Blake Hampton

-

Posts

295 -

Joined

-

Last visited

Content Type

Profiles

Forums

Events

Everything posted by Blake Hampton

-

I was reading BRK shareholder letters when I had a thought: Since unrealized investment gains are now included in net income, wouldn’t that mean that the S&P 500’s EPS is overstated? Buffett has repeatedly explained since 2017 how Berkshire’s reported net income isn’t actually representative of its earnings. In a rising market, wouldn’t this then have the same effect with the S&P? It’s sort of hard to wrap my head around but I feel like appreciation in stocks generally would then show up in the earnings of companies. Edit: The change was ASU 2016-01

-

I wanted to ask at what point do you think that a company’s management is adequate enough to buy a stock. I feel like I’m constantly seeing a large amount of undervalued companies with the caveat being managements that refuse to return any money to shareholders. I’m starting to think that this could possibly be the most important aspect of what differentiates a good investment from a bad one. I really want to emphasize just how many managements I see that refuse returning any money, it’s crazy. I’m assuming that it’s from a standpoint of preserving their job but isn’t their job to ultimately increase shareholder value? Where are the directors in this situation? Maybe this is why Buffett only wants to buy good business. With bad businesses, they just sit there and preserve capital when they shouldn’t. Companies like Coke don’t have that same worry.

-

Just out of curiosity, is there a way to bet on oil volatility?

-

So with this deficit thing, we are essentially selling our wealth in return for consumption right? Is that how that works? I’ve also heard talk of a possible fiscal crisis where people could possibly start dumping treasury bonds. I’m interested if anyone has any insight on this.

-

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

The FED posts these monetary policy updates for Congress twice a year. https://www.federalreserve.gov/publications/files/20240301_mprfullreport.pdf -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

Thought some of you might find this great @wabuffo post interesting. The next chart is after the GFC, when spending ramped up in response to the crisis, "money supply" increased 17% per year from mid-2008 to the end of 2012. Gold responded to this as well. Now the relationship between money supply growth and asset inflation (or gold) isn't linear or perfect so its not a perfect "hard and fast" rule. But I think the general relationship makes sense to me as the supply of new gold mined every year is around 1.8% of the above-ground gold inventory. Gold's monetary attribute is stability since it grows very slowly. This is also what Bitcoin is trying to do - grow supply at 2% per year (like gold). My guess is that the reason gold is jumping again since early December is because it is starting to "feel" the effect of this second round of stimulus that has begun this week and will start to appear in the US Treasury spending numbers in January. FWIW, wabuffo -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

I have a couple of questions for anyone willing to answer: Do you think that short-term treasury bills are a good inflation hedge? What are some future implications of deficit spending and how would they coincide with higher long-term interest rates? -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

I want to quickly mention that @Dinar corrected me by saying that using the growth rate in nominal GDP is more accurate than real. I'm glad he did because it cleared a lot of things up for me. In the past, Buffett mentioned that corporate profits should average out at about 6% of GDP over time. We've seen them increase up to around 10% of GDP starting from right before the financial crisis all the way up until now. I don't have any great insight on what is happening there but I do know that it has caused earnings growth to outpace GDP growth. Essentially money has flowed from other parts of our economy into company earnings. I still think though that using that long-term average for nominal GDP growth is the right way to go. Of course I could always be wrong. -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

You're right, thanks for correcting me. Still though by Bogle's valuation standard, the market comes out to be significantly overvalued. -

This was a great summary and I guess in the end, it all comes down to perspective. I haven't read the book but do you mind explaining the context behind "His dad is a monster."

-

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

We desperately need an undo button. I just accidently deleted a long written response and I now want to kms. Anyway, my response was formed around how there is currently a spread between bank reserves and the recorded assets on the FED's balance sheet. I believe that this is cash that has made its way into the economy through asset inflation. By buying bonds and injecting cash, the FED essentially made owning assets more attractive relative to fixed-income and cash, especially when you consider how low rates were and for how long they stayed there. I do agree though that it ultimately comes down to bank reserves. I think that the biggest focus during QT is gonna be watching reserves as they let the bonds run-off. I'm sure they don't want to put banks in a precarious situation. -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

GDP growth has averaged around 2% over the last 10-20 years and 3% preceding that. I think 2% is a good average for growth going forward. I recently listened to an interview with John Bogle in 2017 where he explained his valuation model using dividends. He used the S&P500's dividend yield and 5% growth going forward. Funnily enough, the dividend for the S&P is approximately its net earnings - capex, so it's almost the same as owner earnings. Anyway, I redid his recommended model for dividend growth and got nearly the same results as my model with earnings. Sources: S&P500 Results - it's a spreadsheet btw John Bogle Interview -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

