MMM20

-

Posts

3,350 -

Joined

-

Last visited

-

Days Won

14

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

I had to call Fidelity to tender my shares. It took almost an hour - they had to walk through the terms in painstaking detail and get multiple approvals. I'm guessing this will be enough of a barrier for many people that my chances of a full fill at $500 are higher than I thought an hour ago.

-

The Company’s purchase of Shares from a U.S. Holder pursuant to the Offer will be treated either as a sale of the Shares or as a distribution by the Company, depending upon the circumstances at the time the Shares are purchased. The purchase of Shares from a U.S. Holder will be treated as a sale if (a) the purchase results in a “complete redemption” of the U.S. Holder’s equity interest in the Company, (b) the receipt of cash by the U.S. Holder is “not essentially equivalent to a dividend”, or (c) as a result of the purchase there is a “substantially disproportionate” reduction in the U.S. Holder’s equity interest in the Company, each within the meaning of Section 302(b) of the Code, as described below (referred to as the “Section 302 Tests”). The purchase of Shares from a particular U.S. Holder will be treated as a distribution if none of the Section 302 Tests is satisfied with respect to such holder. 46 In applying the Section 302 Tests, the constructive ownership rules of Section 318 of the Code apply. Thus, a U.S. Holder is treated as owning not only Shares actually owned by the U.S. Holder but also Shares actually (and in some cases constructively) owned by others. Under the constructive ownership rules, a U.S. Holder will be considered to own Shares owned, directly or indirectly, by certain members of the U.S. Holder’s family and by certain entities (such as corporations, partnerships, trusts, and estates) in which the U.S. Holder has an equity interest, as well as Shares that the U.S. Holder has an option to purchase. (a) Complete Redemption. A purchase of Shares pursuant to the Offer will result in a “complete redemption” of the U.S. Holder’s interest in the Company if, immediately after the sale, either (1) the U.S. Holder owns, actually and constructively, no Shares; or (2) the U.S. Holder actually owns no Shares and effectively waives constructive ownership of any constructively owned Shares under the procedures described in Section 302(c)(2) of the Code. U.S. Holders who desire to file such a waiver are urged to consult their own tax advisers. (b) Not Essentially Equivalent to a Dividend. A purchase of Shares pursuant to the Offer will be treated as “not essentially equivalent to a dividend” if it results in a “meaningful reduction” in the selling U.S. Holder’s proportionate interest in the Company. Whether a U.S. Holder meets this test will depend on relevant facts and circumstances. In measuring the change, if any, in a U.S. Holder’s proportionate interest in the Company, the meaningful reduction test is applied by taking into account all Shares that the Company purchases pursuant to the Offer, including Shares purchased from other Shareholders. The IRS has held in a published ruling that, under the particular facts of the ruling, a small reduction in the percentage share ownership of a small minority shareholder in a publicly and widely held corporation who did not exercise any control over corporate affairs constituted a “meaningful reduction”. If, taking into account the constructive ownership rules of Section 318 of the Code, a U.S. Holder owns Shares that constitute only a minimal interest in the Company, and such holder does not exercise any control over the affairs of the Company, then any reduction in the U.S. Holder’s percentage ownership interest in the Company should constitute a “meaningful reduction”. Such selling U.S. Holder should, under these circumstances, be entitled to treat the purchase of such holder’s Shares pursuant to the Offer as a sale for U.S. federal income tax purposes. Shareholders are urged to consult their own tax advisers with respect to the application of the “not essentially equivalent to a dividend” test in their particular circumstances. (c) Substantially Disproportionate. A purchase of Shares pursuant to the Offer will be “substantially disproportionate” as to a U.S. Holder if the percentage of the then outstanding Shares actually and constructively owned by such U.S. Holder immediately after the purchase is less than 80% of the percentage of the outstanding Shares actually and constructively owned by such U.S. Holder immediately before the purchase. Shareholders are urged to consult their own tax advisers with respect to the application of the “substantially disproportionate” test in their particular circumstances. It may be possible for a tendering U.S. Holder to satisfy one of the Section 302 Tests by contemporaneously selling or otherwise disposing of all or some of the Shares that such U.S. Holder actually or constructively owns that are not purchased pursuant to the Offer. Correspondingly, a tendering U.S. Holder may not be able to satisfy one of the Section 302 Tests because of contemporaneous acquisitions of Shares by such U.S. Holder or a related party whose Shares are attributed to such U.S. Holder. Shareholders are urged to consult their own tax advisers regarding the tax consequences of such sales or acquisitions in their particular circumstances.

-

I don’t know about Europe but I believe pg 44/45 of the offering document walks through tax issues for US, in case that points you in the right direction generally. Apparently it’ll be treated as capital gains vs Canadian deemed dividend withholding in various scenarios that they outline. Not a tax guy though.

-

$500 or bust!

