Luke 532

-

Posts

2,931 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Luke 532

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

I wonder how prefs would trade in that scenario given the current market and many other equities depressed in price. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Interesting comment... https://twitter.com/Alec_Mazo/status/1242463500779151366 If the Gov't is going to take equity stakes in the companies to stabilize them, it must convert its warrants in Fannie Mae immediately to signal they wouldn't initiate a Net Worth Sweep with others like with Fannie- effectively nationalizing them. $fnma Note: I think Alec meant the senior preferred shares. That is the mechanism for the NWS. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Tim Howard response when asked "If you care to comment on the recent FED actions as it relates to the GSEs and the calls to allow them to buy MBS paper it would be helpful to get your take on the government’s response." https://howardonmortgagefinance.com/2020/01/16/how-we-got-to-where-we-are/#comment-14794 I’m not sure where to begin on this one. Prior to the 2008 financial crisis, Fannie Mae’s portfolio investment business had been the “bete noire” of the Financial Establishment for longer than the 17 years I was responsible for it (from 1988 to 2004). Fannie had indeed almost failed in the early 1980s because of a mismatch between its mortgage and debt durations, but in the late 1980s the company began using callable debt and derivatives to “rebalance” those durations much more frequently and cost-effectively. From the early 1990s, Fannie’s portfolio was not the “snarkily managed hedge fund” the Wall Street Journal labeled it, but instead a consistent buyer of 30-year fixed-rate mortgages that helped keep interest rates on mortgages low, while at the same time being a significant source of profitability for Fannie. This, however, did not stop Treasury from requiring Fannie (and Freddie, which had been a late entry into the portfolio business) to shrink its portfolio by ten percent—later increased to 15 percent—per year after it was put into conservatorship. Well, now portfolio investments in mortgages and MBS ARE risky. The recent sharp widening in mortgage-to-Treasury spreads reflects not just the typical “flight to safety” one sees during times of market stress but also the fact that with short-term interest rates at zero 30-year fixed-rate mortgages originated today could become extremely long-duration assets. A debt-based mortgage investor in new long-term mortgages therefore must have a very large rebalancing budget to cover the risk of having the durations of these loans extend to an unprecedented degree. It doesn’t surprise me that the Financial Establishment would like to have Fannie and Freddie be permitted to add to their portfolios again—the mortgage market is badly in need of support—but its willingness to ignore the interest-rate risk these investments would pose to the companies, which seemed to be of such great concern when those risks were considerably less, can’t be allowed to go without comment. Yet, “be careful what you wish for.” The current vision of Fannie and Freddie as recapitalized and released companies limits their portfolios to purposes incidental to the credit guaranty business, such as aggregating purchases from smaller lenders prior to packaging for sale as MBS, or holding non-performing loans bought out of existing MBS pools. Were Fannie and Freddie to be allowed to rebuild their investment portfolios, Treasury and FHFA almost certainly would have to agree to extend whatever government support they intend to provide for their MBS credit guarantees (most likely continued access to draws of senior preferred stock, for a fee, in the event of financial difficulty) to the debt that funds their newly expanded portfolio business. Buying government-backstopped MBS using debt without such a backstop is not a viable business proposition. (Remember, banks can fund their fixed-rate MBS with FDIC-insured consumer deposits, and incur no capital penalty for the interest-rate risk they take in doing so). The question thus becomes: does the Financial Establishment want Fannie and Freddie’s support as mortgage purchasers over the next few months to a year badly enough to extend to their debt the same type of government support it’s willing to give to their mortgage guarantees in the companies’ post-conservatorship future? Somehow, I doubt it. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

+1 -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Democrat House Bill: https://appropriations.house.gov/sites/democrats.appropriations.house.gov/files/COVIDSUPP3_xml.pdf Searched the following terms with no hits: Fannie, Freddie, Mae Searched the following with hits but nothing related to GSE's: Mac, housing Searched the following with a hit: GSE Here's what it says... (k) EXTENSION OF THE GSE PATCH.—The Director 18of the Bureau of Consumer Financial Protection shall re-19vise section 1026.43(e)(4)(iii)(B) of title 12, Code of Fed-20eral Regulations, to extend the sunset of the special rule 21provided under such section 1026.43(e)(4) until January 221, 2022, or such later date as may be determined by the 23Bureau. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Midas, well said. I agree that's likely the elephant in the room given the uncertainty of the markets and economy as a whole. To everybody reading, if r'ship doesn't happen, what else can realistically kill/severely hurt the prefs? That's the big question. If the answer is "nothing really" then the only concern is how long it will take. The duration is a big concern, of course, as the longer it takes the more it depletes rate of return. -election risk (if irreversible action isn't taken by the current Admin prior to Inauguration) -losses in court -some other black swan event -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Ackman today on GSE's at 14-minute mark: https://finance.yahoo.com/video/bill-ackman-u-recession-threat-192341688.html -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Nevermind, think I was wrong. Going to delete my post not to confuse anybody. Thanks. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Do a combo order. Either they both fill simultaneously, or neither fill. Makes it less likely to execute, of course, but ensures you don't get on the wrong side of the spread on both. Do keep in mind the possibility that Fannie may exit conservatorship or have consent decree prior to Freddie. I currently only own Fannie prefs in part due to this, although all prefs should do well both Fannie and Freddie. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

