giofranchi

-

Posts

5,510 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by giofranchi

-

Hi Al! Thank you very much, and don’t worry: I have gone nowhere! ;D ;D I just heeded Cardboard’s suggestion and read about a company I didn’t know very well: SPLP – Steel Partners Holdings. It is a small-cap, led by a very shrewd capital allocator, who is an activist value investor, with an excellent track-record as hedge fund manager (+20% annualized sustained for 18 years), and who is still young. He has already been able to increase Diluted Normalized EPS for SPLP as follows: 2009 ($0.3), 2010 $0.6, 2011 $0.97, 2012 $1.22, and there is a lot more growth to come in future years. What do you have to pay to partner with him today? 0.8 x BVPS. So, I have posted some thoughts and articles on the SPLP thread. Cheers! Gio

-

Great! Thank you very much! :) Gio

-

Thank you, David! Very interesting! In fact, I was wondering when it would happen. The article doesn’t specify the date TPRE will start trading on the NYSE. Do you have any clue? giofranchi

-

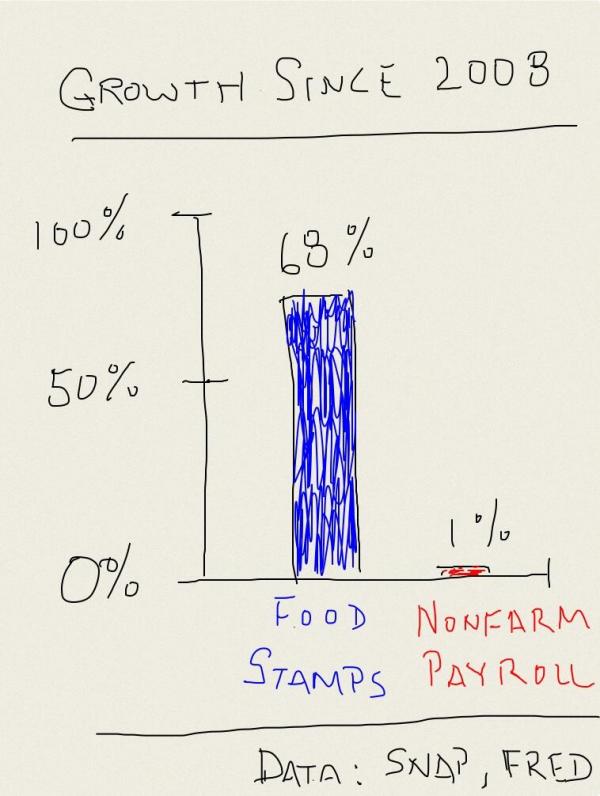

Growth since 2008... ;D ;D ;D giofranchi

-

Interesting observation. I agree. I enjoy gio's posts very much. I hope he continues to kick the tires of ffh & his stalwart belief in its mngt every which way from sunday for as long as it remains controversial & polarizing in the current frothy investment regime. its not like he's having a conversation with only himself, belching out stillborn musings into the silent void. there's a whole lot of different opinions piping up at every turn. in a public forum an engaging thread is likely a long thread. LOL! I agree. I suspect he talks about Fairfax because he's very comfortable with it, the long-term prospects and isn't interested in swinging for 15%+, when Fairfax can do 15% and no tax consequences. Other than a handful of people on here, virtually no one has come close to Prem's 24% compounded since inception (over 25 years), so let's not shoot the goose until you've all laid your golden eggs! ;D Keep talking about Fairfax and Berkshire Gio, because that's why this board is called "The Corner of Berkshire & Fairfax"! Cheers! Thank you, link01 and Parsad! Very nice words! :) giofranchi

