Luke 532

-

Posts

2,931 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Luke 532

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

True, even if they call it what it is (an SPO), 200B would still dwarf the largest which I think was 70B or so...but don't quote me on that number. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Public offering "neither too little nor too big" according to IMF: I like the "not too big" part, although it's admittedly ambiguous. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Still don't understand why Buffett's name doesn't come up in discussion. Great cover for the administration (can announce with picture of Buffett receiving Presidential Medal of Freedom from Obama), perfect legacy solution/career capstone to Buffet's cash problem. There were rumors, albeit not discussed on the COB&F boards as far as I know, that Freddie executives were in Omaha back in early November. Probably just for a nice steak dinner and nothing more. :) -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Dick Bove, fwiw... https://valuewalk.com/fannie-mae/ -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

thanks. no potential 4th amendment until post election, if ever. That's not what it says. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

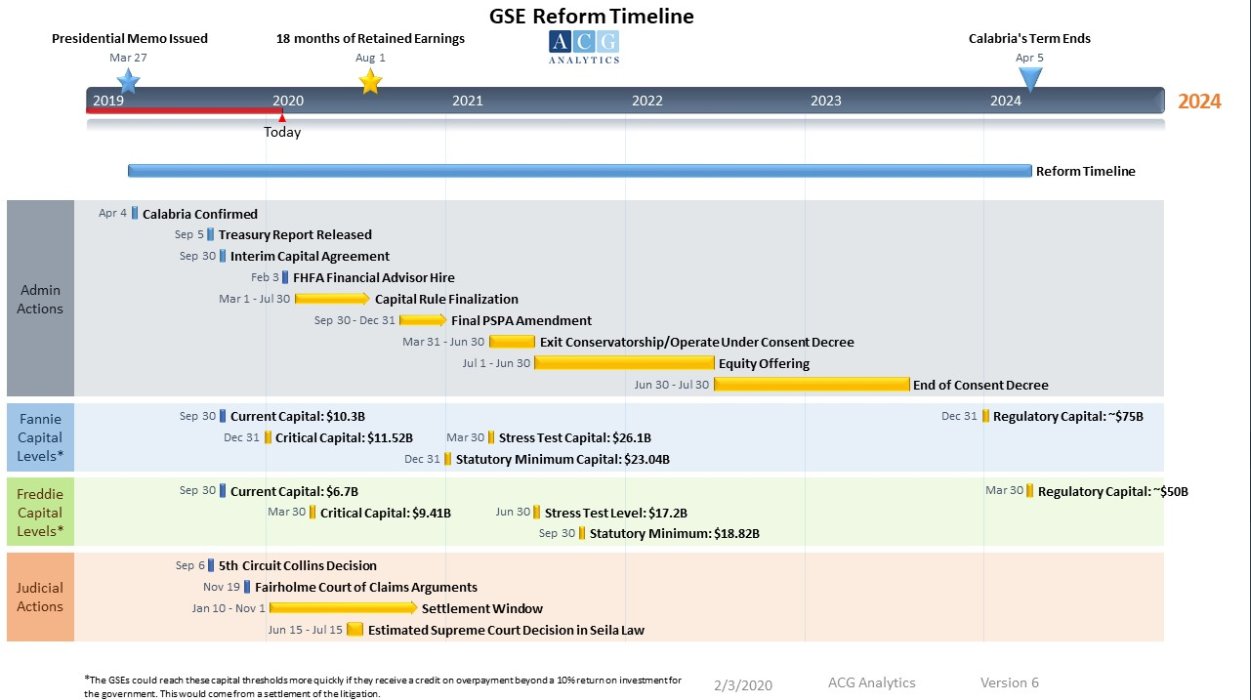

Updated ACG timeline attached (as of February 3, 2020)...

