gokou3

-

Posts

619 -

Joined

Content Type

Profiles

Forums

Events

Everything posted by gokou3

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

(Putting myself into Goodman's shoes) "So let's see, should I screw the common shareholders (which my family owns 20% of) or the Series 5 holders? Of course the Series 5 guys. Why not give the patsies a stick and a carrot - they can either... 1) convert their series 5 shares for commons per prospectus and get a 32% immediate haircut (based on today's DC.A closing price, without assuming further price pressure from such event), or... or 2) convert to the "Series 6" preferred with a 2022 maturity at 7.5% dividend rate, AND A PAR VALUE OF $20. This would be a lesser 20% haircut, and will almost make the holder whole 3 years later after dividends. Also, this offer would be a 10%+ premium to the current Series 5 prices to encourage the new-ish shareholders and arbitrageurs to bite. This also eliminates $16M of liability in one stroke without any dilution." --------- I think the "series 6 conversion" scenario is quite likely. Of course, I am biased as a Series 2 & 3 pref holder. -

Isn't this trade a bit early relative to the prices seen during 2014-16? The high quality prefs like bce may go to 50% par again if there are signs of Canadian cb rate drop which may happen given the challenges in the oil and real estate industries.

-

WFC

-

All the posturing from the NAFTA re-negotiation seems to eventually target China, according to this article: https://www.wsj.com/articles/u-s-pivots-to-china-with-nafta-deal-in-hand-1538431208?mod=searchresults&page=1&pos=10

-

Is this a paradigm change for (northern) BC? Would the average Joe in BC benefit from this? Shell, Partners Approve $31 Billion Project to Speed Gas to Asia https://www.bloomberg.com/news/articles/2018-09-30/shell-partners-said-to-approve-31-billion-lng-canada-project?srnd=premium-canada TransCanada to begin gas pipeline construction in 2019 if LNG Canada project goes ahead https://business.financialpost.com/commodities/energy/update-1-canada-gas-pipeline-build-to-start-in-2019-pending-lng-plant-fid B.C.'s natural gas reserves double previous estimates https://www.cbc.ca/news/canada/british-columbia/b-c-s-natural-gas-reserves-double-previous-estimates-1.2417050

-

For the past few days, ENB between C$42.7-$44; BIP @ C$49.75.

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

I guess when Dundee reports Q3 the common price may turn south again... more losses at Parq, no update on asset disposals, something catches fire, etc. ::) -

Thanks for sharing. Per 2018Q2 earnings PR, "At June 30, 2018 common shareholders' equity was $2,056.2 million, or $13.26 per share" So adding $1.62 to this would give $14.88, close to the current stock price. The INR currrency dropped by 5% since June 30, but since with the successful investments in Sanmar and Bangalore airport, i think I can have some confidence in the Indian team's ability to allocate capital. For this, I just initiated a long position.

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Brookfield? They have: Hotel operation experience Casino operation experience Vancouver commercial property experience Low cost of capital Of course they won't pay high prices for it... -

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Basically Roumell is asking the company to stiff the E holders instead of the common holders. I like that. E holders have been living in a fantasy for a long while (until recently) that they would get par back in 2019. -

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Another one: http://www.cbre.ca/AssetLibrary/CBREHotels-AccomdationOutlook-Presentation.pdf -

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Additional research from JLL on Nov 2017: http://www.jll.ca/canada/en-ca/Research/CAN-Vancouver-Hotel-Market-Report-2017-JLL.pdf -

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Given the company is lacking cash, I think it's quite possible that management will offer to redeem the E at a discount to par, like $18 per pref, in lieu of converting to the common. This would lessen the dilution for Goodman and stick it to the preferred holders. -

More FCAU by going long the Jan 2020 $13 and $15 leaps.

