orthopa

-

Posts

1,477 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by orthopa

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

FWIW the preferred volume across multiple issues has not been extraordinary as well as the common. If those two were liquidating it would take them months and months to get out. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

Looks like I was a day too soon :o I got some common and preferred today. Any news out? Both crashing again today. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

Now is a perfect time to pad positions with the upcoming events and both the common and preferred trading at lows. -

Its a lot harder to pick tops/bottoms then it is to find good companies priced at fair to (getting to good) prices. Im 100% net long and adding every month but also have ~30 years to retirement age. I find it a lot less complicated to do this then figure out all the working parts of an economy and where it is going. How do you guys get to the point where you think you are able to predict/estimate this with a reasonable degree of certainty?

-

Best account structure to invest for child.

orthopa replied to orthopa's topic in General Discussion

If you max the 529, you probably shouldn’t worry about not getting financial aid. There will be too much money for them to get any need-based aid anyway. That maybe true but who knows what college may cost, esp with room and board. It maybe $100k a year or more in 18 years. Like you said the 529 should cover the majority and some loans are needed she can learn the responsiblity that comes with that. If it was purely my daughters money that she put in I would be totally fine with her having access at 18, 21. It would just break my heart to have an account i built for her over time spent on a boyfriend or in a wasteful manner. I guess it just comes down to personal preferences and tolerances like anything else. -

https://docs.google.com/spreadsheets/d/1bA3Nv5YwiYIJ5Vdha1YrN3A_kyhF65N5LZvoskK86-c/edit?usp=sharing At the bottom there is a timetable. I pay ~26% taxes regardless of holding period and i calculated with a 1 year holding period vs. infinite holding period. If that is realistic is on another paper, and that is maybe the flaw in my thinking. Thanks for the response. That dividend income in your spreadsheet in your 60's and up is very enticing and ultimately my goal over time.

-

I have been researching the best way to save/invest for a child outside of a 529 plan. I plan on maxing out a 529 plan for my daughter but would like a way to invest money for her to use for a house downpayment/first car or preferably to just let sit and grow over her life time. I was under the impression that a custodial account or guardian account was a good option but apparently after some research it isn't. http://fairmark.com/custacct/regret1.htm These accounts count more heavily against college financial aid, 4 times as much and the tax break limits are very low. There is also the often unappealing idea of giving a lot of money to an 18 year old and what they will spend it on. It seems just having an account earmarked for a child and gifting either stock or cash from the account over time is the best way to go about this. Has anyone done something similar and have any experience or thoughts? Thanks

-

Thoughts on dividends -- do you care or not?

orthopa replied to Nelson's topic in General Discussion

I prefer dividends for most of my investments and strangely (probably not) my best returns have been from big dividend paying stocks mainly MO. I think the double taxation scares many people away as well as the assumption that management really reinvests the money at a higher ROI. I think managements ability to do so is very over estimated by investors and management themselves. Of course there are some outliers like Malone and Buffet but they are few and far between. It amazes me a stock like Altria is not celebrated or discussed more on the board. If its the moral aspect Im glad its not because its a waste of time but its returns with dividends invested rivals many of the great investments of all time. -

I think an argument against value investing can be the poll on the 2015 returns thread. More then half of the people were right around returns fore the market with ~75% who did close to what the market did or worse. I love finding good cheap stocks too but sometimes the boring obvious ones give the best returns. I have read very little about tobacco stocks on this site especially MO which has provided Berkshire type returns or better with dividends reinvested over time. I think many on the site dislike dividend stocks due to the double taxation. I like dividend payers and a year like last year was a perfect year for them.

-

BRK-B and BP.

