Xerxes

-

Posts

4,050 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Posts posted by Xerxes

-

-

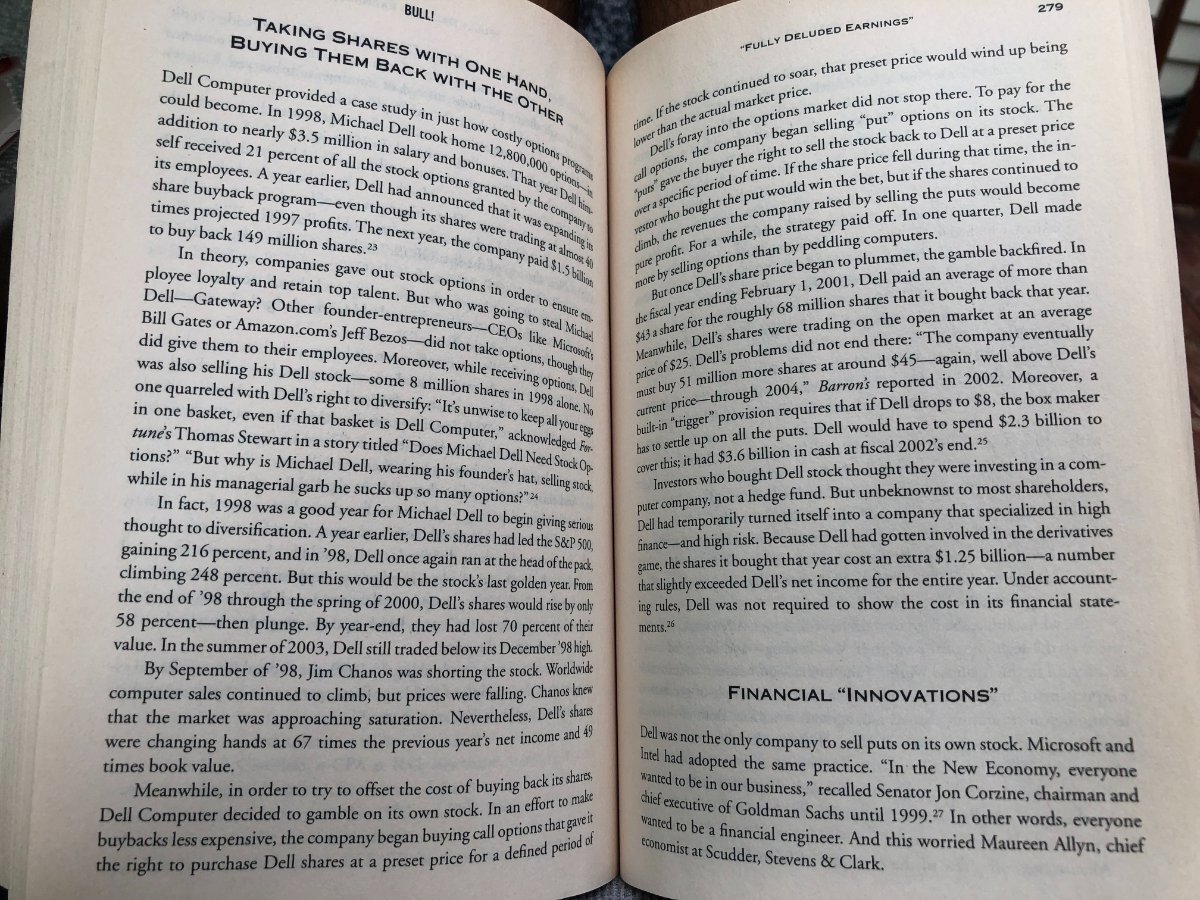

Once upon a time, in galaxy far far away, when Dell Computer was running a hedge fund business.

Fast forward to 20 years later, hopefully, Prem W. has closed out the derivate bet on himself by now.

-

Perhaps, if the intent is to close up the discount, and if the value is real there, than a NY-based listing would provide a boost in that price discovery.

Surely, the NY-based bears have moved on, and FFH today is not FFH of then.

Large pension and/or sovereign fund have a problem these days: low interest rate. That problem is pushing them deeper and deeper into the world alternatives into the arms of Blackstone and Brookfield. FFH (for that matter other insurances) have the same issue as pension and/or sovereign fund, albeit at a smaller scale. Difference is that they cannot push deeper and deeper into alternatives, because they need to keep them into T-bill and bonds for regulatory reasons.