There it is, open-ended MBS buying: The Fed's firehose is fully open. Open-ended Treasury & MBS buying, sets up a TALF program for ABS, student loans, credit card and small business loans. Also planning a small-business lending program. Treasuries rally. The dollar weakens. @TheTerminal FHFA authorizes @FannieMae and @FreddieMac to support additional liquidity in the secondary mortgage market https://t.co/enpXJUXzG4 -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Full unlimited backstop of agency MBS (attached)...

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Not sure if anybody is listening to the press conference tonight, but moments ago Trump said (and I paraphrase): "We don't nationalize businesses. Ask Venezuela how that goes." Certainly seems good for those that fear F&F will be nationalized due to a bad economy. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Whalen calling for immediate warrant exercise by Treasury. If UST takes common stake in GSE's, junior prefs are worth par. https://www.theinstitutionalriskanalyst.com/post/what-must-be-done-to-support-housing-finance -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

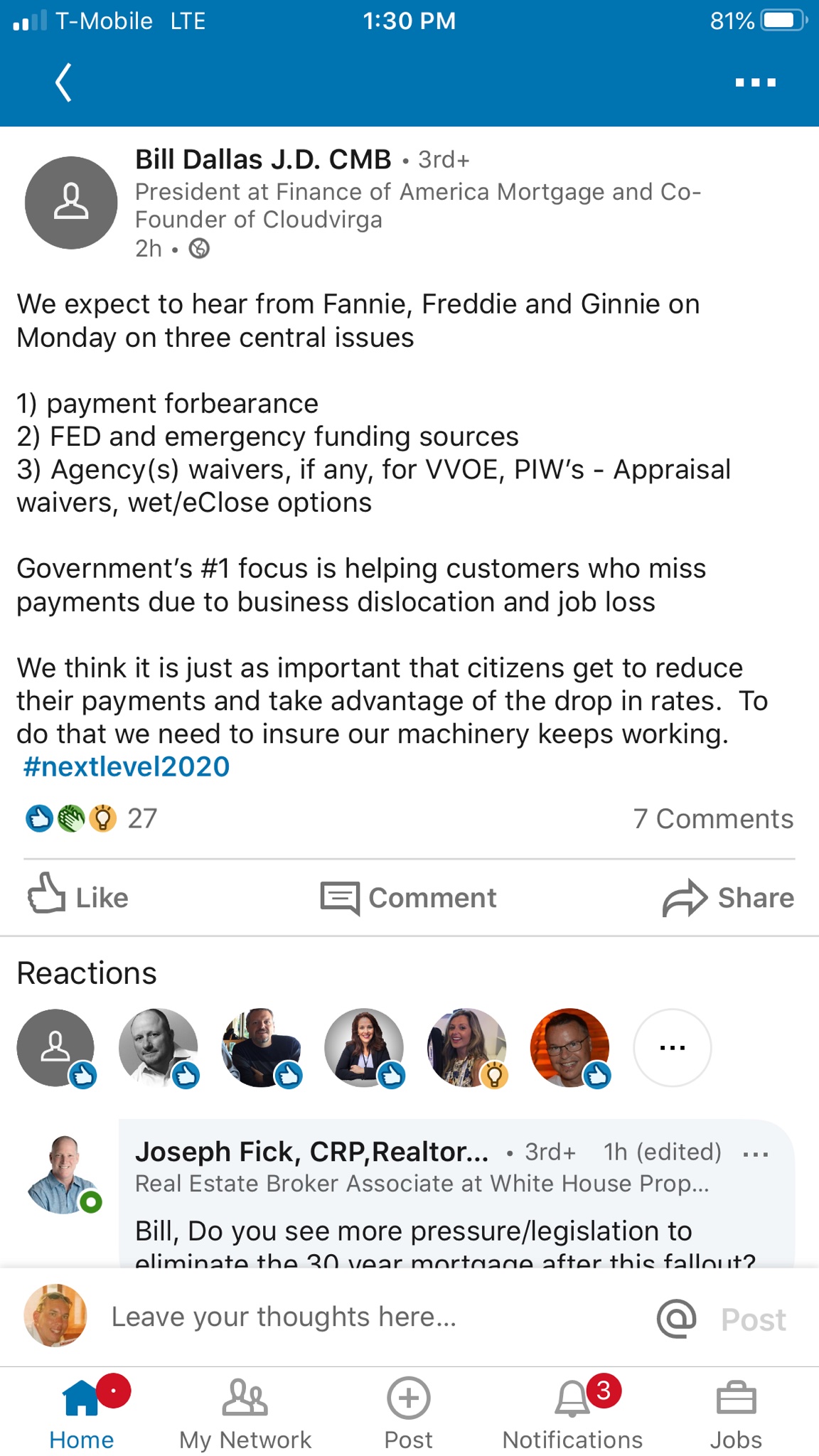

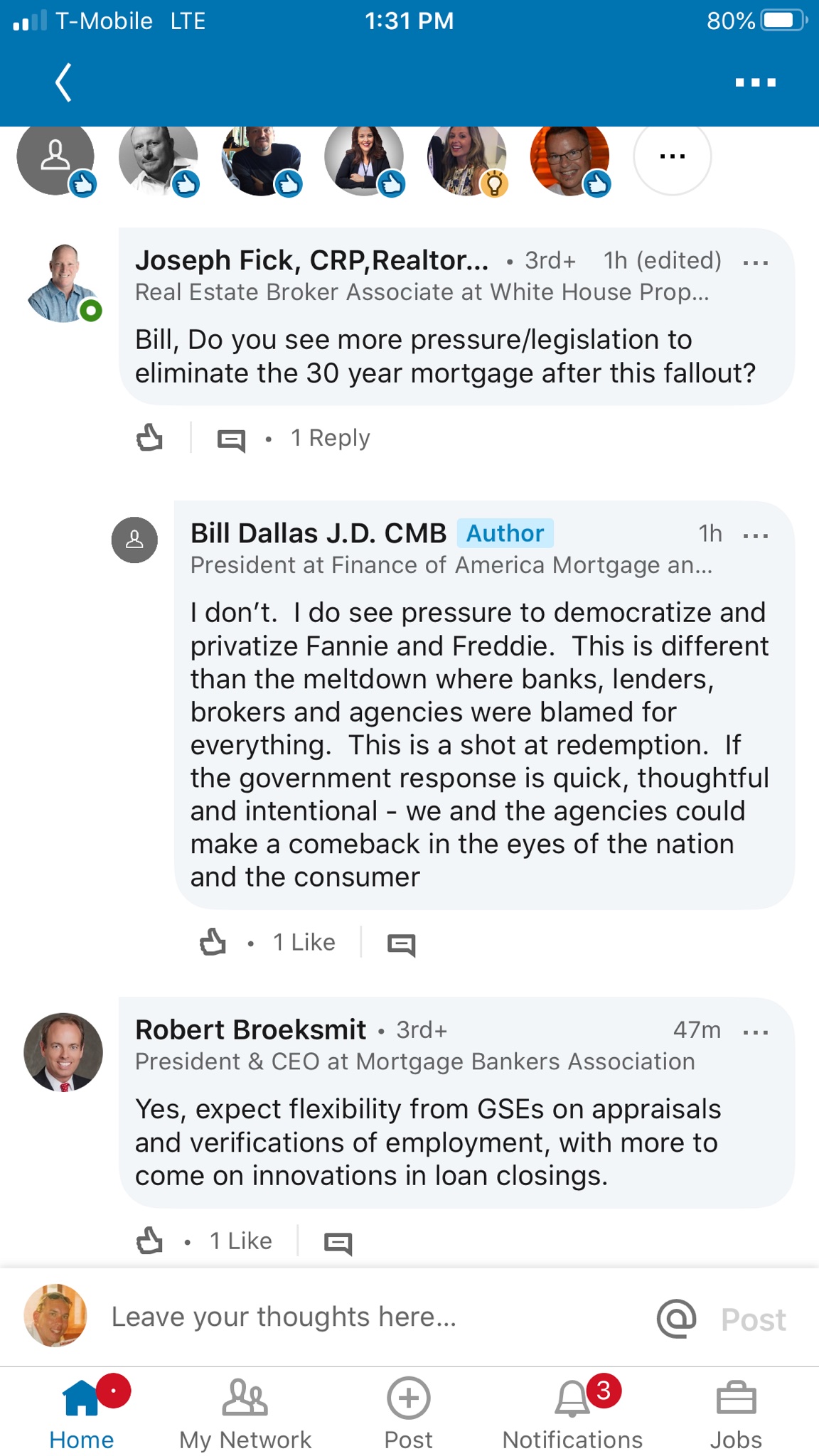

Luke 532 replied to twacowfca's topic in General Discussion

See attached... Edit: FWIW, just asked him and Dick Bove agrees with Bill Dallas' comments in screenshots attached.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Thanks Luke. Was this from their podcast? From a conference call, but I heard it second-hand, so take it with a grain of salt. The re-list and access to Treasury was news to me. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

It’ll be fun to find all the prior ACG bullish call dates and map them on the chart. I only remember last March or so they had a wildly bullish call right at the top. The price retraced quite a bit. But I lost track since last May. Muscle Man (MM) = Mr. Market (MM) -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

More from ACG call Wednesday, March 11th: -ACG never been more positive that conservatorship is about to end -FHFA and Admin want this done -Taking irreversible actions even if Trump loses -Expect re-listed by Fall at the latest (before offering) -Met with Treasury and FHFA and positive PSPA amendment is happening -Politics won't stop PSPA amendment -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Bloomberg Intelligence Regulation Watch: GSE Capital Requirements Ben Elliott Team: Government BI Government Analyst