kilroy04

-

Posts

49 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by kilroy04

-

Word around office space is starting to sound as if rents will be going down. More people working from home - with a trend for this on a long term basis. Less office space need. Don't know what will happen with residential rent. I'm inclined to think that will trend down as well. If you don't have a job or have less income, you move in with somebody else. Vacancy created. Who is going to rent that and at what price? This all seems to be deflationary pressure. In the 2008 crisis, some of the cds gains could be seen before it showed up in the stock price. I wonder if the same could occur here.

-

Any updates on deflation/inflation marks for the EU and the US? Any suggestions as to where this quote can be viewed?

-

Thanks for posting that mcliu. With severe recession (or more) and all the needed stimulus, it will be interesting to see what happens. Even volatility could turn out to be significant with that notional amount. There could be cds rhymes. Based on the last 20 years, it would be somewhat unusual for FFH not to have some level of hedging.

-

From the annual shareholders letter: $100 billion notional amount in deflation hedges which still have 2.8 years to go and are now on our balance sheet at only $7 million. Do you suppose this might yet come into play? Anyone have access to data on this?

-

For years and years the complaint was that the underwriting wasn't good. It was only the investing that saved them. Now it's the opposite. Somehow they made 10B investing. It's hard to believe they won't make significant sums investing again. Regarding admitting being wrong, perhaps that word wasn't used but there was clear talk of results not being good. Perhaps another way of saying it?

-

Crestwood is interesting - a yield in the 30+% is insane. A basket of stocks like that makes me think of Buffett and his Korea bet - PE's of 2-3......it's just cheap. Some have to work out. Looks like this particular take or pay arrangement in a company without IDR's (incentive distribution rights) to the general partner holds some promise. I've tended to be a skeptic on MLP's - hight payouts always worry me from the perspective of needing really good management to be responsible regarding the payout and business risk. All you have to do is look at PWE's history to see the bad side of payouts - fund it with debt, drips, and capital raises/dilution. From the standpoint of will the business continue - will need to look into who their pipes service. Obviously the storage and arbitrage business won't go away. That's likely where the margin of safety would come from. Nice find Picasso. I'll keep digging. It's this type of thing that makes me think shooting fish in a barrel and material portfolio impact.......

-

Picasso - thoughtful post. I suspect you are right in that until we see major shakeups, the pain hasn't yet fully arrived. Stepwise deterioration is certainly a potential scenario. SunCoke seems to be worth a bit more of a dive to get some understanding. Had a quick look...

-

Oil: Shooting Fish in a Barrel.......or Not

kilroy04 replied to kilroy04's topic in General Discussion

UCC - this is precisely the type of discussion the post was meant to stimulate (not feeling picked on and mostly agree with you). The tide out - potential tide in - nature of oil makes it hold the possibility of a material change to a portfolio. It could materially change either way and needs to be weighted as such. In my opinion, the lower oil goes (perhaps into the 20's or even teens) the safer it becomes to invest simply because the rebound would likely happen sooner and stronger. Of course we can't know a bottom for certain until after the fact. It seems to me we are low enough below marginal costs that investing now assures good upside if you choose companies that have staying power but are still reasonably leveraged to oil price. Buffett was early in the fall of 2008 with his NYT's editorial about buying - but he was of right. We might be a little early now.....but keeping some dry powder can certainly help I've allocated about 5-6% and will probably allocate more. Particularly if oil gets into the 20's or teens. Sharper - I was a bit early on PWE but got pretty lucky employing one of the strategies you noted close to the bottom. The swiftness of the upswing was powerful - and in the end I didn't want to sell shares due to the fact that the upswing put me in the money. I also like your idea of the targeted exit. It shows the leverage potential of this type of opportunity. -

Picasso - if you've finished loading up already and are interested in a discussion, I'm sure the board would be interested in your thesis for some energy players in various places in the chain.