Now doesn't that deserve a broad industry discount to intrinsic value (given the very low yield on that bond portfolio).

Add to it, FFH-specific opaqueness compared to other insurers.

Now doesn't that deserve a FFH-specific discount to book value.

-

My 2 cents,

My largest holdings are not high conviction idea, rather they are your-conviction-level-does-not-matter

BAM, BRK, AMZN etc.

-

Men were in the business of empire building since the early days when cavemen were gathering food ... except Barry Diller perhaps.

Looks like it took a major event like the once in a hundred years pandemic for the likes Masayoshi Son or Prem Watsa to change their way, but too often the empire building instincts kicks back in again and again. I don't know what the future holds, but it seems that the transition from asset-gatherer to a CEO that can get a laser focus on shareholder value per share, is usually a bumpy road. Empire builders do not find shrinking the company (i.e. selling assets to fund massive buyback) that exciting, even if it means more absolute wealth and control.

For FFH's value to raise on a higher plateau permanently, one of the three things need to happen:

(1) a large uptick in the insurance business (ala 2001) i wasn't following FFH then, but based based on past conference call, Prem alludes to the period where Odyssey (i think) picked up a lot business

(2) large investment gain that is monetizable. Not enough to have a home run as paper gain. There has to be clear road/intention to monetization. Financial media loves the sum of the parts stories and conglomerate discount. How many of those famous relative trade actually worked out in a timely fashion.

(3) re-rating in the bond market.

---------------------

If 1 out of 3 happens, i think we can see a road to a higher plateau in terms of valuation. If 2 out of 3 happens, might even get a premium of book value. If 3 out of 3 happens, go buy lottery.

---------------------

FFH de-listed from NYSE some years back. I don't know the whole story (related to the hedge fund short sellers i think), but it seems to that by doing that it also removed itself from being "discovered". If it insists it would not want a NYSE listing to get that exposure, perhaps that is a sign that it likes how things are: i.e. being opaque and under the radar.

That is why for me, if FFH can deliver 5-7% gain I will be happy. That is my return target allocation of FFH in my portfolio. Digits and all those other things, all they do is to layer up more and more margin of safety into the stock, which is ok as well.

-

On 7/13/2021 at 12:40 AM, Parsad said:

The only person who has had more influence on me than Warren and Prem was my father...no teacher has had more impact than those two. How has Buffett changed my life:

- He changed everything for me from when I turned 29...the first time I read the 1998 BRK Letter to Shareholders, literally a light went on inside of me. I had been extremely depressed since my father had died when I was 21 and I was helping my mother raise my brother who was only 9...I was a functioning depressed person wondering what I was going to make of my life.

- That letter and reading subsequent letters and books changed my whole investing framework and how I thought about money, life, happiness and integrity.

- It lead me to Fairfax Financial and Prem Watsa who became a mentor and very good friend.

- It lead to the creation of the initial version of this website and now COBF and all of the wonderful friends and posters on here...especially lotsofcoke and Ericopoly...two that played a significant role in my life and learning.

- After meeting Buffett, I came home and quit my job and began my journey in the financial world.

- That lead to finding other more accessible mentors and friends who were equally influenced by Buffett and others like Tim McElvaine, Francis Chou, Mohnish Pabrai, Larry Sarbit, Jeff Stacey, Wayne Peters, Andy Kilpatrick, Guy Spier, etc.

- It lead to me starting my own fund company with my cousin who was like a brother to me.

- Which led me to build PDH...for better or worse!

- All of this lead to the wonderful experiences I've enjoyed and my family has enjoyed...trips to Toronto, Chicago, Los Angeles, China and especially the Fairfax India trip...also meeting Wayne Gretzky, who was a childhood hero for me and my brother.

- It lead to raising nearly $300,000 for Crohn's & Colitis Canada, roughly another $2M that I've helped raise working for Cystic Fibrosis, The Center for Child Development and other charities.

- Finally, Buffett was the seed that allowed me to learn and also influence so many others...via coffees, lunches, dinners, our Toronto dinner, the funds, PDH, COBF, charitable work.

I turned 52 a week ago...Buffett has influenced me now for 23 years, 2 years longer than my father did! I owe my father and Buffett everything...everything! Cheers!

AMAZING !!

-

Thanks ^^

Had no idea that existed,

Here is a description from Linkedin profile which still works.

