SafetyinNumbers

-

Posts

2,812 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

A friend of mine (and very good analyst) thinks BIAL hits $500m in EBITDA as early as calendar 2027 and should hit it by 2028. On that basis fair value for the airport would be $10-15b. Assuming $2b in debt, that’s an equity value north of $50/share for FIH’s stake 12-18 months from now assuming a realistic multiple. Anyone have a different view on EBITDA? The multiple of 20-30x can be debated but it seems fair given comps and growth expectations.

-

Any reason in particular for the heavy volume today? I started a small position after the investor presentation because it seems like BVPS growth has turned the corner.

-

Equitg accounted for investments have grown significantly as a percentage of total equity investments. Essentially, as their balance sheet got bigger it allowed them to take bigger stakes and truly partner with management teams.

-

What size do you think they could do? Personally, I don’t think they will do another SIB b/c it means taking a break from the regular buyback and paying a premium. They have shown they can put over $300m for to work a month (March) and I think they have $2-2.4b to spend without getting creative. Maybe if the stock is a lot lower over the summer, they could defer the Allied World minority interest option that expires in September and buy even more back.

-

I think there is confusion between capital gains and earnings. The increase in the carrying value to fair value would be capital gains which is separate from Fairfax’s share of earnings. This only happens on the portion of equity accounted for or consolidated investments that are sold in which case the associated future earnings stream goes with it.

-

I prefer using the earnings and book value together. If all of Fairfax’s assets were marked at fair value, post adjustment forward ROE would be materially lower. That’s why a high ROE should fetch a higher P/B multiple. The relationship is exponential because of the compounding. I have four different methods to calculate intrinsic value. Two of them use book value. P/B (I use a conservative 2.5x) and the Buffett method, BV + insurance float.

-

At the AGM I came away thinking small and soon and it looks like that’s what we got. This suggests ~$1.6m for 13% so shouldn’t FIH’s share be bigger than $3.6m?

-

Allied World is marked at 6.4x P/E. With FFH’s P/B multiple of ~1.25x its 8x earnings which is about the same as Fairfax as a whole.

-

I think when Buffett says BVPS is not as relevant, I think he means that it’s not an indicator of intrinsic value on its own. It has to be taken in conjunction with ROE to determine a fair P/B multiple all else being equal. Fairfax has the benefit of turning over its equity portfolio which along with reserve releases means that BVPS lags IVPS. It’s why an investor should be willing to pay a premium as Fairfax is when it buys stock back.

-

I agree with this analysis 100%. If we were to adjust everything to fair value including the reserves, we’re probably trading below book value. I think the last cycle showed us how many reserves they could release when motivated. I think they were very motivated in 2013-2019 period to release reserves because hedging, low interest rates and the change in market structure impacted ROE dramatically. Currently, there is no reason to release reserves unless forced by the auditors. They can easily beat their 15% BVPS growth target over a FTM basis so there is no reason to pay taxes and reduce leverage. Meanwhile, they also use excess capital to reduce BVPS and increase forward ROE all else being equal. That should mean a higher terminal multiple. It also means it’s less risky than people think. The quants think the extra reserves is extra debt. i also think they are set up great if there is a big cat. People will sell FFH during hurricane season to avoid being long in case there is a bad one because of the hit to book value. Meanwhile, they not only have the reserves without the combined going over 100 but they will also be able to aggressively grow premiums. Strong premium growth will bring the momentum investors back and the multiple will start to increase again on accounting book value. Higher interest rates might do that too. Based on the low end of consensus Q226E EPS which seems very low given the Poseidon gain, the stock is trading below 1.25x accounting book value. How low can the multiple go? Given how quickly book value is going then how low can the stock go?

-

Has anyone built a model for Fairfax using RBC’s ROE framework? Is this something AI could build? It would allow for sensitivity analysis on combined ratio, investment yield (could be broken out between fixed income and equities) and tax rate. Everything else is pretty static.

-

I believe there is evidence to support my view. This is some pretty good evidence. It makes sense to frame it as an investment for a lot of reasons. One, there is no reason to forego the flexibility to exit and not do a buyback. Two, the accounting treatment is likely better than if it was considered a deferred buyback. Three, it signals to shareholders they think the stock is cheap. The sense I got from the questions asked about the TRS on conference calls and the AGMs over the years was that valuation is the trigger for taking off the TRS. It makes sense to me that it’s the outlet for buybacks when the stock gets above 1.5x BV. I think maintaining the investments to equity leverage is important to them. We’ll see what happens.

-

I think the notional value of the TRS can be added to debt and the share count reduced by the number of shares covered by the TRS.

-

I keep averaging up! My guess is he’s going to let the company do the buying for him. For the most part, I find investors ignore the equity portfolio but every 1% in capital gains is $10 in earnings.

-

Are you assuming they won’t be able to maintain the investments to equity ratio?