-

Oil: Shooting Fish in a Barrel.......or Not

kilroy04 replied to kilroy04's topic in General Discussion

Some metrics on the lower risk side Bonterra - 71% oil/liquids - 29% gas Production about 13000 boe/d Shares 33.1.m Market cap 500m cdn Debt 336m of 425m bank line (last approved 9/15) EV 840m Netback (last quarter ) = $24 at sales price of 43 Dividend = just cut from 0.15 to 0.1/mo (payout 56% last q) yield about 8% EV/flowing barrel = 64k More than doubled debt with 170m Cardium purchase (at mid 97k or more/flowing) in the spring (maybe a bit early on that) Comment – focused on per share metrics – near 15 year record of improvement. I like that per share focus Surge Energy - 76% oil/liquids - Production about 14500 boe/d Shares 220.8m Market cap 413m cdn Debt 143m (400m bank revolver last approved 9/15) EV 556m Netback (last quarter ) = $14 Dividend = 0.15/yr (8-9%) EV/flowing barrel = 38k Debt to cash flow 21% annual decline rate - 50m capex will maintain at 14k boe next year. More a conventional play than tight oil play. No Drip Happy to see rationale for or against any particular plays with the caveat, I don't think one can yet enter this space without risk. There may be a time when you can see through things that others don't (ala Fairfax with the cds) but it doesn't seem we're there yet. -

Just for a pulse of the CoBF board

-

Seems there could be a ton of opportunity and or a ton of risk.... Some of this has been discussed but thought it might be worth revisiting in various ways. Macro – Tide Out Tide in tide out investing vs finding a needle in a haystack (as mention by Brian Spectre outgoing Baupost exec). It is likely we are going through a tide out situation. Supply: It appears that excess supply is not more than 1.5mm boe/day (about 1.5-2% and not the severe excess of the 1980’s). There is risk for further increased production in Libya, Iran, Iraq, Canadian Oil Sands, Gulf of Mexico……and perhaps others. Current excess oil in storage in the OECD. – about 250mm barrels according to the IEA (essentially 33 days of supply vs the usual 30 days globally). Consumption: Growth has been healthy at > 1.8mm boe this year. If there were a global slowdown – that would obviously be important. So far the China “slowdown” with respect to oil has actually been a substantial increase daily consumption Long Term Green Energy: At some point unknown (but I’d guess very incremental for at least 10 years) fossil fuel will be a less dominant form of transportation energy. Though the IEA number still show similar usage as today out for 25-30 yrs. Marginal cost of production is 50-60? Coming down further? Cash lifting costs? Full cycle cost of production is thought to be a bit higher Core Question: Who can survive a few years at ongoing spot prices – whatever they are – including in the 20’s? (without the benefit of hedges that are coming to an end) Some broad ideas below Low Cost Producers and or low debt Survive with oil in the 20’s - 30’s for 2-3 yrs Upside 1.5-3x Bonterra (can be cash positive at WTI 35) Surge Energy(low debt) Peyto ( mostly gas - long history of doing well through cycle) Low to medium cost with debt or other issues Survive with oil in the 40 -50s for 2-3 yrs Upside 5x + Bellatrix? PennWest (requires further asset sales- if possible) Gear (maybe) (netback getting close to zero at these prices) Survive with oil 60-70 - need it soon! Lottery ticket Sandridge (trading for debt at discount) Twin Butte (pennies and a junior) Lightstream (Trading for debt at discount) Thoughts?