-

Cardboard, I understand your point, and thanks for your question. I will try to explain. First of all I think about myself as a businessman: I started my company in December 2004 with an initial capital of 25.000 Euros, and as of yesterday its equity is up to 1,530,830.46 Euros: a 62.25% CAGR in BV… ;D ;D ;D Of course, given my limited skills as an investor, the great majority of those earnings are operating earnings… thanks God I am clearly a better businessman than an investor! ;D I soon realized that a service company like mine suffers from two great weaknesses: 1) It soon gets to a point where, to keep growing, politics is needed: maybe in the US or Canada things are different, but in Italy the construction business is deeply linked and influenced by politics… And, unfortunately, I hate politics… 2) It almost doesn’t need new capital, so what was I supposed to do with its earnings? The solution to both weakness n.1 and weakness n.2 was immediately clear to me: diversify away from construction engineering services, purchasing other businesses. So, paraphrasing Mr. Buffett, I literally began extracting cash from a poor business, to put it into high-quality assets. But I still view myself as a businessman, a business owner, I am interested in owning assets that will grow for a long time, creating much wealth along the way. I am not interested in trading in deeply undervalued stock, and out of them as soon as they reach IV… It simply is not the way I want to live the 12 hours I work each day! Passion + 10-15%, or boredom + 15-20%? I guess we all agree on the right answer! Second, it is true I have some time to completely devote to investing and strategic thinking: both in the management of our engineering services and higher education services I am very thankful to a group of talented and motivated engineers, who constantly help me and without whom I would be lost! But, out of my 12 working hours, only 50% are devoted to investing and strategic thinking, the rest I still must commit to supervise operations and to some PR (which basically is politics to me, so I cannot stand it! ;D). Clearly, another weakness in my organization is that I don’t have a partner, who could be a COO I trust completely, and who could take off my shoulders the not so light burden to be constantly involved with operations. So, though 6 hours a day are not that bad, I am reluctant to push for the highly coveted 20%… When I know other very smart and talented people spend 12 hours each day, just to achieve that same goal! Finally, though I cannot be sure about it, I guess I spend an amount of time, writing about each company that I own, which is proportional to their weight in my firm’s portfolio! I do that for three reasons: 1) the larger a position gets to be in my portfolio, the more time I want to think about it, 2) to write helps me to clarify my thinking like nothing else, 3) to post my thinking on the board gives me the very much appreciated and useful feedback of other great investors: I seek confrontation, the more people disagree with me, the more warnings I get, the better! -- John Maynard Keynes He liked to state, though who knows if it’s true, that he spent no more than one day per week thinking about his investments. ;) giofranchi

-

I have just reread this article from 2010, and I have found it to be more up-to-date than ever. :) giofranchi Be_like_Prem.pdf

-

Al, I am sure they will go that way. But not in a hurry! Never in a hurry, otherwise you will make mistakes. And we all know the game is not how many great things you do, but how many errors you are able to avoid… For now, as I have shown, equity investing if performing very satisfactorily… of course, if you don’t count equity hedges! :) giofranchi

-

If you don’t count equity hedges, in 2012 FFH gained $1,118.7 million in equity and equity-related investments, out of a portfolio of preferred stock ($605.1), common stocks ($4,399.1), and Investments in associates ($1,355.3) of: 605.1 + 4,399.1 + 1,355.3 = $6,359.5 million. That’s a +17.6% return, which beats the S&P500 even in a very good year for the market! Then, for the first quarter 2013, if you don’t count equity hedges, FFH gained $698.4 million in equity and equity related investments, out of a portfolio of $6,712.2. That’s a +10.4% return in 3 months only. While the S&P500 achieved a +10.6%... But, of course, you don’t want to chase the index, when it is in a bubble, right?! ;D FFH purchased 51,855 shares of BBRY at an average price of $17, for a total investment of $881.5 million. At March 31, 2013 its portfolio of investments was worth $24.5 billion: the investment made in BBRY is just 3.6% of AUM. giofranchi

