scorpioncapital

-

Posts

2,780 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Posts posted by scorpioncapital

-

-

"The couple has high expenses including eating out, transportation and music festivals, but, according to the host, there is no way they will change those things"

I think there is something strucurally wrong with the society if you can't do these lifestyle things and still have a home.

-

On 7/14/2022 at 7:22 AM, bizaro86 said:

Bank of Canada raised 100 basis points today and the Canadian dollar barely moved against the USD. I'm not sure what it'll take for the USD to meaningfully weaken. I would have thought the news about China/Australia doing an iron ore deal in Yuan might have hurt the USD.

I think there are some strange issues with how each country can set their rates.

Look at the margin rates at ibkr - https://www.interactivebrokers.com/en/trading/margin-rates.php

Notice the cad rate is 0.5% higher than the US rate. After a 100 bps hike. And US will hike 0.75 to 1% next week.

There seems to be some mechanism issues in the actual market rate vs what the central banks are targeting? I wonder if this may be the focal point of the next crisis where some bank sets a rate of x but they can't get it within some % of x?

-

You have added alot just by suggesting a basket approach. This is key if you want to do it safely since there is an expected positive payoff. I am not sure if you can have a case of this time is different where the traditional majority of deals closing suddenly break not according to statistical history. I believe even the pandemic did not lead to such a result. Another way to think about it is to position size quite small if your goal is simply to say preserve your cash. At the current time this would require around a 5-10% annual return from this operation. So you can work backwards from that goal to find out what position sizes and spreads you'd need to top up your cash. I am not sure if this entire operation is better or worse than holding a TIP etf however.

-

I sort of agree. By making unemployment go up a bunch, productivity down and gdp growth stagnate the CB would be sending a political message that the government needs to wise up. However, the backlash (since the people and government control the government presumably) tends to create populism. I am not sure a cb can be independent in a democracy if things get bad enough, they'll just vote themselves into a banana republic!

-

"Lots of people are in shock right now. Most felt that with all the debt being carried by consumers in Canada there was no way the Bank of Canada would be able to increase interest rates like they have been doing"

Unlike the USA, BofC has a sole, not dual mandate. I interpret this to mean, we have no problem to run our population into the ground in a massive recession as inflation is the only mandate. The States has to balance unemployment with inflation to some degree. Of course the mandate may change and/or the inflation target may be moved up. Read an interesting opinion in WSJ that to avoid a recession the US (and probably Canada) would need to raise the inflation target to 4%. Of course that also means your money is wasting away faster.

-

From a theoretical angle, is it better to invest in commodities or value-added companies that sit slightly above the commodity layer? Or even higher? Is it better to own an oil stock, a semiconductor stock, a cloud infrastructure stock, or an app on that infrastructure? Is abstraction more profitable? Or perhaps the division should be recurring revenue versus capital goods one time sales?

-

20x in like 150 years seems rather slowish. I mean its all great from a detached pov but if you somehow live or seek to live off wealth it has to happen faster I think. More like Microsoft from mid 80s to today. That's why growth is always prized. I never believed in value stocks even under high inflation, of course a high growing value stock is the gold mine if it can be found.

-

2 hours ago, randomep said:

ok I am shocked that someone on Cobf would compare Cathie Wood with Burry, but ok..... I won't argue your view that whoever manages more money is more wise.....

Why not? Since inception around 2014, Woods has outperformed Burry, even with this year's steep loss.

-

Personally I don't think he's very wise. 200m may seem alot, but Cathie Wood is running 23 billion.

-

3 minutes ago, Spekulatius said:

Just a reminder that an interest rate of less than 2% has never caused a recession by itself. Even a raise buy 2-4% onkly causes a recession ~35% of the time.

So i think the Fed can raise a bit from here and likely won't cause a recession. Now that does not mean that a recession does not occur for other reasons. technically we could be in one - because the 1 st quarter inflation adjusted GDP was down already - but that was because Q1+Q2 2021 were monster quarters with >6% GDP growth. So I guess it's a tough comps recession that most people won't really notice.

If raising 2-4% causes recession 35% of the time,

and we have raised now 1.75% total (from 0%),

and we are in recession (seems likely 2 negative GDP quarters or close)

then we can conclude we are in that 35% of the time.

Even more scary it is below the 2-4% raise traditional range - probably due to massive global debt.

This suggests to me we will get less and less raises, and catastrophic financial disasters at lower and lower rates.

negative rates seem they are coming with cbdc? )

-

such small positions. a few million here and there. he's not very rich is he? )

-

33 minutes ago, Gregmal said:

Why would a saver be pissed though? No one is entitled to returns. How is that any different than someone feeling entitled to a return on their stocks? Especially if you were told early on, that there would be no interest?

It’s such a weird thing I’ve heard over and over. Savers got screwed. I should have been getting interest. A “tax” on savers. Huh? Ever hear of capital allocation? If you were told rates would be low, who’s fault is it really?

They should tell everyone when the market goes up - exact date and time, and when it goes down, timestamp too. Rate changes and amount. That way we can all have our guarantees ) But seriously, hyperinflation and inflation only works if covert. It must be definition be deceitful.

-

is the thesis here that low inflation suddenly makes all stocks more valuable again (or, to be less politically correct, overvalued again)?

