changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Again everybody mischaracterizes my ramblings..........its not about when to invest and when not to invest.......I've never said sell it all, wait, dont buy....everybody down tools........its a question of defensive or offensive posture......I'm invested, I remain invested....I buy things when they make sense to me....loaded up more Irish banks today......however I have a broadly defensive posture currently with a view that a time is coming to get aggressive, very aggressive but just not yet......I want cash on-hand.......I want things that will turn to cash in the strife that could come........I'm interested in indexes because I'm interested in the beta.....cause good companies will get caught in the beta and I'll buy them.......I'm interested in the indexes as a hedging and shorting tool. Thats my interest in SPY/QQQ. I buy companies not indexes.

-

Yep - if I counter my own bearishness..... the only thing different this time versus rate hiking/inflationary cycles of the past.........is the sheer number of job openings vs job seekers........the big question and I'm not convinced that it changes anything.......is whether simply killing the number of job openings from historically crazy high rates might be enough, in and of itself to carry the load of the heavy lifting needed to tame inflation pressures. I hope it does........but really I return to the basics when I ponder this.......CPI & wage increase expectations/success and their inextricable link are only killed by higher unemployment & below equilibrium aggregate production for a while......when you think of extreme level of JOLTS then one should think of it like extra dense jungle that the monetary authorities need to cut away at first before they can get to the solving inflation pressures.....pointing to perhaps not higher interest rates.....but rates which need to remain at their terminal level for longer than is usual to have the same desired effect.

-

Yeah broadly @dealraker I agree.....but I'm afraid in this instance the macro and bear market bias is just too obvious to me...but I'm not frozen, I haven't stopped analyzing business/industries.....I'm moving forward with greater caution than usual....a higher hurdle for investment........more hedged, more dry powder........its a kind of positioning thing with some market cycle overlay.....if my bearishness is wrong it'll cost me a few 100bps of performance.......if I'm right and I've been pretty right since the spring/summer it will be and has been a source of outperformance relative to the beta. Not for everyone what I'm doing......but yes wouldnt want anyone to suck their thumb pondering macro it is usually a fools erand...guess you can add me to this fools list in this instance.........but I continue to turn over rocks and find things I like.

-

I'm not too sure its that confusing.......US at beyond full employment, labor shortages everywhere you look....historically low immigration....historically high retirements....historically low participation rates against a backdrop of historically poor educational outcomes for low income cohorts.......historically low productivity growth....historically high nominal spending increases....demographic trends locked in a box for decades........DC unable to get out of its own way to fix the supply side. Then 2020 came and you unleashed just unprecedented monetary & fiscal stimulus......which lit the fuse on inflation which is now with us coming up on two years solid and getting integrated into every pay deal I've spoken to anyone about.........some people talk about inflation, its link to wages and its knock on effect on prices as some kind of fringe academic theory unproven in the real world.........yet I talk to small business owners and its just the most practical common sense mental exercise any of them ever heard.....they literally look at me puzzled when I talk to them about it & inquire how they respond to higher labor costs.........seriously they look at me like "duh! dummy"....."if I have to pay people more in my store I"m gonna charge my customers more, I'm not running a charity"....is the general jist. So inflation is here....its entering its terrible two's.......and the historical record is pretty clear on it.......you need a recession and a period of sustained below trend aggregate output to really conquer it. The FED has a shot heading into 2023 to put the inflation genie back in the bottle.....how......ensure comp discussions in H2 2023 are informed by job insecurity such that chain mail nature of inflation is broken....they've utterly failed at that task in 2022 as they started hiking way too late. Shame on them.

-

Not picking bottoms as we spoke about before - I own what makes sense..........I hedge with what doesn't make sense.......this long/short structure makes little sense most of the time in periods where markets are boring and going up.......during this period......lets call it choppy waters getting from ZIRP to a post ZIRP world.......it makes a tonne of sense to me. Lets see.

-

This cycle aint over......call me.......when unemployment goes to 5%+...... inflation goes down to 2.x%......and the Fed is cutting rates. I still expect us to smash through June/Oct 2022 lows on SPY........with VIX peaking at 40.......once we get that.....happy to think about the next bull market Lets see.

