cdogstu99

-

Posts

22 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by cdogstu99

-

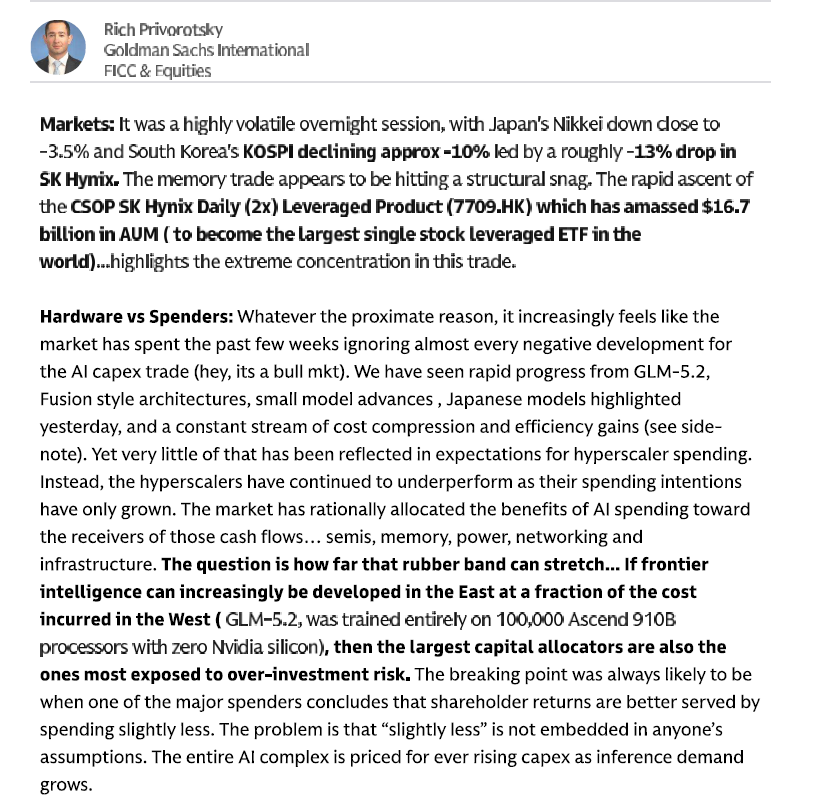

ahhh...ok....now i get it, thanks for being upfront about this....

-

what exactly is Privo ---he didn't quote Privo or anyone for that matter, so he seemed to be passing off as his own writing.

-

i think yesterday? and given your knowledge on the space i was having a hard time believing YOU copied them....so wow, that's pretty messed up but at the very least a nod to you my friend.

-

-

i really like reading your stuff, but either Goldman ripped you off, or you ripped them off....not sure which is which but should at least disclose sources....

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

cdogstu99 replied to twacowfca's topic in General Discussion

Yeah but my initial starting point of $2 in EPS already accounts for that Treasury Stake. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

cdogstu99 replied to twacowfca's topic in General Discussion

I'm trying to think of this as simply as possible, because when I focus on the minutae I get completely sidetracked. But with that said, if this deal follows the Moelis plan even 75% of the way, then I think the common shareholders do just fine. Please let me know if there is anything OFF about this simplistic way of viewing this. Right now Fannie is generating on average about $10 Billion in Profits per Year. Ignoring any ownership details, and assuming a 10x multiple on profits, this is an enterprise that SHOULD be worth on average about $100 Billion. We know that they need probably around $100 Billion in Capital. Take the Moelis 3% requirement times the credit exposure and that's what you get. The way I see it playing out assuming a close resemblance of Moelis plan and AIG recap is something like this: June 2019: Announce Exit From Conservatorship June 2019 + Turn off NWS with a Two Year Plan to Release FNMA and FMCC Sept 2019: Treasury Agrees to Equitize their Junior Preferreds, Hopefully at a Discount Similar to AIG Jan 2020 - Raise $25 Billion via IPO (this timing is representative of comments made by Calabria) June 2020 - Follow on Offering Raise another $25 Billion Sept 2020 - New Junior Preferred Issue $30 Billion June 2021 - By this point you have retained earnings of around $20 Billion + $80 Billion in Raised Capital. Done. Assume over the course of two years Treasury is also liquidating stake - note AIG did this in six various offerings so could take some time. But Simplistically Speaking.... If I have a company that absent the sweep is worth $100 Billion, if they raise an additional $100 Billion, as a standing shareholder, I am diluted by 50%. Thus a $3 Share in FNMA today SHOULD be worth around $20 (assuming roughly 5 Billion Shares at $2 EPS (10 Billion in Profits) assuming that the net worth sweep is abolished. Dilute by 50% and you get to $10 a share. Thoughts? -

