giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by giofranchi

-

Eric, I understand the comparison, but don’t agree 100%. If they were truly the same, both Mr. Buffett and Mr. Watsa wouldn’t have taken the trouble to run insurance operations, right? Instead, the difference is clear enough to me: once again I repeat that “safety” comes first. And, if you write insurance profitably, nobody can take the leverage provided by float away from you, no matter what. To paraphrase Mr. Buffett: Even the best funds, see for instance Mr. Berkowitz in 2011, don’t enjoy such a luxury and constantly risk to disappoint their clients… In insurance you are working for yourself, not for clients: apparently, it seems a small difference, in practice I think it gives a huge advantage to insurance over leveraged funds. giofranchi

-

Did you count taxes in this equation? An unlevered stock mutual fund pays no taxes. You will own taxes once, on the original cap gains/dividends as they pass through to you. All else the same, FFH has to earn a higher return on investments to generate the same net return to investors because of the double taxation in the corporate structure. This mitigates the benefits of cheap leverage to some degree. When I did the math, Eric corrected me as follows: So, yes, taxes are included. giofranchi

-

Al, why do you think insurance operations will always be run poorly? Isn’t it different to try and turn around deeply troubled insurance companies, which had made silly promises in the past, than to be now free from the past and to make new, well thought-out, and carefully studied promises? Isn’t it different to try and build scale in the insurance industry, and to increase rapidly the float generated and managed, accepting to buy deeply troubled insurance companies at a discount, than to run an organization now more focused on profitability than growth? Why do you expect the two situations to yield the same results? Maybe, I am seeing things through rose-colored glasses, but I seriously don’t understand… What about last quarter? Was it difficult for everyone, or do you think FFH will be alone to suffer, because of its own bad decision making? I have already written exhaustingly and boringly enough about my view on the equity hedges, so you are spared! I won’t repeat me here! :) With regard to your 20% annual return, I can only say one thing: sell you FFH shares immediately!! As I have always plainly admitted, I have nothing to say to people who can compound capital at 20% annual. My only game is to find businesses that I can understand, that I think will be safe no matter what for many years into the future, and buy them when the price is right. Then I stick with them. This clearly is not the recipe to compound capital at 20% annual… At least, not with my own poor abilities… giofranchi

-

Stewardship Rating… Standard?!?! … Well, ok … If FFH’s management is “standard” I’d better give up, and find a good and honest job, because I am clearly not made for business… :( giofranchi

-

Eric, in any business I look both at safety (first) and growth (second). The leverage provided by float cannot be enjoyed by any unleveraged stock mutual fund. The fact FFH has to achieve a 7.5% annual return on its portfolio of investments, to compound BVPS at 15% annual, means a lot to me. Should mean a lot to any business owner! (It is the reason why Mr. Watsa first got involved with insurance...) Because FFH’s management will not be under the pressure of achieving 15% on their investments, like an unleveraged stock mutual fund would be. And that is great safety imo. Rationality is among the most important things to be successful in business, and rationality is high, when we are calm and have options; vice versa, it is low, when we are under pressure. You also clearly don’t believe that FFH could achieve an underwriting profit… Nobody would believe that, based on FFH’s history, but I think that the future will be different and more profitable than the past. We will see! :) giofranchi