-

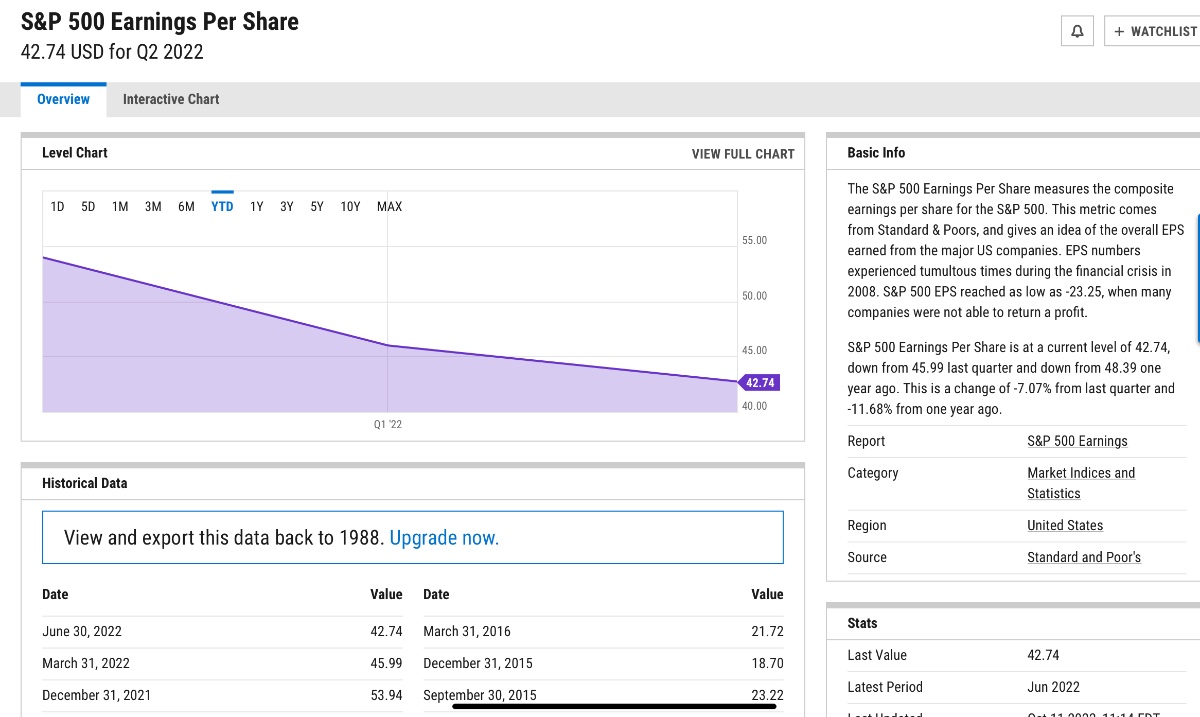

Bit early to declare victory & announce the new bull market open……earnings peaked at 53.94 in Q4 2021…….every subsequent print has been down….if you think we are stopping here you’re gonna be mistaken…..opex costs into 2023 are rising as wage costs ratchet it up…..pushing price game on a weakening consumer is over….you accept lower volume or you accept lower margin……either way it’s not good for the bottom line. Let’s see.

-

Yet......... American consumer has officially gone on to their credit card........possibly one last Christmas where they pretend all is well.....then pay the consequences come Jan/Feb CC bill.....this is my base case + Fed getting rate up to ~5.5%+.....but unlike consensus......they hold it there for much of 2023 as economy/employment/SPY & most importantly inflation begins to tank........this resolve in the face of poor economic data is whats gonna shock market participants I think. Lets see will be very interesting to see what happens but this is my hunch.

-

Agree with this too......but I think this secular change is ultimately why a return to anything close to ZIRP is unlikely....and will inform the risk free rate for the next decade and beyond. Which is important to consider if you touch low FCF/low cap rate investments. However what we have right here, right now is predominately being driven by classic monetary inflation....which is excess income/spending chasing too few DOMESTIC goods and services......this is a very clear domestically created inflation problem......once this is solved.....there is as you say secular inflationary pressures waiting afterwards such that ZIRP wont be an option for the politicians/central bankers.

-

As always what I speak about is monetary inflation driven by nominal spending increases against an economy operating at full tilt..........so it will show up in domestic goods and services.......and it will fight against the fall in what you outlined above such that this wont be linear fall from 8% to 2.x% like people seem to think......if I'm right inflations fall will have these little stubborn plateaus driven by 'flare-ups' in certain goods categories (domestic ones) which will make it so that inflation's fall gets stuck for a time. We wont have a lovely sloping line going from right to left and down. That's my hunch. Importantly these plateaus will break the hearts of market participants waiting for the pivot resulting in negative beta.

-

This is it - I expect a flare up of sorts in early 2023.....why......because the Fed started too late to fully inform Q4 2022 comp discussions across the economy & the economy hasn't weakened enough even now......such that early 2023 will be filled with retrospective 2022 CPI+ incorporated into a large swath of wage increases that will flow through into incremental nominal spending increases in Feb/Mar in an economy STILL potentially at FULL employment..........and the cycle begins again to a certain extent. The solution.......and people wont like this......is that the Fed needs to hold the economy's head under the water for the WHOLE of 2023 such that (1) unemployment rises significantly above its natural rate introducing slack into aggregate productive capacity & (2) Q4 2023 comp discussions need to be informed by job security....not CPI.....such that dis-inflationary forces take hold into late 2023/early 24 and only then can you consider easing off with the knowledge that Q4 2024 comp discussions will have target CPI incorporated. Thats the correct prescription IMO lets see if the implement it or do the popular thing and give the market what it wants which is the much talked about 'pivot'.

