crastogi

-

Posts

152 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by crastogi

-

To add to that, the core of his strategy is to invest in "high quality" companies, at a reasonable price. He defines high quality specifically in a value of ROCE (Return On Capital Employed), which is (almost) net profits divided by total assets. This shows the return the company is generating on capital employed (not taking into account long term debt) - i.e. how valuable will the company become if it is not saddled with any debt. He chooses companies with ROCE around 25% or higher. Assuming a company reinvests its profits internally, then he argues that its intrinsic value also increases by 25% each year. Two points he does not answer in his presentations that I have seen, are the effect of debt servicing on this process, and why doesn't the efficient market theory discount this effect (by making the shares correspondingly expensive at the outset). The implicit answers to these two questions are that compounding by 25% per year will deal with the debt problem over the longer term, and that other investors don't understand the long term uplift of this kind of compounding, leading them to value the business in aggregate higher than, but not sufficiently higher enough, than other businesses with a lower ROCE. Edit: Just to say that in the video of the 2020 meeting posted tonight, he explains this strategy at time 16:48 I've been looking into this tonight. Watching the two annual shareholder meetings for FEET (Fundsmith Emerging Equities Trust), for 2017 and 2019, he says that the fund underperformance of net asset value was caused by outflows of money from far east actively managed funds, into far east index funds (ETFs), resulting from general investor sentiment in favour of passive investing, and regional investing. He says that the sectors of the companies he is invested in are under-represented in the main indexes, hence demand for his companies dropped in aggregate, along with the price). It sounds plausible, but might be an excuse of course. time: 50:50 time: 20:00 I think the key is to only invest in companies where you are fairly certain that the returns on capital are not going to trend down to the mean and the revenues will keep growing. That is the only way this works.

-

How to make money from this crash - Lessons from 2008

crastogi replied to ukvalueinvestment's topic in General Discussion

But you have to know when the bottom is in :) -

I would negotiate commish...after getting a good offer. of course if I get an offer at full asking price I dont negotiate the commish but I haven't seen a full price or bidding war in a couple of decades personally, but one way getting an improved result after the offeror stands pat and the net is lower than you would like is to then simply ask broker to move a bit...and he/she likely will and happily will to cement sale...but dont piss off your broker before getting the listing by trying to discount commish. A little unethical, no?

-

Are Renaissance Technologies just trend followers?

crastogi replied to RuleNumberOne's topic in General Discussion

I would take those returns any day ;) -

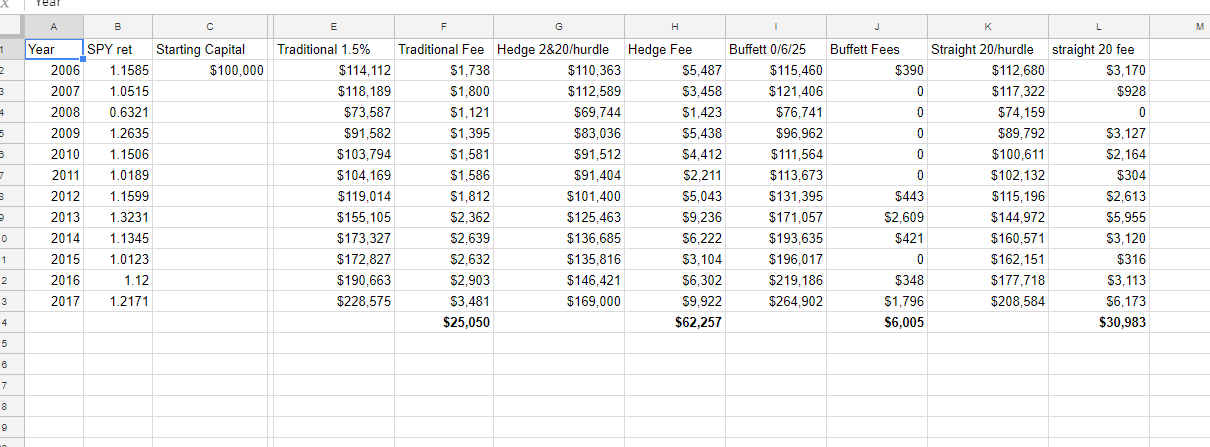

So, FWIW some time back I had done a spreadsheet for net returns to investor with SP500 historical returns under different fee scenarios. It is attached below. Maybe some will find it useful. The big takeway is that the Buffett model only pays for the manager when you are generating serious alpha. Of course, the traditional hedge fund structure is egregiously expensive for the investor.

-

Surprising. I thought it was 0/6/25. But the interview states it differently. Thanks for sharing

-

Thanks Paul

-

Does anyone have an estimate of costs for starting a partnership? Also, can you have incentive based fees for SMAs?

-

Thank you for compliling!

-

That's right, Investmd. And that's why i am baffled. BTW 15% for 5 years is a 2X. However, he is not without some spectacular blowups. Delta financial, compucredit, etc. Clearly after spending a week on this, I cannot come up with a compelling reason. I was hoping someone here could point me in the right direction.