Fannie-Freddie Capital Rule Should Do Job, But Virus a Wild Card Even with FHFA delaying its capital rule proposal until at least May, we are now more confident the regulator will meet investor expectations and be supportive of Fannie Mae and Freddie Mac’s relisting. The constraint now shifts to whether the coronavirus can be contained before doing irreversible damage to the process of returning the GSEs to shareholders. (03/20/20) 1. What’s Next? Next Key Event: ·Re-proposal set for second half of May. ·FHFA’s timeline could slip if the coronavirus isn’t contained. Last Key Event: ·Re-proposal timeline updated to May by Calabria. ·March 18, 2020. Rule re-proposed in May, perhaps. We’re confident the Federal Housing Finance Agency can meet its May deadline if the pandemic allows, but caveat that unsuccessful containment could derail the plan. The proposal would be open for comment for 30-60 days, most likely, and could be completed by year-end. A final rule isn’t as necessary as a well thought out proposal upon which the Treasury Department, the government-sponsored enterprises’ shareholders, potential investors and other stakeholders can base plans and expectations. (03/20/20) 2. What’s the Outlook? Credit Risk Transfers Likely Remain Favored Proposal may exceed expectations. FHFA’s thinking seems to have shifted on GSE capital, greatly limiting downside risk of a suboptimal rule subvertng demand for a relisting of the GSEs. FHFA Director Mark Calabria’s pledge to achieve economic attractiveness and an indication he’s focusing on detailed risk-based rules instead of a draconian leverage requirement suggest to us the proposal will be a net positive for the GSEs, which may even retain some edge over banks if they have more detailed mortgage risk matrixes to work with. (03/20/20) 3. What’s at Stake for Fannie and Freddie? 2018 Proposal: Fannie 3.4%, Freddie 3% MBS dominance for Fannie and Freddie. FHFA may have to de-prioritize its goal of achieving a multi-guarantor future — never easily achievable, in our view — if Fannie and Freddie perform well through the coronavirus crisis. We see less risk that FHFA pursues a leverage constraint that would apply more frequently to limit Fannie and Freddie’s size, given scale may be key to propping up the housing market during a downturn. The proposal’s emphasis on risk-based capital and CRT likely ensure adequate ROE to support a relisting. (03/20/20) 4. What’s at Stake for Mortgage Originators? Fannie, Freddie PLS Treatment May Change Less dependence on Fannie, Freddie. Despite