Libs

-

Posts

622 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Posts posted by Libs

-

-

4 hours ago, lnofeisone said:

If this is your hypothesis, I'd go with a vertical bear spread. 140/138, with an expiration of next week, is trading at 0.50. So, if you are right, you get a 4:1 payout, and TSLA only needs to go down to $138. If you bought the 157 ATM Put @8, TSLA would need to go down to 125 to have a similar payout.

I don't see a quote for the 138's , just 135's ($2.00) and 140's ($3.15). So that one (140/135) costs $1.15, and at $135 you make $5 or 4.7:1. Do I have that right?

What about the 150/145. Cost $2.25. Stock only has to drop to 145 and you make over 2:1. Not bad. You might be on to something. Thanks.

-

With TSLA the growth story is completely broken. No new models, EV'S slumping, layoffs, and all this for 60-70X earnings. The downside is huge and Elon's got nothing that will turn things around for at least 5 years, and that's IF robotaxi and FSD gain traction, which I highly doubt.

So I have a fair amount of TSLS, which is great because I can use my IRA to short it. I'll hold TSLS for as long as it takes to deflate this $500B bubble. That's the long-term play and i can weather the volatility in TSLS.

The options are short-term gambling, with earnings on 4/23, and expiry 4/26. Smaller in size. My bet is that this recent decline still hasn't priced in the earnings miss that is coming. Also early estimates on Q2 deliveries are really bad - down 10% Y/Y again.

-

18 minutes ago, backtothebeach said:

That's kind of in my wheelhouse. There is no objectively or statistically better deal, otherwise it would be arbitraged away in a liquid option chain like TSLA's, especially right before earnings.

One can be subjectively better than the other, though, depending on your expectation of TSLA's stock price and your risk tolerance.

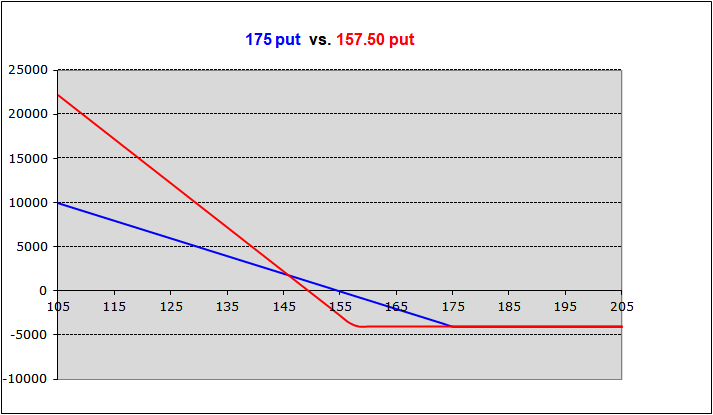

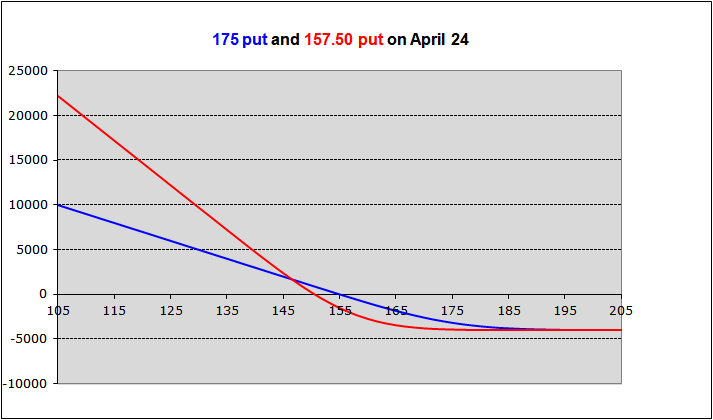

Let's say you decide to risk (gamble) $4000 on the expectation that TSLA will fall after next week's earnings. You could buy 2 contracts of the 175 put, or 5 contracts of the 157.50 put. Below are P/L graphs of both positions, at expiration April 26, and on April 24, at the open after earnings (with unchanged IV, which may only be realistic for the first minutes of April 24, probably IV will drop and the options worth a bit less than modeled).

You can see that if TSLA either surges or drops a lot, the 157.50 put is superior (max loss is capped at $4000, but max profit is much higher due to more contracts). However you have to be right about a large downmove.

The 175 put is "safer" between 150 and 175, and has, as you noted, a higher breakeven - at the cost of each dollar invested not making as much should TSLA drop like a rock to $120.

Very helpful, thank you.

-

1 hour ago, Sweet said:

You aren’t missing anything, it is a ‘better deal’ and it’s somewhat safer too.

However if Tesla the $157 puts cost less to own the same amount.

Can it be that simple? I thought the options market was a lot more efficient than that.

-

I'm sure the answer is obvious, but I couldn't find a satisfying answer with a search. Obviously I'm an options neophyte.

