Picasso

-

Posts

2,027 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Picasso

-

The forum has become self aware.

-

So only down 45% or so from the IPO. Who's buying here?

-

I think I know just the savvy folk this product is geared towards.... https://www.reddit.com/r/wallstreetbets I can't wait to see hedge funds try to use market sentiment data on those day traders...

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Picasso replied to twacowfca's topic in General Discussion

I guess what I'm struggling with (because I get your points to a certain extent) is that this is all being done with the benefit of hindsight. I think that once the bailout deal was made before the NWS, pretty much anything could be put on the table. We might live in the United States of America, but there are hundreds of thousands of people in jail or whatever who can tell you that the system isn't always fair, for various reasons. We shouldn't be waterboarding or torturing people but it happens anyway because the pain of a few is seen as better than pain for millions. A very, very large amount of people are benefiting from the fact that FNMA guys got "screwed" (hey at least there's still *some* value left for the equity/preferred) but the price had to be paid somewhere. IMO, I feel terrible for the investors who gobbled up all these preferred ahead of the bailout. I remember working at a large sell-side firm that was stuffing tons of retail accounts because they were getting paid 3% to do it and rates were so low that it was an easy sell. As soon as they started trading, they dropped 5 points. It was a sucker deal. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Picasso replied to twacowfca's topic in General Discussion

Got it, so the question is, if there was no bailout how exactly was FNMA supposed to fund themselves and at what rates? I recall them having to shove preferred stock at 8% down the throats of poor retail investors in late 2008. Isn't it more reflexive than just accounting losses when FNMA had access to a cheaper cost of capital from the not-100%-implicit government backstop? So 5% versus 10% or NWS versus no-NWS ignores the hidden costs to the government from having the prior arrangement? In some sense, decades of private investors benefited from the arrangement until 2009. Those unlucky investors in FNMA/FMCC got shafted but it was going to happen at some point, no? As far as the questionable nature of the bailout, it happened and no one fought against it then? Where was all the private capital that could have bid a higher price, etc? The losses ended up being a lot of the "accounting" type only because of what the government had to do to step in. In some sense it was like taking risk across a whole portfolio (banks, AIG, FNMA, etc) and there were certain parts that were harder to leave untouched. The overall result has been fantastic (maybe not for the zerohedge guys) but that wasn't a guaranteed outcome. Despite all the injections, there was still risk that was taken on. Anyway just trying to understand this a bit better and maybe my thought process is all off. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Picasso replied to twacowfca's topic in General Discussion

This is where I stand as well, minus putting OPM in it. But I take it a step further with this logic: If FNMA/FMCC are such great businesses, then why would the government have any incentive to give them back to private investors? We as public investors took on the risk (FNMA/FMCC may not have worked out and we'll see how legal the NWS is) and now that things look better, the private investors wants the upside again? Where were these private investors back in 2009? And if FNMA/FMCC are that vulnerable and need to be recapitalized without a NWS, why does the government want to give them back to private investors when no one is big enough to cover the losses when something catastrophic happens? Just seems like a tough sell to me. The government (and by extension, the public) deserves to reap all the upside given how much risk they were taking on. They might have changed the rules a bit mid-game but 2009 was extraordinary and they can pretty much call all the shots after what they had to do to fix the mess, albeit one they helped create. Anyway I know it's a touchy subject but that's where I put the FNMA/FMCC complex in my too hard bucket. -

I'll quote Munger on this one: You just have to deal with it. Do good work, find good value, and be ready for the macro schlonging that makes the macro guys look great for six months out of every three years. It's fine to mix in a little bit of your own "macro magic" when you feel strongly about something. But you'll find, just like I have, that it's a giant waste of time. Then again you guys are probably a lot smarter than I am and I don't mean that jokingly. You should just apply that intelligence to finding cheaper stocks the rest of us are too dumb to buy.