-

Clearly those guys at Morningstar are following too many companies, and they have not done their homework on FFH. FFH’s fair value: After 3 years of no growth, with 30% of the investments portfolio in cash, and all equities hedged, $370 is a conservative way to value FFH BVPS. Of course, these things will fluctuate, because FFH is strong enough to report “mark-to-market”… You all remember that in March 2009 “mark-to-market” was removed, right? Otherwise, US banks would have been insolvent. Even today many European banks would be insolvent, if they had to report “mark-to-market”… Yet, even if Q2 2013 BVPS might be substantially lower, $370 is a conservative value. Now, I tend to think about BRK as a safer business, with fewer opportunities for growth. More safety, less growth: all in all, I would apply the same multiple to both businesses. Here a remark is due: you all tend to think about BRK as a safer business… but, actually, I am not so sure… Imo, even more than growth, safety is strictly dependant on the quality of the people at the helm… And I would put Mr. Watsa and his team second to none! Given the fact that I think Mr. Buffett would not repurchase BRK share, if they weren’t at least 35% undervalued, I would put a multiple of 1.2 / 0.65 = 1.85 to BVPS, to calculate FV. Why not? The S&P500 is selling for 2.46 x Book Value and it has done and will probably continue to do more poorly than both BRK and FFH (on a ROE basis). Therefore, we are left with a FV for FFH of $370 x 1.85 = $685. Morningstar itself uses a multiple of 1.65 x BVPS, to calculate BRK’s FV. If we use 1.65 for FFH as well, instead of 1.85, we get: $370 x 1.65 = $610… still much higher than $325… giofranchi

-

Ok, let me ask you a question: if it were just between you and me, no Mr. Market involved, would you sell your shares of FFH at $380 to me? I would buy them without hesitation. But, forget about having them back at a later date. Because I won’t sell them back to you or to anyone else for anything below $700! If your answer is no, you are playing the market with the shares of a company that already is undervalued. If it weren’t undervalued, your answer would be yes (but, of course, you wouldn’t be receiving this offer from me!! ;)) Well then, good luck! What happened yesterday? giofranchi

-

If the US ever succeed in getting its health-care costs under control, which means just in line with the rest of the world… no dramatic virtuousness required here!, they would really become once again an unstoppable force! ;) giofranchi

-

Cannot wait to watch this movie! ;D ;D ;D giofranchi

-

It is 10:40 PM where you live! So, though very late..., I am not too late to wish you a happy birthday! :) Cheers! giofranchi

-

Hi shalab, you know that I strongly believe in “deliberate practice”. All of us, if we practice in the right way, are capable of great things and of reaching great goals! Yet I also believe that the “right way” to practice most of the times is elusive… very hard to find… and in our endeavors we often fool ourselves into thinking that the right path is in front of us, when actually it is not… And we lose precious time… And we finally realize that something is still missing… And we lose faith and motivation… Sadly, it happens too frequently… That’s why I think that as much as I try to study Novak Djokovic, and practice like him, I’d still be losing against him on a tennis court… That’s imo the true role luck plays: some people, very few, get all the numerous and complex pieces of the “deliberate practice” process exactly right! Think about Novak: since the age of 5 he is followed each day by a team of “experts”… Probably for the first 10 years he made no choice, the team of experts chose everything in his stead… And the choices to be made were a lot! Change even the slightest thing in that child, and we would not have the Djoko-robot we admire today… Then, came his turn to make choices… Can you really believe they were all carefully planned and thought out?… I don’t think so… A lot of randomness here as well! That’s why it is very difficult, almost impossible, to device a “deliberate practice” that is so effective and so successful as the one followed by Nole his whole life! BUT… The way we humans have devised business is fortunately much different from the way we have devised sports! In tennis I just cannot jump on the shoulders of Djokovic and share with him the title of number one tennis player in the world… what a shame! In business, instead, not only I certainly can study great entrepreneurs and investors, not only I certainly can practice like them, but fortunately I can also invest in their companies and reap the benefits of their very unique and ultimately hard to fathom history of wildly successful “deliberate practice”! And Biglari, given his young age, really is a Djokovic: can you name some entrepreneur and investor of the same age, who has already been more successful? No? Well, me neither! Among people still in their ‘30s, he is number 1. You see? As far as I am concerned, that is the most important thing. All else is just noise. Hey, listen: “King Icahn” was published in 1993, and rereading it now, it is clear that he already was an outlier! Then, you would have had 7 more years to study and follow him… without investing a dime in his company… just building more and more confidence in his process and abilities… finally, if you had invested with him in 2000, now you would have 11 times your initial capital… 11 times!!!! While the S&P500 almost went nowhere!! But… well, I know… he was not really shareholders oriented… he was too greedy… not someone you can truly rely on… etc. etc. And so, when I asked who had actually invested with Mr. Icahn in 2000, nobody answered… What I mean: when they put together the Avengers team, do you think they worried much about the fact The Hulk is unreliable?! ;D ;D ;D No, seriously… I still like the BH platform and I still think Biglari is among the very best investors out there. giofranchi