-

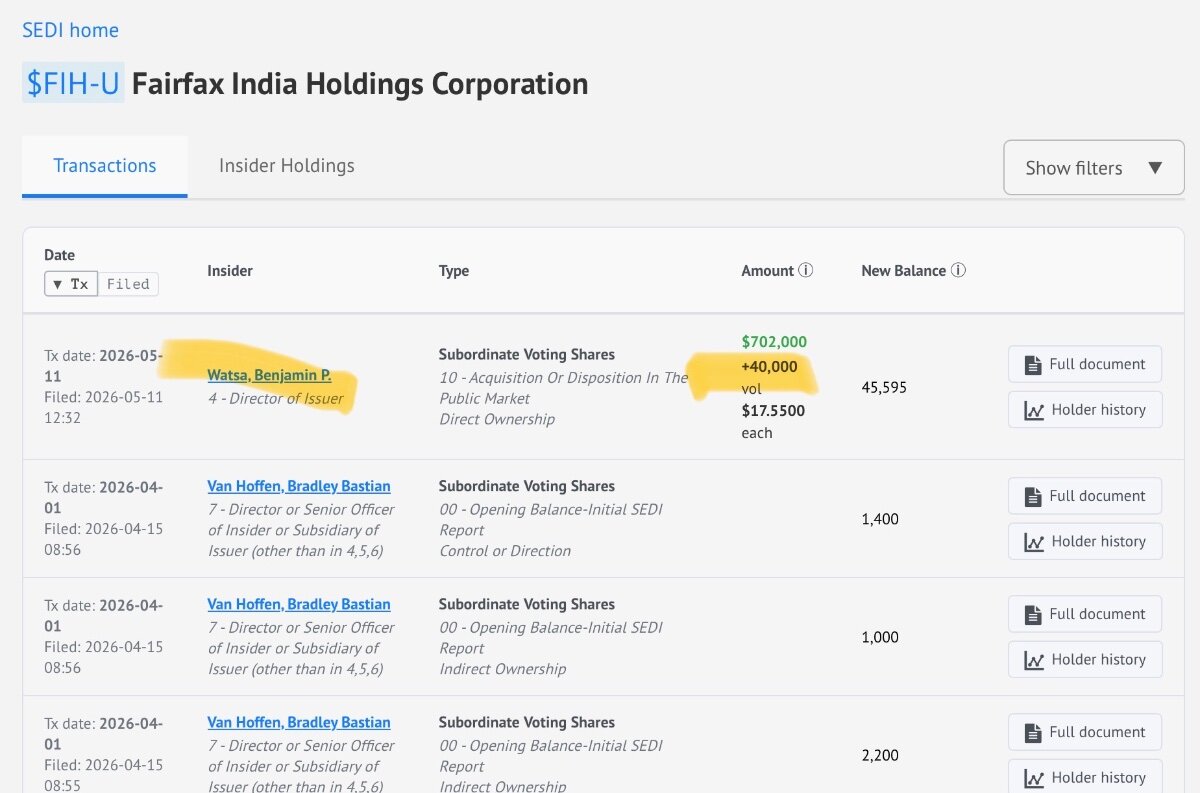

I missed this insider buy by Ben earlier in the week. He picked up 40k shares at $17.55 on May 11.

-

How do you think the softening insurance cycle impacts FFH results?

-

Who are the progressive, drunk, inexperienced FFH people here?

-

The key is a management team that takes advantage of the opportunity. Fortunately for us, unlike a lot of management teams, Prem, won’t take the company private and keep the opportunity for themselves which is a big risk in this market structure. Please see KW.

-

I consider that part of the market structure. Less demand, lower price.

-

I think it’s mostly attributed to the market structure. The big run up we had was because momentum investors piled in on the premium growth and interest income growth. The company was also aggressively buying stock which helped. The multiple peaked out at 1.69x BV in late July, the stock peaked in January off of the TSX 60 add. The multiple had already started to drop. Without the momentum buyers I think it’s hard to get multiple expansion. The company buys on down ticks and so do the type of value investors that would buy Fairfax. I’m surprised that there are still sellers at this multiple but the reality is that Fairfax’s float doesn’t turn over as much as most companies so it doesn’t take much to have an impact on price. I have been adding at 1.3x BV because I liked how aggressive Fairfax was in March on the buyback. I think that helps put a floor in on the multiple but of course the multiple might go much lower. I assume Fairfax will be even more aggressive at lower multiples.

-

I read somewhere the long term returns on the equity book was high teens. It’s been better the last 3 years but not all of this has hit book value yet because of accounting rules. It’s a big part of why I think the margin of safety is so high right now.

-

So you prefer higher growth but without the mechanism (leverage) that delivers it?

-

If you prefer lower returns just buy BRK or MKL. I think FFH trades at 40-50% discount to intrinsic value so I still see it as cheap.

-

I think that is conflating the insurance subsidiary capital with the holdco capital. They are turning stuff over in the insurance subsidiaries portfolios (i.e. making new investments) but also paying up dividends to the holdco to maintain the 3:1 leverage. Also, I don’t think it’s cheap because of poor investment decisions although that’s a common narrative. I think it’s cheap because of the market structure. The only investors that will buy on an uptick are passive and quants. Right now, we don’t have the quants because revenue momentum slowed.