Parsad

-

Posts

16,250 -

Joined

-

Last visited

-

Days Won

64

Content Type

Profiles

Forums

Events

Everything posted by Parsad

-

Norm Rothery did a terrific writeup on the Fairfax events for Moneysense magazine. Norm works tirelessly with me to help put all of these events together, so give him a hardy thanks! Wonderful article and I'm very pleased, that along with Fairfax, we've put together something quite fun and special for investors and shareholders. Cheers! http://www.moneysense.ca/invest/stocks/highlights-from-fairfax-lollapalooza-2015

-

Hey, Sanjeev: Is that a typo you had there, free refreshments for everyone? ;D Soon it will be free parking once we have $2,000 per share! LOL :) Yeah, it's just water, soft drinks and glasses full of ice. Just so people can mingle and relax between George's conference and our dinner. Feel free to donate to CCC if you would like, but I am covering this cost. Cheers!

-

This works on all of the browsers. All you have to do is click "Post" and it will post. Just don't hit "back" or anything, otherwise then you lose the post. Cheers!

-

Why did Warren Buffett buy Berkshire Hathaway?

Parsad replied to SCMessina's topic in Berkshire Hathaway

I remember meeting this gentleman on a flight from Dallas to Omaha about five years back. He was about 90-95 years old, half-blind, but very engaging. He was going to the Berkshire Hathaway meeting. Lived in Dallas, but had a farm in Omaha and was a long-time shareholder. I asked him about his farm..."Ohhh, I bought it many years ago...about 50,000 acres!" I asked him how long he's been a shareholder..."Oh, I owned it before Buffett got involved. My broker accidentally bought me 5,000 shares when I asked him to buy something else, but he thought this was a better investment." What happened...did you keep the shares? "Yeah, I ended up keeping them. I gave my idiot son 500 shares ten years ago, but he sold them, but I kept the rest of them!" And the broker? "Oh, I fired him right after he bought me the stock and told me what he did!" Did you ever see him again or thank him years later? "Nope!" as he chuckled. So why did Buffett buy Berkshire? Perhaps serendipity. Maybe it was a mistake for Buffett to buy Berkshire, but maybe he would not have turned Berkshire into what he did if he had sold it or bought something else. Thank goodness he made the worst mistake of his life by buying Berkshire! Cheers! -

The pre-dinner meeting on April 15th is in Salon 1 of the Fairmont Royal York on the 19th Floor from 3pm to 6pm with free refreshments for everyone. Cheers!