I believe that the valuations for almost everything are simply absurd right now. The median home sale price is 6x the median household income. The S&P500 is set to return approximately 5-5.5% at current prices. This is assuming 2% earnings growth and that corporate taxes stay at 21%. A higher growth rate is certainly possible but so are higher corporate taxes, arguably more so. The point here is that you can get this same yield with cash, and this is without any of the added risk. -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

My idea of the two options at the FED: Shrink the balance sheet and cripple markets Or don't and we see runaway inflation Please correct me if I'm wrong -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

Isn't QE simply an asset swap of long-term bonds for cash, with QT being the reverse? The Federal Reserve's balance sheet has shrunk by around $1.2 trillion in assets since last year and is continuing, and I don't see how this doesn't affect asset prices. The system is currently tightening and we'll almost certainly see higher long-term rates in the near future. It's interesting to me because when I talk to anyone about the value behind both stocks and real estate, it seems they believe that prices just have to continuously go up. Looking at past data, this seems somewhat more true for real estate but certainly not equities. -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

Why? -

How is the Fed going to cut rates with inflation over 3%?

Blake Hampton replied to ratiman's topic in General Discussion

Does anyone here think that QT will have a big effect on markets? I would think higher long-term rates might cause a lot of damage. -

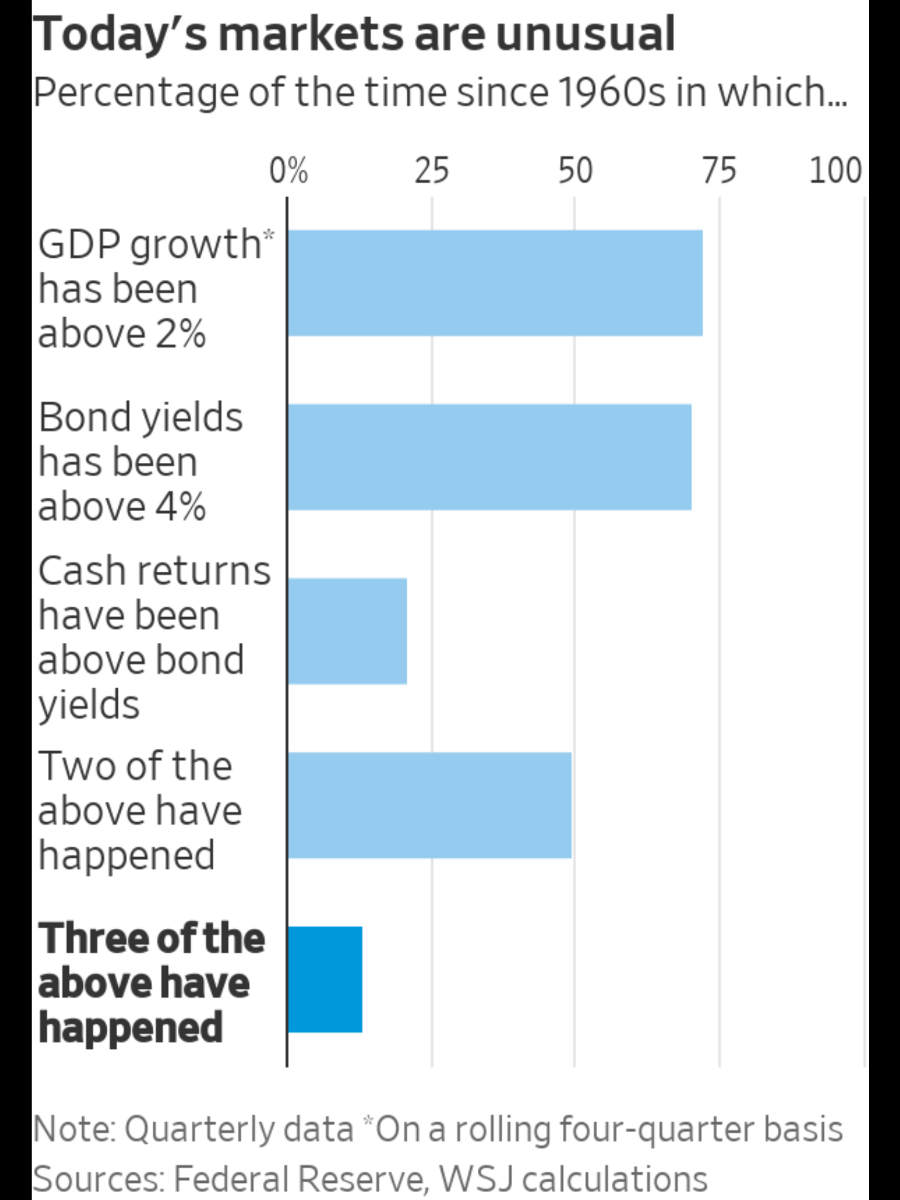

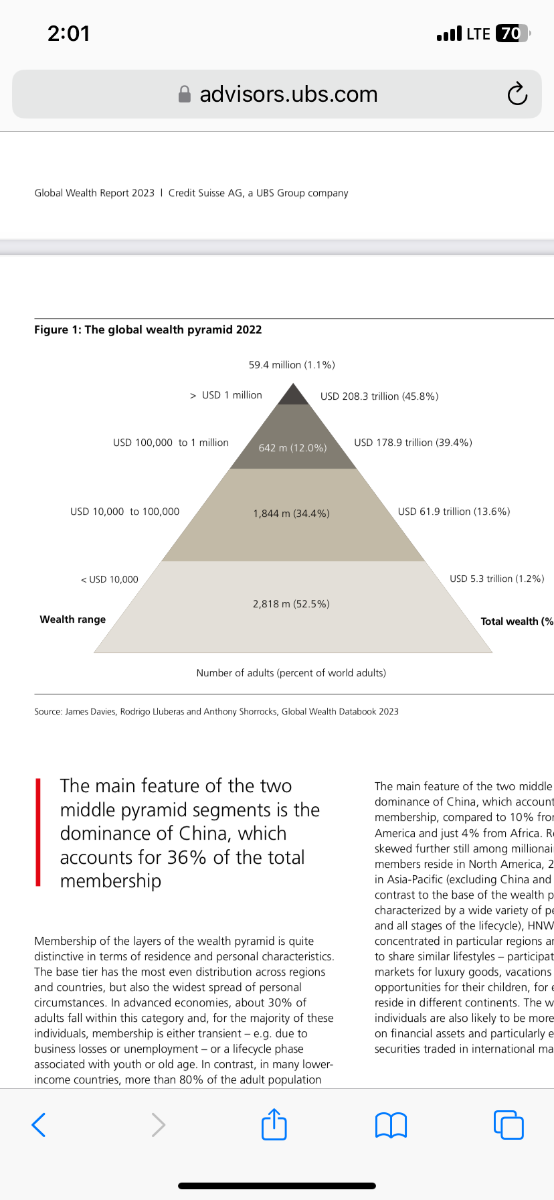

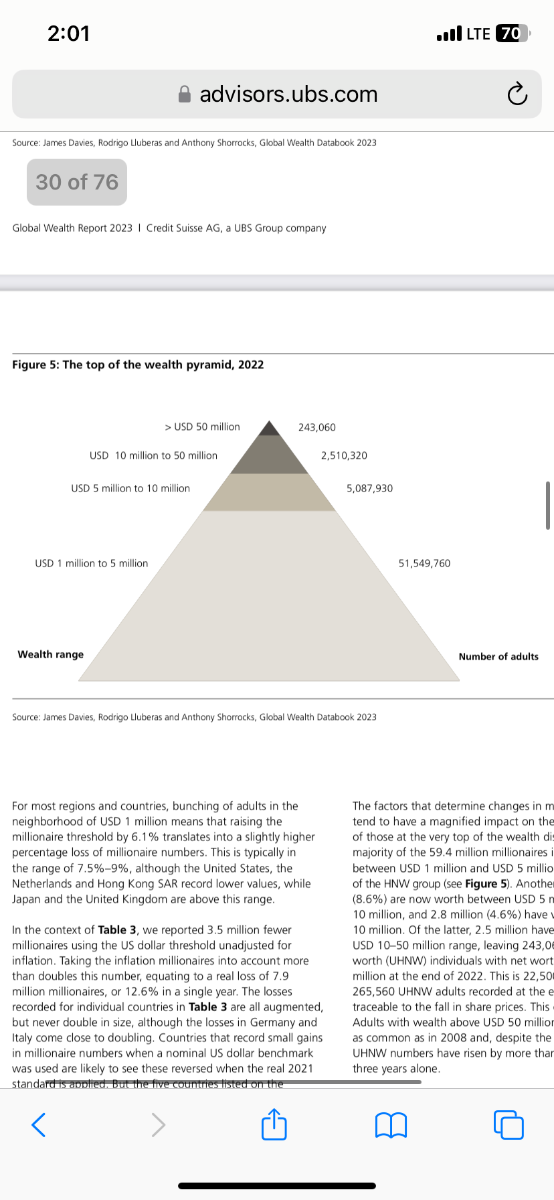

I saw the threads about movies and podcasts, and thought it might be interesting to create a thread centered around any business reading material. If you find anything interesting that you would like to have others read and discuss, drop a link or pdf with a title, and possibly a description, so that others might know what they're clicking on. I'll list a few that I've found lately: Transcript of Interview With Warren Buffett, May 26, 2010 - Interview detailing Buffett's reflection on the financial crisis The Truth About Diversification by the Numbers.pdf - Diversification study Global Wealth Report 2023.pdf - Title Long-Term Asset Return Study 2020.pdf - Title