-

Plato, this is macro investing, and is very dangerous: in 2008 FFH was up 30%+, while the market was down 30%+… :) giofranchi FFH got down to roughly $210 in 2008 from over $300 in 2007 (or perhaps early 2008). (US DOLLARS). Hedged the entire time. In fact, hedges soaring while it was plumbing the 2008 lows. Everything thrown out with the bathwater. As for 2008's performance, the stock closed 2007 at $286 and finished 2008 at $313. Total of 9.4% gain (not including dividend). US Dollars. As you can see on its financial track record web page: http://www.fairfax.ca/Corporate/Financial-Track-Record/default.aspx In Canadian dollars FFH stock price closed 2007 at 287.00 and 2008 at 390.00: +35.89%. The fact is the USD surged against any other currency during 2008, CND included. But, even if you use USD, +9.4% plus the dividends is better than cash, right? Anyway, traders might be interested in these things… businessmen seldom are… The only thing a businessman should be fixed upon today follows: The last time FFH looked so foolish was in 2004-2005-2006, then in 2007-2008-2009 BVPS went up a cumulative +146%. You want to buy at the bottom, sell at the top, etc… Well, I am sure YOU can do that, so good for you! :) giofranchi

-

Plato, this is macro investing, and is very dangerous: in 2008 FFH was up 30%+, while the market was down 30%+… :) giofranchi

-

This is a very good point! Except for the “if you expected the collapse to come you would be best off never owning FFH in the first place (because it too will drop)” part… That is macro investing… And I never do such a thing… I am always invested in good businesses led by strong men. I just like them to be cautious, when caution is warranted, and to be aggressive, when aggressiveness is the right policy to follow. But I understand when you say: they might never be aggressive enough for my taste… giofranchi

-

Dow Jones Industrial Average Historical giofranchi

-

scorpioncapital has posted the file in attachment a few hours ago in another thread. I want to quote it here as well, because theme n.3 and theme n.4 on page 2 are of great relevance in the discussion about FFH as well: The true reason it is so hard to invest in FFH is because they constantly buy when everyone is selling and vice versa. But that is always where value is created, if you buy when everyone is selling, or protected, if you sell when everyone is buying. Both are extremely important! The focus should be 90% of the time on the creation of value, and only 10% of the time on the protection of value, but this doesn’t mean that 10% is less important! I think the protection of value is underrated and not studied enough even among value investors. giofranchi JefferiesInsights_July2013.pdf

-

These are somewhat erroneous statements and assumptions. Let me clarify the first glaring one: HWIC is nowhere near a 100 person team. 7 principals including Prem, probably about another 6 analysts and then say 5-6 managers they have capital with (I'm guessing on that, but have some information about some managers, so consider it a calculated guess). You then also have a couple of enterprises that will be acquiring businesses in certain areas like Fairbridge and Thomas Cook. In total, I think you are talking about 20-25 people! The next one I would like to tackle is the recommendation to reduce their ROE to 6-7%. This is crazy! Historically, they've done far better...closer to 24%. With the leverage they employ, they could easily return 15% ROE by achieving a 6% return on their portfolio and keeping insurance losses to historical levels. Like Berkshire, they are going to have a significant advantage over the next 20 years when they really start acquiring private companies, and the global reach of their insurance business becomes much more pertinent. They will return 15% ROE long-term for the next 20 years. Lastly, succession at Fairfax is one of the least concerns for shareholders. Succession planning at Fairfax has been in place for many years, and the people in place are probably the best they've ever had. You have Andy Barnard overseeing all of the insurance companies...a man who achieved extraordinary results at Odyssey Re, nearly on par with Berkshire's insurance businesses. You have a decentralized investment team where the bench was far deeper than Berkshire's 15 years ago! It may be the best team out there today...they definitely have one of the best fixed income minds of the last 30 years running their bond portfolio. And Prem is already delegating many duties to subordinates such as Paul Rivett and Madhaven Menon to name just a couple. Cheers! Ok… Now, I know that when Parsad speaks, people listen! And rightly so!! But… what else have I tried to "desperately" say for the last few days?!?! >:( giofranchi