-

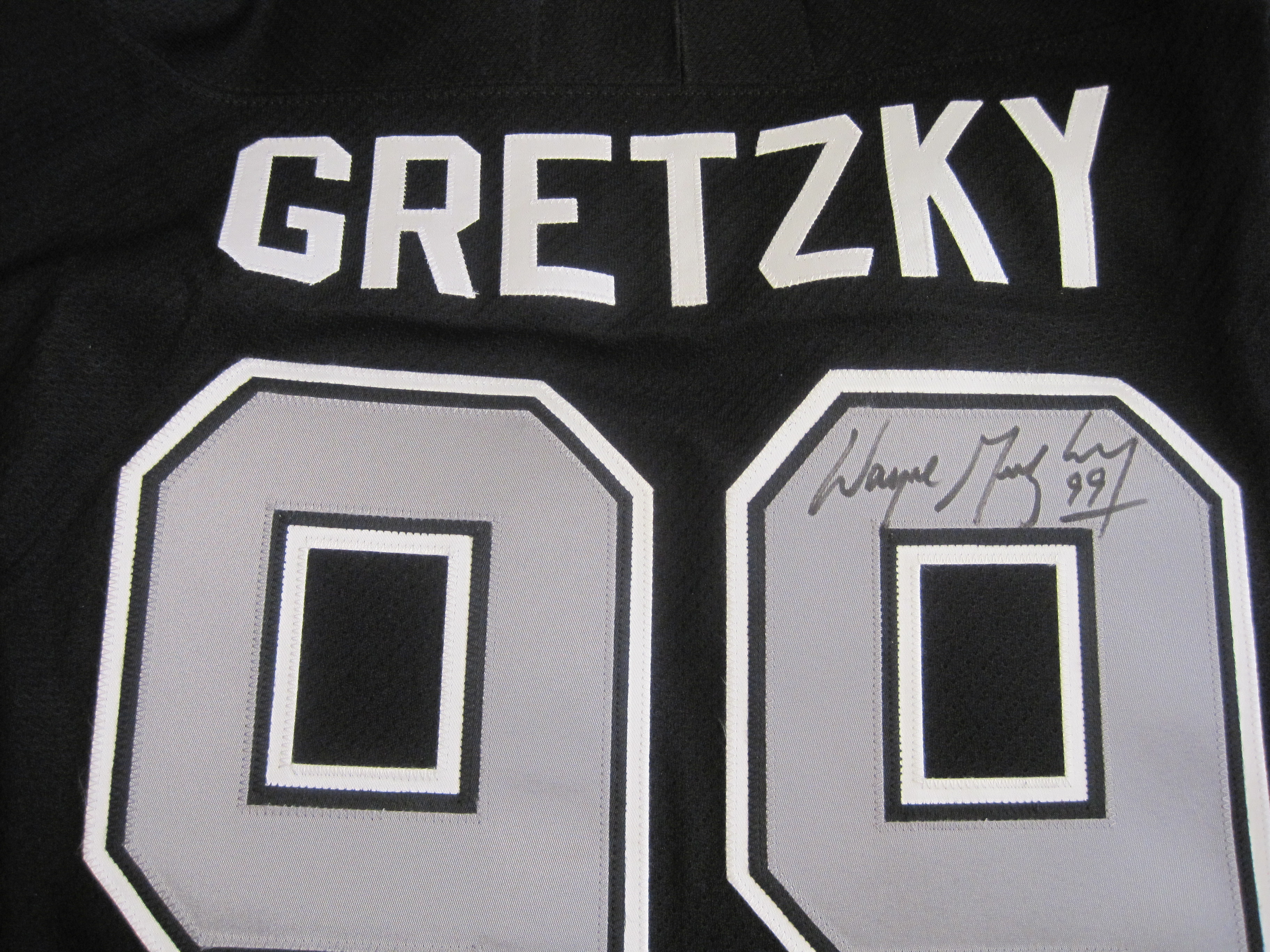

Hi Folks, Last chance to buy tickets to our 10th Annual Fairfax Financial Shareholder's Dinner which occurs Wednesday, April 15th at 6pm in the Imperial Room at the Fairmont Royal York Hotel in Toronto. www.cornerofberkshireandfairfax.ca - scroll down a little and you'll see the ticket box on the left hand column We also have a few fantastic new silent auction items that Fairfax was able to arrange: - Wayne Gretzky autographed Edmonton Oilers Jersey w/Certificate of Authentication - Wayne Gretzky autographed Los Angeles Kings Jersey w/Certificate of Authentication - Milos Roanic autographed gift set w/includes a racket, shirt, bag and photograph...all signed by Milos! The Edmonton Jersey will begin the auction bidding at our dinner and end at the Fairfax AGM. The jersey will be at the table where I hand out the Templeton Foundation books at Fairfax's AGM. A special person will be waiting to award the jersey to the highest bidder! Cheers!

-

10th Annual Fairfax Financial Shareholder's Dinner - Updates!!

Parsad replied to Parsad's topic in Fairfax Financial

Again to reiterate on changes to the dinner: - Now in the Imperial Room on the Lobby Level - Nametags at Registration Table in Foyer of Imperial Room - Doors open at 6pm - Dinner / Presentations begin at 6:30pm - Guests arrive at 8:30pm-8:45pm for Q&A - Bring your credit card and cash, as we will have some terrific silent auction prizes! Pre-Dinner Gathering - 3pm to 6pm in Salon 1 now on the 18th Floor - Complimentary refreshments Cheers! -

How does a value investor go about buying a automobile?

Parsad replied to SmallCap's topic in General Discussion

I agree with FFHWatcher in terms of logic on how you spend on a car...whether you have a large capital base/income or small capital base/income. In other words, even if you are younger and have a small capital base/income, then you would allocate a more modest amount into a vehicle than someone with a larger capital base/income. FFHWatcher may buy a $50-60K car. Someone younger with a smaller capital base should probably allocate around $15-20K. I have no hard and fast rules. I liked the new Jeep Cherokee, so I bought one new, but not without haggling at a number of dealers and then having the winner throw in a couple of things free like a flat screen tv and unlimited car washes. The other car I bought, a Mercedes B200 Turbo, I simply kept going to a couple of dealerships on a Saturday for a couple of months...just watching what they had in inventory. Of the cars I liked, the one that kept sitting out there each week...the dealer kept dropping the price because it wouldn't sell...that's the one I went and bargained hard for after about 2 months. I got it for a song and it runs beautifully! The bottom line though is I cannot buy anything without haggling a bit, or looking for a discount or coupon...I don't like paying retail. So, I would say there are no hard and fast rules about buying a car, but the biggest would be that you are buying something you can comfortably afford. If you don't know anything about cars, then I would recommend CONeal suggests...buy new, but what you can afford, and then drive it until the wheels fall off and the body rusts. Cheers! -

Nothing nefarious in their motives, so the "red-flags" issue is irrelevant. They've taken a teaching approach in their presentations...to share the knowledge they've garnered from their experiences...and it just means a lot of exposure to a lot of students. Cheers!

