changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Too much focus on Fed balance sheet this is kind of financial instrument game which has some but very little effect in the real economy sure it can blow out mortgage rates for a time, cause liquidity issues in this particular market etc……but the main show is inflation and inflation is a real economy phenomenon..….…….see the Fed doesn’t buy or sell cars or order dinner in the real economy……..folks need to remember that……….it buys/sells or allows to roll off financial instruments like MBS’s it holds which go into or out of other financial instruments…….….sure, OK, when it buys Treasurys from the government and the government sends it to people as per 2020 I’m really interested (debt monetization) and it matters cause folks take those cheques and buy REAL things in the REAL economy……….this MBS stuff is a side show now & a rounding error in the context of the wider broader American economy in its totality……..2021 there $23 trillion of spending….…..of which about $16 trillion was private sector consumption. As I’ve explained….….the issue is nominal spending & income increases in the economy relative to aggregate productive capacity in any one year + productivity growth….….the delta of which is…..inflation So where is the too much money coming from? Well its coming from pay increases workers are receiving 6-8%……problem here is you can only eat what you PRODUCE (productivity)….go back and look at my widget world example a few pages back……….in widget world you can give workers nominal pay increases but NOBODY gets to consume more widgets without more widgets getting made…..NOBODY!…..the nominal numbers change around but so what…….well not so what…..it hurts those on lower incomes as they’ve less shock absorbers built into their monthly income. The second source of inflation is credit or more precisely the private sector banks/non-bank lenders creating money, giving it to people…who then go and spend it in the real economy. This is real….way more real than the Fed & financial instrument chicanery…..a consumer applies for a loan, a bank creates a loan……that loan is used to demand products and services in the real economy……it increases nominal spending today/right now…….but again money is just paper……productivity is what matters……too much paper (via credit creation & wages increases) is chasing too few goods. Again, same as nominal pay increases, you can’t eat credit……you can only eat/consume what you produce and no more. End of. Here we are months after we’ve talked about this ad nauseam……with folks claiming that we are near the end and the pivot is near and the Fed needs to stop……..yet credit remains a bargain!!!!…….. even mortgages at 7%……when you adjust for CPI/C-CPE the real interest rate is low, very low. Lots of personal line of credit offers I get bombarded with are great deals……as they sit below CPI for sure…..a lot below CPE……..its free money…….but money is never free……you can’t eat money…..only productivity…….and until the abundant credit creation & wage increases moderate significantly……inflation is going to persist. You moderate credit creation by raising its cost…..the Fed has a ways to go…..as Jay-P said himself.

-

The incremental point is those charts everybody has seen on growth vs. value spreads etc being the widest they've ever been in decades.......well mean reversion is a bitch (if you believe in it)....how is the reversion going to occur then between these assets.......well the way the spread is compressed back to normal is that growth/higher multiple/low FCF yield stocks contract.....all the re-rating travel is going to occur in these assets.......they are ultimately part of the same conversation around a normalizing of rates...talk of the 10yr/30yr......which is to say these equites were levered long plays on low inflation/low rates/zirp & there is a strong argument to say that we have exited that era given the (1) reemergence of real inflation post-GFC/C19 cumulative stimulus (2) future inflationary forces discussed ad nauseam. How does value outperform growth over long cycles? Answer.......investing is a very long movie with lots of twists and turns and where 'growth' in Act Two looks like the hero of the tale.......problem is in Act 3 'growth' gets murdered......& 'value' emerges from the supporting cast bruised and battered but alive........the unlikely hero as the end credits start to roll and its outperformance crown is restored

-

For sure listen 8% CPI……moving down to 5% is a mathematical certainty….it’s the journey from 5% to 2% that’s the problem & mystery for 2023/24

-

Consistent with my previous posts on what I watch but contra to my persistent inflation thesis - wage growth in October BLS moderated and annualized it indicates a deceleration on MoM increases which is positive......one month doesn't make a year but I think this is indeed positive re:wage-price spiral fears & what you would expect to see in an economy moving back to equilibrium in response to demand side moderation. Danger as I've noted and I'll be watching this closely is with still strong JOLTS heading EoY.....early 2023 BLS wage data might see a re-acceleration from a large re-setting of salaries across the economy as employees get 2022 CPI incorporated into 2023 comps. This is the problem with inflation.....it can in any short period have been 'fixed' in MoM data......but humans don't think in the present.....we extrapolate the past. Lets see this is positive for the return of price stability but very nascent and early sign of progress.