-

No NAV per share in that report? NAV is reported on a weekly basis… not on the monthly report. :) giofranchi

-

Thank you SD for your numerical example! Yet, my question remains unanswered: why do you suppose Mr. Barnard ignores what you have written?! Instead, I am almost sure he is very well aware of it! Anyway, he stated that one of FFH’s goals is to become as highly regarded on the insurance side of the business as it already is on the investment side… So, is he promising something that cannot be attained?! Knowing how FFH has always been conservative in its promises to shareholders, that would struck me as highly unusual… almost unprecedented! Also, Mr. Watsa has very often repeated that with interest rates so low “there is no place to hide” for the industry, unless an underwriting profit is achieved. To reach for yield, when it is reckless to do so, clearly is not the solution. So, two things might happen: 1) An hard market develops and CRs fall, 2) Insurance as a business will cease to be a viable option for the private sector. As it always happens for a necessary service that cannot be fulfilled by the private sector, because returns on capital are not adequate, the whole insurance industry will be gradually nationalized… giofranchi

-

--“King Icahn” ;D ;D ;D giofranchi

-

June 2013 Monthly Report giofranchi 2013-6-June-Monthly-Report-TPOU.pdf

-

Hi Joel, I wouldn’t be so sure… last time that I checked, MKL had substantially larger investments in stocks, as a percentage of equity, than FFH! giofranchi Hi Gio, I think he was not talking about the portion of equity in the portfolio, but instead the float / book value ratio for the company (i.e., that FFH had more float to shareholders equity of FFH than the corresponding ratio at BRK). Yes, I understood what he meant, but I am not so sure I would agree… In a stock market decline, the losses that will hit your capital are only the losses you would incur on the stocks portfolio… the rest of the float is invested in bonds, or something else… am I wrong? So, which equity will shrink more in a stock market decline? FFH’s or MKL’s? I think MKL, because its portfolio of stocks is worth a higher percentage of equity than FFH’s. This of course was before the merger with Alterra. Let’s do some very simple math: FFH: Total portfolio of investments = 30 Equity = 10 Portfolio of stocks = 6 Portfolio of bonds + cash + privately held companies + etc. = 24 MKL: Total portfolio of investments = 20 Equity = 10 Portfolio of stocks = 8 Portfolio of bonds + cash + privately held companies + etc. = 12 Let’s assume a 40% decline in the stock market, and let’s assume their holdings go down with the market. Let’s assume also that bonds + cash + privately held companies + etc. don’t change. The two resulting scenarios would be as follows: FFH: Total portfolio of investments = 27.6 Equity = 7.6 Portfolio of stocks = 3.6 Portfolio of bonds + cash + privately held companies + etc. = 24 MKL: Total portfolio of investments = 16.8 Equity = 6.8 Portfolio of stocks = 4.8 Portfolio of bonds + cash + privately held companies + etc. = 12 Although FFH’s total portfolio of investments is 3 times its equity, while MKL’s total portfolio of investments is only 2 times its equity, the same price decline in stocks would be more detrimental to MKL’s capital than FFH’s: in the MKL case it would decline from 10 to 6.8, in the FFH case, instead, it would decline from 10 to 7.6. This is because MKL’s stock portfolio at the beginning was a higher percentage of its equity than FFH’s: 8 / 10 = 80% in the MKL case, and only 6 / 10 = 60% in the FFH case. If I am wrong, please correct me! giofranchi