-

Oil, wow, WTF happened to all of the oil bugs on this site?

orthopa replied to opihiman2's topic in General Discussion

This of course is just speculation but how much oil comes offline if SA gets involved in a full out war here? Will the Persian Gulf get closed? Im not young to remember but when IRAQ invaded Kuwait didnt the US navy keep the Gulf open? A couple sunk tankers and that will decrease supply real quick. With all the middle east news in the media and oil not reacting shows significant complacency. -

What fund manager/s would you choose to invest your money?

orthopa replied to feynmanresearch's topic in General Discussion

First of all, people should not plan to use money they invest in stocks for holidays. They probably should not even plan to use it for bigger house, but that's more of a "depends" situation. If I had a significant amount of money, I'd be living from it (and not working), so losing a lot of it would impact the lifestyle a lot (force me to work again, plus I can't replace lost money easily by earnings). I am talking portfolio of $10M+ here. If I lose little money, it is actually rather easy to replace it by working. I am talking portfolio of up to $200K or so here. Between $200K and $10M is a grey area. As you go up through it, it gets harder and harder to replace lost money by working&saving. It is also getting harder and harder to get to the next step by just saving + having a conservative portfolio. So there's a tension between the two and IMHO that's the area where it is important to invest for outperformance. You may disagree, although it seems that you are too emotional about it. ;) BTW, if you go over $30M or so, you are right, you get back to "you can afford to lose a lot without any impact on your lifestyle" zone. Of course, it depends on individual circumstances and all that. Take care So very true. Saving in a small portfolio can make it grow quickly or at least seem that way. Get a substantial amount of money and a bad month in the market can wipe the equivalent of months of savings. The flip side is though good performance really starts to become noticeable as it grows. -

Was going to ask this myself. Couldn't you just subtract total funds added and calculate percent chance from there? any money you make or lose from funds you have added should count for or against total returns right? What's interesting from the poll is as much as we try to beat the market the great majority of portfolios on the website seem to have returns very close to the market. And this site is full of very smart people.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

That's the way the documents read. The $188B the U.S. has put into F&F entitles the U.S. to receive 10% per annum on cumulative preferred shares. Those accumulating dividends that have not been paid compound at 10% per annum, adding to what is owed the U.S. Pro forma, what would be owed the U.S. annually without the sweep is considerably more than $18.8 Billion, and the mountain of arrears in addition to the $188 principal amount is growing at a rate of 10% per annum as we speak. So that's what I was hoping to tease out with my question. Why would the dividends accumulate but for the sweep? Because but for the sweep, the companies were making tremendous profits (even aside from the mountain of non-cash DTAs that were recognized because of that profitability). And the non-2013 profits above understate the companies' cash earning abilities because the DTAs would have kept cash taxes low, which means even more dividend paying capability for the GSEs. Alternatively, I suspect that, to the government, trading DTAs for dividends is probably just as good to them as cash, but that's a leap that doesn't need to be made because cash profitability would have been enough to continue to pay the $18B in dividends. Am I missing something here? Do you have a link to this? I'd be curious to see who that might have been. It looks to me that any settlement is going to have to come from the Administration because the Treasury holds the GSEs by the balls via the covenants in the SPSPA, and I'm not optimistic that this Administration would be willing to make any move unless forced to do so by some development in the legal courts. (Which is why I was asking for the reason you think a settlement might have been in the works.) I think both Pelosi and Reid both issued statements several days ago back pedaling on their previous opposition to any deal that would give something to the public preferred holders or the common holders. When that happened it looked like there might be something nice in prospect for public preferred holders, and I considered getting back in for our fourth possibly multi bagger round trip. However, the Jumpstart bill seems to throw a monkey wrench into the works. With the loss from their balance sheet of the funds taken in the sweep, dividends would not prudently be paid to the public preferred holders until that balance sheet is rebuilt. Profits are now normalizing for F&F, and their latest year's earnings don't even provide enough to pay the annual dividends on the U.S. preferred,according to the chart. Does anyone think the Administration is going to return the swept profits to F&F and restore their balance sheets? In an election year? Would that help their election chances next fall? If the answer is yes, well --- there's this bridge over an important river I would like to sell you. I am not seeking confirmation of my latest view. I would be delighted to hear a credible way the administration can cut a deal now that is favorable to preferred holders. Well theoretically there are 2 ways this can work out for shareholders. 1. The administration sees enough evidence or tries to save face and settle. 2. Gov is forced by court decision to work out settlement or return funds. This of course could be appealed but if any of the courts find the net sweep, delaware preferred law illegal etc funds have to be return regardless of the omnibus bill, what the administration thinks etc correct? It may not be this administration but eventually whoever is the president may not have a say in what $$$ is given back and how much. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