-

Not a clue - Japan is a mystery to me in terms of what they've done and for how long.

-

True

-

Ironically Liz is not helping here, not that she'd know........the Fed only effects the short end of the curve........politicians like Liz & expectations around fiscal discipline or lack thereof effect the long end.....ask the other Liz, the one they kicked out of the UK about that one. Congrats in your own modest way Elizabeth Warren you've probably contributed to a tightening of financial conditions.....the opposite of what you intended.

-

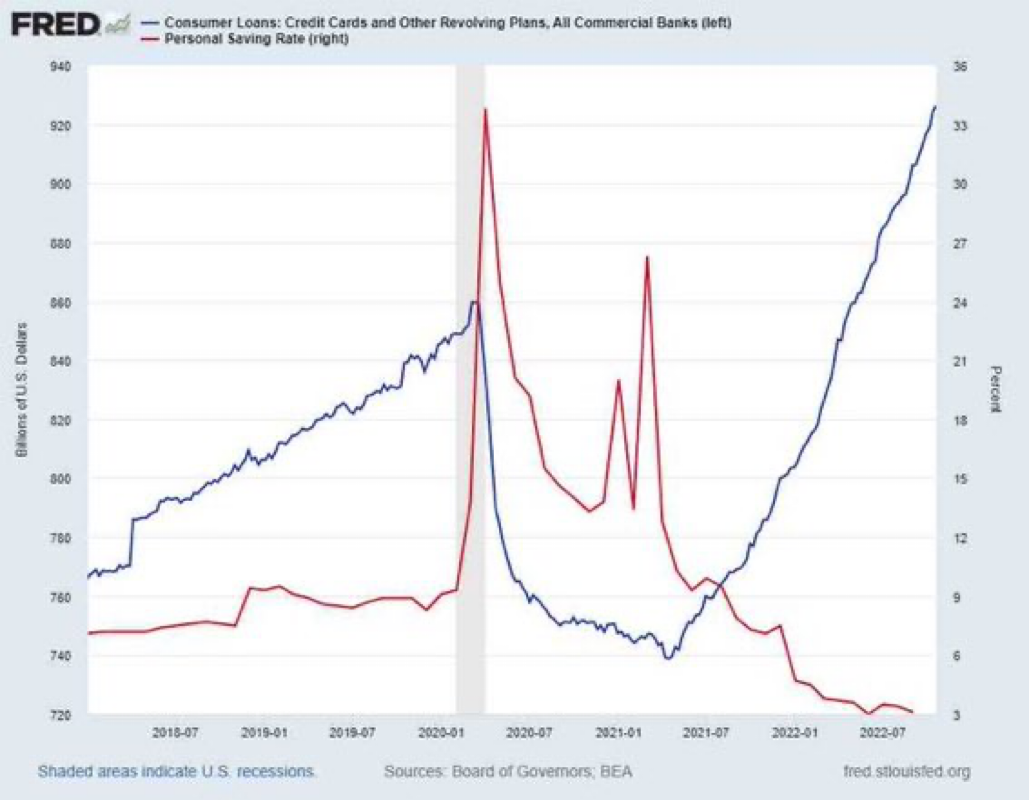

JOLTS data not good - thought best case end of 2023 we could see some rate cuts........suspect its easily 2024 now......American consumers ability to access credit once savings have been exhausted is quite something to behold......ironically stuffing the banks with so much capital post-GFC, while also training bank customers for a decade plus not to expect any interest at all on checking/savings accounts, means the problem the Fed has is that much harder.....the banks have the balance sheets & little pressure to raise deposit rates.

