling with is what exactly you are buying with all these mid sized businesses. As you mention, this is an elevator asset business and the best producers will go out on their own pretty easily - and probably take their best accounts with them. When they get big enough they sell out for a premium and the cycle starts over again. If you stop making acquisitions it seems the business will gradually dissipate as producers move on. Yes there is organic growth but I assume most of that is during the non-compete period and while selling owners are still engaged.

Is there any benefit to the client from dealing with a BRO or an AJG instead of the smaller family firm? I would imagine definitely at the large end where you need specialization of product expertise and diversity of insurers. But it feels like there is a point where market share of the big guys caps out and the dissipation of business to the new entrants splitting out is equal to the amount of business being acquired. Is this accurate? Are we close to that point? Where does the market share of the top 10 cap out in the industry? Is this why they're all looking overseas?

Thanks again for all the color!!

-

On 5/21/2023 at 1:47 PM, longterminvestor said:

Good report.

Thought it was interesting how PB commented on PL/D&O market with lots of capacity due to market pull back on property – risk bearers needed to deploy capacity and they are now competing on PL/D&O. he goes “I am not saying that, but some would say that”. Just thought that was funny. Can confirm we are seeing that, we just doubled the limit on a D&O placement for publicly traded company for the same price last year – 2X limit for same premium.

Regarding Florida/Citizens Insurance question. I was in a meeting once at Brown – this is 10+ yrs ago and the word was “Where Florida goes, so does the rest of the company”. PB downplayed Florida yesterday on the call – my gut/my opinion, Florida insurance plays into BRO revenue/earnings – materially. I think I know why management is attempting to dissuade street from thinking BRO is buoyed to Florida. Here is some data:

As per 10K’s, revenue in Florida as a percentage of revenue:

2022 - 19% of total revenue comes from 55 offices in Florida

2021 – 18% of total revenue comes from 55 offices in Florida

2020 – 19% of total revenue comes from 55 offices in Florida

2019 – no breakout – mentions 52 offices and headquarters in Florida

2018 – no breakout – mentions 46 offices and headquarters in Florida

2017 – no breakout – mentions 41 offices and headquarters in Florida

2016 – no breakout – mentions 41 offices and headquarters in Florida

2015 – no breakout - mentions 41 offices and headquarters in Florida

2014 – no breakout - mentions 41 offices and headquarters in Florida

% numbers above from 2020-2022 are deceiving because Atlanta wholesale office’s produce huge amounts of Florida borne business and yet the “office”, as you know, is in Georgia – not Florida. There could be other wholesale offices outside Florida that have relationships with Florida agents and place deals in Florida – would be tough to get a “to the penny” number on % of revenue deriving from Florida based on the way reporting goes so Brown reporting by office geographic location is logical.

CITIZENS REVENUE BREAKOUT FROM K’s YEARS AGO:

2014 - $3.8M

2013 - $5.7M

2012 - $6.4M

2011 - $7.8M

2010 - $8.3M

PB’s comment on Citizens commission was 100% accurate. Premiums are higher today than they were when Citizens played into the market in 2006-07 – 2015ish. Risk is legislature reduces commission at some point if premiums continue to rise however for the work we are putting in as agents, gonna be tough to justify. But that politics, not insurance (I guess they go hand in hand).

Also – did a quick search in AON, Willis, Marsh 10K’s – no mention of Florida at all and revenue aggregation in Florida.

WTW disclosed 21% of revenue generated from UK

Aon disclosed 55% of consolidated revenue is non-US

Marsh is a little different – 51% of company revenue is insurance, 10% reinsurance, and 39% consulting. Marsh does disclose 51% of total revenue was from outside US

This is great color @longterminvestor! I'm trying to do a bit of a deeper dive on BRO and must admit all the Florida insurance stories are concerning - although I'm continuing to see it as more of a risk for property owners through premium increases than for the broker side (which actually benefits). Let's assume BRO has about 25% of revenue risk in Florida (higher than above due to the out of state initiated coverage, and probably reducing as they seem to be expanding in the UK market faster than US). What exactly is the risk here for BRO? Is it Citizen's reducing commission rates? Reduced coverage as prices grow fast? A new state funded insurer getting stood up to take on additional risk that will bypass or cut commissions from brokers like BRO?

Secondly, do you have any color on the acquisition side? If BRO alone has acquired over 600 companies in the past 30 years and they are one of many acquisitive public brokers, and now private equity is scooping them up for inflated prices, what is the outlook? How many small brokers can possibly be left that are of size to warrant acquisition that moves the needle? Where are all these small firms coming from - is it brokers leaving BRO, AJG etc to go out on their own knowing they'll get bought at a premium?

Would love to get more of your input. Despite my wife looking at me like I'm nuts when I say this is a really interesting industry, from an investment perspective I love these FCF, acquisitive machines that fly under the radar screen because it causes people's eyes to glaze over. Thanks!!

-

2 hours ago, Parsad said:

Regarding why it's quite painful to watch the Saudi's get their mitts on the PGA. I don't think there is another sports organization that is in control of and connects with players/fans at every level. The PGA is responsible for numerous tours around the world, including virtually all of men's golf and lady's golf. They have their hands on college players, amateur championships, the senior's tour, instructors at every major golf course around the world, and any member who wants to handicap their game has to run through the PGA's programs and rankings. It was a virtual monopoly until LIV came along. While certain aspects of LIV were good for golf, it is the perfect stepping stone for the Saudi's to get into other sports. Cheers!

Just reading some of the summaries of the deal it looks like the PGA made out like a bandit. They got rid of a competitor, got rid of the litigation, got a minority partner who will put up a ton of sponsorship cash, and retain ultimate control of the sport. PGA keeps the non-profit holding company and has majority of the Board of the operating company that will run not only the PGA events but also the LIV events. I'm actually struggling to understand what LIV got out of this.

-

2 hours ago, Parsad said:

They aren't leaving the California market...they just can't take on any more risk unless premium pricing compensates them. Their reinsurance costs are probably significantly higher this year for California, so they can't afford to write any more policies without adequate premium pricing to compensate for reinsurance costs. Cheers!

I was referring to the fact that if you can't get the savings from bundling home and auto (because you don't offer home anymore) the auto side is likely to see volumes suffer quite a bit so it's not just the one p4oduct line that will shrink.

At some point you simply can't put unrealistic caps on free market participants and not see the consumer suffer.

-

53 minutes ago, RedLion said:

Thankfully I got a State Farm policy just a couple months ago. I can say, State Farm is the absolute best if your house burns in a wildfire, but it looks like we might all be stuck on California (un)FAIR plan.

I hope.youre not speaking from personal experience!!!

With bundling savings of auto policies this would imply SF is almost pulling out of California altogether.

I would guess this is a major public statement largely to pressure regulators to allow price increases.

DRIP pro/con for the issuer (not the investor)

in General Discussion

Posted

forgot to reiterate what Inofeisone mentioned - if the plan is a true "reinvestment" plan and not one that issues new shares, you will effectively be receiving cash and simultaneously be making a market purchase of stock. There's price risk there for a very short period of time but the important difference is the accounting: lower Equity by the amount of the dividend and simulaneously lower cash. The share count would be unchanged. You will be taxed as a regular dividend even though you didn't net any new cash in your account.