FairVentures is the innovation initiative of Fairfax Financial Holdings Ltd., with the mandate to research, develop, partner, and invest in innovative solutions to support the Fairfax family of companies. We recognize that Fairfax companies need to be on the leading edge of emerging technologies, processes, and thoughts as well as their application to their industry in order to stay competitive. The purpose of FairVentures is to evaluate new technologies, opportunities and businesses that are applicable to Fairfax subsidiaries and their customers.

I am counting on these deep-value / distress guys to put money to work, when I am going to be wrong with the overall market (not that I am right), in the meantime, I will take 5-7% BV growth. I do not need 15%.

Not talking about investing through flash crash, which they have shown they cannot as they are not nimble enough. But something like 2000-2001 slow 50% lumbering rollover bear market.

Remains to be seen, if this massive 12+ months rally we have seen is a cyclical bull embedded in a long-term secular bull market, or just one massive bear market rally, which will loose steam and roll over in the next 15 months, with us standing on the top, and just not knowing it.

-

Viking,

The more concentrated one is, the more one is concerned about a crash. But in reality, a crash doesn't discriminant so much between concentrated and diversified positions.

As far as the crash is concerned, it is always six month away, because it helps us anchor our expectation. That being said, I would offer a differentiation between two types of events:

A relative correction: is only six months away IMO

If markets are forward looking mechanisms that saw a massive GDP bounce back a year earlier, one would expect that they would also see the decrease in the rate of change in the economy. For instance, it is expected that US GDP growth will be something like 8% by close of the year, with most of that being due to the arithmetic of starting at a very low base. One could say that the massive market rebound we had thus far, was "seeing" that GDP bounce back.

Imagine, in March-April 2020, in the middle of complete chaos, the foundation of the next bull market was being laid, as it was "looking" past the noise and zooming into the recovery. After all, the economy went on pause and was strong going in.

Therefore, it stands to reason that if we expect that 8% GDP growth to normalize to something more like normal 3% in 2022, the scent of that decrease in the rate of change would be pickup by the market 6-8 months in advance. But I think that would be a healthy correction. And while the not so nimble Berkshire and Fairfax of the world couldn't take opportunity of a massive drawdown (see below) for different reasons, a healthy relative correction would be ok for these self-proclaimed capital allocators.

Mike Wilson from Morgan Stanley (who nailed the recovery) is saying the bull is aging rapidly and already in mid-cycle. The flatting yield curve is supporting that narrative.

Market crash on an absolute sense

A massive liquidity drawdown like the one we saw in March 2020 or Oct 1987, cannot be guessed/forecasted in anyway. By definition, if we all expected a crash (and I call this a crash and not a correction), there would be no crash. There is crash, because it is unexpected.

Consider this, by Feb 2020, the virus was not an unknown and in fact the economic impact was well known, yet how many people saw the market crashing the way it did. I, for one, was expecting a mild correction. And of the ones that were smart enough to sell/hedge heavily, how many were able to go back in in full force in April. (Ackman ?)

Those kind of crash, take down anything and everything (including gold). Only USD and US Treasury bond do well as they soak up liquidity on a global scale, for a brief moment, that is.

Whatever event will cause the next meltdown, we don't know, but it safe to say that it will not be a pandemic or a variant of the current one. why ? simply because, IMO, market has a probability distribution table built into it. That "table" has now been updated and includes probabilities associated with pandemic and possible outcome. Yes, market can roll over and can correct, but it will not crash the way it did in March 2020, if there is a new variant or a new pandemic.

Crypto and a SPAC

PS: we already had a crypto and a SPAC correction, as it shows that excess liquidity is being pulled from speculative assets and going into the real economy. I think this is bullish for the real economy, as those sponges (crypto/SPAC etc.) are squeezed of liquidity.

2003-04

I just finished reading this book.

Bull!: A History of the Boom and Bust, 1982-2004: Mahar, Maggie: 9780060564148: Books - Amazon.ca

Great history book. Interestingly the book finishes around 2003-04, where the market bottomed in hindsight, yet in the book you got Warren Buffett and Jeremy Grantham of the world, calling the market still too expensive in 2003.

-

On 11/29/2020 at 6:54 PM, Xerxes said:

aug3020.pdf (berkshirehathaway.com)

About a year out, so how did they do .. even though we don't really know the initial purchase date, but we can assume perhaps the heavy buying would have been post March-2020.