-

Yep to fix inflation you ideally increase productivity & temper nominal income/spending growth at the same time.......eventually you bring things back into equilibrium (or for a time more precisely slightly below equilibrium (slack))......this restores price stability.........I've seen almost no attention to the productivity trap the US is in right now (this is a job for the fiscal authorities & they are too busy fighting with each other)............therefore to 'fix' inflation all the heavy lifting needs to be done by the monetary authorities.........who through tightening financial conditions eventually effect nominal spending/income to create the desired slack in the economy to bring it into better alignment with aggregate productive capacity.....the unfortunate thing is it generally actually requires a period of negative dis-alignment to get the desired result........you and I might call it a recession.

-

Recession & job losses is a feature not a bug.......if they do this right......they will sit patiently with higher rates at their terminal rate of say 5%.........at the exact same time that the economy is printing recession numbers & unemployment is rising MoM towards 5-6%......this is how you actually kill inflation......now I know everybody is used to weakening numbers leading to cuts.....that is not how this cycle will work.

-

We're the US government and were here to help, we've got your back..."we" are going to defeat Russia................8 years later: I'm not absolving Russia of its sins, they have many.......but when your a mouse (Ukraine) and you sleep in a bed with an elephant (Russia) you have to remember your a mouse cause when the elephant rolls over it can kill you. The West made Ukraine forget it was a mouse and it started picking fights with the elephant & it got wrecked in the process. Take that video of John McCain..close your eyes.....now imagine a Chinese John McCain Xi down in Mexico rallying Mexican troops like that.........yeah you got it, you wouldn't stand for it Jaurez would look like Mauripol does today in about 15 minutes flat.

-

Agreed - but is 'the West' completely & utterly blameless as it pertains to lets call them the tensions between Ukraine & Russia that have ramped up over the last decade? Do you think we might have egged them on, encouraged to play rough with Russia to 'poke the bear'.......as John Mearsheimar rightly says anybody looking at Ukraine since the end of the USSR see's a country being led down the primose path by the West....as he predicted in his 2016 lecture on the subject such encouragement could lead to Ukraine being wrecked. Its quite rare in social sciences like international relations to have theory, prediction come true so precisely (lucky maybe but it shouldnt discount what he said back then, it should enhance its message.) For those whose's knowledge and understanding of Ukraine began in February 2022....you possibly believe the Western propaganda narrative which a great many people do that I speak too.....which is Vladmir Putin woke up in February 2022 having spent too long alone in isolation in the Kremlin, terrified and afraid of COVID (possibly terminally ill) he went crazy and decided to become Catherine the Great......to re-build the USSR by invading and taking over Ukraine with an army so small (190,000 troops) it could barely occupy & hold a city the size of Denver never mind a vast country like Ukraine. This is the myth we tell ourselves in the West.....the truth is too complicated and full of hubris & stupidity to be told to the masses.

-

Agree. Forget their past stupidity in keeping the purchases up and rates low in 2021. All we have is now and the future. This Fed is saying the right things, right now…..I commend the language…..the references to the risks being around doing too little versus too much are 100% correct…….folks are in for a surprise next week with all this pivot bullshit…….the screams of pain in the economy, mainly via unemployment haven’t ticked up yet to justify a pivot….a slowdown in 75bps hikes to 50bps, sure but when did that become a pivot? I’ll tell you when…..to institutional sales people getting on CNBC desperate to hold on to your 401k, IRA moneys no matter what happens …..heaven is only around the corner if you can stand the pain folks …..there is nothing to pivot away from as a central banker……yet…the equity markets down 20%, who gives a shit……...if the past is prologue…..spineless central bankers chicken out (pivot) too early….and only in the face of inevitable unemployment numbers ticking up…and unfortunately too early to slaw the inflation dragon ….let’s see what this crowd do. It’s a dastardly job being a central banker in an inflationary cycle…..everybody hates your guts, literally everybody. The average human being crumbles under such exogenous pressure.