Example: Tesla stock price is $157. The April 26 $175 puts cost $20. Meaning I need the stock to be at 175-20= $155 to break even. A $2 drop from the current price. Right?Meanwhile, the April 26 $157 puts (ATM) cost $8...which is a $149 break-even price...now you need the stock to drop $8 to break even.What am I missing? Aren't the $175 puts a much better deal? -

On 4/13/2024 at 12:27 PM, RichardGibbons said:

It's pretty amazing to me that managed economies have been tried since Marx, and not one has even had close to the astounding beneficial results that arise from liberal free-market economies. And even more amazing that many people are so eager to completely ignore that evidence in favor of a story.

Bingo. As a friend of mine says, "wow, Marxism is the unluckiest system; if only some country could finally pick the right people to try it out!"

Karl Marx inflicted untold misery upon the world.

-

55 minutes ago, gfp said:

I would be nervous if I was the company that had just filled that ship up with fuel.

Why?

-

39 minutes ago, nwoodman said:

Kingswell also linked to this, you end up running out of superlatives :

"Charlie Munger, who died in November within sight of his 100th birthday on Jan. 1, fell ill at his home in Santa Barbara. When he got to the hospital, a nurse asked him how he was. 'I’m dying,' he said. 'How are you?'"

https://diocesela.org/the-bishops-blog/charlie-munger-memorial/

Someone once asked if he knew how to play the piano. “I don’t know,” he said. “I’ve never tried.”

Another classic.

-

I bought a handful for $200 each way back in the day (2015?); then bought two more for $50,000 each a little while ago. Talk about averaging up! Anyway that last buy was to get me to to a 3% position, where it will remain untouched. I guess it's 4% now.

-

1 hour ago, Luca said:

I strongly disagree. The only thing that matters is that China is a significant competitor of the US on all fronts. Are there sanctions against other countries with human rights abuses? Its one sided against china only.

Here is a list of U.S. Sanctions, from the Treasury Department.

https://ofac.treasury.gov/sanctions-programs-and-country-information

Luca- I like your posts on other topics, I think you have a lot to add, but I think you are way off on China. Just look at the drop in foreign investments in China; down 90% since 2021. That's not just because of sanctions or human rights abuses. Investing in a communist country is dangerous as hell.

-

Sold most of my Tesla puts that exploded this week. I'm finally in the black betting against Tesla (my white whale!).

-

The comments about railroad and energy are quite jarring, and a complete departure from the past. Kudos to Warren for facing these issues head-first. As a shareholder it's forcing me to re-examine some of my assumptions, though. I had thought these two pillars were iron-clad.

-

Classic. The property bubble was driven by central planning mistakes - 1) they incentivized local governments to raise revenue by selling land to developers; 2) They made sure Chinese had no other good investment options.

And of course, the bubble finally blew up. And the solution? More central planning!

I see China as basically a battle between their hard-working, resourceful people and the CCP, which is constantly doing stupid things to hold them back ( one child policy, Covid, etc.)

It's the same race we have here in the U.S., but here the people still have a shot to overcome the idiots we elect. I think.....

-

<A great example as I've mentioned so many times is the insurance broker contingency commissions, something that I considered quite accurate as to Spitzer's complaint>

Sorry for a quick derail here, but I remember this well. I was in the thick of it as a branch (So Cal.) marketing manager for one of the major insurers. This was the mid 90's. We came up with the genius idea of offering bonuses to the brokers (Marsh Mac, Gallagher, etc.) if they put X amount of business with us for the year. It never occurred to us how unseemly it was! But of course, in keeping with Munger's teachings about incentives, brokers would, especially at year-end, put clients with the wrong carrier, to hit the goal. Not very ethical.

To go on a further tangent- at this same time (actually 2000) Buffett thought it was OK to 'rent out' Berkshire's balance sheet. As I recall AIG took him up on that. Most of us thought Brandon ( Gen Re head) took the fall for him on that one. A very rare lapse of judgement on Buffett's part IMO.

End of tangent. I think Dealraker has made me nostalgic for my old P & C days.

-

2 hours ago, Kupotea said:

There’s no money chasing small cap value (it’s all gone to passive large cap) so if a company beats expectations no one notices. Without price discovery you need to find companies willing to initiate large buybacks if you want to get paid. In the meantime, the most overvalued components of the S&P continue to attract ever larger inflows.Thank you. Not very persuasive though. My small caps move pretty violently to quarterly results, so someone is noticing.

-

7 hours ago, Spooky said:

Thanks for sharing. I found his hypothesis that passive investing has broken price discovery for certain segments of small stocks interesting.

Would you mind summarizing this hypothesis?

-

Fair enough about the Fins. But there must be other places they could try this approach.

-

So there's been talk of Russia taking on NATO, which on the surface sounds preposterous, just given the overwhelming power of NATO forces relative to Russia. But what if, instead of taking on all of NATO, they nibbled at the corners, so to speak, in a such a way that the NATO members say to themselves: "I'm not risking our soldiers / WW3 breaking out by fighting for X."

In other words, the plan is to destroy NATO by exposing it as toothless. Then, over time, Russia starts to take the smaller / weaker countries.

This guy explains it. The example he gives is a remote outpost in Finland with little strategic value to anyone. Technically, it's a violation of Article 5 if Russia takes a small slice. Will that be worth a full-scale war with a nuclear power?