-

From 2000 until present, book value grew from about 150 to 400 USD/share (this quarter). That's a compounding rate, over nearly 16 years, of 6+%. The stock currently trades at about 1.25 book value. Having said that - they tend to have burst of gains in book value. Not much has happened since 2009. Below is book value divided into the "7 lean years" when they were cleaning up acquisition troubles and then the subsequent years with "normalized operations". 2000 148.14 2001 117.03 2002 125.25 2003 163.70 2004 162.76 2005 137.50 2006 150.16 2007 230.01 2008 278.28 2009 369.80 2010 376.33 2011 364.55 2012 378.10 2013 339.00 2014 394.83 2015 q3 (399.65) Their target is 15% return on equity. Since the lean years passed (the second set of book values starting with 2007) they have hit about 10%. However, essentially all that return occurred in 2007-2009 from their bet agains mortgage backed securities. If they were hitting their 15% book value growth, it would now be approaching 550 USD. Time will tell if there is another "catch up" burst in book value growth.

-

I suspect it is their DNA (Prem pretty much said so at the AGM) to be Graham type value investors - more than Fisher type. One might wish for them to change their style. It is hard to change DNA. Despite their challenges with common stocks - book value is growing. Just not at the 15% they and we hope for. What I like: 1) They've dramatically expanded their insurance foot print in the west and globally. Asian insurance is growing like FFH in the early days. There is plenty of statutory capital reserve to nearly double their premiums written in the next hard market - that will likely lead to the stock doubling (look back at the last hard market about 10 years ago). 2) They recognize the world is still extremely highly leveraged. A recession will come. Central banks have little more they can do beyond what is now being done. I sleep well at night knowing that the chance of permanent loss of capital is very low with Fairfax. Stocks are protected. There is strong protection against a big macro deflation event - which could come with a recession. FFH is the an anchor in my portfolio. With their downside protection, other risks I take are effectively hedged. They will win again. The timing is the question.

-

Gear Energy. Chairman: Don Gray (of Peyto fame). Heavy oil specialty. Junior. Seems to be following the same principles as Peyto. Trades at about an EV of 30k/flowing barrel. 5500 ish barrels/d. Market cap now around 60m. Net debt just over 70m and coming down. Still had good cash flow in q1. Nice monthly updates from CEO. Plenty of drill room. Very good debt adjusted growth and growth per share. They've held capex substantially in 1st half and are determining what to do in 2nd half (didn't think it made sense to have the high volume high decline portions of new wells sell into this environment). Potential capex of around 25m for the year. Seem to be very rational allocators with costs of about $23/b of oil. Good hedging with collars that may get them through this very low oil phase. Stock is about 90c now - previously up to $6. Insider buying in 2nd half of August at around $1.

-

http://www.nytimes.com/2015/07/09/business/dealbook/greek-debt-dispute-highlights-prospect-of-a-euro-exit.html?hp&action=click&pgtype=Homepage&module=a-lede-package-region®ion=top-news&WT.nav=top-news “I don’t think the Greeks want that and I don’t think the Europeans want that,” said David R. Cameron, a professor of political science at Yale. “At the end of the day, it is a lot easier to write another check.” Top left article on the NYT's website - The Euro as a weapon. Byline: Peter Eavis - I believe it is the same individual of a dozen years ago who wrote repeated articles on FFH and its "problems". Couldn't resist posting it under FFH. No real connection other than the fact that Fairfax has investments in Greece. Do you suppose the NYT's investigates its journalist's history in detail?

-

http://cdn2.hubspot.net/hub/312313/file-2316059151-pdf/Canadian_Oil_Gas_50_Sustainable_Report.pdf?submissionGuid=7d092c30-d20a-4ab0-8951-17470f838c63 Stress testing Cdn oil companies for various oil prices. Some good aggregate data on debt ratios for various companies.

-

More China http://dealbook.nytimes.com/2014/12/29/seeking-to-ride-on-chinas-stock-market-highs/?hp&action=click&pgtype=Homepage&module=second-column-region®ion=top-news&WT.nav=top-news&_r=0 “Almost everyone I know is investing, so I think I should be investing, too,” said Mr. Kuang, 51. “The index has been rising this year,” he added. But his own stock portfolio’s performance, he said, was essentially flat. China has been grappling with a slowing economy, falling property prices and increasingly tight financing conditions. But the country’s stock markets have been surging, thanks in large part to regular investors like Mr. Kuang.