I find the whole thing fascinating and wish I had more to add other then just speculation. FWIW it appears going forward all the court cases can do is push FNF more towards a release/settlement/recap etc, etc. Unless of course there is a big set back but at a minimum Sweenys court and the Delaware court seem very promising. This investment for me is still either still a moderate to big win or a complete loss and even with my limited legal knowledge I'm still OK holding with what has transpired. If anything I'm more interested now that the price has dropped. I didn't expect a settlement soon and I'm Ok waiting till 2018 if need be. -

Looks like Visa is getting into tokenization http://www.bidnessetc.com/59298-visa-inc-brings-token-service-to-asia-pacific/ http://www.mobilecommercedaily.com/visa-introduces-token-service-to-top-off-mcommerces-fruitful-year

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

Seems like there have been some pretty good developments for shareholders but the market has paid little attention. Hard to believe all of this is flying below the radar. Market must sick of trading on hopes and wishes, traders at least that is... -

I have eaten there. Dont see the surprise in the E coli breakout. When you fertilize naturally and organically you use manure instead of fertilizers. There is e coli in shit.

-

Wireless Carrier Poll - Who do you use?

orthopa replied to LowIQinvestor's topic in General Discussion

Sprint, I phone 6s. $70 a month for unlimited, text, data, phone. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

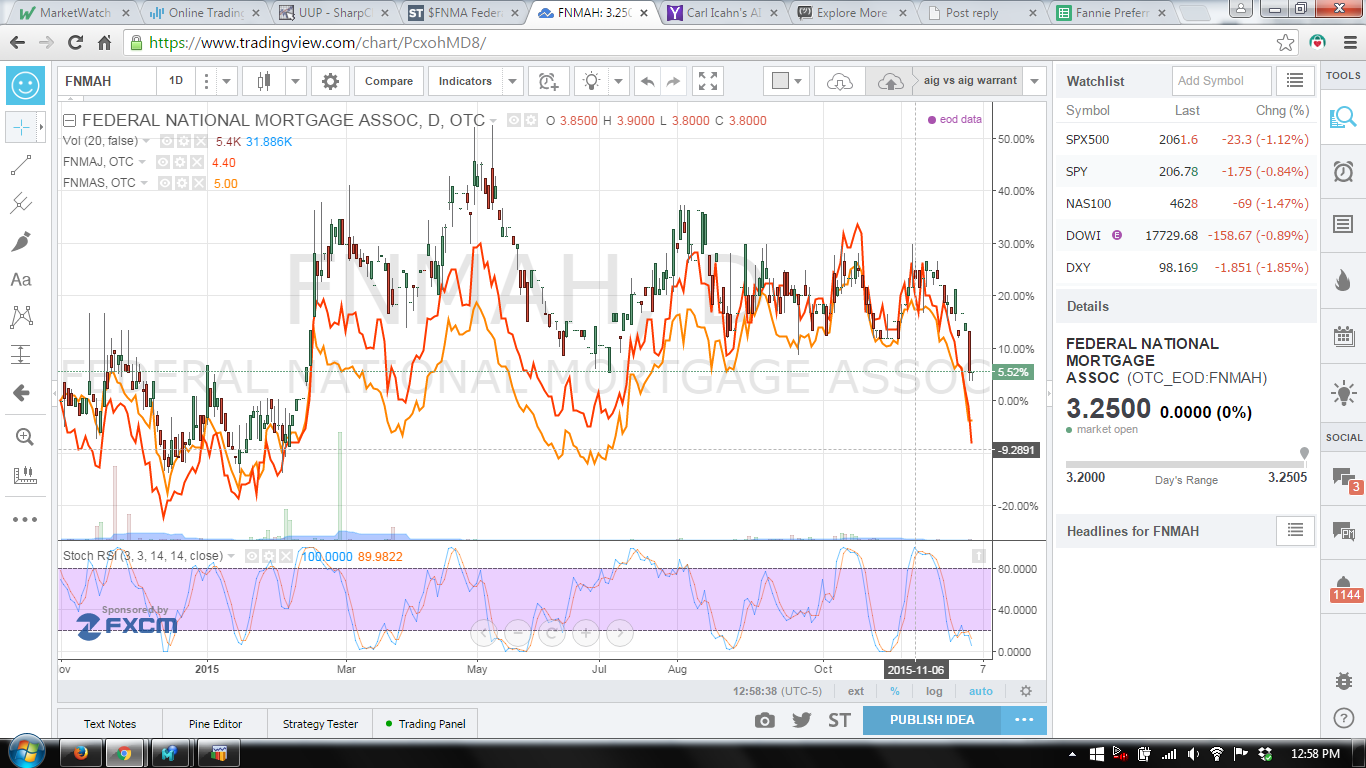

Common way down today, some of the preferred too, FNMAS seems to have lost some of its premium compared to other preferred over the last little bit. I added some FNMAJ today.