-

I've been guilty of this in the past - the first and most important question always is whether the enterprise has an improving, stable or deteriorating business fundamental future in front of it.........leverage amplifies whatever the answer is.......the mistake that can be made & therefore amplified in a Malone company is you make the wrong business analyst assessment.......a value trap is always a painful experience.......a levered value trap is torture.

-

Not huge call to say inflation has peaked........Ken reckons 2-handle by end of 2023.......hope he's right

-

Yep its been a virtuous circle - VC firms fed into start-ups......start-ups bought ads......ads drove valuations of earlier VC investments.....which beget more VC investment & performance records.....which attracted more outside capital.....which fed more startups....who bought more ads and services from 2nd generation micro-services start-ups....which drove valuations........ I've a friend in tech........who's startup company just did an audit of all the 'hot' SAAS services they built their enterprise stack on......not to save money but rather to understand if any of these services were to cease existing....how might their workflow & internal processes be effected........counterparty service risk is real when you've built your company on top of every hot B2B software startup....legacy companies sitting on Office365/SAP/Oracle.....rarely have to ask themselves such questions.

-

He sure does......from talking to friends/family in Europe.....they'll do this winter getting squeezed on energy bills in support of Ukraine......but not a second.........I expect once surpluses turn to deficits in the US....and the deficit starts to matter again & with the Republican's in control of the house (investigating Hunter Biden & finding out all the corruption with him/Ukrainian) the narrative is gonna shift to why are we spending so much scarce money over there. Ukraine would be wise to push as hard as they can now with Russians on the back foot and their friends in the West still full throated in their support.

-

Yep too many banks, landesbanken, credit unions........most of which dont earn their cost of capital and would be wound up or merged if in US......in Italy, Spain, Germany....they provide gainful employment and prestige to their leadership teams/boards who are happy to sit on shareholder equity and in a real practical sense torch it over time.

-

Yep Bank of Ireland - European bank….but unlike other European banks its in a banking market that looks more like an oligopoly than the bloodbath on the continent..….where there are way too many credit institutions competing with each other for deposits/loans…..I’ve written about it in a thread that is confusingly titled AIB on here. AIB being the other Irish bank. For sure - this is the first time I’ve ever let the macro tail really wag the dog……the evidence is simply too overwhelming not to introduce a macro bearish bias…..I dont intend to carry it forward once we move through this period into the new normal (whatever that is/whatever that means).

-

Your 100% right........macro forecasting 99% of the time is a waste of brain power.........but sometimes the macro environment is just kind of so crazy that the direction of travel is somewhat obvious & the warning signs so clear that I would argue you should pay attention this time..........and then put away your macro books for another 40 years............I can list them.....the COVID fiscal largess in the trillions (not billions), monetizing government debt, inflation where it is, speed & scale of rate hikes......advertising canary in the coal mine stopping chirping....etc etc. (Also self-aware enough to realize that this is what macro guys always say, thats its blindingly obvious.....but I've some form to contrary......I ignored the marco guys in the 2010's....their arguments didn't stack up...I was long, very long). So I'm not a perma bear macro lunatic, though I sound like one . I also just dont like fighting the Fed. But also not freezing here - I own what I like long term I'm fundamentally long......just bought more MSGE/HSW Thursday.........have bearish hedges sitting around a core long portfolio..........I guess if I was to sum up what I'm doing is that I'm both an owner and a seller of vol right now & cycling through each what I consider to be a bear market rally.......for example......Friday I sold SPY OTM June 2023 Calls......cash covered, not a big chunk of NAV......will materialize into cash at some point with the volatility & I'll turn around and buy more BOI. Kind of recycling short type hedges into core longs but at the margins of the portfolio....nothing of any existential size that would endanger more than a coupe of hundred bps.

-

Agree - there will always be winners and losers. My reference above which I should have made clearer (and I have fixed now), to the paradox of thrift, speaks to the concept of the aggregate economy......and its circular nature.....and how recessions, driven by belt tightening/saving, result in aggregate savings not going up at all across the system. That is the paradox & this is how recessions begin & have their own momentum. Its exactly how a slow down in ad tech, leads to a slow down in luxury condo sales in SF, which results in SF house price falls, which has negative wealth effects such that people decide to hold on to their two year old Tesla a bit longer and not get the new one........and so on and so forth.....it feels like that type of chain reaction has begun.....the title of the thread is 'is the bottom almost here?'.....my answer is NO (as it refers to the indexes)....underneath the indexes is a beautiful world of complexity......its why for example I don't hold Marriott......but I've a huge slug of Hostelworld.....exactly to your point....Marriott's biz & leisure customers are macro economically sensitive....Hostelworld's customers not so much. But yes - another simple winner to your point in the paradox of thrift type economy were stepping into is - trustees and administrators of bankruptcy's. Business will boom.