-

It's been a couple of years since I last spoke to Francois, but my opinion would not change about him. He's an honest, good guy and a good investor. He has a good team as well. The one caveat I would give, and I always give this...doesn't matter who the manager is: In examining a manager's long-term results, I never look at what he did managing his personal portfolio, or money for family or friends. It's not the same thing...not at all...not even if it is audited. Managing capital from people you have more than an arms-length fiduciary responsibility to is completely different. Why? Because your parents and your best friend's Mom or Dad most likely won't pull the capital from you...and they also won't question you when you put 100% of it into Berkshire Hathaway or some other company. So whenever I see personal portfolio or family/friends data incorporated into long-term results, that caveat always comes to mind. That being said, Francois has still done very well if you exclude the 1993-1998 years...so the caveat is somewhat irrelevant in this case. Cheers!

-

It's not a particularly good article, and while some things are inaccurate, some of it is accurate. I would suggest this fed off or is reporting the Groveland party line. What I'm disappointed with is not that Sardar is finally being taken to task, but that the task master leaves a lot to desire as well. I'm not impressed by Groveland's proxy other than the fact they had the balls to do this with such a tiny stake in BH. Cheers!

-

You quote Carnegie, but the Janitor did exactly the same thing as Carnegie...donated his wealth to the local library and community. Perhaps, he was influenced by Carnegie...perhaps he was just a frugal old man who loved investing the way others love crosswords...perhaps he was lonely and selfish. No one really knows unless you know the man. For us to comment like we are doing is a lazy simplification of his life. Cheers!

-

Presentation at Google! Dynamic Duo...good stuff, but you guys need to be careful of getting too much exposure. You don't want people to start becoming de-sensitized to the message. It's why the Rolling Stones only tour every three-five years! ;D Otherwise you become the Grateful Dead and their Deadheads! Cheers!

-

Hi Folks, Due to changes at the Royal York, our dinner has moved to the Imperial Room on the lobby level floor. What that does is give us a far bigger venue and we have plenty of seats available. If you are on the waiting list, or were not interested in buying tickets because we were sold out, the Paypal button has been added back to the home page site on the left hand side: www.cornerofberkshireandfairfax.ca Select the type of ticket you want, and click "Buy Now"! Please review the updated details below for the dinner. Cheers! 10th Annual Fairfax Financial Shareholder’s Dinner CMC Fairfax Financial Shareholder’s Dinner Imperial Room - Main Lobby Level Wednesday, April 15th, 2015 Fairmont Royal York 100 Front Street West Toronto, Ontario (416) 368-2511 Presentation Only - $100.00 CDN Presentation & Expansive Full-Buffet Dinner - $200.00 CDN Cash Bar If anyone is interested in corporate sponsorship of prizes, or any donors for prizes, please contact me at [email protected].

-

Generally, they do read many of your posts...especially about Fairfax! Getting a Ping-Pong table into Roy Thomson hall is easy enough, but I'm not sure how the dynamics would work. It would be more suitable for a more relaxed atmosphere, like the way Berkshire does it in Regency Mall in front of Borsheims. Cheers!

-

Prem watsa investing style. Ben Graham vs John templeton

Parsad replied to caprivenky's topic in Fairfax Financial

+1! Remember Buffett was a fan of Phil Fisher as well. He also tried technical analysis when he was younger. I think the best way to view any investment manager is as an amalgam of their readings, life experiences and circle of knowledge they've developed over time. They may be heavily influenced by a handful of people, but they are far more than just that. Cheers! -

It's an unfortunate securities loophole he's exploiting. For example, in Canada the exchanges will not let you issue shares, even via convertible debt, below $0.05 a share. So, you cannot do this. It would be very easy for U.S. securities regulators to stop this practice. Cheers!