-

Approximate % Change From 2019 - Price of the S&P 500: 58% - M2 Money Supply: 36% - Earnings of the S&P 500: 34% - Median home price: 28% - Inflation: 21% - Median household income: 12% I thought to make a list of these items, and their respective changes before money printing, to lay out a picture of how the economy has responded since the pandemic. In my mind, all of these items should match the increase of the money supply but I also understand that the dispersion isn't going to be equal. Shouldn't we see them equal out over time though? Wont we see a reversion to the mean? This data tells me that we haven't seen the end of inflation and that household incomes haven't kept pace with really anything else. I also thought it might be interesting to think about company earnings and if they are generally quicker to revert than incomes. It seems unfair but so is the world.

-

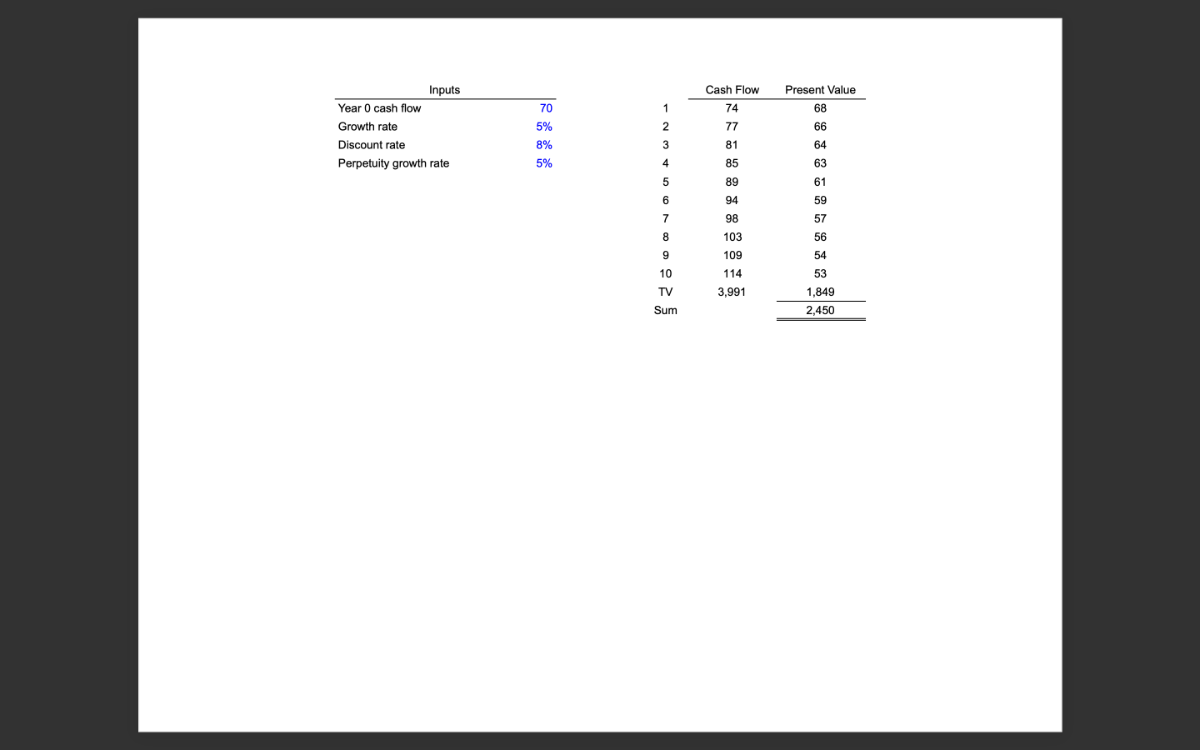

This is my crude valuation of the S&P500. I took the TTM dividend and put in a long-term average of 5% for dividend growth. Funnily enough, the S&P500 dividend is roughly the difference between its net earnings and capital expenditures. My discount rate is debatable, but I did a lot of thinking and concluded that 8% was a solid number. Please destroy it and prove me wrong.

-

Also curious on which steps in the process you guys find to be the most important

-

I'm trying to conceive of a mental model for investment, my overall goal being to build my strategy around it. I've already thought of a simple model for personal finance that is earn, save, and invest. I like to occasionally break down things further so that I can focus more on specific concepts within each group. So far for my invest group I've come up with Idea generation, research and valuation, position sizing, and monitoring, I've laid them out in their general order of operations. I was curious if you guys have any similar models and also if I'm missing anything on the ones I'm working with so far. Rest in peace Mr. Munger

-

-

What an incredible response

-