-

Yep - one mans spending, is another mans income. One company's expenses, are another companies revenues. Cutting spending/expenses in splendid isolation works very well........the time to tighten your belt and expense account was in 2021.........nobody else was doing it and it would have worked very well........................but if everybody else is also cutting their spending/expenses at the same time (which this economy is starting to feel like).......ironically it means nobody in AGGREGATE across the economy actually gets to save incrementally anything. https://en.wikipedia.org/wiki/Paradox_of_thrift

-

See what you mean!

-

Agree but you have to be very careful what you own in this period - and this is kind of what I warn against with my macro talk as the backdrop......I'm not encouraging anyone to freeze, I'm encouraging them to think of a world where savings account pay 4%, corporate credit is at 6% and ask yourself why would someone own the company I'm thinking about buying in that world and at that price..........lots of effective confiscation certificates floating around out there still (sub-4% FCF yields) which peeps need to be really careful about.......and that includes companies with business models & so net income that were bumped up by (1) COVID (2) the biz model actually relies on cheap debt to work .......if.......we are heading into a future that is non-ZIRP. So what your proposing and what @Gregmal talks about is totally right. I'm on board here, we are saying the same thing...........7 times earnings with earnings conservatively estimated such that FCF yield is well above 10%........that makes sense total....and I own a basket of these things to and am buying more even in the last few days.......the danger is folks looking at say tech (not FB) with the falls in some of these companies and thinking they are now 'safe' just because they fell 80%...... My lesson - is that current Free Cash Flow is now KING.....when liquidity is being trained from the system financial instruments with no FCF base have no anchor, no foundation.......it needs to be high enough such that (1) equity risk premium contained within makes sense in a world of say 4% 10yr treasury's (2) it has pricing power such that the company can raise prices in-line with or better than inflation.

-

Maybe Jeremy is right but its very early to be declaring victory.......in a full employment economy.......it doesn't matter what the Fed thinks inflation is or a what Jeremy Seagul's adjusted inflation rate is........its what workers believe it to be & the relative leverage they have with employers.......that cultural 'meme' inflation rate is ~8%......and its forming the foundation of every salary comp discussion I'm aware of....such that 2023 nominal income/spend is going to loaded with 2022 CPI++....anecdotally ~10%+........whats the problem with that?............you cant 'consume' nominal pay increases, you can only consume REAL increases in the aggregate level of actual goods and services produced.........outside of a measly 2% productivity gain where are those real goods and services gonna come from in an economy with 3.7% unemployment and running at what accepted to be full tilt? I hope we are on a perfect glide path now to 2.x% inflation........but without a significant increase in unemployment in H1 2023.........my guess is we are going to get what happened in the 1970's which was inflations descent hitting stubborn plateau's and/or surprising flares upwards. In fact I would expect in early 2023 BLS data, then subsequently in inflation data to see what I described above.....nominal pay/spend increases hitting measly productivity gains and generating a new cycle of inflation which will be the delta between the two. On the other hand this Christmas we might see enough households leverage up their balance sheet so much that spending collapses into H1 2023.....which would result in what I described above not happening. Its why the Fed I think will continue to act and talk exceptionally tough heading into the December meeting and beyond.....they've got a window heading in 2023 to kick inflations butt.....and to ensure EoY 2023 comp discussions don't incorporate historical CPI.....the way you do that is not nice, the economy has to be put over the hot coals for a little while. I hope I'm wrong......and Jeremy is right and inflation is just gonna magically go away and the Fed can get cutting again in mid-2023.

-

Ditto getting the same feedback.......another reason the Fed messed up.......outside ad-tech.....fear around job security hasn't circulated fully because they started hiking too late..............if they started hiking earlier and put some very public strain on the economy…..employers could have gone into 2023 comp negotiations holding a line that wasn't something like CPI++....that window has passed.....2023 comp is going to be LOADED with 2022 CPI..........and this folks is exactly why inflation doesn't go away so easily.........its backward looking.....it feeds on itself.... Its why inflation expectations matter but don’t matter…..nobody is negotiating comp on inflation expectations…they are negotiating comp on PAST inflation and we’ve had quite a lot of inflation recently if you haven’t noticed.

-

One addition to the above that I failed to make clear - as one could misinterpret….. the Fed’s balance sheet matters ALOT in regards to other financial instruments…like I told you they buy a financial instrument, give cash to institutional counterparty who invariably buys another financial instrument ….like stocks….or puts the cash back on deposit with Fed until they buy another financial instrument. This liquidity sucking sound means things without strong cash flows underneath are equities with no foundation…..