-

Prem redemption media tour has begun in earnest...

-

At this point I'm just jealous of anyone who isn't already maxed out into the deadline.

-

My main question is whether reasonable investors are even paying attention. And their tax situations!

-

One question for anyone else who might try to get cute and round-trip this one. How long does it take to actually receive the cash proceeds in these SIB processes? I saw a couple posts on the Fairfax India board that suggested the cash hadn't hit some accounts even 10+ days later, seemingly dependent on the broker (IBKR sooner, Schwab later). Anyone know?

-

Ok, so here is the part (see pg 44-45) that I think is most relevant to my situation, in case this helps anyone else. Nothing in here that changes my prior assessment of the current opportunity. Don't come for me if you get stuck with a fat bill.

-

Thanks. I definitely skimmed over that whole section earlier. Time to sharpen the pencils!

-

Got it, makes sense. BTW I just found the below on Brookfield's website. Hope it is safe to assume this applies to this FFH situation. Withholding Tax on Dividends Under Canadian domestic law, dividends paid by Brookfield Asset Management Inc. to a non-resident shareholder are subject to 25% withholding tax. Generally, the Canada – U.S. Income Tax Treaty will reduce the rate of dividend withholding tax from 25% down to 15% for a resident of the United States. Where the U.S. resident owns the shares of Brookfield Asset Management Inc. in a 401K, IRA or similar plan, the Canada – U.S. Income Tax Treaty will reduce the rate of dividend withholding tax to nil. https://bam.brookfield.com/stock-distributions/tax-information

-

Got it. I know you are not my tax guy, so feel free to ignore this. But that is an issue only for Canadian residents, correct? Or will they come after USA residents if done in a taxable account? Sorry if this has already been discussed here.

-

I might also be too dumb too understand what’s happening here. Usually when I think there's blindingly obvious opportunity to pick up big alpha, it turns out I was just missing something. Why shouldn’t I load up at $450 and, idk, maybe buy some TSX puts, to tender in <10 days? Why shouldn’t I go full Munger and sell all my BRK, index funds, etc in my retirement accounts to raise as much capital as possible for what will almost certainly be a ~10% return? (famous last words, i know) This now feels like a repeat of the Fairfax India SIB where there turned out to be a big opportunity to load up and tender right before the deadline. Is it not obvious based on the funky shareholder base, tax incentives, low trading volume, still-near-all-time-low valuation (even at the high end of the range), etc., that the tender will almost certainly happen at or close to $500? A la $14.90 with Fairfax India not even 6 months ago. Unless the world falls apart over the next week, I guess? Is it simply that the bank prop desks are dead and everyone’s pulled money from the arb hedge funds to buy more FAAMNGTklsjgs? Are flows around the Fed decision (and/or insurance specifically with the tornadoes?) really just pushing this down to $450 when $480+ would clearly make more sense? Is that you, Mr. Market? I'm not afraid to pick up free money if I see it. Just want to be sure I'm not picking up nickels ($100,000 bills?) in front of a steamroller. Where are the arbitrageurs? What am I missing?

-

Maybe it’s naive but I’d be much more concerned about the Fed if FFH was already trading at 1.5x book.