-

Well, shalab, imo this makes no arithmetic sense… ??? they would have to achieve a 3-3.5% return on their portfolio of investments, to get a 6-7% growth in BVPS… I don’t even get out of bed in the morning for a 3.5%… ;) This doesn’t worry me at all. As I have shown many a time in previous posts, as a stock picker FFH is trouncing the indices hands down! Take away the equity hedges, and their investment abilities are undiminished and in plain sight! I couldn’t care less about what happens after Mr. Watsa retires… I will think about it 20 years from now! giofranchi

-

Sorry Partner24, but I don’t understand: either your aim is to protect capital, or your aim is to increase capital. If you think rationally, you know there is a time when the first policy is right, and another time when the second policy is right. I understand Packer who says: for me now is the time to increase capital, so I won’t invest in FFH, until they take away the equity hedges. I think, on the contrary, that now is the time to protect capital, so the equity hedges are part of the reasons I am investing in FFH. Two different views, but I can understand both. Do you, instead, know a way to increase capital, should the sun shine, and at the same time to protect capital, should rain come?! ??? giofranchi

-

Ok, I have understood your thinking. I would also like to know what Eric and Al think about the causes of HWIC’s mistakes today, and whether they will be able to correct them in the future. giofranchi

-

Ok. What happened after 2008? After your greatest fall, what has pulled you out of the hole? If you were able to regain lost ground, why do you assume Mr. Watsa and his team won’t be able to change course? giofranchi

-

Packer, You assume they don’t know what you have written? Of course not! Then, why? I would really like to know what you, Al, Eric, and others on the bear camp think about Mr. Watsa and his team. What do you think their reasoning actually is? And why do you think they persist in their mistakes? giofranchi

-

Al, I don’t know what is going to happen… Maybe you are right, and I will average down to the mid 200s… If that happens, it will be a major blunder on the part of the man at the helm and his team. Remember: with all their hedges they are really trying to do just 1 thing: to protect capital. If BVPS declines to the mid 200s, they will have failed miserably... Yet, it won’t change my view that profitable insurance underwriting coupled with the investment of float on a value basis is a wonderful vehicle to do business. And, if management is making such serious mistakes now, let’s hope they admit them sooner or later, and change course of action! Why shouldn’t they? giofranchi