-

If I devoted 100% of my time on macro, I highly doubt I could use that insight to generate above average, somewhat consistent long-term results. If I devote 95% of my time to finding value (which can take many, many forms), I know that I can generate above average, somewhat consistent long-term results. The remaining 5% can be spent vaguely monitoring what's going on from a macro perspective. I personally never bought into the whole "rates are low, they have to go higher" argument. So I avoided investing in all kinds of rate driven value traps. Is that macro? Maybe. I would probably just say it's common sense that rates are unlikely to move considerably higher under a wide range out potential outcomes. If that 10% chance of super high rates hits, I'll just take my ass kicking like 99% of everyone out there. Not the end of the world if I've already earned several multiples on my capital by the time we all take a nice 50% hit. Value is always going to be 10x better than macro. But there will be stories of the few macro survivors like Burry or Paulson who hit one out of the park while 10,000 others lost a great deal. But by definition value is about finding something trading for a lot less than it's worth under most potential outcomes. How can that not be a better approach? Consistency and "repeatability" is key here and macro doesn't give you that either. So here's my definition of macro now that I've sort of defined what value is. Macro investing (mak-roh; adjective): a waste of time.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Picasso replied to twacowfca's topic in General Discussion

Would you capture it, or let it slip? Yo -

Btw ni-co... there's a "brief" short write up on VIC under torico on IHYG (euro high yield). I think that is a pretty interesting way to play the view that you have. Paying out 4% on a short while you wait for the liquidity to dry up could be a really good trade. It won't make a ton of money but I don't see how one could get terribly hurt on the short either. For that reason it probably works out well because no one cares enough to put on that trade. It's faster to put on a sovereign debt trade and get the move you're looking for. But I don't see how IHYG holds up if you think your views play out in the next few years.

-

I mean if you keep buying up dollars for 30-50 cents, does it really matter what happens with deleveraging and macro? I don't like BAC or GM but if you buy up enough of half of book and 7x earnings type stocks it's hard to lose even though macro is a factor. You just don't want to go balls to the wall long at 2x book or 10x peak earnings, etc. Macro matters a hell of a lot when you're paying a full price. Respect the macro and market but it's too easy to lose track of why value investing works when all these slick tongued macro guys come out. Dalio spends an insane amount of time only thinking about these macro issues.... Can any of us say that spending a similar amount of time will get us better investing results? Just some simple due diligence and respect for the macro will keep you out of a lot of blow ups and hopefully buying up enough cheap assets will show in the result over time. And you can't rely on Dalio's thoughts either. He's only recently become a more public speaker on these various issues. I wouldn't expect him to tell us when the macro suddenly looks great.

-

+1. We need to waterboard Dalio to get him to tell us how he really feels.

-

Nice usage of Eminem. +1

-

Bridgewater’s Ray Dalio Says ‘I’m Not Bearish on Stocks’ (1) Dalio sees global stocks rising about 4% in the long-term Hedge fund founder doesn't see another crisis like 2008 So is anyone who has been quoting Dalio lately going to quote that as well?