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

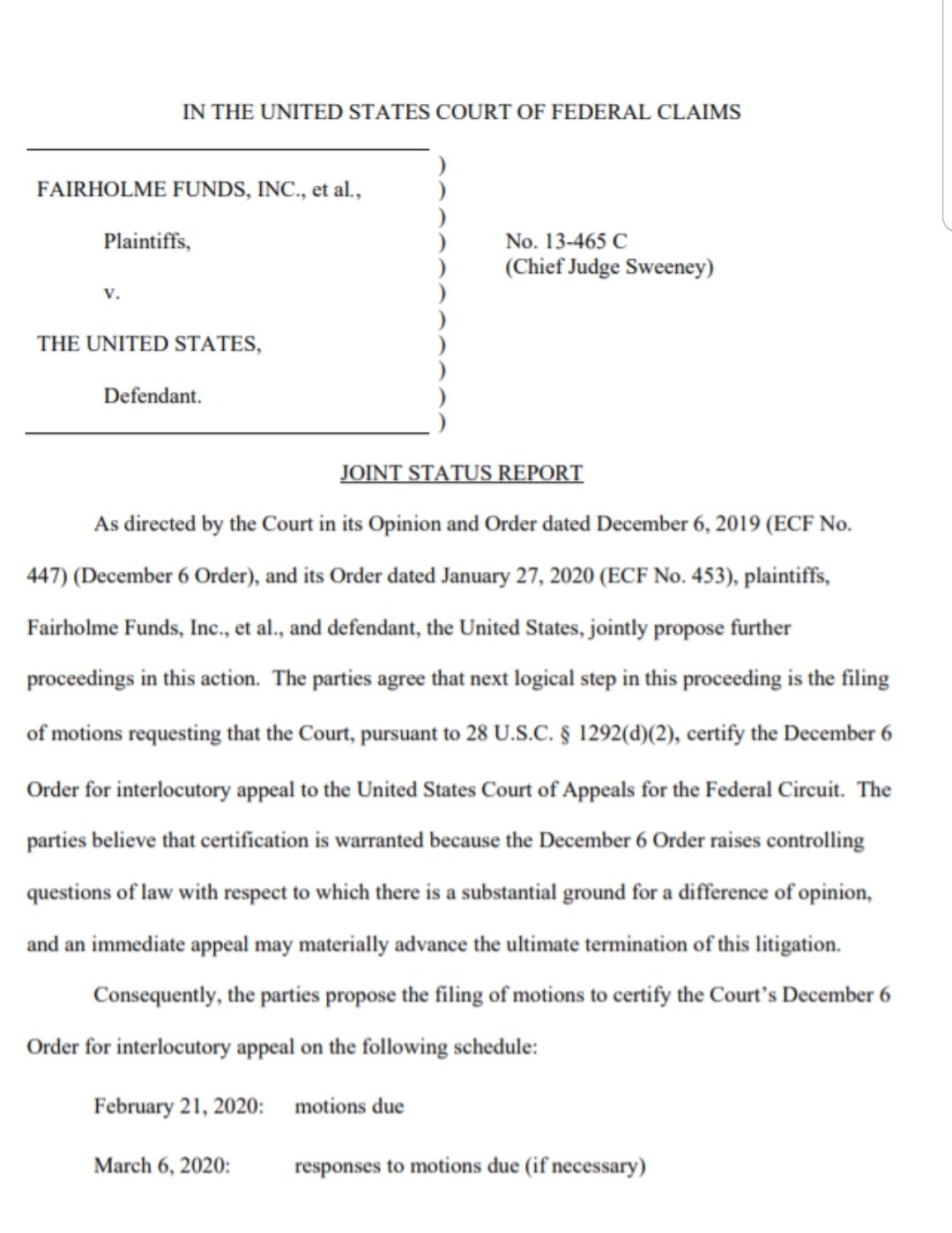

"ultimate termination of this litigation" mentioned in today's joint status report.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

A trillion common shares for every pref share, Emily, not a zillion. Be realistic. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Interesting... FHFA renames the "Division of Conservatorship" to the "Division of Resolutions" https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Realignment-of-its-Agency-Structure.aspx -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Seems like Treasury pre-screened Houlihan a few months ago... https://www.bloomberg.com/amp/news/articles/2019-09-04/treasury-discussed-hiring-houlihan-to-advise-on-fannie-freddie?__twitter_impression=true -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Tim Howard agrees... https://howardonmortgagefinance.com/2020/01/16/how-we-got-to-where-we-are/#comment-14439 I would encourage readers to listen to the transcript of the call themselves. It’s only half an hour long, and David’s discussion is thorough, informative, and accessible to a generalist audience. For those looking just for a main “takeaway,” though, I would say it is that the administration is not likely to get certainty about the legality of the net worth sweep and Treasury’s liquidation preference in Fannie and Fannie before the end of this year, so if it wants to put in place an irreversible process for releasing Fannie and Freddie from conservatorship before the election—after which both FHFA Director Calabria and Treasury Secretary Mnuchin may no longer hold their current positions—it will need to initiate settlement discussions with plaintiffs without that legal certainty, and successfully conclude them by November. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