the virus’s destabilizing impact, we expect a new capital rule may make concessions with future portfolio lending or private label securities in mind, though Fannie and Freddie may retain their implicit and explicit guarantee advantage. The proposal’s procyclicality, which would have turbocharged qualified mortgage demand as prices rose, likely remains curtailed, improving bank competitiveness. The rule may reflect a new appreciation for the fragility of some nonbank originators. (03/20/20) 5. What’s the Issue? Rule Documents: ·2018 Enterprise Capital Requirements Proposed Rule (will be superseded by 2020 proposal) Industries Impacted: ·Mortgage gurantors Fannie Mae and Freddie Mac ·Mortgage originators including JPMorgan, Bank of America, Wells Fargo, Quicken Loans, U.S. Bancorp ·Mortgage insurers including Arch Capital, Essent, Genworth, MGIC, Radian, United Guaranty Government Entity: ·Federal Housing Finance Agency (FHFA) Fannie and Freddie’s capital requirements. FHFA is increasingly likely to adhere to its 2018 capital rule proposal when issuing a new version under Director Calabria. The rule likely requires enough capital to be a significant barrier to entry for competitors and takes on a more counter-cyclical character. Under a 2018 proposal, Fannie would have needed $115 billion and Freddie $66 billion as of September 2017 — enough capital to cover the government-sponsored enterprises’ “peak cumulative losses,” according to FHFA. (03/20/20) 6. What Else? Treasury becomes the bottleneck. If an accommodative proposal comes in May, which we see as reasonably likely, the bottleneck will be Treasury’s willingness and ability to proceed, which will depend on virus containment, fallout and the 2020 election. While the proposal will be recognizable, we still expect mark-to-market LTVs to be ditched. Deferred-tax-asset fixes likely remain to avoid large paper losses. The GSEs’ new business model is likely made permanent with exemptions for trust assets and credit risk transfers (CRTs). (03/20/20) Final Rule Likely Informed By 2018 Proposal -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Calabria would probably just say this rule is in direct response to the stressed environment the virus has caused. Mark Calabria: "The reproposal will look a lot like the previous version, he says, adding that the goal will be to have a rule that makes the companies “economically attractive” while also being sufficiently capitalized to survive in a stressed environment" -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