-

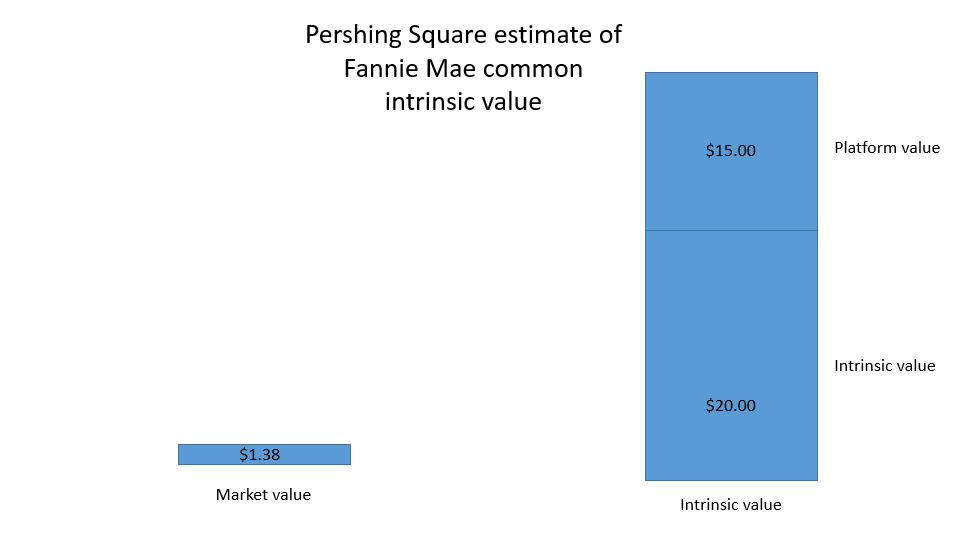

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Picasso replied to twacowfca's topic in General Discussion

I attached what I have from the Pershing presentation on FNMA.

-

Meet Mr Money Mustache who retired at the age 30

Picasso replied to shalab's topic in General Discussion

This NewYorker piece provides interesting perspective on the guy. I understand his thought process around frugality and it resonates with me. I was like that when I was younger. But to me the point of money is to trade it in for life enjoyment. To me frugality is a means to an end.... the article says he makes $400K a year from his blog now and yet he doesn't seem willing to make any changes or compromises in any way. That personality seems a bit on the obsessive side. If his wife is completely aligned with those beliefs and practices, then great! Otherwise seems like it wouldn't be much fun to share a house with him. Maybe it is partly for show now to maintain the personality cult that has developed around him from the blog. +1. He just strikes me as annoying at this point. -

Go buy a used Tesla Model S. They hold up value well, super safe, fun to drive and you get to see what will eventually put the other automakers out of business. The money you save avoiding stocks like GM will be worth a lot depending on the size of your portfolio. Then you're saving money on future health problems your grand children will avoid by breathing cleaner air. Thrn you'll save even more by avoiding stupid wars centered around energy supplies. Etc etc. So many savings!

-

Nice trade. I almost bought in the low $2's but dropped the ball on that one.

-

Last I looked his special Japan fund lost 80%. I understand your viewpoint now. Thanks for clarifying. It seems like the downturn is being led by energy and maybe China more than the banking system. We won't know until we see some economic numbers in a year and by then prices will likely have adjusted to whatever reality is. Edit: Some of the reports out there says he lost 61% the first year and then made 200% over the next couple years. I don't know what to believe with Kyle Bass. He's the kind of guy to go out and show the world how much he made on the trade if shorting Japan really made his investors over 200% but it could be possible, who knows.

-

If there's no growth, is that really the end of the world for European banks? You could have made the same argument for Japanese banks for close to two decades before people gave up on that trade. Except for Kyle Bass. He decided to try his luck recently and get his ass kicked as well. He looked at the leverage, low growth, bad demographics, low interest rates in Japan and came to the logical, first level thinking that JGB's were a short. Well he got what he wanted out Japan (first sky rocketing oil + TEPCO + full on BOJ pushing on a string) and now rates are negative on those JGB's. It's too hard to go from looking at this macro situation and making the bet to full financial crisis. Guys like Kyle Bass or John Paulson had a once in a lifetime opportunity and everyone's now constantly trying to find the next one. Hint: it'll be the thing people least expect. As far as the exposure relative to the economy. Well, isn't that the banks fault for taking on that kind of balance sheet? No one is forcing them to do so. If it ends up blowing up their institution then I'd expect the equity and preferred holders to eat it in the shorts. In comparison 2008 happened too quickly (it went 0-60 faster than a La Ferrari), this is a slow moving train wreck that will be involve less lubricant and Netflix and chill before the action happens. There's also 200 pages on the poor FNMA guys who are fighting against what happens when the government needs to step in and protect an asset when no one else has enough capital/courage to plug the hole. Expect the ECB to change the rules mid-game, break up the offending banks in pieces that protect certain debt holders, screw the rest of the stakeholders, and do whatever is necessary now that they're pot committed with big central bank balance sheets. They won't admit they made a mistake for a long time, this is just the path they've all chosen. If the relative size of these banks is problematic (seemingly every couple years these days) then they'll eventually be broken up, whether by force or necessity. Let the crappy, more exposed banks take it in the shorts. No one would really care about the bad bank spinoffs except the investors that were stuck holding the equity and debt of those banks. And (in my opinion) that's their fault for still investing in these banks after we saw what happened in 2008 with FNMA and other entities. It's not the end of the world and it doesn't need to create another financial crisis. And it will take time to get to the point where the various governments would need to step in. In the meantime these banks will earn whatever profit they can to offset the future losses that will prove once again that it makes no sense to invest in these institutions. The better short is probably the high yield debt in Europe. It's going to catch up to the rest of the worlds high yield and there isn't a lot of liquidity in those bonds. It was bid up on all this ECB easing but it doesn't mean it has the protection or lack of credit risk that the other EU member sovereign debt has. Anyway I think there are other reasons to be negative on the market but financial crisis doesn't seem like one. Maybe it's all too interconnected and it hits everyone but I think those types of events are once in a lifetime. I'll have to give it to these central banks if they do it twice in less than ten years. That would be quite the accomplishment worthy of a certificate of achievement.

