Thrifty3000

-

Posts

646 -

Joined

-

Last visited

-

Days Won

5

3 Followers

Recent Profile Visitors

3,896 profile views

Thrifty3000's Achievements

")

-

Putting on my “think like a billionaire cap”… FFH is Terminating TRS contracts - not Selling contracts. TERMINATING a TRS contract is not the same as SELLING a TRS contract. No cash is exchanged for terminating a contract. A TRS is a derivative contract - not a share of stock. The TRS settled/settles every quarter, and has essentially accrued zero dollars at the beginning of each new quarter. All cash/gains from the TRS contracts was received at the end of each 90 day contract period. Imagine someone has been giving you cash every 90 days that equates to the difference between what your FFH shares were worth at the beginning and end of said quarter. If you’re wearing your billionaire cap what would you do with cash you had already booked/received from a contract you’ve since terminated? Under what scenario would you close a derivative contract on an asset that you then turn around and feel is undervalued enough to purchase outright?

-

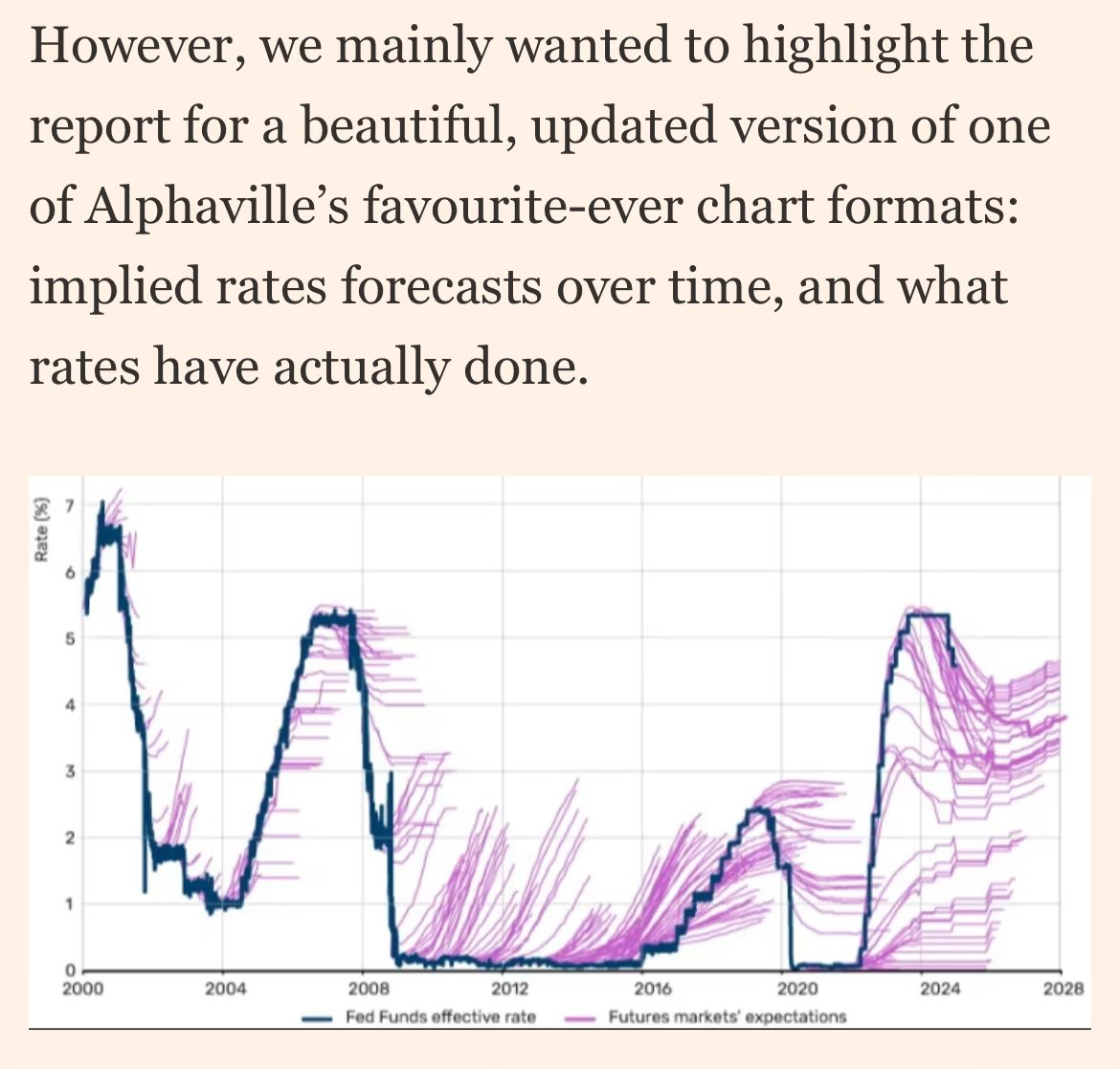

Yeah, here’s a chart showing rate predictions vs reality overtime. A big ol’ time waster.