What do you guys think?

-

Shameless brag, I bought some BTC years ago for $200...22 bags later, it's grown to a 2% position. Had I not stupidly sold half of them when it went to $400, it would be a 4% position.

So to answer OP's question, I am making it a 4% position today via the Fidelity ETF. Ran it by the wife and she agreed.

-

4 hours ago, Sweet said:

In terms of PE we aren’t too far away from the from the ~35 year average of 19.Notable that the lowest PE since 1989 has been 13.

Ex the MAG-7, the other 493 stocks have a P/E under 15. The market is not overvalued. If you don't want to pay 31X for Apple, you can easily work around that.

Also U.S small and mid caps are even cheaper.

-

<I’ve never understood the institutionally inspired obsession with fretting or fearing volatility. You should only be investing money you don’t need. And if you don’t need it who cares about what’s literally just one of the features of the stock market? I can’t think of anything that probably costs investors more money over the course of a lifetime than trying to avoid volatility. >

Very true, Greg, and this point isn't made enough. I have a real-life example. I manage some 'scraps' for a few members of a family, each worth $100MM+. They have the vast majority of their money with a fund-of-funds guy charging 1% and putting them in a bunch of 2 + 20 type stuff. He's successfully smoothed out their returns; in the big down years they see only minor impairment. But over 20+ years, they've made their smooth 5% while I've made them 12% just opportunistically buying individual stocks like Berkshire and COST and the other stuff we talk about here. Common sense, coffee-can stocks.

It's funny how they see it...... every once in a while - after a good year like 2023- they'll say, geez 'libs' is doing so great, why are we putting so much with funds-of-funds guy instead of him?"

And the answer is "because in 2008 'libs' was down 35% and FOF guy was down 4%." And they say, "oh yeah, that's right."

I'm not saying they're being stupid- some people just can't handle the swings. I'm not even criticizing the approach; the FOF guy is very smart and a friend of mine now. It's just the way people are, especially if they are already rich.

But if you add up the numbers, after 20 years the difference is staggering. In essence they are paying me 60BP's, with no underlying costs, to make 12%; and they are paying FOF guy untold multiples of that to make 5%.

Maybe we should just consider ourselves lucky we're wired differently than most, and let it go at that.

-

On 12/27/2023 at 10:27 PM, dpetrescu said:

My two best ideas going forward are the same as last year:

1. SSD - Simpson

this company continues to amaze me. Perfect for a 50 year holding. Just one minor note… being such a wonderful company, it is today very very highly valued after a couple big corrections. So you might need to deal with a 30% to 40% correction in 2024. Aside from that technicality, it will continue to be my 75% holding and I will just keep buying in 2024

. If we ever have a world war 3, Simpson will also act as a complimentary sleep aid - will help you sleep through worst of times worry free.

. If we ever have a world war 3, Simpson will also act as a complimentary sleep aid - will help you sleep through worst of times worry free.

2. ADSK - Autodesk

This will continue to be the Robin to the Batman in my portfolio for 2024 These two together will continue to make up 95% of my portfolio. Another wonderful company. While many know about its strong competitive advantage - I’ve reached the conclusion that even the most fancy of analysts don’t truly understand the depth of that advantage. Stock price has been miraculously flat for a few years but we might be seeing a breakout. Also of note a minor detail - the share price is veeerreyyy! expensive. But then again - if you’re like me and planning to hold it for 20 years, then it makes sense and I also just keep buying this one and can’t wait to keep buying in 2024. And I hope this one also sees a 30 - 40% correction in 2024 but I’m not waiting for it. The big risk with this one: still not sure how the decline in demand for new commercial office buildings could impact it over the next decades. With some decent percentage working from home currently and that percentage likely to grow over time. This is the big unknown for me.

Thanks for the heads-up on SSD; an amazing company. Kicking myself for missing this one ( so far).

ADSK also great but the SBC is a deal-breaker for me. I can live with some of this, but yikes...they've been spending a billion a year to buy back stock, to make up for the SBC. Am I missing something here?

-

Wow, some great results, and I'm glad the heavy lifters here like Greg and Parsad went huge. They deserve it.

As for myself, up 28%, without holding any of the MAG 7. No mishaps to speak of. Notables:

GLASF + 128%

LUMINE + 85% (seemingly all in the last 10 weeks)

JOE + 59%

CNSWF +59%

PATHWARD +24%

-

9 hours ago, dpetrescu said:

My best investment has been after I stepped away from being a Buffett clone to uncovering hidden gems in my own professional field.

A long time ago I found a great company and invested in it. And I had such great conviction in it. The error was in not going all in (Soros and the juggular). Years later I realized this, I overcame my regret - and went all in, made this one company the vast majority of my portfolio and threw out the other junk.

Worked amazingly. That might be the biggest challenge with investing (as anything of value in life) - lessons and rewards are best understood over a great portion of time passed - in decades.

Which company?

Question about in-the-money puts versus ATM

in General Discussion

Posted

have put in $1 increments in the 108-150 range.

Schwab. I will give that a try, thx.