-

Good stuff & instructive…..everyone should be careful when your nationalistic underbelly is tickled by dim witted politicians desperate for a vote…..especially ones with more years behind them on this planet than in front of them……..autocracy versus democracy…….good guys versus bad guys….cowboys and Indians…….give me a break…to believe it is to betray a lack of understanding around the way the world really works…to not understand Nazism is to not understand how a nation of rational people can be turned into murderers….Nation States have interests…..chiefly their own survival & safety……the United States isn’t in Tawain cause we’re good guys……we’re not in Ukraine because we love getting our Presidents crack head son board seats on gas companies….I’m sorry to say we aren’t even there to spread democracy and freedom thru some ill conceived social engineering experiment that has damn near failed in every country the West has attempted it in…….we are there because we want to contain & hold down States, in this case Russia, that we perceive come even close to us in terms of a threat. See the United States knows well the playbook, you first become a regional hegemon in this case the Western Hemisphere (for example invade Canada (1775, 1812), then Mexico (1846)……exert your regional dominance, become the neighborhood bully, get to be the 800ilbs gorilla in your hood…….once your firmly in control of your region as the USA was in the early 20th century……your free then, if you wish, to meddle in other regions such that no states there could ever conceive of having the scope/capacity to meddle in your region….Middle East, Asia etc…… The big error being committed in Ukraine is the usual bullshit social engineering escapades the USA gets involved in ad nauseam, that always fail, and this is its usual cover story, for what is a containment strategy for Russia which uses spreading liberal democracy as its Trojan horse. I dont see the USA desperately trying to spread liberal democracy into Rwanda…..no crack head sons are getting sent there. The stupidity out there comes from believing that Russia actually needs to be contained. Russia is not and will not be anytime soon a peer competitor. For God sake, they couldn’t even topple a weak country like Ukraine. What kind of threat is Russia to the might of NATO/USA. The real threat is China, which overtime my guess is will begin to look very much like the United States did in the 1800s, invading other countries no.1 Tawain and exerting its regional dominance in Asia, so that it to becomes an undisputed regional hegemon in Asia. The USA doesn’t really give a shit about Asia…..what it gives a shit about…..is it knows, better than most ever could, once you become a regional hegemon it frees you up to ‘play’ in other regions of the world I dunno like the Western Hemisphere!

-

You’ll notice I don’t speak about current CPI, and also we could spend all day talking about Core PCE…all the ex-energy good stuff….I’m aware of your nuanced point, I know MoM data, I’ve seen it…you’ve cherry picked CPI you know that is (1) the wrong /most favorable measure ….….but it even CPE also as a data set has tonnes of head fakes as you well know, base effects, FX / $ strength. You’ll notice I never talk about CPI/CPE…..I only ever reference in any real sense nominal spending/income growth….I always speak about non-farm payrolls increases annualized against productivity growth….the BLS data & productivity data is where one should look…most folks don’t get it so I use the word inflation as a proxy/shorthand…..THIS place…..is domestic inflation…it gets to be a like a rash too….it flares up and flares down….I predict another flare up in Q1 2023 BLS data as wage increases negotiated now roll thru….annualized CPI and even CPE are kind of poor proxies for the direction of travel…you have to go up cash flow statement of the macro economy as Dalio/Bob Prince/bridgewater do ….income/spending growth against productivity this is where the devil is for those who wish to look at him……one man’s spending is another man’s income..,..,you can only eat/consume incremental productivity gains….you do not get to eat/consume incremental nominal increases in spending/income..there are no free lunches as anybody who works in finance knows

-

Like the analogy…lets continue with it……..problem with the drug is the half life of increasing nominal spending growth way above productivity is very very long………..once enough of it is administered for a descent period of time (as we have had)……the thing you miss @Gregmalis its extended half life comes from it being incorporated into ALL future contracts of all kinds being negotiated today….wage/construction etc etc…..example railroad union negotiations like Druckenmiller pointed out…they aren’t using forward 5/5’s at negotiating table…like fuck they are….nobody is…..they are doing what humans do….. extrapolating the recent past out into the future and the workers right now have LEVERAGE cause of full employment……https://raillaborfacts.org/news/bargaining-status-faq-2022/…..this railroad deal ain’t going away in 3 months…or by Q1 2023…..right? It’s five years long! My final insight for today, then gonna run so excuse no replies…..in the context of inflation expectations….which for a while I hung on to as a sign that I might be wrong and your thesis @Gregmalcould be right….that this inflation thing was short lived……and would just ‘disappear’ super quick without the Fed even getting going……was that inflation expectations remain anchored in surveys….but as Stan pointed out….that’s the future….I’m walking into my boss in two weeks….I’m not talking about the future, till we settle up the past…..I want 2023 comp to incorporate 2022! CPI….then we can talk about an increase on TOP…..and word on the corridors is we are gonna get CPI+, no problemo. Remember though the widget factory can only grow productivity at 2%. Houston we have a problem. You know it’s name.