-

I agree with this in that any equity market pops you get on central bank hope (new easing, lowering rates, etc.) should be shorted aggressively. To me that's just weak money that's coming in on the tail end of the effective 2010-2014 policy. I don't see how you can sustain any rallies on central bank easing versus real economic growth. I don't think there's enough growth to justify a lot of valuations out there so it's a fairly safe short but I've been known to be wrong.

-

Central banks are the nuclear option for problems the private market can't effectively solve on it's own without sending us back to the stone ages. They're also supposed to smooth out the extreme of the economic cycles. I don't think they're *supposed* to be effective at controlling the short term movements of the economy. That's been sort of this new thing to combat slow growth which doesn't make a ton of sense to me. I was telling someone that I'd rather pay 15% interest on a house that's undervalued than paying 0% on an asset which is way too expensive. They seem to be driving people to buy up expensive assets regardless of their value and that's a problem. Look at all the guys blown up on REIT's, MLP's, dividend stocks, etc. You have to let the markets work out these problems, there isn't supposed to be an easy fix all the time. I take the view that most bank equities are just a retarded investment regardless of what happens with the economy. It's just classic tails you lose and heads the government wins and you still lose. And central bank policy is just making it harder to be a bank so either they have to start making riskier loans or they'll be continually driven to less and less profits over time. Why is the market just realizing this now and why do we jump to financial crisis conclusions? There's too many variables before you get to that conclusion which makes it a very low outcome event imo.

-

I'm trying to figure out why investors on this board think a European financial crisis is looming or whatever. I pulled up a total return index on Deutsche Bank since 1992 and I show a 14% nominal return when you include dividends. Over that time frame the share count tripled so they just keep raising equity at the detriment to existing investors. It's been an investing graveyard but we've gone through it many times and it's been fine. How does that spell financial crisis? A stock like DB continually round trips back and forth and as one of my friends who used to work there says, those guys are idiots who will lend to almost anything. Worrying about stupid European bankers would have prevented you from investing in a lot of really good or inexpensive businesses/bonds for the past thirty years. If some of these European stocks weren't trading crappy (as they've always done over history) I don't think people would come to the European crisis conclusions. And if we didn't have 2008 fresh in our minds we would be even less likely to think that's around the corner. That's not to say these euro banks are not terrible investments. But I don't see how we jump from crappy equity performance, crappy business models and write downs to financial crisis. Investors in these banks will keep getting crappy returns just like they always have. I don't think it's much more complicated than that.

-

Also keep in mind that most of his holdings were hedge fund hotels. Those have been subject to relentless selling pressure. I thought he did good work (logic wise) but that's a tough space when flows go negative.

-

+1