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

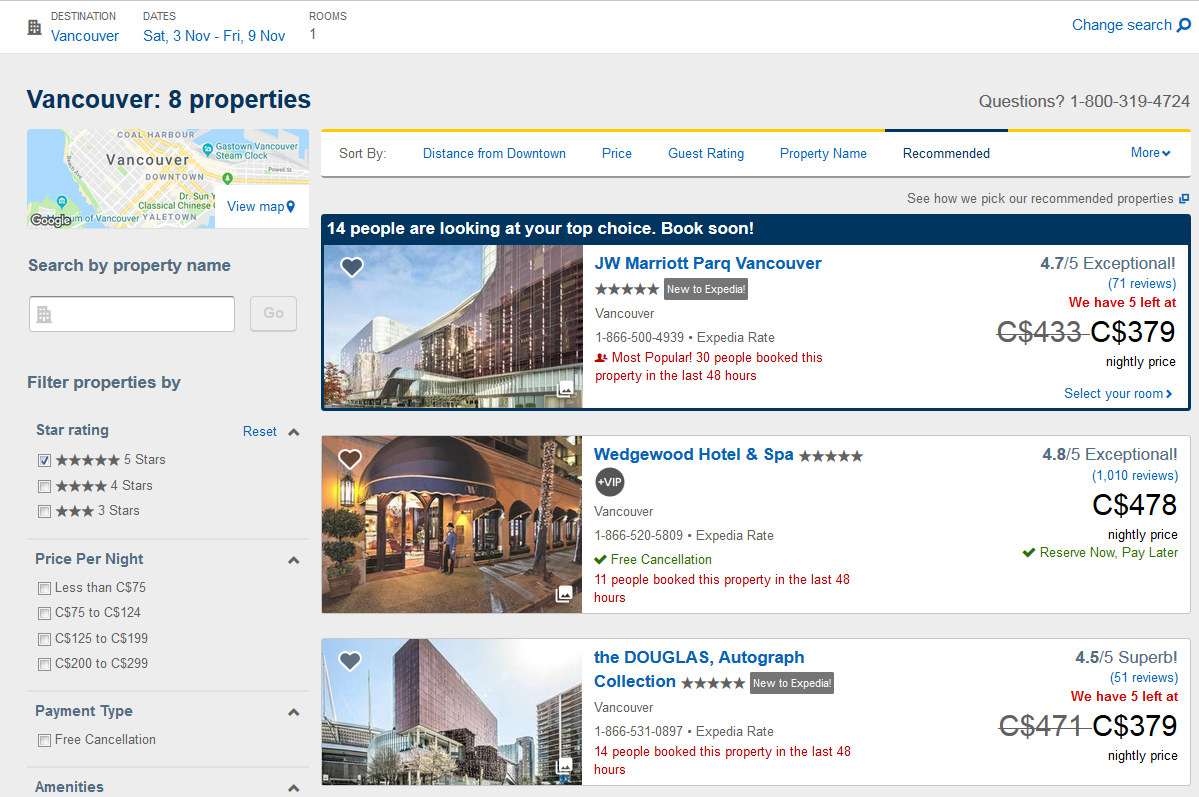

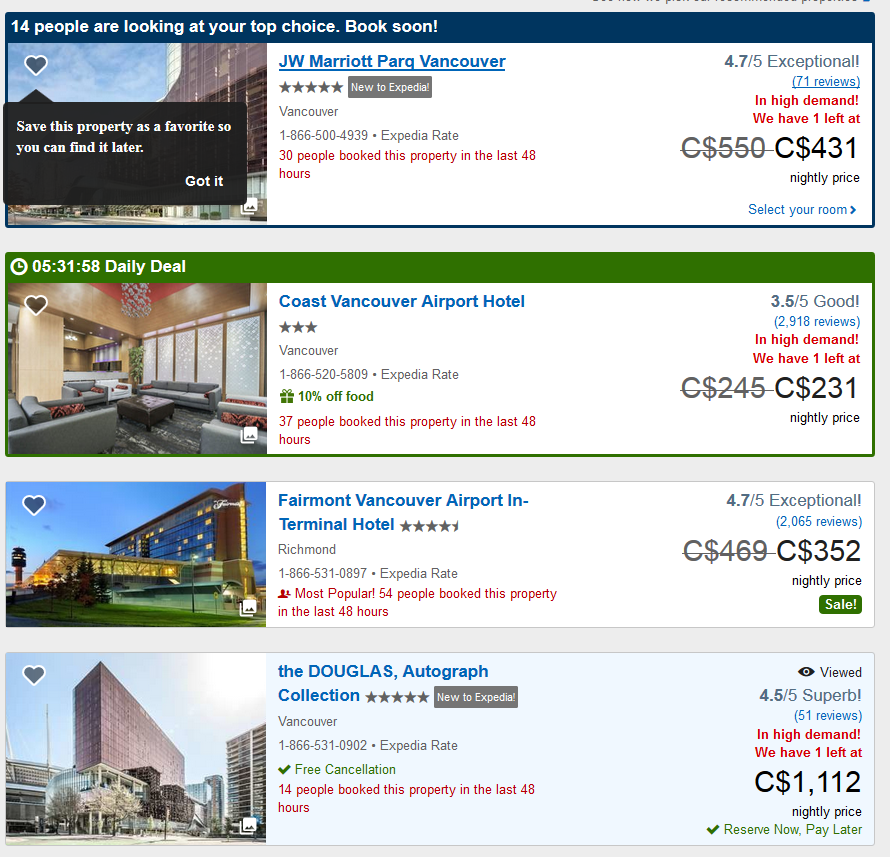

...and rates for the beginning of November, should be low season. Someone who has more experience in hotel valuations can figure out a value based on these room rates.

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Their two hotels should worth something. Here are some room rates for end of July (peak hotel season for Vancouver) - first and last ones.

-

Who is making money from struggling U.S. malls? https://www.reuters.com/article/us-usa-malls-investment/who-is-making-money-from-struggling-u-s-malls-idUSKBN1JM17V

-

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Commons. Not sure whether that's the best risk-reward investment but I find it easier to get a sense for value with common stocks versus preferreds. How do you compare the two asset classes to determine best value in this case? Or did you buy both to not have to? For Dundee, I simply do not trust the competency or integrity of the management so from a risk perspective I don't have enough confidence in the commons. The preferred OTOH offers a nice 12% dividend return (on cost) and I think it's very safe given the large discount to NAV at the moment. However, if management continues to screw around and has more writedown, even the preferred may become uninvestable. If they are able to turn around, then yes the common could provide a much greater return than the pref. -

Dumbdee - The Goodmans, The Bad & The Ugly - 30% of NAV bargain?

gokou3 replied to sculpin's topic in General Discussion

Common or prefs? -

This is insane. WW is basically in a spread business - pay long-term rent to a landlord, do something to the premise, and then sub-lease it short(er)-term at a hopefully higher price while taking all the hassles and risks of vacanies, dealing with small tenants, etc. If they are successful at it, then 