-

Guy Spier and Mohnish will be speaking to MBA students at The Stanford Graduate School of Business in a joint session on Monday, March 16 from 12:15 to 1:15 PM (Room C106, 655 Knight Way, Stanford, CA). If you'd like to attend, please drop a note to [email protected]. They have very limited seats for non-Stanford students. First come; First served! And then they are on to TED 2015 in Vancouver!!! Cheers!

-

+1! I can tell you exactly why I'm fat and overweight. It has nothing to do with sugar, gluten, etc, but the fact that I do not eat a balanced diet and do not get enough exercise. You eat too many calories and don't exercise at least three times a week, your body will slowly, if not over years, become unbalanced and your health will deteriorate. It's as simple as that! Not that sugar is toxic, or whatever smoke people are blowing up your ass these days. Anything in a large enough dose will kill you...even water! Your body is self-regulating and a prime piece of technology...to call it a marvel of engineering is an understatement. Yes, processed foods over the years have increased the amount of sugar and sodium levels in them. But it all still comes down to a balanced diet, watching your total caloric intake and a moderate amount of exercise. Those three things will take care of a whole host of other ills. 15 years ago, scientists and doctors said you shouldn't consume more than a few eggs a week. Now, doctors and scientists are saying that eating a couple of eggs a day isn't an issue. Red meat, coffee, sugar, salt, butter, alcohol, and whatever else go in and out of favour every decade. The real problem isn't sugar or fat, but the sheer size of the portions we get these days. It all started with Big Gulps and Supersized...7/11, Costco and McDonalds should all get the same amount of blame! If you went to a restaurant 20-30 years ago, their dinner plate is today's appetizer plate, and today's dinner plate can hold twice as much food as back then. A Big Mac used to be the biggest burger you could eat when I was a teenager...today it's about the same size as a fully-loaded "L'il Buddy Burger" at Five Guys! That's the little burger at Five Guys...the one children order these days! Even if you order something healthy at a restaurant, the portion size is huge. So while you may be eating a nice salad, the total caloric value of that salad may be well over 1,000 calories. A 7 oz steak, with vegetables and mashed potatoes is healthier and less than 2/3rds of the calories. You could add a Coke and still come in under the salad. And then you have all of the food porn that people love! Inundated with food culture, and the fact that acquiring food gets easier and easier, while lifestyles are more and more sedentary, you can easily see why the world is becoming fat...and it isn't due to the sugar, salt, fat or gluten. Cheers! Sanjeev, You are right about your circumstances and what we should be doing to trim down, but in a strange way we may be unwitting victims of an alien invasion. No, this isn't about spooky invasions of aliens from other planets or graveyards, but about aliens all around us and even inside us. Yikes! That sounds even weirder, but it's true! We all have hundreds of species of bacteria living inside us in our digestive tracts and especially in our colons. These are continuously fighting against each other for living space and dominance. When we eat a diet that is mostly wholesome whole grains, vegetables and fruits, an amazing thing happens after a period of time. Certain types of bacteria will take over most of the space in our colons. These are the ones that like to feed on the fiber and larger molecules of resistant starch that are part of a mostly plant based diet. When that happens, there is an amazing transformation. The products of that beneficial biome release substances that are absorbed through the gut and have great health benefits throughout the body. One of those benefits is to suppress excessive appetite and to predispose us to enjoy the same whole grains, fruits and vegetables those types of bacteria like. If we continue to eat those foods the undesirable competitors of the good bacteria won't have available the different type of food from our diet that they need to mount a counterattack and re conquer the territory. Then, we are in the sweet spot. We now like and enjoy those foods that are good for us as we benefit from the positive feedback loop from the colon with the good bacteria that release beneficial substances throughout our bodies. The diet that once seemed so hard to transition to is now very easy. But wait, there is more! We have lost a lot of extra weight, and it is easy for us to get up out of our chairs and move around. We realize we have begun to enjoy taking walks; so we walk a little farther. That nagging pain we used to have in our feet is getting better as our feet don 't have to bear as much weight. Then, we may do something we haven't done in years: we begin to jog a little bit. And the feedback loop goes around and around as we get more and more healthy. I totally understand the bioflora residing in our colon and how that affects our health. But my main point was a lot of the problems with the car can be fixed by simply making sure the battery is charged, brakes aren't rusted out from sitting still, and the engine is revved from time to time. Everything else is the fine tuning of the engine...using better gas, oil, washes, detailing, etc. If more of us just did the basics, that would change a lot of things...I'm as guilty as anyone on this matter! :-X Cheers!