There's a chance they don't see that as possible. I'd say it's not very probable, but certainly possible. -

Prime broker or reguard brokerage going bankrupt

Luke 532 replied to hyten1's topic in General Discussion

the principal shareholder, peterffey, is very interested in his reputation (which is stellar). I wouldn't think he would walk away Thank you. -

Prime broker or reguard brokerage going bankrupt

Luke 532 replied to hyten1's topic in General Discussion

I wonder if anybody knows the potential risks of Interactive Brokers as a prime broker? -

Prime broker or reguard brokerage going bankrupt

Luke 532 replied to hyten1's topic in General Discussion

I'd be interested in hearing thoughts on this as well. Resurrecting a 10 year old thread :-) -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Notes from today's call... David Thompson: "Bottom line is that government is in massive litigation pressure." Lamberth is full steam ahead. The indication is that both issues before SCOTUS are "being held." This means they are waiting for resolution in the Seila Law vs CFPB case. If they were going to deny, they would have already. If they were going to hear the case, they would have already. The Seila Law vs CFPB case is being heard March 3rd and decided last week of June. Then SCOTUS will decide on our case. This "being held" is not bad for plaintiffs. Tim Pagliara asked David Thompson about settlement... he can't comment on any previous discussions or possible future discussions but said there is massive incentive for government to settle (don't have to pay $125B in cash, NWS not invalidated and dictated by courts so it would be completely out of gov't hands how that is done, etc.). He said none of the cases will be resolved in gov't favor prior to the election, so unless they want to roll the dice on him being re-elected, they need to settle prior to then. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Justices issue more orders, but no action on high-profile cases https://www.scotusblog.com/2020/01/justices-issue-more-orders-but-no-action-on-high-profile-cases/amp/?__twitter_impression=true ACG response, for what it's worth... Yes, but the 5th Circuit will now be remanded to the District Court in Texas. This is not good for the government. And Pagliara's response to ACG... Absolutely Correct. Watch for the announcement @_InvestorsUnite @timpagliara for the time of our conference call with lead attorney David Thompson on January 24th. He will explain the ruling and the strategy going forward. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

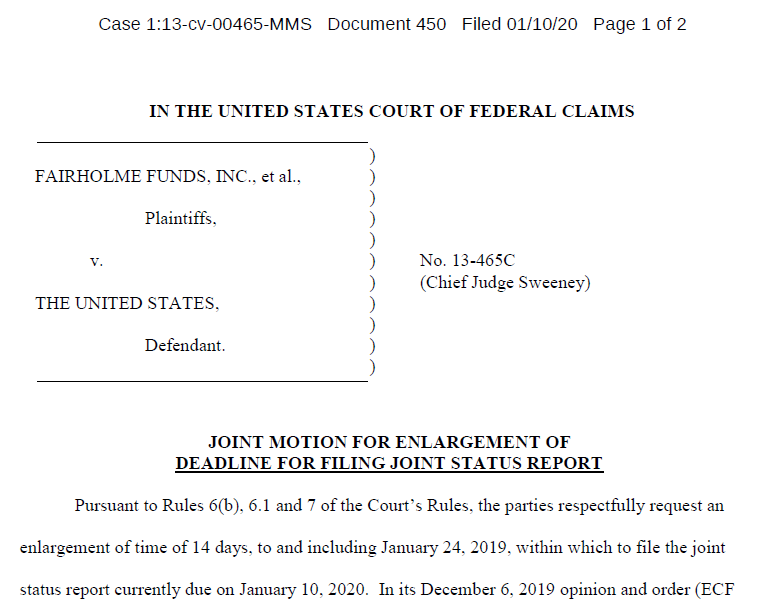

Joint status report due today has requested 14 day extension. Typo in document...should be January 24, 2020.