1) the landlord would rise its rent at renewal, and/or 2) the landlord will copy the not-so-secret sauce. In fact, large landlords like Brookfield must be already thinking about it, per below (i think the deal has been called off since though): https://www.ft.com/content/2e670bea-e82a-11e7-bd17-521324c81e23 Does anyone know how much spread WW earns, i.e. what's the rent difference between their premises and a comparable space?

-

A little bit more BRK-B at $190

-

More PVF.UN (Partners Value LP). 30%+ discount to NAV now.

-

More Dundee preferred. DC.pr.d

-

Infrastructure costs money to maintain... and in many cases their deterioration is inline with usage.. and sometimes the cost is not monetary, but in the declining level of service. Vancouver has the second worst traffic jam in NA. Healthcare has no real additional cost? I am not sure how to respond to that.. in any case, I wouldn't want my tax dollars go to the treatments of abled people who just happen to be a resident and have never paid income tax because they are rich enough to not need to work. And for departure tax... I actually never heard of them; not saying it doesn't exist, i just don't know. Perhaps because I have never heard people paying them? When someone decides to leave for good, I am not sure if they would have the appetite to pay for a departure tax. Not like they would get stopped at the airport for not paying the tax...

-

I read sometime ago that Richmond is one of the poorest communities in BC - ranked by income, of course. Go figure. There are people who live in $5+ million dollar homes and receive childcare benefits due to their "low incomes". Their income may not even pay off their property tax. Why would one support a system where people could bring their wealth to Canada, not work for a single day here and hence not pay any income tax, and be eligible automatically for all benefits (healthcare, infrastructure, etc), is beyond me.