"The companies, listed alphabetically, are Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo. These holdings were acquired over a period of approximately twelve months through regular purchases on the Tokyo Stock Exchange"

Mitsubishi (8058), Mitsui (8031), Itochu (8001), Marubeni (8002) and Sumitomo (8053)

38%, 62%, 39%, 29% and finally 20%, respectively, as one year return.

Interestingly, looking at these I realized that some of that of them (Ex: Mitsubishi) have a NYSE listing. Not for the whole conglomerate, Mitsubishi Group, which is fact private, but different tentacles (i.e. Mitsubishi UFJ Financial Group), which by itself is worth $70 billion, has a NYSE listing.

My guess would be that Buffett bought Mitsubishi Corporation (8058) and not MUFG (8306/MUFG) nor Mitsubishi Heavy Industries (7011).

Mitsubishi UFJ Financial Group - Wikipedia

"MUFG holds assets of around US$2,459 billion as of 2016 and is one of the "Three Great Houses" of the Mitsubishi Group[6] alongside Mitsubishi Corporation and Mitsubishi Heavy Industries. It is Japan's largest financial group and the world's second largest bank holding company holding around US$1.8 trillion (JPY 148 trillion) in deposits as of March 2011.[1] The letters MUFG come from Mitsubishi and United Financial of Japan."

-

I like how Prem took some of the wording word for word from BDT mission objective on its site:

"Founded in 2009 by Byron Trott, BDT serves as a trusted advisor to closely held companies and owners with world-class capabilities across a variety of areas, including M&A, capital structure optimization, strategic and financial planning, family office, philanthropy and social impact, and next generation transition and development. BDT Capital Partners provides family- and founder-led businesses with long-term, differentiated capital. The firm has raised over USD 18 billion across its investment funds and has created and manages more than USD 6 billion of co-investments from its global limited partner investor base. The firm’s affiliate, BDT & Company, is a merchant bank that works with family- and founder-led businesses to help them achieve their strategic and financial objectives. The firm has offices in Chicago, New York, Los Angeles, London and Frankfurt."

-

On 7/11/2021 at 12:49 PM, Viking said:

But given the lag between written and earned we should see some pretty good results from insurance companies over the next year or two (assuming a normal cat loss years).

This is key here. After all, the whole point of the 'hard market' was for them to invest their capital, for a future return, which we have not see (mostly?) yet flow through P&L as earned.

Incidentally, further growth potential (or lack thereof) in the insurance side of the business will impact intrinsic value and not current book value. So BV can be continued to be used as the proxy for the floor for here and now.

-

To those saying higher valuation are somewhat justified due to lower interest rate, Jeremy Grantham would say, you are using an inflated asset (bonds) as a yardstick to determine if another asset class (stocks) are in bubble.

To those saying (mostly on Twitter), US printing press will take US to the ways of Weimar Republic, I would say comparing the current incumbent super-power with USD as reserve currency (allbeit one that is relative decline), to the Weimar Republic that at the time was coming out of revolution in 1918 that saw the Wilhelmian monarchy fall, that got the short end of the stick coming of Treaty of Versailles, is a far fetch comparison.

-

20 hours ago, SharperDingaan said:

As this is a 'material' transaction IFRS basicaly allows 2 choices.

1) Report the higher value ($47) on the face of the financials, along with a dislosure note relating to the following $14 regulatory aspect, or 2) no change on the face of the financials, and a disclosure note outlining the entire $63 'market' revaluation. Go with 1) and you also improve the financial ratios.

In an efficient market, the choice of disclosure shouldn't matter.

However, we all know markets are NOT as efficient as claimed .....

SD

I don't know anything about re-valuation to the upside for associates in IAS 28. I am guess their accountants did all the legwork to get it here, ... but was just curious the accounting framework on this.

If FFH was selling a portion of its stake, I could understand the mark-up on the rest.

IAS 28 — Investments in Associates and Joint Ventures (2011) (iasplus.com)

-

I read it as two steps (granted it is not totally clear to me):

- +$47 in book value by close of Q3 once Digit issues those new shares to the new investors, allowing FFH to re-value its stake (not clear if FFH participates or if there is dilution)

- +$14 further when regulatory aspect goes through (Q4 or thereafter), allowing a higher % ownership, which implies that FFH is participating and adding more money.

Again not clear to me

-

Thanks for posting the video; i thought i had no hope with CNBC firewall, but there was hope.

Loved how the interview opened like that:

"Think of how massively stupid that was ...."

-

Petec => "The transactions are subject to customary closing conditions, including regulatory approval, and are expected to close in the third quarter of 2021."