-

"Bad Omens" by Charles & Louis Gave giofranchi 2013_07_09_OTB.pdf

-

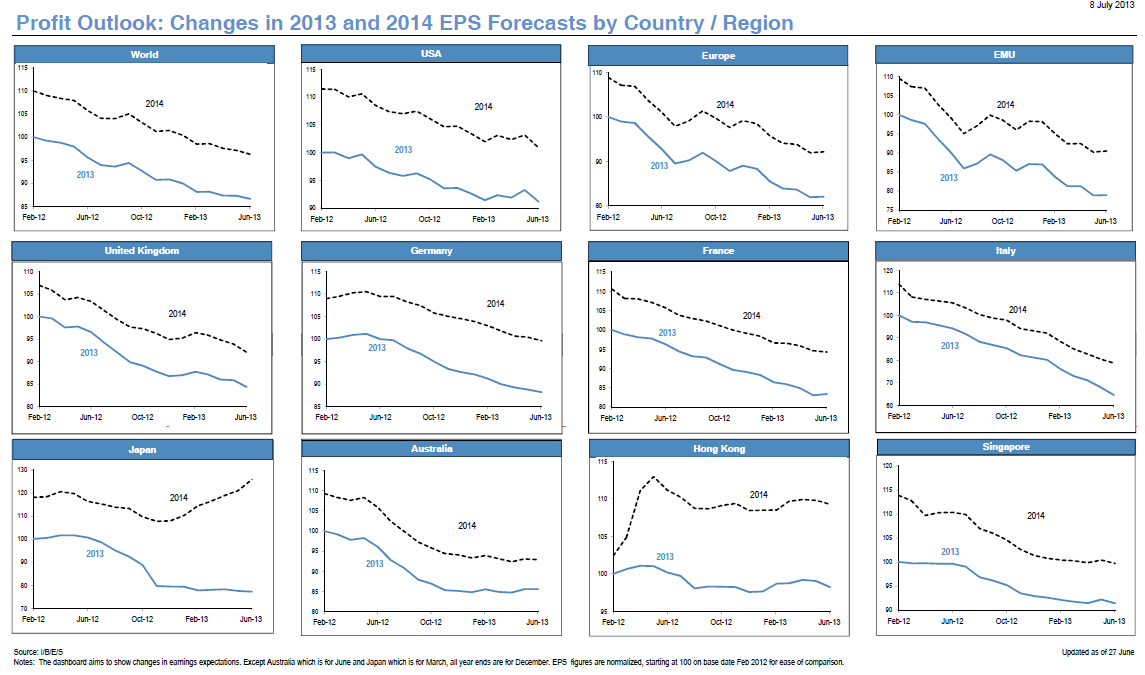

Profit Outlook July 2013 giofranchi

-

SharperDingaan, You already know that I don’t agree... right? ;D ;D Anyway, I thank you and all the members of this board for your deep thinking and well thought-out analysis! But… please, don’t miss the forest for the tree… Maybe, it is just me, who doesn’t think and analyze deeply enough… yet, I always try to keep in mind Mr. Buffett’s definition of the best among businesses: Profitable underwriting + float managed on a value basis = Mr. Buffett’s definition of the best among businesses. And with FFH today you can buy Mr. Buffett’s definition of the best among businesses at BV. Now, imo that is the forest! Then, I am sure there are a lot of “terrifying trees” and there will be some trouble down the road… But I am not smart enough to predict it, or when it will occur. I am content enough with a clear picture of the forest: a wonderful business, a wonderful management, a wonderful price. We will see! giofranchi

-

This is the irony I am seeing. These guys are wonderful equity investors and just a few years ago I was reading that their lifetime return on equities was 17% annualized. One who looks at safety first and return second, isn't satisfied with this performance and would choose to add the risk of insurance operation to get better results? Myself, I'm guilty as charged and would do the same, but I wouldn't claim that it reduces my risk. I would call this looking at growth at the expense of some additional calculated risk. I'm of the opinion that an unlevered fund is safer than a levered one, even if that leverage be from insurance. There was a little bit of a scrape they got into ten years ago that suggests I'm right about this. Then of course Berkshire was run at the risk of permanent 100% capital loss for years before Buffett woke up to the risk of terrorists -- history could be written differently and Berkshire could be a zero today. He might have had a long string of wonderful results followed by a zero. Fortunately, he realized his blind side and nothing terrible ever came to pass. More recently he claims that his operation was last in a line of dominoes (financial crisis) that would have fallen if the government hadn't acted in 2008. Sorry Eric, But I don’t quite agree with this also… Equity investing and insurance underwriting have a lot in common. Those who are successful in investing usually possess the right mental attitudes and skills to be successful in insurance too. They know how to be opportunistic, how to look for neglected markets, how to recognize and take advantage of other people’s errors, and they know how to wait for the odds to be disproportionately stacked in their favor, then invest aggressively or write a lot of premiums. They also understand cycles, or the importance of the “pendulum”, paraphrasing Mr. Marks. So, I see insurance underwriting basically as “diversification”, or the opportunity to employ their skills in a slightly different and mostly uncorrelated business. I agree that diversification in not always good, but FFH’s insurance management, led by Mr. Barnard, has by now become one of the most experienced in the world. And I really don’t see them making too many serious mistakes going forward. Instead, they will take pressure off the shoulders of the HWIC: clearly, it has been 3 years they don’t want to be aggressive in equity investing, right? Well, thanks to insurance they can afford that luxury, without compromising long term performance. And that’s safety imo: they can afford to swim against the current, or hold their stance against the market, for much longer than any mutual or hedge fund. They are free to change their mind only when the facts change, not when the pressure becomes unbearable. giofranchi