-

+1! I can tell you exactly why I'm fat and overweight. It has nothing to do with sugar, gluten, etc, but the fact that I do not eat a balanced diet and do not get enough exercise. You eat too many calories and don't exercise at least three times a week, your body will slowly, if not over years, become unbalanced and your health will deteriorate. It's as simple as that! Not that sugar is toxic, or whatever smoke people are blowing up your ass these days. Anything in a large enough dose will kill you...even water! Your body is self-regulating and a prime piece of technology...to call it a marvel of engineering is an understatement. Yes, processed foods over the years have increased the amount of sugar and sodium levels in them. But it all still comes down to a balanced diet, watching your total caloric intake and a moderate amount of exercise. Those three things will take care of a whole host of other ills. 15 years ago, scientists and doctors said you shouldn't consume more than a few eggs a week. Now, doctors and scientists are saying that eating a couple of eggs a day isn't an issue. Red meat, coffee, sugar, salt, butter, alcohol, and whatever else go in and out of favour every decade. The real problem isn't sugar or fat, but the sheer size of the portions we get these days. It all started with Big Gulps and Supersized...7/11, Costco and McDonalds should all get the same amount of blame! If you went to a restaurant 20-30 years ago, their dinner plate is today's appetizer plate, and today's dinner plate can hold twice as much food as back then. A Big Mac used to be the biggest burger you could eat when I was a teenager...today it's about the same size as a fully-loaded "L'il Buddy Burger" at Five Guys! That's the little burger at Five Guys...the one children order these days! Even if you order something healthy at a restaurant, the portion size is huge. So while you may be eating a nice salad, the total caloric value of that salad may be well over 1,000 calories. A 7 oz steak, with vegetables and mashed potatoes is healthier and less than 2/3rds of the calories. You could add a Coke and still come in under the salad. And then you have all of the food porn that people love! Inundated with food culture, and the fact that acquiring food gets easier and easier, while lifestyles are more and more sedentary, you can easily see why the world is becoming fat...and it isn't due to the sugar, salt, fat or gluten. Cheers!

-

I'm sorry, I don't go on these boards often. Who's Sanjeev? I wouldst be Sanjeev...thy Lord of the message boards! Do not use my name in vain, lest thee be banned hence forth. What username did you want instead? Cheers!

-

Too early to say that. If China slows further, deflation will increase. Cheers!

-

+1! If anything should perturb investors, and I think to certain degree this was a royal f**k up because they were so conservative, but the hedges cost us a lot. They were just way too early with them. Equity prices were cheap, the hedges had limited upside at the time, and the only reason they needed them was because any significant drop in their equity/bond portfolio would have been magnified by the amount of asset/equity leverage they use. You can't fault them for their conservatism, as the world was falling apart...but They would have been better off holding more cash and no hedges, or maintained a lower ratio of leverage. Cheers!

-

Ben's a terrific choice! Prem's wife Nalini would have been a good choice too. Cheers!

-

First of all...Prem is not Buffett. No one is Buffett, except for Buffett. It's a moot point, because there is no one like him...period! Second, Buffett no longer invests like he did when he was younger...Charlie had a lot of influence on him...he's no longer a pure Ben Graham investor. Can anyone say that BNSF was an investment Graham would have made when Berkshire bought it? Yet, it has turned out spectacularly well. Fairfax and their team are pure Ben Graham investors. They will buy out of favour, distressed assets that other people don't give a damn about. They will make 10-12 investments and 1-2 of those will go to zero or there abouts. But they will hit home runs on another 4-5, while 4-5 will be modestly higher, lower or flat. That's how they operate...average in, average out...and hopefully your analysis was correct on a good chunk of your ideas. There's nothing complex or hidden that you are missing. They have a team of people who invest the capital...some of those team members will get their analysis right on an idea, and some will get it wrong. No different than Todd Combs or Ted Weschler looking after some of Berkshire's portfolio and getting things right or wrong relative to Buffett. It's not about questioning someone who looks after your money. Everyone cares about their own money as much as you do. But I've noticed that the ones who usually say that are the ones that sell at the wrong time and buy at the wrong time. It's like mutual fund investors...they generally put capital in at the wrong times and pull it in a panic at the wrong times. The average investor's time horizon is relatively short...a couple of years at best. How much of an impact will SD have on Fairfax? We'll find out at some point in time, but I bet it is heck of a lot less than this discussion is suggesting it will be. Cheers!