-

How Are You Thinking Bout The Drop In Oil Prices?

kilroy04 replied to Viking's topic in General Discussion

http://www.bloombergview.com/articles/2014-12-21/ready-for-20-oil?cmpid=yhoo Gary Shilling - the cash cost of pumping the cheapest oil - once the well is producing is as low as $10-20/b. -

I'll bite. How about a Hamblin Watsa group detailed presentation of the due diligence done (and the findings) for 2 outlier and completed investments? One failure and one success. Two that come to mind are Canwest and Bank of Ireland. Purpose - educate on the process and depth of their due diligence, inform on the level of uncertainty in decision making, inform on alternative investments being considered at the time, and also to expose the intellectual honesty.

-

Something is happening...... http://www.nytimes.com/2014/12/19/business/international/in-china-housing-market-pressure-to-sell-hesitation-to-buy.html?ref=business Prices for newly constructed housing fell 1 percent to 9 percent in recent months in all 70 mainland cities tracked by the national government, according to data released Thursday. Prices kept falling in November compared with October in all but three cities, where they were unchanged. Yet real estate developers’ inventories of unsold apartments now equal 12 to 18 months’ worth of sales in China’s biggest cities, like Beijing and Shanghai, according to Haitong Securities, a big Chinese brokerage firm and investment bank. The industry considers six months’ worth of inventory to be healthy. While the property market is under pressure, a crisis does not appear imminent. State-owned banks are reluctant to foreclose on borrowers in arrears, and few buyers are forced to sell at a loss. Anne Stevenson Yang's latest interview. She was at last years FFH AGM http://online.barrons.com/articles/anne-stevenson-yang-why-xi-jinpings-troubles-and-chinas-could-get-worse-1417846773 We track the 400 Chinese consumer companies listed on the Shanghai and Shenzhen stock markets, and in the third quarter, their gross revenues fell 4% from a year ago. This is hardly a vibrant economy. Also says 50 million units owned but empty

-

Various costs of oil production by source according to Morgan Stanley Research. http://www.businessinsider.com/crude-oil-cost-of-production-2014-5 (can't seem to load the image - it's in the link) Middle East avg about $27/barrel. Russia about 50 and as high as 70. Oil sands as high as 80-85.