-

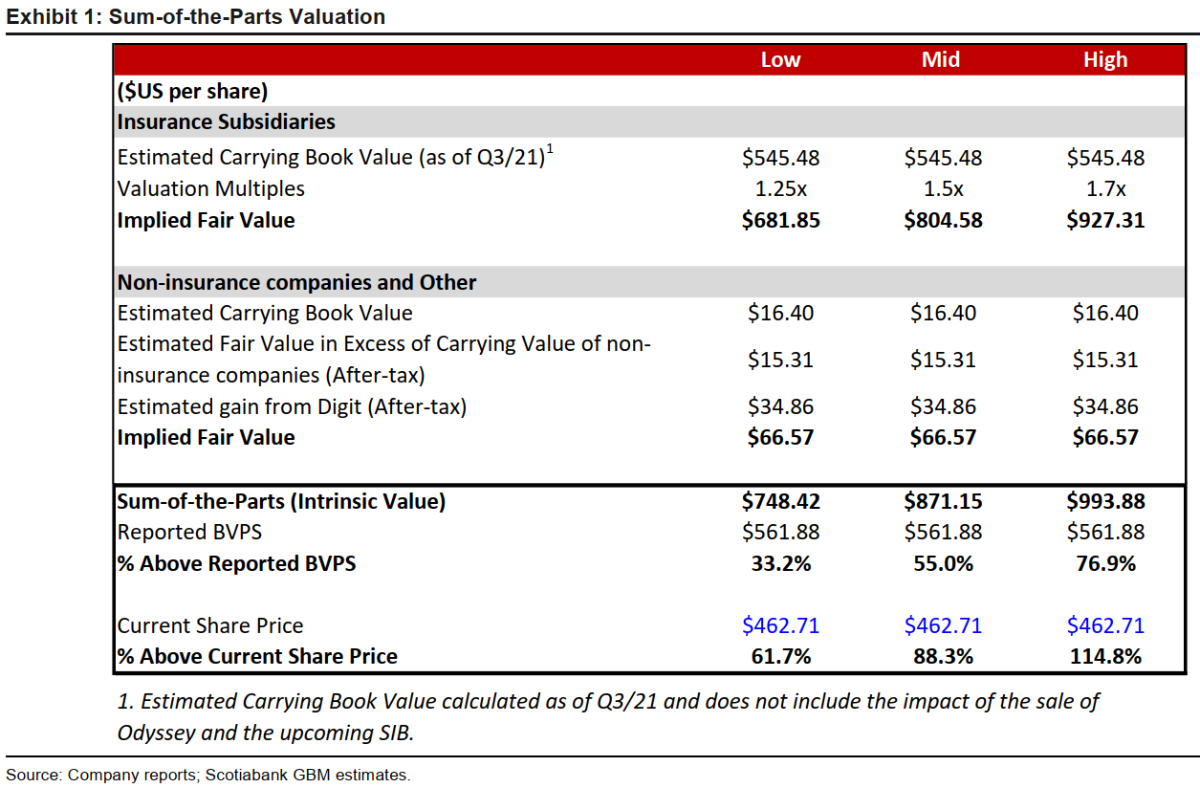

FWIW, sell-side seems to be getting more, I don't know, realistic? Earnings exploding, valuation on any metric still near all time lows, and now Scotiabank says half of intrinsic value. Can the momentum traders pile in now please?

-

Got mine from Fidelity today (Schwab and TD last week)

-

Plus I wonder if the technology ultimately gets commoditized and drives down insurance pricing across the board to the benefit of customers but not necessarily Fairfax. Too negative? Maybe they can cash in first...

-

Agreed, but why not give them full credit for their ~74% of Digit, so more like $100/share there alone? Why discount it so heavily? b/c Indian markets running hot? What am I missing?

-

how do you account for something like Digit in this framework? I know they are just now (supposedly) flipping to break even so no major contribution to look through eps, but I feel like it could be analogous (on a much smaller scale I admit) to leaving out aws from Amzn valuation years ago. it’s more ‘explosive growth high tech investment’ vs ‘new insurance subsidiary’ IMHO. I truly still can’t believe there is this 15x investment, $2b+, now-also-sequoia-backed hypergrowth long runway type of investment inside fairfax. feels like it’s still under the radar and needs more attention and some consideration in all SOTP-ish valuations til proven otherwise. maybe the answer is just that FFH is truly now worth 1.5x bv?

-

Seems like a not-super-improbable upside scenario in which FFH BVPS is up ~$30-50/sh (?) next year from this alone

-

VIC write-up on Eurobank by miser861, who I believe is Quincy Lee of Ancient Art/Teton Capital (check out the Santangel's Review feature on him from a while back). Will this turn into a big winner for Fairfax? Hey, would be nice. https://www.valueinvestorsclub.com/idea/EUROBANK_ERGASIAS_SERVICES_A/7217319524 "So once this train wreck is cleaned up, we have a bank that trades for .6x tangible book value. It’s not the cheapest the stock has ever been, but it’s the closest it’s ever been to resolving its balance sheet problems. I don't want the whole fish, I just want the fillet. It’s earning €1 billion of core pre-provision pre-tax income. In a recovery year I don’t think it’s crazy to assume 1% provisions per year (€380 million). So Eurobank could earn €.13/share in a year or so. So today it trades for 6.5x one year out EPS. It seems possible that the stock could double in a year or so. And I think there is good downside protection from the low price/TBV and the trajectory of NPLs, and a likely recovery in tourism. I’ve thrown out a lot of numbers but the bottom line is this. There’s a rotation into value going on. There’s nothing more value than Greek banks. Greek banks were value before value was cool."

-

Agreed, added today too. Maybe the smart move is to size up FFH to the point it’s borderline uncomfortably big and also buy some OOTM puts on a broad index to hedge the ‘world falls apart’ risk

-

True, I'm assuming it'll be undersubscribed. i think that's a fair bet but of course won't necessarily be the case.

-

Makes sense. Only question is how we handicap the risk of a material modification to the terms at this point? I know deals break all the time in sharp down markets but I have a hard time seeing that here unless things truly fall apart over the next few weeks. But stranger things have surely happened. I own a lot (for me) and plan to hold for a long time. But might size it up even more for short term trade.

-

With odd lots first in line, why wouldn’t I tell all my friends to buy 99 shares at <$450 to tender at $500? Of course the deal could be modified but seems like the closest thing to a guaranteed 10%+ return I’ve seen, admittedly not necessarily scalable!