-

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Nothing new to us here, but Calabria confirms today that Congress is not needed to exit conservatorship... Calabria at WHF lunch: “I can only call it a myth, the belief that somehow got out there that [Fannie and Freddie are] not supposed to exit conservatorship without congressional action.” -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Agreed. They probably just wanted to publicly state their objection to delays, knowing it won't have any impact on the process. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Trades Express Opposition to Re-Proposing GSE Capital Rule https://www.insidemortgagefinance.com/articles/216794-trades-express-opposition-to-re-proposing-gse-capital-rule?v=preview Trade groups representing independent mortgage lenders and homebuilders aren’t too thrilled with the Federal Housing Finance Agency re-proposing the regulatory capital rule for Fannie Mae and Freddie Mac. In a recent letter to FHFA Director Mark Calabria, the groups were critical of the move, warning that a re-proposal would ultimately delay the process. The letter was written by Ed Wallace, executive director of the Community Mortgage Lenders Association, and signed by the executives of the Independent Community Bankers of America, the Community Home Lenders Association and Leading Builders of America. The American Bankers Association and the Mortgage Bankers Association were not part of the group. The signees agreed that some of the previously issued capital rules may require “adjustment,” but still, they’re concerned. For more details, see the new edition of Inside MBS & ABS, now available online. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Thanks for the responses. I agree with you guys, just looking for opposing viewpoints if anybody has one. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Curious of everybody's thoughts on Bove's comments below. This was in the text of his e-mail this morning... 1. For preferred shareholders the next event will be in mid-January when the Supreme Court decides whether to hear arguments on the many GSE lawsuits. Failure to review would be devastating and but it is widely believed that the court will take up the GSE issues. The rest is in the attached document, but I'm more curious of your thoughts on the quote above. Bove12-29-2019.pdf -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