-

Below is exceptionally simple for illustrative purposes and to move any further you have to agree with the idea and I’m not too sure how you can disagree that the US is at FULL FULL employment. Full productive capacity. Staff shortages still everywhere. For hire signs everywhere. Businesses running reduced hours everywhere cause they cant get people. 2X number of job openings for everyone looking for a job. There are no statistically significant pools of labor on the sidelines in this economy, save immigrants outside the USA who would come here but the political system can’t get out of its own way. If we can agree that then we can move on to my illustrative simplistic example of the problem. Year 1: The USA is soup to nuts a widget economy. Every man/woman/child works in the widget economy and consumes only widgets. It’s a 100% widget economy. Every man/woman and child now works in widgets factories. There is no one left to add to the widget factory. Every inch of which has been filled with automated production lines. There is no obvious easy way to increase capacity. Widget factory USA now has ann absolute max productive capacity of 100 widgets per year. Total nominal monetary spending/income in the economy is $100, all people spend their money on is widgets! - therefore a widget costs $1 to buy. No inflation. Year 2: Productivity in widget factory USA improves by a measly 2% per year through technological innovation. Widget factory USA in Yr2 can now produce 102 widgets. However nominal spending/income in the economy grew this year by 8% to $108….cause Widget Biden printed $8 extra dollars and sent a bit to everyone - a widget now costs $1.06…..6% inflation. 8% nominal spending growth minus 2% productivity growth = 6% nominal price inflation. 6% inflation, in a full employment economy through wage demands, begets 6% nominal income growth or somewhere close to it as employees bargain for NOMINAL pay increases in-line with inflation….……but that doesn’t solve anything cause your productivity growth is stuck at 2% growth…..its PRODUCTIVITY that matters over the long pull not funny money nominal spending/income. Inflation in the classical sense is defined as too much money chasing too few goods and services. Exactly right. You have two choices in widget world to restore price stability………you drive productivity WAY way up……which is just not easy………..or you reduce nominal income/spending…such that for a time productivity growth exceeds nominal spending/income growth or in fact nominal spending goes negative/contracts for a time…… and you get disinflation……then you build out from there…..….the Fed cant do anything on productivity (politicians could, write your senator) so the FED first via (1) Money Supply then via (2) Credit conditions they eventually begin to hit (3)spending/income……and widget world gets price stability back. Price stability is like oxygen for productivity growth - it gives predictability…..which allows for capital investment planning, which actually expands productivity…..which is what matters most over time.

-

How many years does inflation need to be at 5%+ for you to stop calling it BS? Tapped out is one way to put - you dont think thats a problem in an economy where consumption is 60%+ of GDP. Great environment for margins/earnings? Especially peak/record margins/earnings. Finally a tapped out consumer, feeling inflations wrath is also an employee heading into EoY 2023 comp discussions motivated to restore purchasing power. Non-farm payrolls growth is going to accelerate into 2023 I think…..we are going to be surprised that underlying inflation might accerlate a bit. Folks getting pay increases, whats wrong with that I hear you say? The only problem is as I’ve said before is the USA is beyond full employment 3.5%…when the natural rate is closer to 5%, nominal spending growth (via wage inflation) is exceeding productivity growth (of goods/services). The gap between nominal spending/income growth (wage inflation) and productivity growth in an economy with full employment………is……….INFLATION.

