MMM20

-

Posts

1,870 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by MMM20

-

I think this is in reference to my post. So, round numbers, FFH is up 15x on Digit. It now represents ~20-25% of FFH's market cap. Digit is growing like a weed in a huge and rapidly growing market. Dyed in the wool deep value guys like Prem and his loyal followers are notoriously terrible at recognizing this sort of opportunity. Ironic then, isn't it, that nearly 3/4ths of Digit's ownership happens to be embedded in FFH? What if Digit does, in fact, have a better mousetrap and ends up a massive low cost operator in the not-too-distant future? Where might that put the Digit piece vs. the hypothetical FFH stub? Maybe it ends up just a thought exercise but my point was that I don't dismiss the possibility of it playing out that way, especially after Sequoia's investment. And yet FFH trades at an all-time low valuation. Fun. I'll take the gift from Mr. Market and see how it plays out.

-

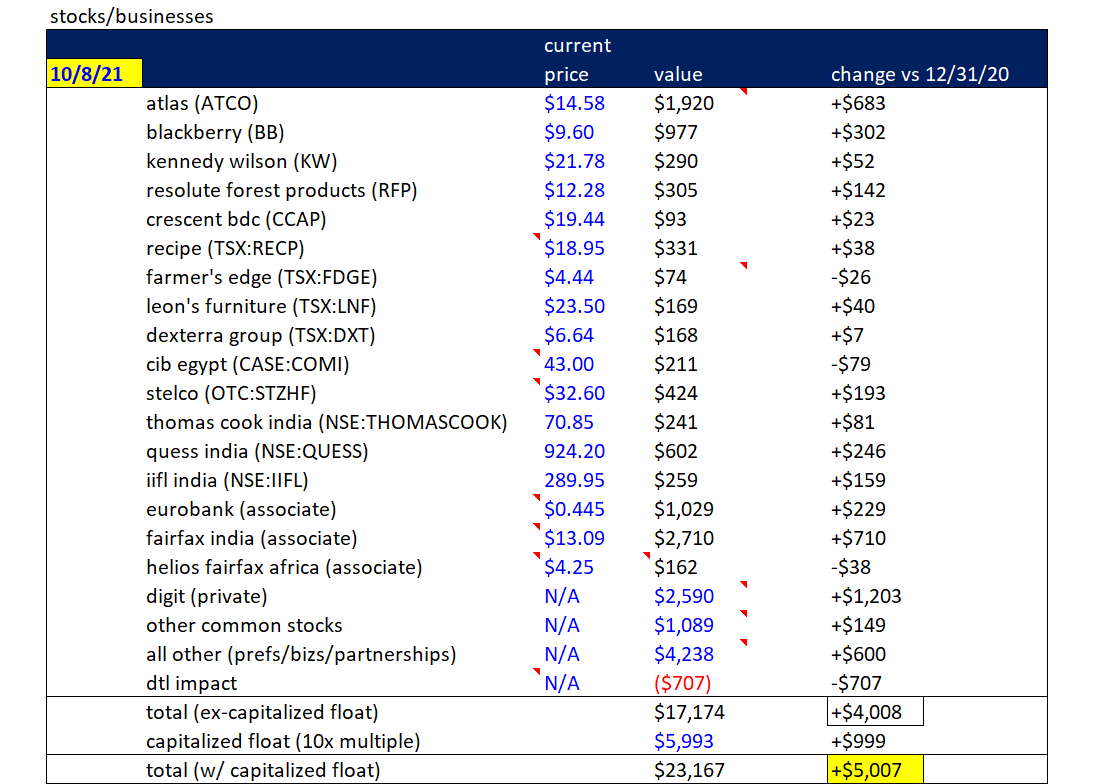

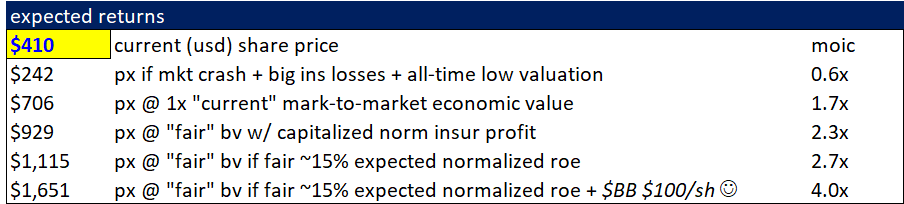

Hi all. I'm new to the forum and to deep diving on FFH. I've followed it on and off for 10+ years but took a hard look after the whole BB situation and Sequoia's investment in Digit. By my math, FFH's underlying stock/business holdings are now +$4B vs. 12/31/2020. And giving them credit for the capitalized value of growth in insurance float, maybe the uplift is +$5B to the equity at this point. (Obviously much of this has not flowed through to the reports - I'll just note that pro forma BVPS growth over the trailing 3/5-ish years is actually quite good adjusting for the yet-unreported performance, for what it's worth to the algos among us.) The Indian investments including Digit represent well over half of the current market value now. Even if 0.8-0.9x P/B is fair, that's a +50% from today on the marked-to-market book value. And do we have a potential Naspers/Tencent redux on our hands with Digit? I'm not sure how to handicap that, but it seems like a real possibility. From a starting point of an all-time low (post-9/11) valuation, the risk/reward seems skewed to the upside with that sort of optionality built in. How do we think about the true share count? Would it be fair to include the TRS effectively as a buyback in our modeling? This would give us a current share count of ~24.4M, right? That gives me the following range of outcomes (bear with me on the last line): It must have been tough to be a FFH shareholder post-GFC. I understand why plenty of shareholders are not happy. Here's hoping that the ability to bring fresh eyes to this situation is an asset. Appreciate the helpful discussion. Thanks all.