In a recession the incumbent very rarely wins re-election. But given what was said at the Goldman meeting 2-3 weeks ago (source: Managing Director at major inv bank), and corroborated with what ACG is hearing (I know, I know, not everybody trusts them), the actions will be irreversible even if Trump loses. And they expect some of those actions to take place after the election, but during calendar year 2020. I verified with 3 lawyers that agencies can, in fact, take irreversible actions in a lame-duck period. So I don't think the election is all that big of a deal anymore. At the very least, it is only a fraction the importance it would be if irreversible actions didn't take place. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

FHFA Will Delay Capital Rule Plan Until Late May, Calabria Says By Elizabeth Dexheimer (Bloomberg) -- The Federal Housing Finance Agency will delay seeking public comment on a new version of proposed capital rules for Fannie Maeand Freddie Mac until “probably the second half of May,” Director Mark Calabria says Wednesday. FHFA is currently under mandatory telework concerns over the spread of coronavirus and so won’t be able to hold the kind of meetings it typically would during a rulemaking and public comment process, Calabria says in a call with the Exchequer Club of Washington. “Our ability to hear from the public is compromised,” he says in explaining the decision to delay the seeking comment on the rule until late May “We continue to do work on the new rule, and the rule will be ready, but we’re going to be cognizant of the fact that it’s going to be very difficult for people to weigh in,” Calabria says. The reproposal will look a lot like the previous version, he says, adding that the goal will be to have a rule that makes the companies “economically attractive” while also being sufficiently capitalized to survive in a stressed environment. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Mark Calabria: "The reproposal will look a lot like the previous version, he says, adding that the goal will be to have a rule that makes the companies “economically attractive” while also being sufficiently capitalized to survive in a stressed environment" -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

If anybody on this board has some powerful contacts, get this idea in their hands pronto. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Katy O'Donnell @KatyODonnell_ Calabria: "I don’t see [virus crisis] as greatly delaying what we’re trying to do with fixing Fannie and Freddie." If anything, he says, the stressed environment underscores need for getting them to safe and sound position. Although Calabria did earlier say re-proposal delayed until mid-to-late May. So, ironically, as seysmont and cherzeca alluded to, this crisis could speed up the process. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

I don't think it will happen, but at the same time I wouldn't be surprised if we're made whole (or close to it) much earlier than anyone expects. seysmont from Google Groups said this yesterday: "Before UST was maximizing profits. During the crisis, their priorities have changed to battling the crisis. It's a whole new math for them. When you look at ways to maximize UST returns, you operate with constraints. Constraints are all gone. Our protection is we are not convertible. Helicopter money is here. The UST priority is to help home owners now, not maximize their profits. Helps MBS holders too. It's all on the table now."