-

Anyone else hear rates gonna be higher for longer? Or, just me?

-

If you’re having trouble sleeping, might I recommend: https://therest.ca

-

Imagine you have $500 billion. Would you rather own $30 billion of an index with an earnings yield of maybe 4% that’s growing 5 or 6% annually, or a single, diversified, conglomerate, with an earnings yield of 10 or more percent that’s growing 10 to 14% annually? No matter what, both assets will be under, fairly and over-valued over time, whether or not said conglomerate is or isn’t in said index.

-

You’re also getting increasing geographic and revenue diversity - expanding that moat.

-

Congrats, the season’s officially over. Looks like we survived another one! Glad it went better than expected.

-

Industry average P/E is 12. Prem puts the normal earnings floor around $125 per share. 12 x $125 = $1,500. I definitely wouldn’t sell for less than that.

-

I took the day off to play golf. Did I miss anything?

-

FWIW My neighbor moved all her valuables and her most beloved memorabilia into a storage unit about 3 years ago. The timing was rather fortunate because only a couple weeks later her house happened to catch on fire, at which point she panicked and traveled on foot to her boyfriend’s house some distance away - to seek his assistance during this trying time. Shortly thereafter they got in his truck and drove to her house to decide how best to handle the growing emergency. By the time they arrived some good samaritans had already called the fire department, though the call was made too late to salvage the home. After 3 years of reconstruction, my neighbor and her daughters just moved back into their fully rebuilt and refurnished, dream home - courtesy of whatever insurance company she has royally suckered. Long story short. Incurred losses are a fun little fictional adventure that play out over several years. Even if FFH estimates record losses from Milton, they’ll be able to charge record premiums for the next few years while they’re shelling out the money needed for post-Milton reconstruction.

-

Ok, so I do feel like I get what you’re saying about reinsurance and retrocession policies (aka reinsuring reinsurers). But, in my tiny little meat computer I have to oversimplify by making it all about replacing or repairing “structure/asset equivalents”. For example, if a boat insurer insures 10,000 boats, but pays FFH to accept risk for 2,000 boats in the event more than 20% of their insured 10,000 boats have been damaged, then I have to think about how many boats FFH is on the hook for. Yes, it’s vast oversimplification, but my monkey brain would stroke out if I didn’t oversimplify. By oversimplifying I’m basically telling myself that if a fictional super-hurricane wiped out every single home in Florida that FFH would be on the hook for roughly 90,000 residential policy equivalents for homes with values averaging $400,000. I know I’m wrong but I’m just trying broadly frame this risk, while also eliciting excellent feedback from more evolved monkeys who also contribute to this forum. (After all this typing I’m really starting to crave a banana.)

-

If Florida has 9 million homes and Fairfax insures approximately 1% of them then I'm going to assume FFH is insuring maybe 90,000 homes in the state. FFH just needs to be sure they're spreadin' them suckers out. Piece of cake. Haha

-

Some stats on home destruction/damage in Florida from a couple recent storms... Hurricane Ian: Homes Destroyed: 5,000 Homes Damaged: 30,000 Hurricane Michael: Damaged or destroyed approximately 60,000 structures If you contrast those numbers against 9 million total homes in Florida, it seems there's plenty of opportunity to spread the risk.

-

Milton's impact area and trajectory across Florida are shaping up pretty similarly to Hurricane Ian in 2022. Ian was very powerful, only 2 MPH short of being a category 5, and made landfall south of Tampa - heading west to east. It sounds like insurance industry losses for Ian ended up in the neighborhood of $50 billion. At the time, Fairfax estimated their Hurricane Ian losses would be in the neighborhood of $560 million. Fairfax ended up fairing rather well despite the Hurricane Ian setback.

-

^ he says 20 years ago he identified a west to east direct hurricane hit on Tampa bay as the top insurance risk in the country. Rounding out his top 3 risks at the time were a hit on New Orleans (prescient) and a hit on Manhattan (Sandy was close but not worst case). Says Tampa’s downtown will likely be 15 to 30 feet under water. Ouch.