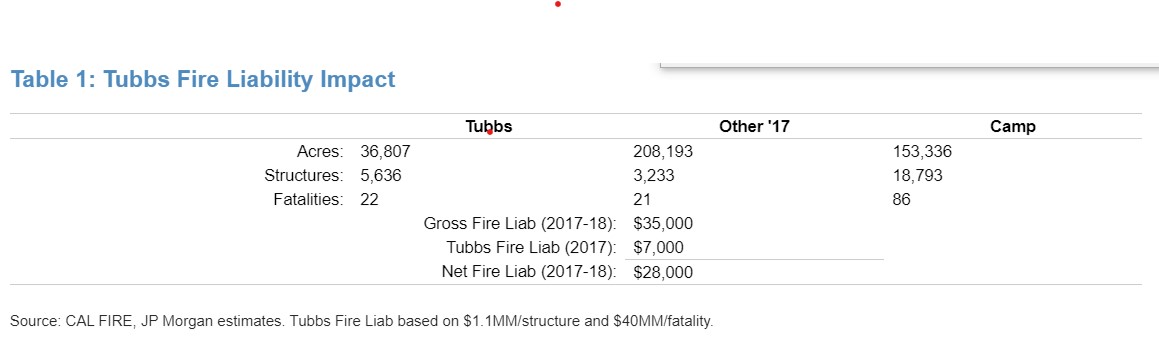

don't think that's right. here's chart from jpm

-

Nice

-

I think it all looks interesting for sure..even with a stake in the game, i'm finding this all fascinating to follow. The morgan stanley note was interesting in that they mention the ch 11 filing could be challenged, given that they are potentially solvent. I'm pretty sure PG&E is just filing in order to get the state to reverse the inverse condemnation laws, since fundamentally the company is in good shape, ~$6 Billion in operating income on average per year; if they were able to stretch out any claims against them over the course of several years, while somehow adjusting the laws so that they don't get screwed on any future fires (while at the same time cleaning up their sloppiness) they would be perfectly fine. I also find it interesting that at the source of the Camp Fires from 2018, PG&E found bullet holes at the transmission pole. https://www.cnn.com/2018/12/13/us/pge-camp-fire-report-outages/index.html Now the big problem here, is that it will probably be a while- at least a few months I think - before they actually determine the cause of that fire, but can you imagine if someone was just taking target practice at a few poles and ignited the fire? Totally possible. Again, not likely to help them stave off bankruptcy, but certainly a homerun wild card moving forward.

-

i think you are right, fidelity said as long as the stock is trading, nothing changes, so in this case it would probably be a while if ever that PCG is actually delisted. I unfortunately didn't close the options yet (UGH) but still well positive, but about half of what I would have made if I sold when I actually should have. Still a lot of moving parts, so hoping for some more good news before my expiration.

-

hey guys, i bought a few call options before the pop on PCG that expire on Feb 15th. Do you guys know what happens to options with a company that is going into bankruptcy? Do i need to sell them before the 29th? I see that Sears still has options on its stock so I'm thinking i might be okay to hold on. I probably should have sold when the stock got over $14, but I was getting too greedy--ughh!