If inflation averages 4% instead of 2% for years and years, I would imagine p/e multiples will not get so out of hand, and may even be subdued, putting a ceiling on prices that have been very high for the last 20 years

-

You know I used to look at stock charts from a few decades back and I saw periods where the stocks literally flatlined...for years if not decades. It was uncanny. I wonder if something like this can happen again. If you look at these charts its like flat for 20 years and then everything shoots up.

-

1 hour ago, crs223 said:

fewer abortions => bigger labor pool => lower inflation

if so smacks of desperation.

-

Viktor Shvets at Macquire thinks not just payments will be disrupted but the entire concept of banks. He thinks banks will have no reason to exist for the allocation of capital into the economy when there is CBDC. I see scary disruption in every direction. Heck, I even see disruption in fields that haven't even started yet really! like gene sequencing. i see a gaggle of competitors on the heels of every industry, new or old. This is scary times for moat investors because if the value of moats all flatten to a pancake then perhaps management efficiency becomes the superior variable. This would seem to argue for lower interest rates across the board though. It seems that the entry of competitors may be somewhat sensitive to economic variables therefore the more recession/inflation /etc..there is, the harder it may be for new things to get entrenched, favouring the moaty stocks like visa/mc.

-

6 hours ago, Parsad said:

Yup, totally agree! Cheers!

seems like everything is getting cancelled. cancel culture has come to stocks!

-

could it have something to do with ability of people to live in other places or even outside the country?

-

"$15,000 - Pre-Tax Investment look through"

Look through earnings would seem to be represented by the change in unrealized/realized capital gain/loss declared each year. Otherwise, how do you access these funds , as they are internal to the company. Even if they do buybacks, it still shows up in carrying value.

-

22 hours ago, thepupil said:

So bills did yield 7% in the 70s? I am not sure if holding cash in a money market won't eventually get to be a return (almost) the same as a i-bond or any shorter term bond. But the escalating phase takes some time so maybe that is why people buy a TIP or 2-5 year bond, trying to time the rate of acceleration of rates.

-

"Even in your example of Venezuela, the real purchasing power of the money invested in stocks was falling rapidly even as share prices climbed vertically. You'd have been better off holding foreign currencies outside of a bank and gold. "

I don't know the situation but do you mean the stock rise was less than the currency devaluation?

What you write sounds sinister. Almost makes you want to take even a 50% stock drop to get rid of it. I suppose if you buy the stocks after they get knocked down you get real earning power which has to be more valuable than gold but perhaps less so than immediate needs like housing and food.

How do you know WHEN the inflation is coming to an end to buy though?

In a scary inflation would renters feel worried? Can you hypothetically get a case where all landlords evict everyone and retake posession for themselves? Presumably governments will enact laws and the worst case you need more worthless money to rent housing. If you don't have the extra money not sure what happens. Perhaps homelessness and poverty are a consequence of inflations. Then the homeless squat on properties, violence, real end of civilization stuf.. More likely the government via populism will expropriate the real property to give to those who can't keep up. What happens though when the entire middle class can't keep up? Seems inflation really leads to dog eat dog world.

-

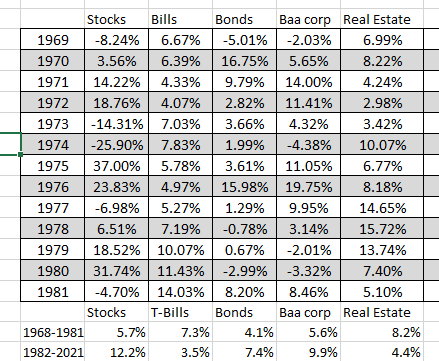

" the persistent inflation of the 1970’s was terrible for most equity investors;"

Honestly I do not understand it.

Hyperinflation is very good for stocks. And where is the line between run of the mill 20% a year inflation and hyperinflation? Does something flip at some point to make the 70s result become its opposite in hyperinflation?

Venezuela had one of the best performing stock market of all time. Vertical. All assets, even financial, should skyrocket under high inflation. Of course the society may fall apart and everything confiscated but it seems even under this threat at least stocks do very well (although the currency is trashed and you have to sell your stocks for local currency).Or was something else happening in that 70s article? Were interest rates rising by any chance?

Also shouldn't we look at the 70s experience as a continous process. Sure there were gains after in the 80s but people who held from the 50s and 60s probably got clobbered on the 25 year downside. The sp500 was flat from 1968 to 1991 i think. That was all due to higher rates compressing multiples I imagine. Am I to understand that inflation accumulates stock gains by front-loading them and when the Fed 'fights inflation' , the front-ended gains (often called a bubble) are reversed, causing the index to revert to the level it was many years before??

-

On 5/20/2022 at 4:42 PM, backtothebeach said:

And Markel's stock portfolio is 13.5% Berkshire.

so a buyout would be a 13.5% brk stock buyback? )

-

To the claim that stocks did poorly in the 1970s I saw an article on SA where the author says that stocks actually doubled during the 70s. It was the high p/e tech stocks that did not do well. So it sounds to me that the forces of inflated gains in earnings does not fully offset the high prices of leading companies if the inflation is high enough. However buying cheaper stocks throughout the period did not do so badly.

Oxy Pref

in Berkshire Hathaway

Posted

Wonder why he is slowing down the buying even though it is within his juicy target range. Does it imply not 100% confidence in a full buyout? Another reason? No rush because range-bound? No desire to go above 20% ever?