-

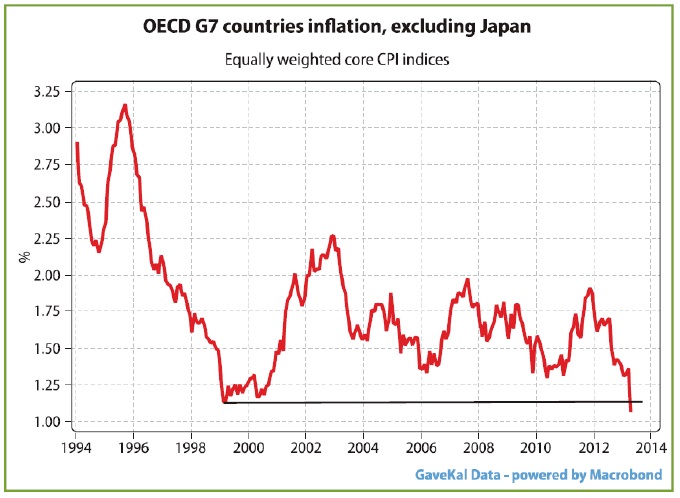

Please, look at the image in attachment: maybe, FFH's CPI linked securities are starting to recover? giofranchi

-

Hi Joel, I wouldn’t be so sure… last time that I checked, MKL had substantially larger investments in stocks, as a percentage of equity, than FFH! giofranchi

-

Jay, could you please elaborate a little bit further? Bonds are in a secular bull that has been lasting for 30 years now… Thank you, giofranchi

-

Sorry to all, if sometimes I seem too “aggressive” in expounding my thesis about FFH… I know criticism and skepticism are very important, and I thank you all for pointing at weaknesses in my reasonings! Anyway, when your thesis is the object of criticism and skepticism, even though you know they will ultimately be very useful, it is not always easy to keep calm, and answer in a relaxed and gentle manner… my fault!! giofranchi

-

premfan, I don’t think it is that easy… If it were, please explain Japan and Europe! Of course nothing is certain! I just look for something that has the potential to compound capital at 15% annual for a long time, try to understand it as deeply as I can, and then stick with it. That’s all! giofranchi

-

SharperDingaan, I am not sure I have understood what you mean… but I think I have grasped that you don’t believe in an improvement of FFH’s insurance operations. To that I can only say I have great respect for Mr. Barnard and all he has achieved at OdysseyRe, and great faith in what he could achieve overseeing all FFH’s insurance operations. You said annual weather events are getting more frequent, more certain, & more severe… So what? Tell me the rules, and I will make money! Change can only help a great manager like Mr. Barnard, because he will assess it better than other insurers and better than the insured, therefore will be able to benefit from it! Insurance is not going away… and it will always be a relative game: the best managers will make money, all the others will lose money. And Mr. Barnard is among the very best! ;) giofranchi

-

ap1234, I was talking about the BRK of today as an example of what FFH could become tomorrow. You say that FFH will always have a high percentage of assets invested in bonds… Why? Regulatory constraints? Maybe… but I am also convinced that Mr. Watsa and his team will go on seeking the best investment opportunities, available within regulatory constraints! If bonds face serious headwinds in the years ahead, Mr. Watsa and his team will reduce the percentage of bonds in their portfolio of investment as much as possible. Don’t you agree? giofranchi

-

These are the net investment numbers and I'll leave it at that, most of this is a waste of time anyway. http://en.wikipedia.org/wiki/Net_international_investment_position PlanMaestro, I agree: it is a waste of time. ;) giofranchi

-

shalab, sorry but I am not sophisticated enough… at page 3 of the file you have previously posted, I have found a 3.2% personal saving rate for May 2013. That’s the figure to compare with the 2.6% in February 2013. And for that figure I have a chart that goes back to 1959. So I can put those numbers in an historical context. Vice versa, I lack a similar chart for the FFA, so a 10% rate is meaningless to me… But, if you could post it, I will be glad to examine which kind of information it really provides. Thank you, giofranchi