-

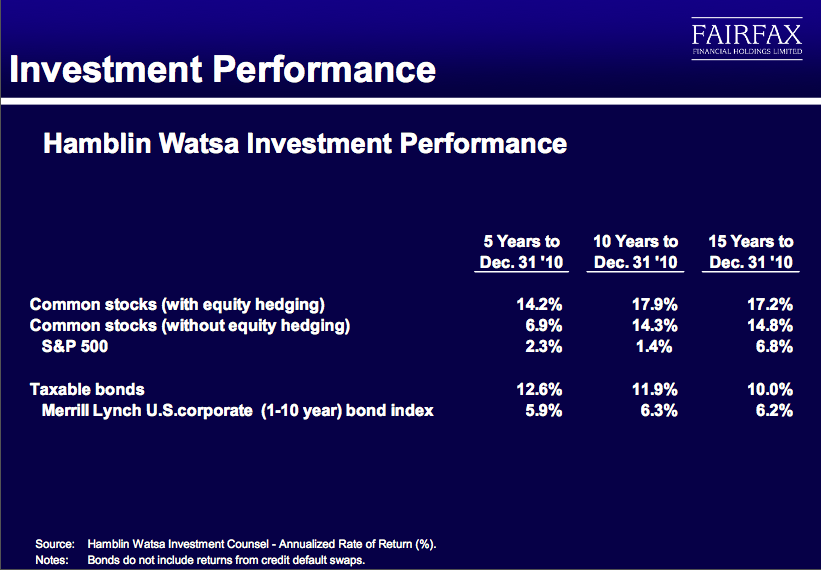

Slide 25 from the 2011 AGM. Returns with and without hedges. FFH hedges. It's what they do. They were doing it around 2000 and there was some angst around it then as well - particularly when there were issues of increasing asbestos reserves. The nature of their returns and the stock since the big correction of the late 90's is to stagnate and pop, stagnate and pop. It's stagnating now....... 2-3 years ago there were tremendous complaints about underwriting. Yes, cats were light this year, but Andy Bernard working on the culture of underwriting seems to be having an effect. I spoke with him at last years AGM and it was clear that he saw practices in the various companies that could be improved. Improvement has and is happening. Cost of float has declined from around 4 (if I remember right) to 2 to less than 1% over the past decade or so. There is a real chance of being paid for float going forward (and cumulative since the Prem took over). The insurance business is getting a bigger foot print, is expanding, and will expand tremendously in the next hard market. This will drive up float, provide more investments/share and thus improve book value. We just don't know when a hard market will come. Last time they essentially doubled underwriting. Think about that impact on float! If they are wrong about the hedges and BBRY - there's room to regroup again. They will if that is the case. The concerns about acquisition and investment business quality, as well as the hedges, are simply the concerns of this year. These are all far less threatening than the acquisitions of TIG and C&F and the associated reserving issues that came to light in the early 2000's. Time tends to fix things when you have honest and aligned management. And it puts things in perspective for those of us on the outside. If you absolutely need and expect yearly 15% returns - you'll probably be disappointed. The data shows less since the late 90's. If it happens - great! The numbers to achieve it are certainly there and I certainly hope it does. It is a $1000+ stock someday. Just not as soon as we might wish.....

-

Where are we in the innings of the 2008/2009 crisis? A little different way of looking at it but insightful nevertheless. Below from Fisher's Houston talk that Giofranchi posted. "Scholars know that Shakespearian plays all have five acts. I would suggest that we are but in the third act of a play—we had the tempest in Act 1; the jury-rigging of monetary policy and radical maneuvers by the Fed to save the ship in Act 2; and in the present act, we are back on course but somewhat becalmed, sailing at less-than-desired cruising speed even as we have cranked up an auxiliary motor of large-scale asset purchases. Act 4 will involve the travails and challenges of adjusting our policy course, fine-tuning the motor and rearranging the rigging. And not until the final act will we know whether we have achieved the felicitous outcome that is the hallmark of most romantic plays, or whether the melancholy that defines a tragedy awaits us. The romantic outcome ends, as most all Shakespearian comedies do, in a marriage—in this case, a marriage of sensible fiscal and monetary policy that lifts employment and carries the American economy to new heights. The tragic outcome is one in which the fiscal authorities—the Congress and the president—are unable to provide incentives for risk takers to make use of the cheap and abundant capital the Fed has made available, and the play ends in a debasement of the central bank and the ruination of our economy and lifestyle."

-

We've had this hand wringing vortex regarding FFH underwriting numerous times on the board. The fully developed last 8 year record suggests that perhaps we forget..... From the 2011 AGM - Slides 11 and 12: Fully developed 2002-2010 ratios NB - 95.6% - redundancy 02-09 = 7.6% CF - 99.8% - redundancy = 8.9% ORH - 91.2% - redundancy = 9.6% Asia - 88.0% - redundancy = 2.6% Fairfax is very conservative in reserving. There were a lot of bad quarters and some bad years in that time frame - including Katrina. What they report in a quarter and what then fully develops are very different numbers. Far better to under promise and over deliver. The data suggests that they are very good underwriters when you factor in the under promise and final outcome after reserve release. Here is a link that has a bit of a discussion around the underwriting issue and the implications of a hard market. Within that thread is a link to the AGM slides. http://www.cornerofberkshireandfairfax.ca/forum/fairfax-financial/ffh-agm-slides-2011/msg44800/#msg44800