-

This out today and seems pertinent. http://finance.yahoo.com/news/why-apple-wants-unprofitable-world-130003755.html Looks like the article thinks ATM companies and companies that deal in cash are at risk the most but then at the end says Visa could lose market share. This all depends on significant user uptake by Apple Pay users which is down 50% on black friday compared to last year at 2.7% of transactions. Visa didnt respond for comment but at a minimum this inquiry should get them aware of the risk.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

orthopa replied to twacowfca's topic in General Discussion

I think there is no doubt the depositions hold that info. Probably why many documents have been redacted and why some info would cause "instability in the markets". I would have to imagine the Fairholme lawyers know by now what that person is. -

Exactly, you need these people to care enough to switch. Using a card is not difficult enough to make people switch. If anything its emotionally much easier then paying with cash.

-

Who pays $1.50? The customer doesn't correct? The business does. If that was the motivating factor the business would get rid of V/MC and advertise google pay not the reverse. What about everyone who shopped thurs/fri for black friday? Do you think everyone had the cash to pay in cash for the items they wanted? If not those people need some form of credit/banks and the banks take a nice chunk of the interchange fee so they are not in a rush to get rid of that $$$. Again like I said you have to get consumers to care enough to switch to divert the payment of money from banks/V/MC to the retailers etc. Using your credit card is not hard enough for the consumer to want to switch. A fair amount of people in this thread didnt even know what fees went to what parties and these are investors who think about this stuff. Not your common everyday consumer. As I have said before getting the expensive item you want NOW on credit is a lot cooler then waiting to save up and use google to pay. Unless banks have similar margins in a new system I can see them protecting V/MA's moat in trying to keep the status quo.

-

I guess I just don't understand your point why its a must that you pay in full for something or not others, and if your argument is that the same service can be provided at a lower cost or zero cost why does Apple/Google/chase, BAC, C, etc want to get into a zero margin business? Why do they care? The loan is the same either way like you said. Same digital currency. How are you going to explain to this "young generation" that they are to use P2P for stuff they can afford and credit for others? Its either one or the other in my mind because people especially young Americans want stuff they cant afford and usually find a way to get it. Secondly in paying $4 for $3 how is that any different then any type of loan with interest? Thirdly how many people don't care if they pay $4 for $3. (Sometimes I think we forget how we think about $$$ on an investing/money conscious message board).How does Apple or Google market P2P as a way to not pay interest for every day expenses when that same person is spending hundreds of thousands in interest for a house? If we lived in a society where people saved 80-90% of the cost of a house, paid cash for nearly all items I can see the attractiveness of P2P. America/world is no where near that outside of maybe China but policy there now is pushing a consumer society, ie more debt. Ultimately the consumer has to drive this and it has to make the purchase and the satisfaction of the process way more desirable then using a credit card. I just don't see this happening, especially with cash needed up front. In regards to little to no fees for the merchants P2P is no doubt the better way to go to save 2-3%. But as a customer why do I care if walmart, or target or anyone else gets dinged on each swipe? I want my purchase now or as fast as possible. You need the consumer to care enough to use Apple/Google and in turn making margins better for everyone else involved in the transaction right? Compress those margins! Do you honestly see the young generation as you put it giving a crap if are helping lower margins? Im rambling here but I guess you could see advertisements like this... Switch to Apple/Google ****P2P to help lower margins and fees target/walmart pays with the cash you already have!!! OR Stay with Visa/MC and we will give you 5% cash back and or points you can use for FREE stuff. The more you spend the more FREE stuff you get!!! With this are the competing advertisement I take Visa at 30x earnings all day long.