-

Thanks for the comment. I agree they are dominant and have had sustained excellent ROE/ROC. And that the market for Basmati is growing. And also that there is a trend in India to migrate from buying from Bulk packaged generic to branded. All these are trends are tailwinds for them. However, the management seems promotional. And at a 30 PE, the growth story has to be really good get decent returns. Actually as an aside, I know Pabrai is bullish on Indian stocks, but the valuations in general seem to be high in India, especially given that LT bonds yields are north of 7%.

-

So Rohit, have you analyzed this? My preliminary analysis indicates a 12-15% ann return for the next 5 years. Better than most opportunities in US but not a slam dunk that Pabrai looks for. Your thoughts?

-

Thank you! Very nice

-

Since 99. I have always been a value investor. May be a function of bargaining for groceries in India where I grew up ;) Have held Berkshire since 2001

-

That was their first choice. Unfortunately recertification in USA is a very involved process. Hence, the search.

-

Best thing to do is land and start the immigration process and work in their home country part-time if they need the money, if they don't need the money early retirement or get a hobby. With some contemplation, they should not be taking on risk at this age so allocation should be below 20%. I don't think you should give be giving advice on this topic if it doesn't work out it will create real human misery. He asked for advice on where to start their search not advice on whether they should start a business or not. OP, bizbuysell.com could be a place to start to look for business broker listings in your area. Thanks BCI!

-

Best thing to do is land and start the immigration process and work in their home country part-time if they need the money, if they don't need the money early retirement or get a hobby. With some contemplation, they should not be taking on risk at this age so allocation should be below 20%. I don't think you should give be giving advice on this topic if it doesn't work out it will create real human misery. I think they have no financial need to work, but they feel that doing something productive will keep them active and young. I know it is a decision fraught with risk. I am just trying to get them all possible information, so they can make informed decision

-

I would like to tap the wisdom of this board about the following: I have family immigrating to the USA. They are in their late 50s, physicians in their homeland. So, they cannot practice medicine here as the clock is running out for them to recertify, etc. But they are young and inclined enough to start a business. Any suggestions on what kind of businesses are available? A franchise would be preferred. I do not have the foggiest idea where to start looking. Any directions to help them start this search would be appreciated.

-

https://www.screener.in/ http://www.valuepickr.com/ Thanks Hobbit. Do i take it that you are active in the indian market?

-

I too am interested in Analyzing Indian Equities. As someone living away from India for the last 30 years, i am lost as to where to start. Could someone please point me to: - A site to get company filings ( like sec.gov) - Some reputable Indian investors, whose holding we can look into for idea generation. Is there an equivalent of a dataroma or whalewisdom in India? - Any good website/boards discussing indian equities Thanks to the best investing board in the world!!

-

Would be interested in hearing your thesis. Right now they are at 16X earnings, which seem depressed. where do you expect the earnings to go to?

-

yes, Congrats!! Thanks for so generously sharing with this board over the years

-

As I mentioned earlier, all the big value guys are sucking right now. Why single him out so hard? Also, he's not the same as the "helpers" Buffett is talking about--Buffett singles out 2/20 and fund of funds. Pabrai is 25% over 6%, just like Buffett was, and has not paid himself for years at a time. I sincerely hope you guys never screw up and have someone judge you as harshly as you are doing Pabrai right now... +1! As I mentioned in a post when Mohnish was hitting bottom and people were piling on him...this board, just like any other, is a reverse indicator of the future. Since that time, his funds are up around 100%. Yeah, he hasn't performed as well as he would like for his investors, but he's only human. Anyone who invested with him from day one is doing as well or better than the S&P500 TR to date, with PIF2 and PIF3 outperforming by about 4% annualized and PIF4 essentially breaking even. His interests are aligned with partners, he's had massive redemptions at the bottom on two occasions, and continues to fight and claw his way back up. Yeah, he's a cloner and his ideas may turn with what books he's reading, but he still uses the same fundamentals in analyzing the investments. His fund is volatile, but his results have actually been pretty good as a manager, and he only makes money when partners make money. Aren't there alot more (like 95%) managers more deserving of such scorn than Mohnish? How many young fund managers has he helped? How many investors has he helped by freely sharing his knowledge...and you know who you are...you don't invest with him, but love stealing his ideas and eating his hor d'oeurves! How many presentations and speeches has he done...like he's not busy enough? How many kids has he put through Dakshana into the IIT's? There's alot more to like about Pabrai, than not like, that's for sure! And who has the balls at his age to wear spandex when cycling (recurring joke by me)! Cheers! +1... there is lot to appreciate in how he lives his life for sure.

-

Granted Pabrai's return have not been that great lately. But unlike majority of the investment products, he does not get paid for assets under management. He has to clear 6% and high water mark. So he really does not have that much incentive do asset gathering. In fact, i thought he was closed to investors. Everybody markets to some degree. A good investor should have a good nose for marketing messages, else we will have a hard time buying individual stocks. What I like about Pabrai is that at least he is candid about admitting his mistakes and he occasionally does post mortems on some of them. We all can learn from that. Most managers never talk at length about their mistakes

-

Well, Berkshire's P/B will always be lower because they are in different kind of businesses as the list above. The returns on capital employed are much higher for companies like Google, as they have fewer hard assets. Buffett is looking to soak up all the capital Berkshire is creating by deploying in businesses which will provide a predictable return, even if the returns are not spectacular.