WASHINGTON — Even though Fannie Mae and Freddie Mac are still controlled by the government, 2019 saw some of the first signs of progress in efforts to end the mortgage giants' federal conservatorships. The Federal Housing Finance Agency, which regulates the government-sponsored enterprises, gained a new Trump-appointed director with his sights set on releasing Fannie and Freddie from the government's clutches. Mark Calabria took initial steps to prepare Fannie and Freddie for the private sector, making it a priority to improve the companies' capital position. Capitalizing the GSEs is expected to stay in the focus in 2020, particularly as the agency retools a risk-based capital rule Calabria inherited from his predecessor. “The capital rule is one of the most important rules I will issue as director,” Calabria said in November. “This rule will be re-proposed and finalized within a timeline fully consistent with ending the conservatorships.” Bloomberg News Two months earlier, in September, the GSEs were permitted to retain billions of dollars more in earnings to build up their capital cushions, and in the same month, the Trump administration published a report detailing its principles for an overhaul of the housing finance system. Although many expected FHFA Director Mark Calabria to finalize a post-conservatorship capital framework for the GSEs that was originally proposed by former Director Mel Watt in June 2018, Calabria spent months deliberating the direction he wanted to take with the proposed rule before ultimately deciding in November to re-propose the framework. The original proposal under Watt called for assessing the GSEs' credit risk for different mortgage categories, and would have included market and operational risk components in measuring the firms' capital strength. While it remains to be seen what exact details of the rule Calabria might change or keep intact, he said Dec. 10 that his goal is to be able to issue his own iteration of the capital framework “sometime early in the first quarter.” FHFA is also in the process of hiring a financial adviser to help the GSEs raise capital. After the agency hires its financial adviser, Fannie and Freddie will also hire their own financial advisers, Calabria has said. Calabria has also said that he hopes to formalize various private directives issued to the GSEs during conservatorship as rules sometime next year and plans to enhance the FHFA’s own capability as a regulator. This will include launching a macro forecasting unit that would be able to evaluate Fannie and Freddie’s house price forecasts. He also hopes to be able to lift the $45 billion retained earnings cap, he said in October. But heading into the new year, mortgage policy watchers are zeroing in on how the FHFA will approach risk-based capital requirements. “The final capital rule is going to be about what are the appropriate levels to protect taxpayers when they emerge from conservatorship,” said Scott Olson, the executive director of the Community Home Lenders Association. And that determination will be “very significant,” said Mark Goldhaber, a principal at Goldhaber Policy Services who also serves on the board of the Center for Responsible Lending. “The capital rules lead to pricing, and in this case, it's going to lead to what loans go to [the Federal Housing Administration] versus what loans really are going to go to the conventional market,” he said. One of the major concerns about the original proposed capital framework that various groups expressed in comment letters to the FHFA was that the rules were too procyclical and could leave the mortgage giants severely weakened in a crisis. “It requires additional capital at exactly the wrong time — once stress has already occurred,” said Tom Parrent, a principal at Quantilytic LLC, a financial and biostatistics research consulting practice. “It would not only be very difficult to raise capital under stress and would probably shut down large segments of the market, but it would also mean that the fees charged to the homeowners would increase at that time, reducing demand for new loans.” A degree of regulatory forbearance is an essential tool in an economic downturn, Olson agreed. “That's the way things have been done historically and that's the way it should be here, as opposed to having too strict of an adherence to very high levels of capital all the time and you freak out if your capital gets depleted in a down cycle,” he said. Calabria himself acknowledged the concerns that the original proposal was too procyclical in a December speech at the Federalist Society. “The very purpose of Fannie and Freddie and the Federal Home Loan banks is to be countercyclical, and my belief is that they have been a little too procyclical in the past,” he said. “I think it’s critical as we re-propose the capital rule that how do we make sure that we’re having a capital rule that is countercyclical rather than procyclical?” To combat procyclicality, Parrent suggested that the rule incorporate a contingency reserve that could be built up over time, a device used by some insurance companies. For it to work at Fannie and Freddie, a portion of guarantee fees could be set aside in a reserve that would only be used to pay claims during periods of financial stress. “Once the reserve dollars have been held for 10 years, they can be released and replaced with fees generated on new loans,” Parrent said. In fact, the FHFA should contemplate a capital regime by looking at the GSEs through the lens of insurance companies and not banks at all, Goldhaber said. “You've got to start with a baseline that says nobody wants to see them in an undercapitalized state as they were before the crisis,” he said. “The question really becomes using the right capital framework to achieve the appropriate level of capital, and the reality is, these entities look a lot more like insurance companies than they do banks.” The GSEs’ capital framework could also be a hybrid of a bank and insurance company capital framework, said Pete Mills, senior vice president of residential policy at the Mortgage Bankers Association. “That's where I think there will be differences as a guarantor versus a holder of risk. Banks lay off risk as well, but they retain capital against the risks that they lay off,” he said. “So it won't look exactly like bank capital either, but in terms of overall levels of capital for various mortgage exposures, they're going to try and get some rough equivalency is my guess.” Olson said it’s critical that the capital framework take into account the development of the credit risk transfer programs at the GSEs and the two companies’ risk-sharing activities. “Particularly if it's a utility model that's being used — which we think is the right way — they're more of an insurance company type of operation, as opposed to a risk-based operation,” he said. “It's a pretty vanilla product. It's not that it's not risky at all, it's just that bank capital standards seem inappropriate, because they're not doing commercial loans. They're doing more of an insurance.” If the FHFA developed a capital framework that either required the GSEs to hold too much or too little capital, there could be serious consequences, Parrent warned. “If you had a capital structure that was too liberal, as the market feels that stress is approaching, the reinsurance and transfer trades would stop, and the GSEs would end up holding all of that risk because they would have a beneficial capital position relative to the reinsurers,” he said. But at the same time, “you don't want the GSEs to have to hold a punitive amount of capital where the reinsurers are basically arbitraging that,” Parrent said. In that kind of a regime, not only could people be pushed out of the housing market, but they could be forced into the less-regulated mortgage spaces, like the subprime and nonqualified mortgage markets, he added. -

FNMA and FMCC preferreds. In search of the elusive 10 bagger.

Luke 532 replied to twacowfca's topic in General Discussion

Capital, capital, capital by Hannah Lang, American Banker https://www.americanbanker.com/news/fhfas-focus-in-reforming-gses-capital-capital-capital