-

-

Pretty much - there are no bullish outcomes in the near term given the opportunity set.....10year of ZIRP, Trump corp tax cuts, COVID stimilus.....everything got priced for perfection.....but then perfection didn't show up.......inflation did, then Putin & geopolitical tensions. @Gregmal points out you can still find individual names for sure....but lets be clear....the Fed & the beta had your back in 2010's, it bailed out lots of errors I made thats for sure.....but the stock picking game just got exponentially harder for those not paying attention. The beta is trying to stab you in the back now. So folks don't misunderstand me, I'm urging caution, Im urging enhanced due diligence.....I'm suggesting a larger margin of safety than one would otherwise seek. There are more ways to lose currently....multiple compression, earnings getting whacked, recession. I'm not saying dont play. I'm saying play sure but move forward with extreme caution.....look for 2ft hurdles, not 20ft ones. This is the way. @LC I'm afraid earnings were gonna suck either way.......inflation, all on its own without the Fed or Wall St. narratives on the short side, is/was destroying purchasing power, driving up costs.....which is hurting sales/earnings/profit margins of businesses. Some people act like it was all roses till Jay Powell started talking about persistent inflation and ruined it for everybody.....the real problem is Jay Powell wasn't talking about persistent inflation early enough he was too busy buying god damn MBS's and keeping rates at 0% when they'd put the vaccine into everybody's arms. The Fed can let inflation just do its thing....that is an option they have.......which is to painfully and slowly over time allow it to ravage the economy such that inflation itself gets worse and worse....but eventually left to its own devices inflation itself would put the economy into a horrible recession, which would be disinflationary & return price stability having put millions and millions of people out of work directly and through the meat grinder indirectly for unknown years. or the Fed can administer some tough love.....and hopefully get this thing done in 12-18 months....in a controlled way minimizing misery. There are no good options here folks..........only less bad ones......its an economic Sophie's Choice for you movie/book lovers out there.

-

https://www.bloomberg.com/news/articles/2022-10-29/good-news-bad-s-p-500-earnings-are-playing-into-the-fed-s-hand?srnd=premium&sref=7zqHEcxJ From article:

-

Wow hadnt seen it nice too see some, formerly AOC fans, wake up and smell the coffee.........AOC's of the world and her mirror image folks on the radical right.......think only in black, whites & absolutes.....good guys and bad guys.........the world is fifty shades of grey ......and the scary thing about the Ukrainian/Russia situation is maybe the only thing they agree on down in DC is perpetuating & escalating this conflict. https://nypost.com/2022/10/13/aoc-heckled-by-anti-ukraine-war-activists-at-town-hall/ Word.

-

https://www.telegraph.co.uk/world-news/2022/10/27/us-send-nuclear-weapons-nato-bases-amid-rising-tensions-russia/ Its all just posturing and saber rattling and escalating to deescalate.......until it isn't.

-

The logical flaw in yours is that you are implicitly assuming that growth isn't negative.......forget 0%, try on -2% for size...then inflation adjust that cash flow growth.....not so hot now.......but listen its a multi-variant equation lots of things can move around but my premise still holds which is there a exists a class of stock with really low FCF yields and exposed to a both peak earnings & a recession....now whats their smoothed out earnings (minus COVID stimulus/demand bubble), whats the FCF on that new smoothed out earnings stream for 10 years (hint: the FCF yield is even lower now)...........now strip out a couple of years trough recession earnings, now inflation adjust it all back from 10 years in future with 8% this, 5% next year, 3% year after, then 2,2,2..........for slow-ish growers....the math is quite scary.......and this why I warn against high multiple stocks, in an inflationary & a rate hiking regime change. But yes I understand a stream of growing free cash flow changes the math....but some things arent growing cash flows nearly enough, or have and wont in the future. Its complicated...but you have to think in alternatives is my main point.....think of everything as just another financial instrument.........cash, bonds, equites, RE....then think about relative risk, duration risk, principal risk.....and ask are you being adequately compensated, are you beating inflation......if not your purchasing power just got whacked.......we've gone from TINA to a new world folks need to start thinking a little more fluidly...

-

Anyhow - its beyond bonkers IMO the market rallying........and the pivot people are deluded.......unemployment really hasn't budged, the GDP numbers were actually pretty good......is this an economy with 'slack' appearing such that it has strong disinflationary pressures driven by sitting below its productive capacity for a while - such that we are on the pathway back to 2-3% inflation very soon. I just don't see yet. Again define pivot........it used to mean cutting rates and printing fiat.......I guess for people desperate for the market to go up....pivot now means 50bps increases moving forward vs. 75bps. Its funny the way the narrative changes