On a different note, purely from an accounting point of view, can an associate be marked-up ? mark-downs are through impairment, just was not aware that IFRS allows marking up as well on an associate or a consolidated entity.

-

Globe & Mail incorrectly reporting this as "booked".

I am no expert, but they could have included this release as part of their Q2 results in a few weeks.

"Fairfax Financial Holdings Ltd. booked a US$1.4-billion gain after a subsidiary in India, Go Digit General Insurance Ltd., launched a US$200-million share sale at a valuation well above Fairfax’s investment in the four-year-old company."

Viking, you cannot include Digit gain into your Q2 results of BV.

Digit goes into Q3.

-

Lots of economic value created at Digit. Good stuff !

Hopefully the accounting windfall in Q3, does not get offset by (1) large one-off cat events in Q3 and (2) by shorts-gone-mad.

Wait a minute, we don't have to worry about (2) anymore !!

That being said, I wonder what is the point of the press release here. This is not even close yet.

Or perhaps they intend to close the total return swaps soon, so want to capture as much call option as possible before un-winding the trade.

-

Thanks !

I think Sopranos started that unhealthy practice of having two parts to a last season that was a year apart.

-

Just finished the new season with Bosch.

I am unsure if this last season has a part 2 to it.

Enjoying Loki on Disney+

-

Viking,

At least for Farmer's Edge it is confirmed to be an associate.

If I had to guess, I would put Rocker in the same bucket.

"Share of loss of associates of $113 million includes our share of loss from Quess ($125 million, including a $98 million writedown), Astarta ($28 million), Farmers Edge ($22 million) and associates of our non-insurance consolidated investments Fairfax Africa ($74 million) and Fairfax India ($25 million). Offsetting this was our share of profit of Atlas ($116 million) and Peak Achievement ($34 million) and $11 million in net profit from all other 12associates. COVID-19 was a significant contributor to the losses at many of our associates during 2020 due to the global shutdown"

-

I am unfamiliar with Kennedy Wilson just knowing that its somehow related to real estate. Kind of surprised to see that voting machine didn't even gave it a heavier valuation with all the hoopla about real estate.

Any one had a take on this name KW ?

-

I tend to echo this point of view. I don't have any proof, but my gut feeling is that he never intended to sell BB back in Q1, even if there were no regulatory constraint. Totally, my gut feeling and completely unfounded. Maybe not for personal reason, but perhaps just for a vision that he wants to see through with BB .. and that vision cannot conclude by: saved-by-the-Reddit club.

However, if he were to resign next week from BB board, than I think selling the stake is in the cards.

Being on the Board of BB as an independent director, or owning a significant chunk of Resolute are supposed to be the "assets" that the FFH should be able to leverage; but sometimes i feel these are more "liabilities".

Then again, Prem W. built a +$10 billion business from scratch and has been investments and building businesses for decades; that is many fold more than me, and net-net he has been far more right than wrong, otherwise we wouldn't be here.

-

5 hours ago, hobbit said:

a) Fairfax financial gets paid in shares of FIH based on the appreciation in BV regardless of whether the shareholders of FIH make money or not. This BV is dominated by private investments which FIH mgmt is marking . A better way of doing this should have been to take the minimum of ( BV, share price ) and charge fees based on that so that fees only get paid when shareholders are making money too.

Thanks for the in-depth review Hobbit. You are a credit to the Shire; i admit i focused on the bit about the airport mostly.

On the incentives shown above, agree that the fees being structured on BVs (and not what the market ascribes) creates all kind of wrong incentives. That being said, as those fees are collected over time, there is an end line where FFH does well out of that paper investment based on what it can do with its marketable value rather than its accounting value.

-

There are two different things: (1) What is Prem pitching as a global thesis/story for FIH and (2) the reality.

The Modi debacle did hurt the (1) argument, however thankfully the reality matter more than an investment thesis/story pitched to investors on conference calls. Modi' ascension some years ago had, I believe, put India on a different trajectory. i.e. there is no going back to the way things were even without Modi in charge. So I think we are safe on that specific front.

Perhaps someone from the region can comment.

Market Disconnect is One of the Craziest I've Seen in 23 Years!

in Fairfax Financial

Posted · Edited by Xerxes

The F'ING MONEY IS THERE, (i.e. Stelco is on fire today) ... but we keep getting 80 cents on every dollar that we put in.

Need 20 cents more to make us whole.